5G Standalone Core Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

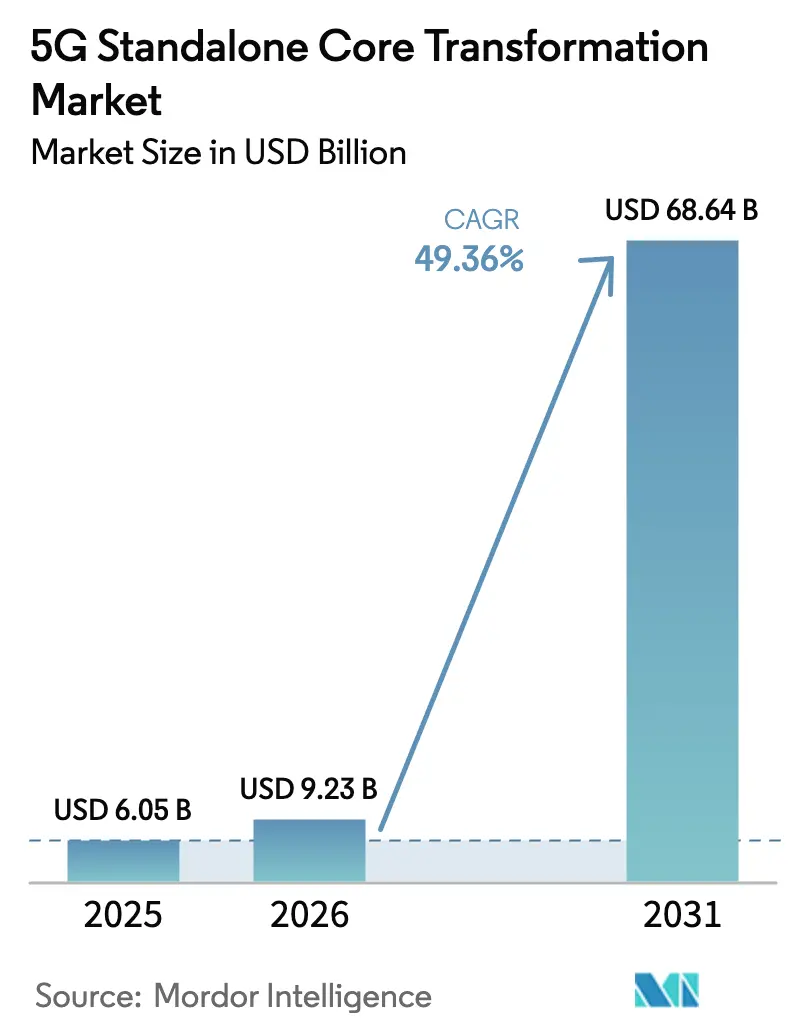

| Market Size (2026) | USD 9.23 Billion |

| Market Size (2031) | USD 68.64 Billion |

| Growth Rate (2026 - 2031) | 49.36% CAGR |

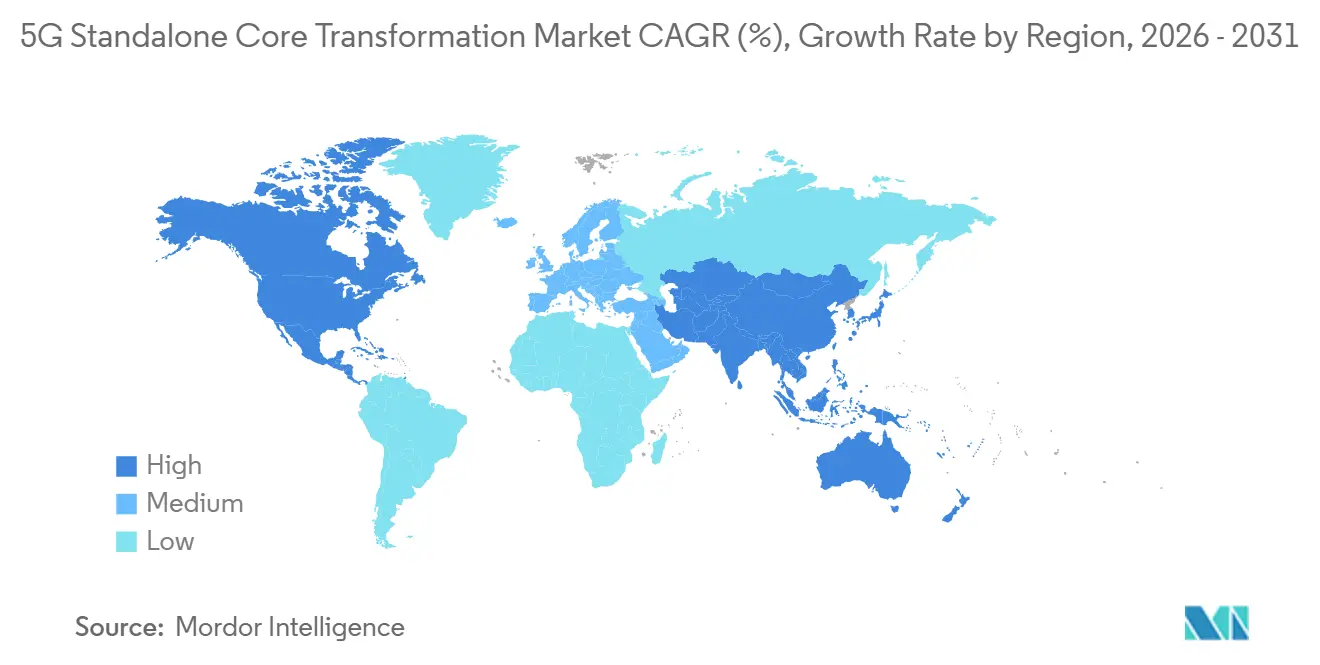

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

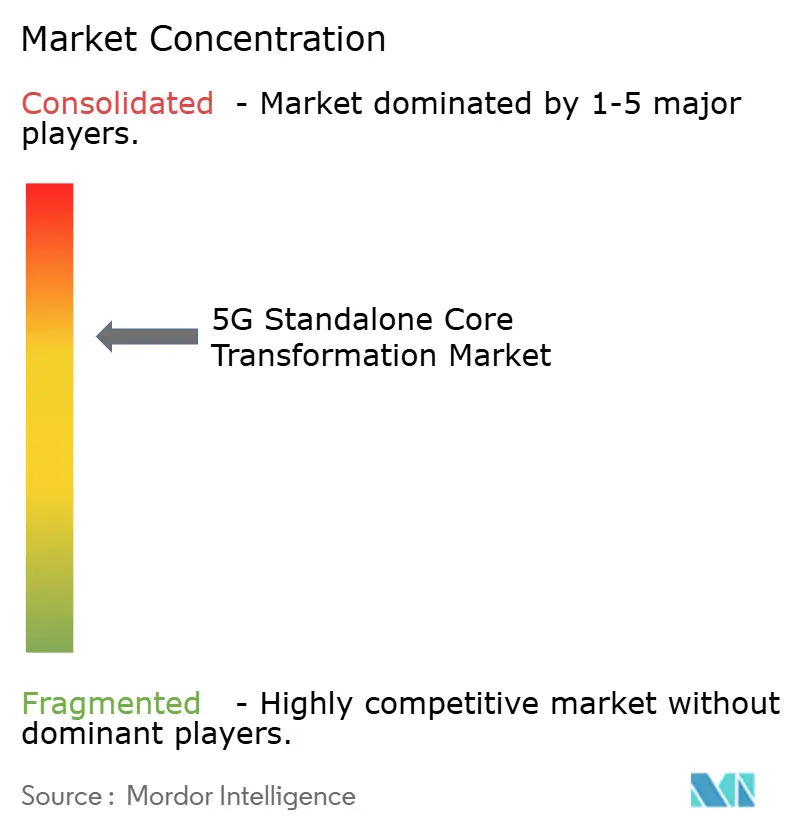

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Standalone Core Transformation Market Analysis by Mordor Intelligence

The 5G Standalone Core Transformation Market size is expected to increase from USD 6.05 billion in 2025 to USD 9.23 billion in 2026 and reach USD 68.64 billion by 2031, growing at a CAGR of 49.36% over 2026-2031. Rising operator migration from non-standalone architectures, expanding private network spend across Industry 4.0 sites, and hyperscaler alliances that shorten deployment cycles underpin this sharp trajectory. Cloud-native design unlocks network slicing, ultra-low latency, and edge-computing monetization, allowing carriers to retire duplicated evolved packet core resources and shrink signaling overhead. Public-sector incentives in the United States, China, India, and the European Union accelerate coverage in rural zones, while 3GPP Release 18 specifications simplify multi-vendor integration, encouraging tier-2 operators and enterprises to adopt API-driven solutions. At the same time, containerized network functions, RedCap-enabled mass-IoT modules, and AI-assisted slice orchestration expand the addressable revenue pool far beyond consumer mobile broadband, positioning the 5G standalone core transformation market for sustained double-digit growth.

Key Report Takeaways

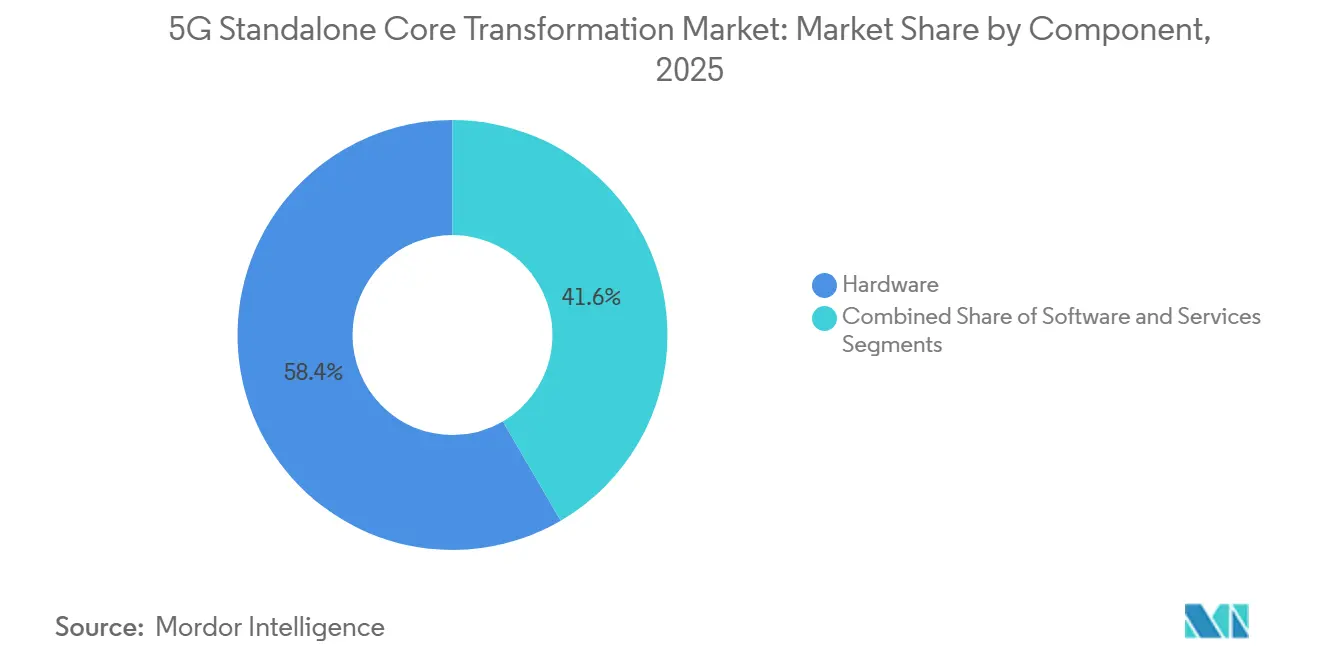

- By component, hardware led with 58.40% of the 5G standalone core transformation market share in 2025, while software is projected to expand at a 52.4% CAGR through 2031.

- By deployment model, public cloud captured 52.81% of 2025 revenue, whereas Hybrid/On-premises configurations are forecast to grow at a 53.1% CAGR through 2031.

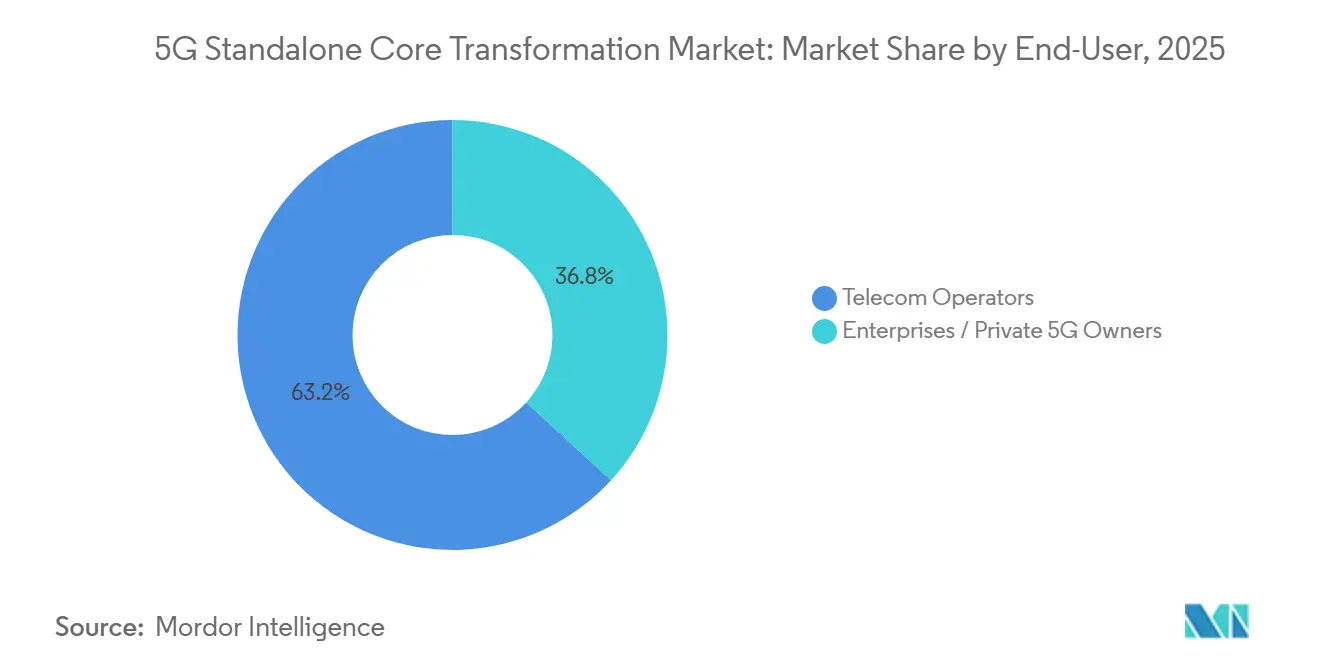

- By end user, telecom operators accounted for 63.20% of spending in 2025; Enterprises/Private 5G Owners are expected to grow at a 53.4% CAGR through 2031.

- By geography, North America commanded 40.03% of 2025 revenue, and Asia-Pacific is expected to register the fastest 54.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 5G Standalone Core Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Migration of Operators From NSA to SA Deployments | +12.5% | Global, with early momentum in Europe, Asia-Pacific, and North America | Medium term (2-4 years) |

| Government-Backed 5G Stimulus Packages and Spectrum Incentives | +11.2% | Global, led by North America and Europe tier-1 operators | Medium term (2-4 years) |

| Explosion of Private-5G and Campus Networks Across Industry 4.0 Sites | +10.8% | APAC core, North America manufacturing belt, Germany automotive corridor | Long term (≥ 4 years) |

| Cloud-Native, Containerised Network-Function Adoption by Tier-1 CSPs | +8.9% | North America, Europe, South Korea, Japan | Short term (≤ 2 years) |

| AI-Optimised Dynamic Network Slicing Commercial Pilots | +6.4% | North America (FCC/NTIA), China (MIIT), India (DoT), EU (EC) | Short term (≤ 2 years) |

| Emergence of RedCap Devices Unlocking Mass-IoT SA Traffic | +4.0% | Global, with early adoption in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Migration of Operators From NSA to SA Deployments

Operators are abandoning dual-core architectures because parallel maintenance inflates operating costs and blocks advanced features such as ultra-reliable low-latency communication and dedicated network slices. Commercial cutovers by Telia, Three UK, MTN South Africa, and O2 Telefónica during 2024-2025 validated the economic upside, with Telia reporting a 30% reduction in signaling overhead after decommissioning its evolved packet core. The Global Mobile Suppliers Association counted 181 operators investing in standalone infrastructure, up from 140 a year earlier. This migration unlocks network-as-a-service revenue, as enterprises lease guaranteed slices for mission-critical workloads unattainable under non-standalone constraints.

Cloud-Native, Containerized Network-Function Adoption by Tier-1 CSPs

Tier-1 carriers are re-platforming cores on Kubernetes to gain horizontal scaling and zero-downtime upgrades. Ericsson’s On-Demand core on Google Cloud spins up user-plane functions in under 60 seconds, helping operators scale capacity tenfold during peak events.[1]Ericsson, “Ericsson 5G Core Solutions,” ericsson.com Three UK operates a 9 Tbit/s core orchestrated by Red Hat OpenShift, serving 30 million subscribers with 40% fewer physical servers. O2 Telefónica colocated control-plane workloads on AWS Outposts in Frankfurt, trimming latency for automotive and industrial clients. These proofs confirm that containerization compresses service introduction cycles and reduces hardware intensity.

Explosion of Private-5G and Campus Networks Across Industry 4.0 Sites

Factories, ports, and mines prefer private standalone networks for deterministic performance and air-gapped security. Tesla’s Gigafactories stream high-definition machine-vision feeds at 120 frames per second on in-house cores. John Deere’s Iowa campus achieved 99.999% uptime for autonomous guided vehicles after the stand-up of a campus network. Airbus, Bosch, and Newmont report similar gains, with Ericsson finding that 70% of 40 audited private sites chose standalone cores to future-proof for edge computing.

AI-Optimized Dynamic Network Slicing Commercial Pilots

AI-driven orchestrators now tune slice bandwidth, spectrum, and compute in real time, replacing static templates. Vodafone UK offers a public-safety slice that guarantees sub-20 ms latency during disasters. Far EasTone predicts congestion 15 minutes in advance and pre-allocates spectrum using machine learning models. Ericsson’s automation suite cut slice-provisioning time from hours to minutes, making slicing a viable product rather than a laboratory demo.

Restraint Impact Analysis`*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Skills Gap for Cloud-Native 5GC Transformation | -6.2% | Global, acute in emerging markets and tier-2/3 operators | Medium term (2-4 years) |

| Inter-Operability Issues Across Multi-Vendor Cores and Legacy EPC | -4.7% | Global, particularly in operators with heterogeneous vendor ecosystems | Short term (≤ 2 years) |

| Elevated Cyber-Attack Surface in Service-Based Architectures | -3.1% | Global, with heightened concern in North America and Europe | Medium term (2-4 years) |

| Mid-band Spectrum Fragmentation Slowing SA Coverage Expansion | -2.8% | North America (C-band), Europe (3.5 GHz variations), fragmented Asia-Pacific allocations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Skills Gap for Cloud-Native 5GC Transformation

Standalone adoption demands new compute clusters, software licenses, and DevOps pipelines while certified Kubernetes engineers remain scarce. McKinsey pegged the total 5G spend at USD 400-500 billion, with core modernization accounting for up to one-fifth of that. Deloitte found 65% of surveyed operators cited talent shortages as the primary bottleneck. As smaller carriers turn to managed services, margin compression and slower customization follow.

Inter-Operability Issues Across Multi-Vendor Cores and Legacy EPC

RESTful APIs promise modularity, but version drift and proprietary extensions still trigger signaling faults. Dish Network spent six months debugging handovers across AWS, Mavenir, Nokia, and Samsung elements before commercial launch. O-RAN Alliance plugfests accelerate convergence, yet maintaining dual-core stacks during migration magnifies complexity. Without tighter 3GPP interface definitions, multi-vendor friction remains a hidden tax on transformation speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Overtakes Hardware in Growth Velocity

Hardware accounted for 58.40% of 2025 revenue, reflecting up-front purchases of x86 or ARM compute nodes, 100-gigabit switches, and RAN gear needed to host containerized functions. The 5G standalone core transformation market size for hardware is projected to grow steadily but cede share as value shifts toward orchestration intelligence. In contrast, software revenue is forecast to climb at a robust 52.4% CAGR, propelled by microservice licensing, AI-powered lifecycle automation, and continuous delivery. Operators deploying Ericsson Release 25A and Nokia MX Industrial Edge report weekly feature drops rather than quarterly code releases, demonstrating the speed premium of cloud-native stacks.

Service providers increasingly bundle consulting, integration, and managed operations alongside software. Oracle’s Communications Cloud Native Core lowered capital intensity by 30% for Vodafone and Telefónica by running on commodity gear.[2]Oracle, “Oracle Communications Cloud Native Core,” oracle.com VMware’s Telco Cloud Platform supplies the Kubernetes substrate that decouples vendor software from hardware, allowing carriers to negotiate favorable appliance pricing. As Release 18 hardwires open APIs, differentiation shifts from custom silicon to software agility, widening the performance gap between fast-moving container ecosystems and static appliance estates.

By Deployment Model: Hybrid Architectures Surge on Sovereignty Concerns

Public cloud absorbed 52.81% of 2025 spend because hyperscalers deliver infinite scale and global availability. O2 Telefónica’s AWS install and Three UK’s Google partnership illustrate how carriers extend coverage without standing up local data centers. Yet the 5G standalone core transformation market share for public cloud is projected to decline slightly as hybrid uptake accelerates. Enterprises in defense, finance, and healthcare favor on-premises or single-tenant edges for compliance. Tesla’s gigafactories house cores entirely on site to keep production telemetry internal.[3]Tesla, “Gigafactory Private 5G Network,” tesla.com

Hybrid deployments place user-plane functions near cell-site edges or within enterprise premises while keeping control-plane logic in public or private cloud. Nokia’s MX Industrial Edge, HPE Athonet, and Ericsson Edge Gravity collapse core, compute, and application hosting into a single rugged enclosure. With data-localization mandates tightening in India, Europe, and China, hybrid architectures are forecast to expand at a 53.1% CAGR, outpacing pure public installations as enterprises seek deterministic latency and regulatory peace of mind.

By End-User: Enterprises Accelerate Private-Network Investments

Telecom carriers remained the largest buyers, accounting for 63.20% of 2025 revenue as they overhauled national networks, monetized slices, and cut operating expenses. Yet enterprise demand is the faster-growing engine. The 5G standalone core transformation market size for factories, logistics hubs, and ports is projected to surge at a 53.4% CAGR, reflecting Industry 4.0 ambitions. Manufacturing plants rely on private cores to orchestrate robots and automated guided vehicles, slashing cycle times by up to 20%. Logistics operators such as DHL build campus networks to track forklifts in real time.

Bosch and Airbus demonstrate that latency-sensitive 8K video inspection, predictive maintenance, and AI analytics perform best on dedicated, air-gapped networks. Falling RedCap module prices enable thousands of sensors per site, expanding the addressable IoT footprint. As GSMA guidelines clarify spectrum licensing and security baselines, boardrooms that were formerly wary of telecom complexity now view private-network ownership as a strategic lever for uptime, data control, and a competitive edge.

Geography Analysis

North America generated 40.03% of 2025 revenue on the back of FCC rural-fund subsidies, NTIA Open RAN grants, and aggressive C-band rollouts that reached 200 million POPs. Verizon’s standalone cutover in Chicago and Dallas opened premium slices for industrial automation, while AT&T plans to decommission non-standalone anchors by late 2026. Canada auctioned 3.8 GHz spectrum and saw Rogers, Bell, and Telus pilot cores in Toronto and Vancouver, whereas Mexico’s Telcel and AT&T Mexico began trials in Mexico City and Monterrey. Strong capital markets, early access to spectrum, and proximity to hyperscale data centers position the region as a profitability leader.

Asia-Pacific is the high-growth engine, forecast to expand at a 59.6% CAGR through 2031. China’s 3.6 million base-station grid and MIIT mandate for standalone cores underpin explosive scale across 890 million subscribers. Japan’s nationwide launch by NTT Docomo, KDDI, and SoftBank leverages Ericsson, Nokia, and Samsung gear to service autonomous-vehicle and smart-factory clients. South Korea’s SK Telecom, KT, and LG U+ focus on AI-driven network slicing for automotive and cloud gaming, while India’s Reliance Jio covers 5,000 cities on a greenfield standalone architecture. Regional industrial policies, including India’s 6 GHz allocation and South Korea’s 5G+ roadmap, further lift demand for edge-enabled cores.

Europe trails North America and Asia-Pacific on an absolute scale, but benefits from coordinated spectrum policy under the EU 5G Action Plan. Deutsche Telekom lit standalone cores in Frankfurt, Munich, and Berlin, targeting automotive OEMs along the Autobahn corridors. Orange activated service in Paris and Lyon, and EE and Vodafone UK rolled out cores in London and Manchester. Sanctions limit Russian operator access to Western equipment, slowing adoption, but Swisscom, Telenor, and TIM demonstrate that smaller markets can still transition quickly by adopting cloud-native appliances. Meanwhile, South America and the Middle East, and Africa remain early-stage yet promising. Claro, TIM, and Vivo conducted trials in São Paulo and Rio de Janeiro, while STC Saudi Arabia, Etisalat UAE, and MTN South Africa launched urban enterprise zones and plan broader coverage by 2027 as spectrum auctions conclude.

Competitive Landscape

Market leadership remains moderately concentrated, with Ericsson, Nokia, Huawei, Samsung, and ZTE controlling most carrier-grade core deployments, yet fragmentation is accelerating. Ericsson powers roughly half of all live standalone networks and maintains deep hyperscaler alliances with Google Cloud to enable fully managed cores. Nokia’s AirScale and MX Industrial Edge target both public networks and verticals, leveraging containerization and AI analytics to secure contracts at Telia and John Deere. Huawei still dominates China and selects Middle Eastern markets thanks to tight operator integration, while Samsung’s vRAN 3.0 partnership with Verizon and KDDI offers a Western diversification option.

Software-centric challengers erode incumbent share by offering disaggregated, API-driven platforms. Mavenir supplies open RAN and cloud-native cores for Dish Network and greenfield Asian carriers. Rakuten Symphony markets a turnkey architecture derived from its Japanese network and recently secured investments from Cisco, enhancing credibility with tier-1 prospects. Oracle’s USD 300 million Vodafone deal illustrates how IT-heritage vendors can break into telecom domains by emphasizing cloud portability and microservice compliance.

Open-source initiatives amplify competition. The Linux Foundation’s Magma and free 5GC cores appeal to tier-3 carriers and enterprises that value cost minimization and code transparency. HPE’s acquisition of Athonet bundles core, edge compute, and managed services into a plug-and-play kit suited for factories and mines. Juniper Networks focuses on transport, aligning Cloud Metro with 5G backhaul needs. As O-RAN Alliance conformance tests mature and Telecom Infra Project plugfests validate interoperability, the market tilts toward best-of-breed ecosystems, broadening supplier diversity and lowering switching barriers.

5G Standalone Core Transformation Industry Leaders

Huawei Technologies Co., Ltd.

Telefonaktiebolaget LM Ericsson

Nokia Corporation

ZTE Corporation

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ericsson and Google Cloud have deepened their collaboration, rolling out cloud-native 5G core solutions throughout Europe and the Asia-Pacific. This initiative allows operators to deploy standalone cores on Google Cloud's infrastructure, with features such as automated scaling and upgrades without downtime. The partnership primarily caters to tier-1 operators aiming to cut capital expenditures, all while upholding stringent service-level agreements concerning latency and availability.

- January 2026: Nokia unveiled its MX Industrial Edge 2.0 platform, which combines a standalone 5G core, edge computing, and AI-driven analytics into a single rugged chassis tailored for factory floors. Early adopters, including automotive plants in Germany and electronics manufacturers in South Korea, have reported an 18% reduction in production-line downtime.

- November 2025: Oracle Communications has clinched a multi-year contract with Vodafone, set to roll out its Cloud Native Core in 12 European markets. This move not only replaces the older evolved packet cores but also paves the way for network slicing tailored for enterprise clients. With the deal exceeding a valuation of USD 300 million, Oracle is carving out a niche as a formidable contender against established telecom-equipment vendors.

Global 5G Standalone Core Transformation Market Report Scope

The 5G Standalone Core Transformation Market Report is Segmented by Component (Hardware, Software, and Services), Deployment Model (Public Cloud, Private Cloud, and Hybrid/On-premises), End-User (Telecom Operators, and Enterprises/Private 5G Owners), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Public Cloud |

| Private Cloud |

| Hybrid / On-premises |

| Telecom Operators |

| Enterprises / Private 5G Owners |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid / On-premises | |||

| By End-User | Telecom Operators | ||

| Enterprises / Private 5G Owners | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the 5G standalone core transformation market in 2031?

The market is forecast to reach USD 68.64 billion by 2031, reflecting a 49.36% CAGR over 2026-2031.

Which component is growing fastest within 5G standalone cores?

Software is expected to expand at a 52.4% CAGR through 2031 as operators invest in microservices licensing and AI-driven automation.

Why are enterprises investing in private 5G standalone networks?

Private cores deliver deterministic latency, guaranteed bandwidth, and air-gapped security, enabling Industry 4.0 applications such as robotic control and 8K video inspection.

Which region will record the highest growth rate through 2031?

Asia-Pacific is projected to lead with a 54.0% CAGR, bolstered by large-scale deployments in China, Japan, South Korea, and India.

How are hyperscalers influencing standalone core deployment?

Partnerships with AWS, Google Cloud, and Microsoft Azure let carriers quickly spin up cloud-native cores while reducing capex, driving growth across hybrid and public-cloud models.

Page last updated on: