8K TV Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

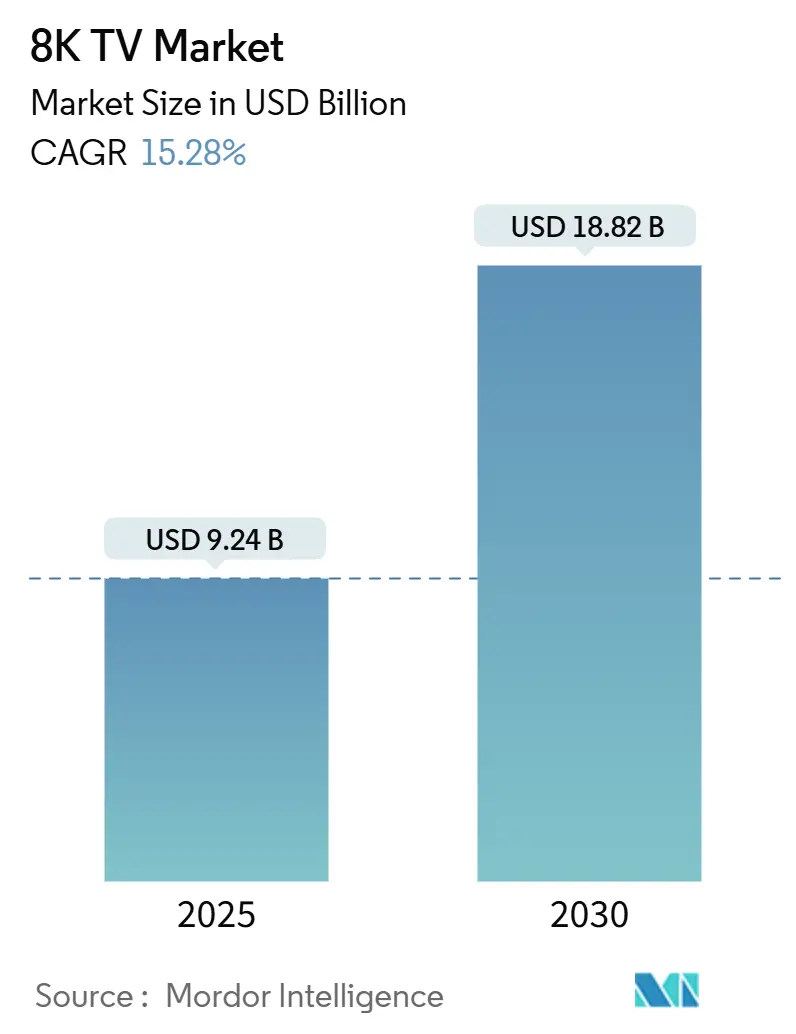

| Market Size (2025) | USD 9.24 Billion |

| Market Size (2030) | USD 18.82 Billion |

| Growth Rate (2025 - 2030) | 15.28% CAGR |

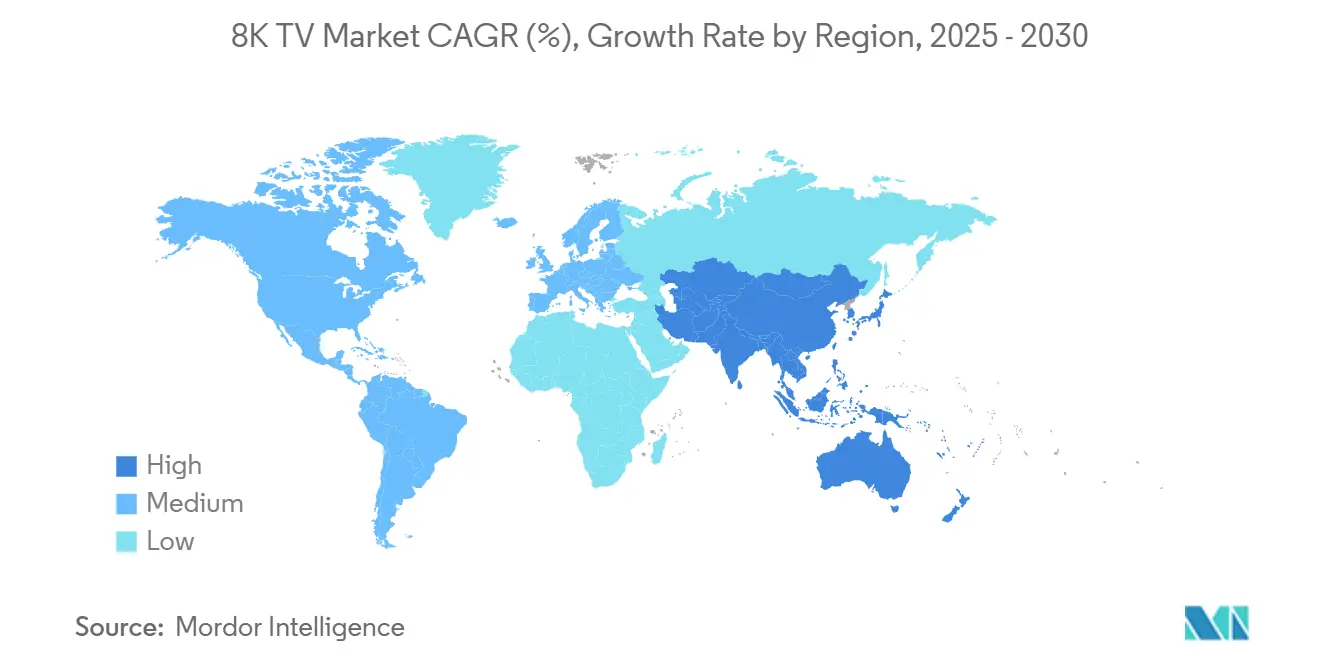

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

8K TV Market Analysis by Mordor Intelligence

The 8K TV market size was USD 9.24 billion in 2025 and is projected to reach USD 18.82 billion by 2030, growing at a 15.28% CAGR over the forecast period. The 8K TV market is expanding as panel makers leverage Gen 10.5 fabrication to lower production costs, television brands refine AI-based upscaling engines, and regional governments run ultra-high-definition broadcast pilots in Japan and South Korea. Samsung Electronics continues to lead the 8K TV market with its QN990F and QN900F Neo QLED lines, while LG Electronics’ strategic pullback and Sony’s exit in April 2025 underscore the segment’s reliance on a small pool of premium vendors. Content scarcity, limited residential bandwidth, and the European Union’s 2024/1781 Ecodesign rule on energy labeling remain material headwinds, yet affluent households and commercial venues still value 8K resolution for prestige installations. Momentum in the 8K TV market is therefore shaped by falling panel prices, premiumization trends across North America, Europe, and the Middle East, as well as sustained marketing investments by the dominant brands.

Key Report Takeaways

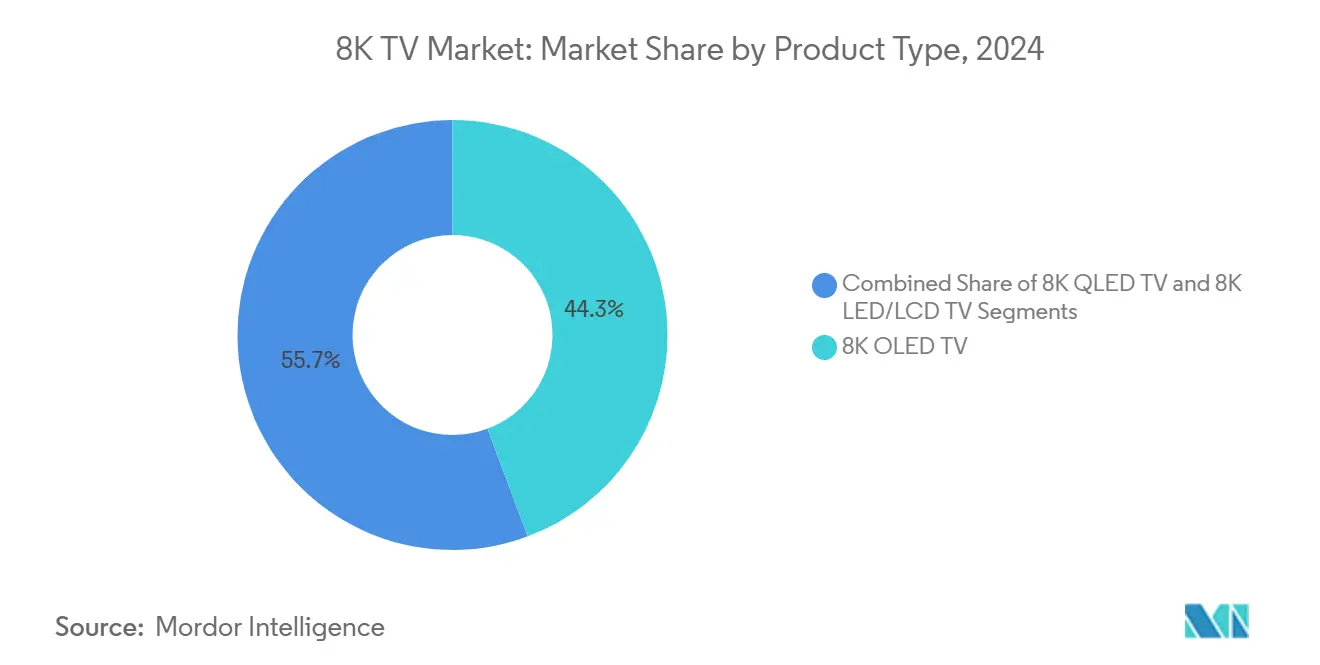

- By product type, 8K OLED televisions led the 8K TV market with a 44.3% revenue share in 2024, while 8K QLED units are projected to achieve a 17.12% CAGR through 2030.

- By screen size, the 66–75-inch class captured 53.8% of 2024 sales of the 8K TV market, whereas the 76-inch-and-above category is forecast to expand at a 17.31% CAGR.

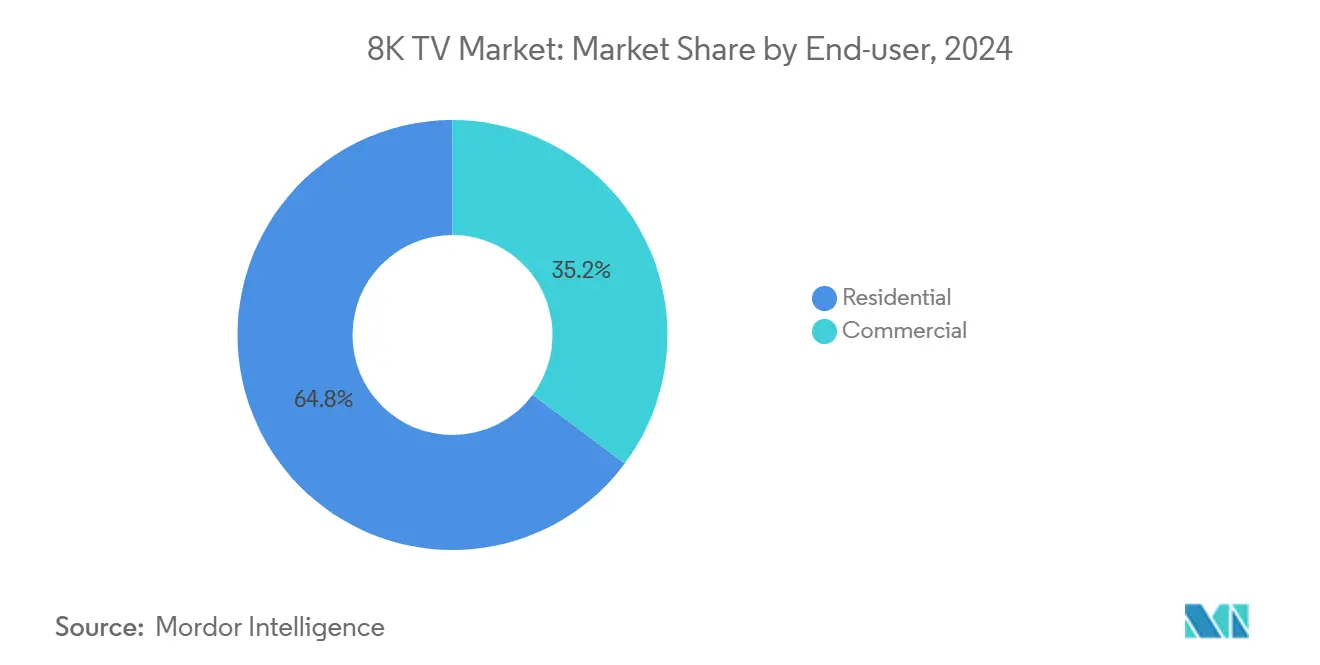

- By end user, household buyers commanded 64.8% of the 2024 revenue in the 8K TV market, while commercial installations are poised for a 17.07% CAGR through 2030.

- By distribution channel, offline retail secured 57.82% of the 2024 revenue of the 8K TV market, but online platforms are expected to grow at a 16.91% CAGR.

- By geography, the Asia-Pacific region dominated the 8K TV market, accounting for a 52.22% market share in 2024, and is projected to grow at an 18.09% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 8K TV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 8K streaming content and upscaling technologies | +3.2% | Japan, South Korea, North America, global spillover | Medium term (2-4 years) |

| Falling 8K panel production costs due to Gen 10.5 fabs | +2.8% | Asia-Pacific core, Europe and North America spillover | Long term (≥ 4 years) |

| Premiumization trend among high-income consumers | +2.5% | North America, Europe, UAE, Saudi Arabia | Short term (≤ 2 years) |

| Intensifying marketing push by TV OEMs and content platforms | +2.1% | Global | Short term (≤ 2 years) |

| Government incentives for ultra-HD broadcasting pilots | +1.9% | Japan, South Korea, select EU members | Medium term (2-4 years) |

| Rise of 8K TVs as digital art and NFT display surfaces | +1.4% | Major urban centers worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 8K Streaming Content and Upscaling Technologies

AI-based processors, such as Samsung’s NQ8 AI Gen3 and MediaTek’s Pentonic 2000, now interpolate 4K or 1080p inputs into a 7680 × 4320 resolution in real-time, narrowing the perceptual gap with native 8K footage.[1]Samsung Electronics, “QN990F Neo QLED 8K TV Specifications,” samsung.com Upscaling is essential because YouTube hosts fewer than 10,000 native 8K clips, and premium services like Netflix or Disney+ have yet to launch 8K tiers. NHK’s BS8K channel demonstrates that continuous 8K broadcasting is viable; however, the high costs of infrastructure and cameras hinder its global replication. As a result, upscaling technology sustains the 8K TV market by maximizing value from existing 4K libraries. Early adopters in luxury homes, gaming setups, and corporate showcase rooms increasingly treat AI upscaling accuracy as a key purchase criterion. Consequently, chipset innovation remains a primary differentiator among flagship models.

Falling 8K Panel Production Costs Due to Gen 10.5 Fabs

Gen 10.5 fabs cut ten 75-inch or six 85-inch screens from a single glass sheet, trimming per-unit costs for large panels. BOE’s Hefei and Wuhan lines feed TCL and Hisense, while Samsung Display and LG Display favor QD-OLED or WOLED pathways.[2]BOE Technology Group, “Gen 10.5 Fab Investor Deck,” boe.com Yields, however, still lag those of 4K lines, and advanced driver ICs add 15-20% to bills of material. Sharp’s Sakai Gen 10 plant produced 70-inch 8K panels priced under USD 3,000 in 2024, signaling margin pressure but also hinting at mid-term affordability gains. Once yields converge with 4K benchmarks, expected after 2027, the 8K TV market could benefit from sharper pricing and a broader model portfolio. Until then, Gen 10.5 economics primarily assist premium-tier SKUs, sustaining ASPs well above mainstream 4K equivalents.

Premiumization Trend Among High-Income Consumers

Affluent buyers in the United States, Germany, the United Arab Emirates, and Saudi Arabia continue to treat 8K displays as status symbols. Samsung’s 98-inch QN990F retails at USD 40,000 and is often found in private theaters and penthouses, while LG’s 75-inch QNED99, at USD 6,500, caters to buyers who value screen area over OLED contrast. Luxury hotels in Dubai and Singapore are adding 85-inch 8K screens to their suites, leveraging the wow factor to justify premium nightly rates. For these customers, the resolution headline acts as a lifestyle signal rather than a pure functional upgrade. Limited mid-tier offerings mean the 8K TV market remains disproportionately dependent on discretionary income groups, reinforcing premiumization as both driver and constraint.

Intensifying Marketing Push by TV OEMs and Content Platforms

Samsung and LG invested heavily in the CES 2024 and CES 2025 show floors, highlighting HDMI 2.1 gaming, AI upscaling, and smart-home integration. Samsung’s 8K Universe app curates roughly 500 demo clips, while TCL and Hisense target cost-sensitive early adopters with 75-inch 8K sets priced near USD 2,500. Consumer awareness, however, lags investment: Sony’s April 2025 withdrawal signaled that even tier-one brands question short-term returns. Marketing efficacy hinges on credible 8K content commitments from major video platforms and on-premise demonstrations that showcase the step-up from 4K. Effective campaigns temporarily stimulate spikes in sell-through but cannot fully offset the structural content gap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited native 8K content availability | -2.9% | Global | Medium term (2-4 years) |

| High retail prices compared to 4K | -2.3% | Worldwide, acute in price-sensitive markets | Short term (≤ 2 years) |

| Bandwidth bottlenecks in residential networks for 8K streaming | -1.8% | Emerging markets, rural areas | Medium term (2-4 years) |

| Post-pandemic shift to portable devices | -1.2% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Native 8K Content Availability

Fewer than 10,000 native 8K videos reside on YouTube, and no major subscription streamer offers an 8K tier as of late 2025.[3]YouTube, “8K Video Support FAQ,” youtube.com NHK alone broadcasts continuous 8K, delivering around 12 hours daily, but only within Japan. Netflix abandoned its commercial 8K rollouts after bandwidth tests showed that residential fiber averages were below the 50–100 Mbps needed for 60 fps 8K delivery. Hardware makers thus rely on AI interpolation, a stopgap that fails to satisfy purists hunting for true 33-megapixel footage. Surveys show that over 60% of U.S. consumers cite content scarcity as the main deterrent to purchasing an 8K set, which limits the near-term upside of the 8K TV market.

High Retail Prices Compared to 4K

A 75-inch 8K QLED costs USD 2,500–3,500, which is double the price of a comparable 4K model. Meanwhile, Samsung’s 85-inch QN900F, priced at USD 8,500, carries a 2.5-times markup compared to LG’s 83-inch C3 OLED 4K screen. Advanced driver ICs, lower yields, and mini-LED arrays inflate bills of material. In India, Brazil, and Nigeria, 8K TVs are rarely found on shelves because 4K remains the aspirational standard. Chinese challengers sell 75-inch 8K units at USD 2,100, yet they still struggle against premium 4K sets that offer superior HDR and app ecosystems. Without a cost breakthrough, the 8K TV market stays skewed toward buyers immune to price shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: OLED Leadership Faces QLED Momentum

8K OLED models claimed 44.3% of revenue in 2024, driven by LG’s 77-inch and 88-inch Z2 offerings, which deliver pixel-level dimming and near-infinite contrast. These sets command premiums because WOLED production at 8K density remains yield-challenged. Meanwhile, 8K QLED televisions, equipped with quantum-dot filters and mini-LED backlights, are projected to surge at a 17.12% CAGR, the highest among product categories. Samsung’s Neo QLED architecture surpasses 3,000 nit peak brightness, attracting buyers in brightly lit commercial spaces. 8K LED/LCD models play the value card but suffer color gamut and black-level limitations that blur differentiation from top-end 4K QLED alternatives. The 8K TV market size tied to QLED is therefore expanding the fastest, even if OLED still holds a share at the ultra-premium tier. Over time, panel makers expect mini-LED cost compression and Gen 10.5 capacity to sharpen QLED’s value proposition, potentially eroding OLED’s share once brightness and burn-in risk are no longer a concern, as absolute black levels become less important.

The sustainability of OLED’s advantage hinges on material innovations that lower defect rates and enhance the longevity of blue subpixels. If tandem-stack OLED structures arrive before 2027, LG could protect margins despite QLED’s brightness lead. Conversely, should QLED brands integrate even finer local-dimming zones and adopt quantum-dot color-conversion layers, mid-decade shipments may realign in favor of QLED. The interplay between manufacturing yields, backlight evolution, and chipset roadmaps will dictate whether OLED retains command of the 8K TV market share or cedes ground to QLED contenders.

By Screen Size: Large-Format Sets Command Growth

Panels measuring 66–75 inches accounted for 53.8% of 2024 revenue, striking a balance between living-room compatibility and immersive scale. Retail prices averaging USD 3,000 for a 75-inch 8K QLED attracted early adopters keen on flagship specifications. The 76-inch-and-above cohort, however, is forecast to accelerate at a 17.31% CAGR, driven by hospitality and corporate demand for large-scale displays. Samsung’s 98-inch QN990F and TCL’s 115-inch X955 Max headline this push, reinforcing the premium size tied to the 8K TV market, particularly for very large panels. Buyers in luxury hotels and executive briefing centers view these screens as digital canvases for branding and virtual conferencing.

Conversely, sub-65-inch 8K models struggle because the human eye cannot resolve 33-million-pixel counts from typical sofa distances. Sharp’s 60-inch Aquos 8K found limited takers after consumers favored premium 4K OLEDs at lower price points. The screen-size stratification illustrates a bifurcated 8K TV market: mass-market volumes remain anchored in 65-inch 4K sets, while ultra-large 8K screens chase high-margin verticals. Unless cost curves flatten dramatically, 8K will likely remain synonymous with displays 75 inches and larger, reinforcing differentiation through scale rather than resolution alone.

By End-user: Commercial Venues Outpace Home Theaters

Households still generated 64.8% of the 2024 8K revenue, but commercial installations, spanning hotels, corporate boardrooms, and public venues, are expected to compound at 17.07% through 2030. Hospitality pioneers in Dubai and Singapore mount 85-inch Neo QLED units in suites to elevate guest perception. Corporations retrofit executive centers with 8K screens to visualize big-data dashboards and host immersive telepresence sessions via HDMI 2.1 bandwidth. Museums and airports deploy 8K signage for art exhibits and way-finding, though content playback hardware remains costly. As a result, the 8K TV market share mix shifts gradually toward commercial buyers who amortize display costs over branding or visitor-experience returns.

Residential growth slows as streaming time migrates to portable devices and smart projectors. Yet high-income consumers continue to integrate 8K TV walls within dedicated cinemas and loft apartments. Market expansion in either end-user camp will depend on native content rollouts and improved compression standards, such as Versatile Video Coding (H.266), that reduce bit-rate burdens without visibly compromising picture quality.

By Distribution Channel: E-Commerce Scales but Stores Retain Primacy

Brick-and-mortar chains delivered 57.82% of 2024 8K turnover, driven by interactive demos at Best Buy, Yodobashi Camera, and MediaMarkt. Trained sales staff walk prospects through AI upscaling demos and gaming latency tests, offering confidence on five-figure purchases. Yet online sellers are projected to log a 16.91% CAGR to 2030, buoyed by Amazon, JD.com, and brand-owned web shops that bundle white-glove delivery and installation. Reviews and comparison matrices reduce information asymmetry, while same-day shipping narrows the experiential gap.

E-commerce excels in price transparency and flash-promo mechanics that coax fence-sitters into making a purchase. Physical retailers counter with curated in-store experiences that spotlight 8K differentiators over commoditized 4K lines. The 8K TV market thus maintains a hybrid distribution pattern, where big-ticket flagships are often sold inside showrooms, but mid-premium SKUs are increasingly transacted online once buyers trust logistics and support processes.

Geography Analysis

The Asia-Pacific region owned 52.22% of 2024 sales and is forecast to grow at an 18.09% CAGR, the fastest regional growth rate in the 8K TV market.[4]NHK, “BS8K Broadcast Overview,” nhk.or.jp China’s BOE, CSOT, and Tianma shipped more than 60% of the global 8K LCD panels, allowing TCL and Hisense to price 75-inch 8K sets at USD 2,000–2,500 domestically. Japan’s NHK maintains the only continuous 8K broadcast channel worldwide, although the high cost of set-top boxes and limited catalog depth hinders uptake. South Korea’s premium consumer segment drives 8K penetration to surpass 5% of domestic TV sales, reflecting brand loyalty toward Samsung and LG. India, Australia, and Southeast Asian nations lag in terms of price sensitivity and fiber under-penetration, but they represent latent upside once yields compress and localized content becomes available.

North America generated roughly one-quarter of global 8K revenue in 2024. U.S. households in California, New York, and Texas adopt early thanks to gigabit fiber footprints and higher disposable incomes. Samsung leads in retail footprints through Best Buy and its direct e-commerce storefronts, while Canada’s smaller population and duty structure dampen sales volume. For North America, progress will track streamer commitments to native 8K tiers and ISPs’ willingness to guarantee 100 Mbps pipes. Without those enablers, the 8K TV market’s ceiling remains constrained to luxury segments.

Europe accounted for approximately 18% of 2024 sales, with Germany, the United Kingdom, and France favoring energy-regulated sets that comply with the EU’s Ecodesign framework. LG’s QNED99 meets mandatory efficiency standards through adaptive brightness modulation, giving it an edge among eco-minded buyers. Italy and Spain lag in per-capita income and living-space size, stunting 8K uptake. The Middle East, by contrast, relies on mega-projects in Riyadh and Dubai, where displays measuring 85 inches or larger serve as luxury amenities. Africa and Latin America remain niche markets, with South African and Brazilian retailers positioning 8K as special-order items only.

Competitive Landscape

The 8K TV market features moderate consolidation, with Samsung Electronics, LG Electronics, and TCL Technology Group collectively holding a share of just over 60% in 2024. Samsung enjoys vertical integration across QD-OLED and mini-LED panels, semiconductor NPU design, and the Tizen OS, creating cost and feature moats. LG maintains a minimal presence with the QNED99 LCD after shelving its fresh 8K launches to prioritize OLED and QNED 4K. Sony’s April 2025 withdrawal underscores skepticism around near-term demand. Chinese players TCL, Hisense, and Xiaomi pursue share through aggressive pricing, sourcing panels from BOE and CSOT at discounts of 20–25% to Korean OLED or QD-OLED units.

Technological differentiation centers on AI upscaling silicon, where Samsung’s 512-core NQ8 AI Gen3 and MediaTek’s Pentonic 2000 duel for perceptual supremacy. Samsung filed more than 200 patents on 8K upscaling and backlight control between 2023 and 2025, reinforcing its innovation lead. Market entry barriers remain high as fabs cost billions and brand equity influences risk-averse premium buyers. However, Xiaomi’s ecosystem integration with smart home devices offers a potential disruptor narrative, especially in Asia. Looking ahead, consolidation could intensify if panel economics fail to improve and if microLED or rollable OLED steal R&D budgets, forcing lagging brands to exit.

8K TV Industry Leaders

Samsung Electronics Co., Ltd.

LG Electronics Inc.

Sharp Corporation

Sony Group Corporation

TCL Technology Group Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sony Group Corporation withdrew from 8K, dropping Bravia 8K SKUs to redirect resources toward OLED and mini-LED 4K lines.

- March 2025: Samsung unveiled the QN990F Neo QLED 8K range, featuring a 512-core NPU, 2,048 dimming zones, and prices ranging from USD 8,500 to USD 40,000.

- February 2025: LG confirmed it would carry over the QNED99 8K LCD without refreshing the lineup, citing demand weakness.

- January 2025: TCL showcased the 115-inch X955 Max 8K mini-LED set at CES 2025, priced at USD 20,000 and aimed at luxury venues.

Global 8K TV Market Report Scope

| 8K OLED TV |

| 8K QLED TV |

| 8K LED/LCD TV |

| 55 - 65 Inch |

| 66 - 75 Inch |

| 76 Inch and Above |

| Residential | |

| Commercial | Hospitality |

| Corporate | |

| Public Display |

| Online | |

| Offline | Consumer Electronics Stores |

| Hypermarkets and Supermarkets | |

| Specialty Retailers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product Type | 8K OLED TV | ||

| 8K QLED TV | |||

| 8K LED/LCD TV | |||

| By Screen Size | 55 - 65 Inch | ||

| 66 - 75 Inch | |||

| 76 Inch and Above | |||

| By End User | Residential | ||

| Commercial | Hospitality | ||

| Corporate | |||

| Public Display | |||

| By Distribution Channel | Online | ||

| Offline | Consumer Electronics Stores | ||

| Hypermarkets and Supermarkets | |||

| Specialty Retailers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the 8K TV market?

The 8K TV market size reached USD 9.24 billion in 2025 and is projected at USD 18.82 billion by 2030.

Which region leads global 8K TV sales?

Asia Pacific held 52.22% of 2024 revenue and is forecast to grow the fastest, at an 18.09% CAGR.

Why do many consumers hesitate to buy 8K TVs?

Limited native 8K content, high retail prices, and home-network bandwidth constraints dampen mainstream adoption.

Which product type will grow fastest through 2030?

8K QLED televisions are set for the highest CAGR at 17.12% as quantum-dot and mini-LED costs decline.

How are commercial buyers using 8K displays?

Hotels, corporate boardrooms, and museums deploy large 8K screens for premium guest experiences, data visualization, and digital art exhibits.

Which companies dominate the competitive landscape?

Samsung Electronics, LG Electronics, and TCL Technology Group together controlled just over 60% of global 2024 revenue.

Page last updated on: