5G Infrastructure Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

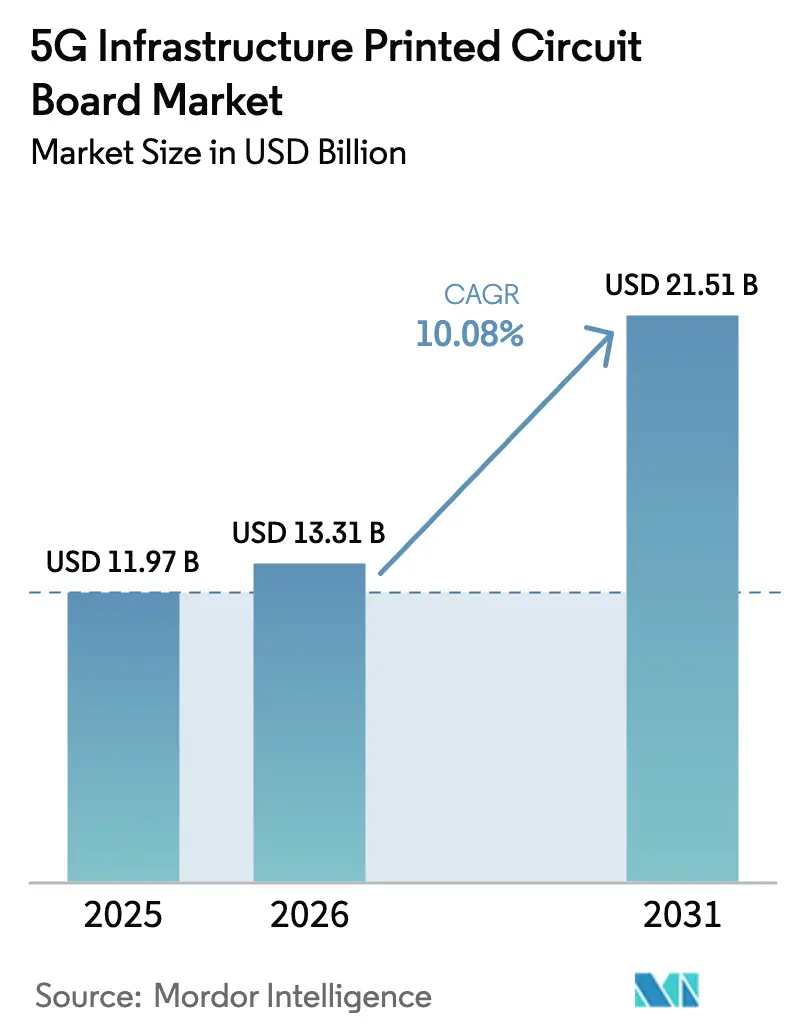

| Market Size (2026) | USD 13.31 Billion |

| Market Size (2031) | USD 21.51 Billion |

| Growth Rate (2026 - 2031) | 10.08% CAGR |

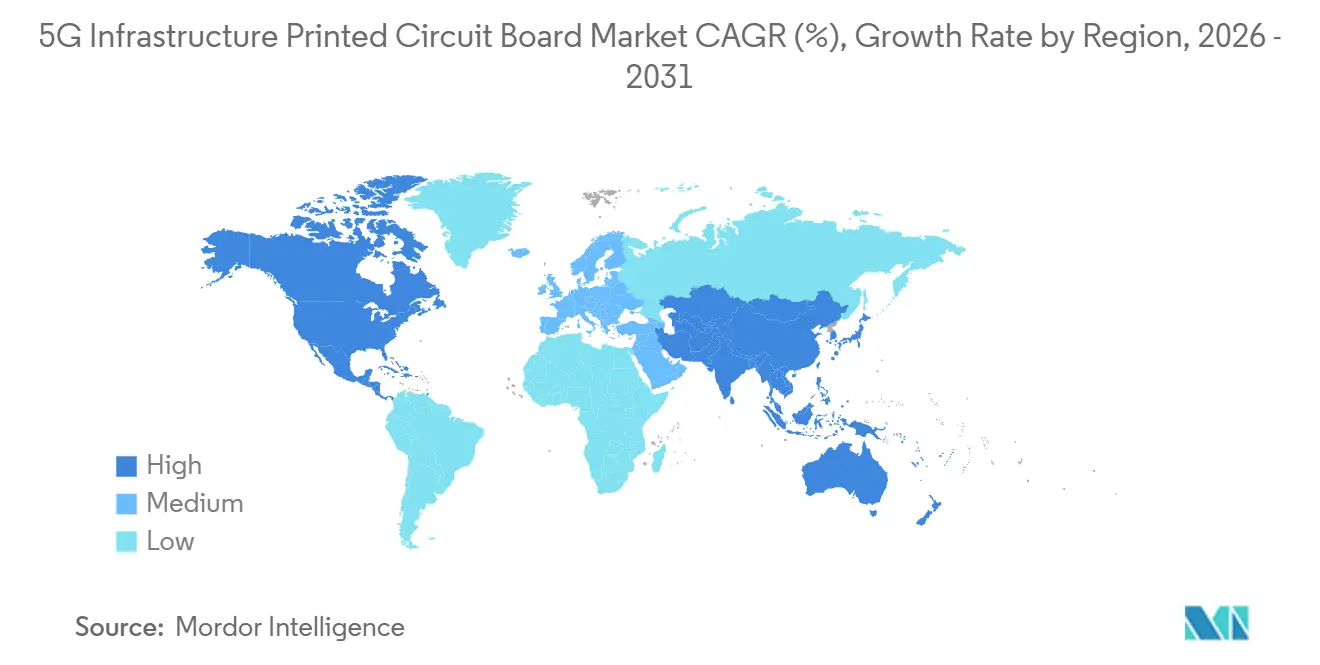

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Infrastructure Printed Circuit Board Market Analysis by Mordor Intelligence

The 5G infrastructure printed circuit board Market size is projected to be USD 11.97 billion in 2025, USD 13.31 billion in 2026, and reach USD 21.51 billion by 2031, growing at a CAGR of 10.08% from 2026 to 2031. Steady public-network build-outs, Open RAN disaggregation, and defense procurement diversification are the three structural forces driving this expansion. Equipment vendors are double-booking capacity to hedge resin shortages, which is keeping fab utilization above 80% even in seasonally soft quarters. System-in-package radio architectures are compressing supply chains, rewarding fabricators that can co-locate substrate and assembly lines. Finally, defensive reshoring programs in the United States and Europe are tilting a modest share of demand toward non-Asian suppliers, even as Asia-Pacific keeps its cost and scale advantages.

Key Report Takeaways

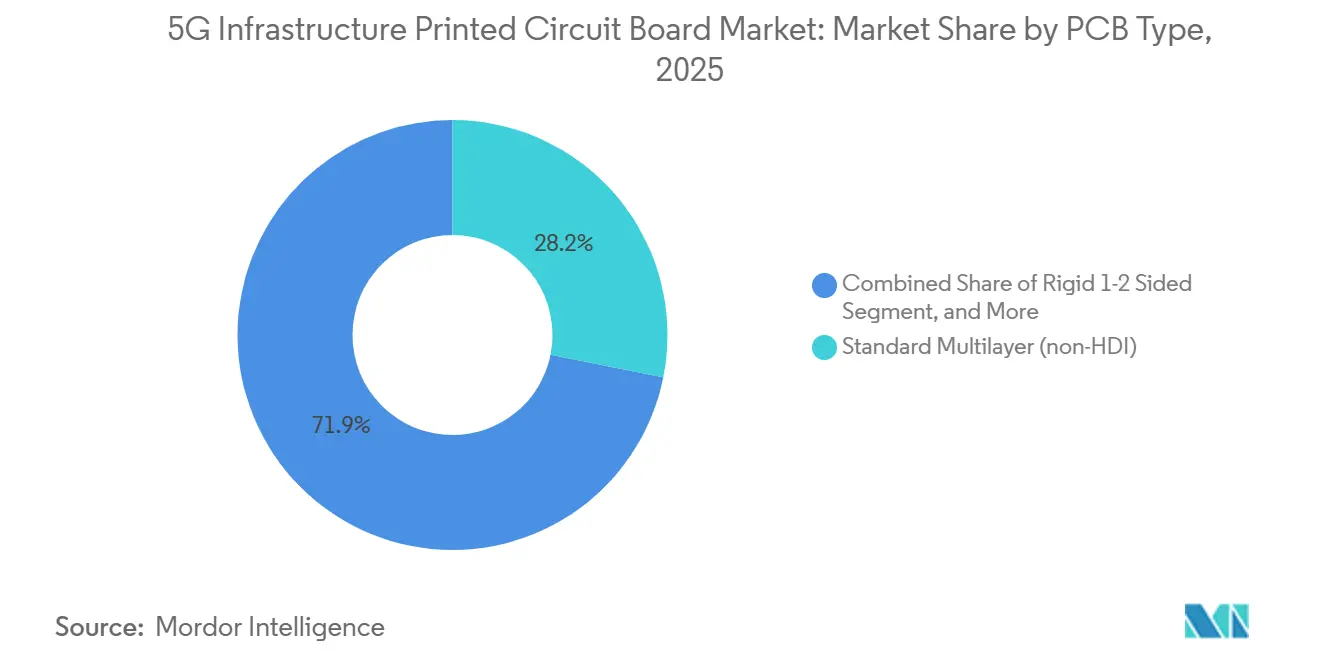

- By PCB type, flexible circuits led growth at a 12.80% CAGR through 2031, while standard multilayer boards retained 28.15% of the 5G Infrastructure printed circuit board (PCB) market share in 2025.

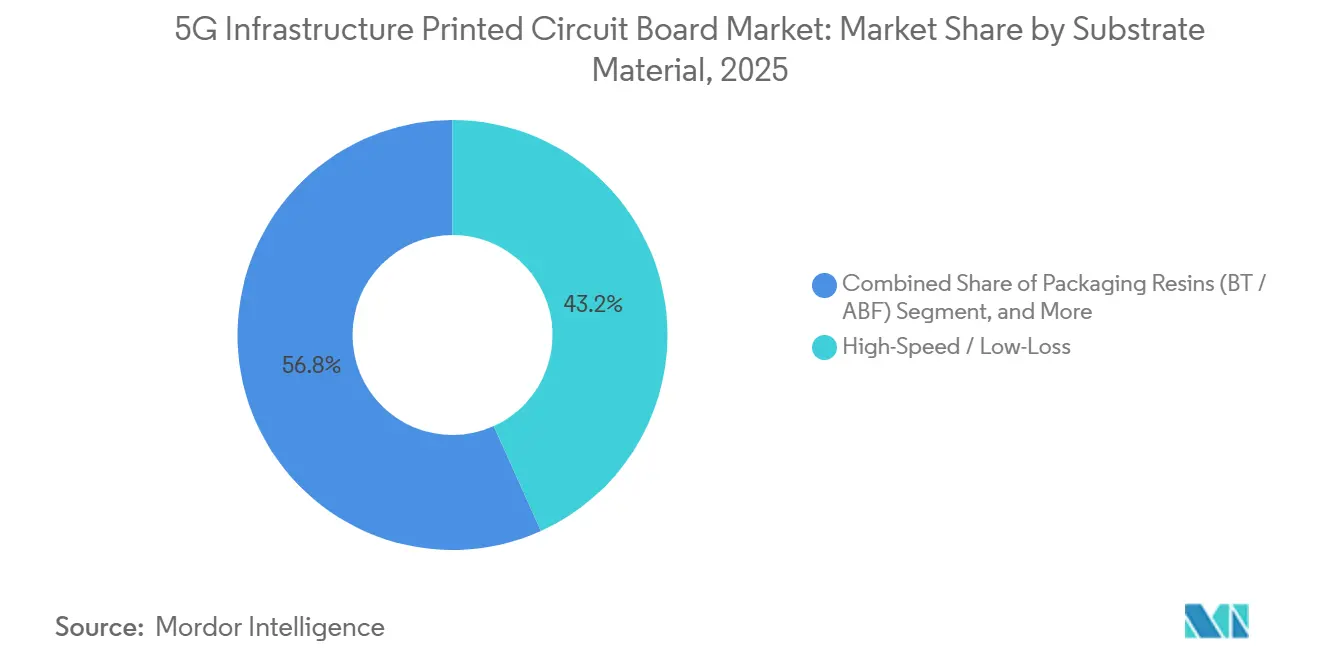

- By substrate material, high-speed and low-loss laminates accounted for 43.24% of the 5G Infrastructure printed circuit board market size in 2025, and polyimide substrates are projected to expand at 11.40% CAGR to 2031.

- By geography, Asia-Pacific captured 88.10% of the 5G Infrastructure PCB market share in 2025 and is positioned to grow at 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 5G Infrastructure Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Led 5G Roll-Out Targets | +2.3% | Global, peak in China, India, Southeast Asia | Medium term (2-4 years) |

| Massive MIMO Antenna Densification | +2.1% | Asia-Pacific core, North America metro clusters | Short term (≤ 2 years) |

| Open RAN Hardware Standardization | +1.6% | North America, Europe, India | Medium term (2-4 years) |

| Telco Cloud Migration | +1.4% | Global, concentrated in North America and Europe data centers | Long term (≥ 4 years) |

| Defence Procurement of 5G Tactical Networks | +0.9% | United States, European Union, Australia | Long term (≥ 4 years) |

| Ultra-Low Loss Materials for mmWave | +1.2% | Asia-Pacific, North America urban corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Led 5G Roll-Out Targets

National spectrum auctions and infrastructure mandates are compressing project timelines, pushing equipment vendors to reserve PCB capacity 12 to 18 months ahead of historical norms. China deployed more than 3.68 million base stations by the end of 2024, representing over 60% of the global installed base. India set a goal of 500,000 base stations by 2027 under its 2024 spectrum plan. The European Union’s 2025 Action Plan links funding to local content, prompting German, French, and Dutch fabricators to add HDI lines despite higher labor costs. These policies create lumpy demand that benefits fabs with flexible scheduling and ready resin inventory.

Massive MIMO Antenna Densification Driving HDI PCB Demand

Antenna arrays with 64 to 256 elements require boards exceeding 20 layers and via densities above 150 per square centimeter, specifications achievable only with HDI processes. Ericsson’s 2025 Antenna Integrated Radio uses blind and buried vias to minimize loss above 3.5 gigahertz.[1]Source: Telefonaktiebolaget LM Ericsson, “Annual Report 2025,” ericsson.com Nokia adopted any-layer HDI to shorten trace lengths in its 2025 portfolio.[2]Source: Nokia Corporation, “Investor Presentation Q1 2025,” nokia.com Average selling prices for antenna PCBs rose 15% to 20% versus 2023 baselines, lifting revenue per square inch for fabricators that invested in laser drilling.

Open RAN Hardware Standardization Across Operators

The O-RAN Alliance’s 2024 E2 interface creates interoperability between multi-vendor radio units and baseband controllers, opening supply opportunities for mid-tier PCB shops. Dish Network sourced radio PCBs from regional fabricators during its United States roll-out that concluded in 2025. Vodafone earmarked 30% of 2025 radio-unit spending for Open RAN vendors, signaling a permanent shift toward modular procurement. Standardization lowers switching costs, letting operators negotiate shorter lead times and volume-flex terms.

Telco Cloud Migration Requiring High-Speed Backplane Boards

Virtualized RAN and core workloads on commercial servers need backplanes supporting 100 Gbps lane speeds, driving demand for low-loss dielectrics with dissipation factors below 0.003 at 10 gigahertz. AT&T’s 2025 edge compute rollout relies on PCIe Gen 5 backplanes. Verizon expects 40% of RAN processing to shift to virtual infrastructure by 2028. This convergence of telecom and data-center design allows fabricators with hyperscale experience to win 5G contracts.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility in High-Speed Laminate Resin | -1.1% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Capital-Intensive HDI Line Installation for Legacy PCB Shops | -0.8% | North America, Europe, secondary Asia-Pacific | Medium term (2-4 years) |

| Export Controls on Advanced IC Substrates | -0.6% | China, Russia, select emerging markets | Long term (≥ 4 years) |

| Reliability Concerns in 5G Active Antenna PCB Integration | -0.5% | Global, early-deployment markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility in High-Speed Laminate Resin

Modified epoxy and PTFE resins come from a narrow supplier base in Japan and South Korea. Panasonic’s late-2024 force-majeure at its Osaka plant constrained low-loss resin supply for months. Rogers Corporation warned in its Q3 2025 call that allocation remained tight despite pre-buy programs. Dual-sourcing adds 12-month qualification cycles, capping HDI output at roughly 10% annual growth against 5G demand that is rising faster.

Capital-Intensive HDI Line Installation for Legacy PCB Shops

Laser drilling, sequential lamination, and automated optical inspection packages cost USD 15 million to USD 25 million per line. TTM invested USD 40 million in Asia-Pacific HDI capacity in 2024 but reported sub-70% utilization in its annual filing. Small North American and European fabs face higher financing costs, pushing them toward low-margin contract work or exits. The capital hurdle consolidates supply, elevating scale as the primary barrier to entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Capture Momentum

Flexible circuits are expanding at a 12.80% CAGR through 2031, reflecting antenna designers’ preference for lighter, bendable interconnects that survive tower vibration and thermal cycling. Standard multilayer boards still controlled 28.15% of 2025 revenue, underpinning baseband units where rigidity supports heat sinks. High-density interconnect boards are carving share in front-end modules, with via-in-pad designs pushing component densities past 200 parts per square inch. Rigid 1-2 sided boards remain fixtures in power distribution, although their contribution is shrinking as subsystems consolidate. The broader shift toward flex is expected to add four percentage points to the 5G Infrastructure PCB market size for this category by 2031.

The 5G Infrastructure printed circuit board market rewards fabs that combine any-layer HDI with roll-to-roll flex processing. Antenna vendors report 15% weight reduction when swapping rigid cores for flex tails, enabling lighter tower loads and faster installation. IC substrates, tracked separately, are growing at 10.50% CAGR as flip-chip packages proliferate. Rigid-flex solutions occupy a niche in compact radio heads that need both mechanical stability near connectors and flexibility around curved housings. Metal-core and ceramic options, while below 5% of revenue, remain indispensable where amplifier heat exceeds 100 watts.

By Substrate Material: High-Speed Laminates Lead, Polyimide Outpaces

High-speed and low-loss laminates held 43.24% of 2025 revenue of the 5G infrastructure printed circuit board market, buoyed by operator willingness to pay 20% to 30% premiums for millimeter-wave performance. Polyimide is the fastest-growing material at 11.40% CAGR, delivering dimensional stability from -40 °C to +85 °C in flexible antenna assemblies. FR-4 glass epoxy is still prevalent in baseband and backhaul boards below 6 GHz, yet its share erodes as functions migrate upward in frequency. Packaging resins such as bismaleimide-triazine underpin IC substrates driving the newest baseband ASICs.

The 5G Infrastructure PCB market relies on tight dielectric-constant control, making IPC-4101 high-frequency grades baseline procurement requirements.[3]Source: IPC, “IPC-4101 Specification for High-Frequency Laminates,” ipc.org Rogers RO4000 and Isola Astra MT77 laminates are winning designs in 28 GHz antenna panels.[4]Source: Isola Group, “Astra MT77 Product Data Sheet,” isola-group.com Polyimide’s rise underscores the trade-off between flexibility and dielectric performance, a balance that laminate vendors are now optimizing by tweaking filler composition.

Geography Analysis

Asia-Pacific generated 88.10% of 2025 5G infrastructure PCB market revenue and is projected to grow at 10.12% CAGR through 2031. China’s 1 million-plus 2024 base-station additions created captive demand for Shennan Circuits and Kinwong, each of which expanded HDI lines in 2025. Taiwan’s Unimicron and Tripod leverage proximity to advanced semiconductor fabs to offer four-week lead times. South Korea’s Samsung Electro-Mechanics pursues vertical integration, pairing substrate fabrication with module assembly for cost savings and faster product cycles.

In the 5G infrastructure printed circuit board market, North America held a mid-single-digit share in 2025, hindered by labor costs and limited HDI capacity. The United States CHIPS and Science Act earmarks subsidies for domestic PCB production, and TTM’s planned USD 150 million Indian joint venture illustrates the pivot toward cost-effective Asian expansion paired with Western quality standards. Europe also sits below 5% share yet benefits from supply-chain diversification grants. AT&S is investing EUR 300 million (USD 330 million) in Austrian HDI capacity to win Open RAN and automotive contracts.

South America remains marginal, focusing on assembly rather than fabrication. Brazil’s local content rules apply mainly to final equipment, leaving PCB fabs under-scaled for 5G requirements. Overall, the 5G Infrastructure PCB market size continues to mirror global base-station deployment density, reinforcing Asia-Pacific’s dominance while allowing modest share gains for regions deploying security-of-supply subsidies.

Competitive Landscape

The top ten suppliers, in the 5G Infrastructure PCB Market, captured roughly 55% to 60% of global revenue in 2025, placing the sector in moderate concentration. Samsung Electro-Mechanics and Ibiden co-locate substrate production with component assembly, extracting margin at multiple stages. Taiwanese and Chinese fabs expand HDI lines faster than demand, compressing lead times but pressuring average selling prices. Open RAN contracts create a new volume of bids that smaller shops can pursue without proprietary lock-ins, while defense agencies in the United States and Europe fund second-source qualifications to safeguard strategic supply.

Emerging disruptors, in the 5G Infrastructure Printed Circuit Board Market, include AT&S India, leveraging production-linked incentives to add HDI lines optimized for domestic telecom projects. Technology differentiation revolves around any-layer HDI and embedded-component substrates, both of which lower board thickness and improve electrical performance. World Intellectual Property Organization data show a 25% jump in PCB-related patent filings between 2023 and 2025, especially in via-fill chemistry and laser-ablation processes. Compliance with IPC-6012 Class 3 reliability standards has become table stakes for tier-1 bids, further raising the quality bar for new entrants.

Pricing power is under strain as Asia-Pacific fabs chase economies of scale, but specialized niches such as ultra-low-loss mmWave laminates and defense-grade reliability hold firmer margins. Overall, the 5G Infrastructure printed circuit board market continues to reward vertical integration, rapid capacity additions, and standards-driven modularity.

5G Infrastructure Printed Circuit Board Industry Leaders

Nippon Mektron Ltd.

Unimicron Technology Corp.

Zhen Ding Technology Holding Ltd.

Tripod Technology Corp.

Austria Technologie & Systemtechnik AG (AT&S)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unimicron Technology committed USD 500 million to expand HDI and IC substrate capacity at its Taoyuan campus, with 12 additional laser-drilling machines and automated optical inspection slated for Q3 2026 ramp-up.

- December 2025: AT&S secured a multi-year, EUR 200 million (USD 220 million) Open RAN PCB contract with a tier-1 European vendor, dedicating Austrian HDI lines to meet local-content requirements.

- November 2025: Samsung Electro-Mechanics completed a Vietnam packaging-substrate plant capable of 500,000 m² per month, featuring lithography for sub-25 µm lines.

- October 2025: TTM Technologies formed a USD 150 million joint venture in Bangalore to build an HDI fabrication line aimed at domestic and Southeast Asian 5G deployments.

Global 5G Infrastructure Printed Circuit Board Market Report Scope

The 5G Infrastructure Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, HDI, Flexible Circuits, IC Substrates, and Rigid-Flex), Substrate Material (Glass Epoxy, High-Speed/Low-Loss, Polyimide, and Packaging Resins), PCB Materials (CCL, and High-Density Packaging Substrate), and Geography (North America, Europe, Asia-Pacific, and South America). Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| North America | United States |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Taiwan | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By PCB Type | Standard Multilayer (non-HDI) | |

| Rigid 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Flexible Circuits (FPC) | ||

| IC Substrates (Package Substrates) | ||

| Rigid-Flex | ||

| Other PCB Types | ||

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Substrate Materials | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Taiwan | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current value of the 5G Infrastructure PCB market?

The market generated USD 13.31 billion in 2026 and is forecast to reach USD 21.51 billion by 2031.

Which PCB type is growing fastest in 5G infrastructure hardware?

Flexible circuits lead growth with a 12.80% CAGR through 2031 as antenna units prioritize lightweight, bendable interconnects.

Why are high-density packaging substrates gaining share?

System-in-package radios integrate multiple functions on one interposer, pushing demand for substrates with sub-25 µm line widths and driving a 10.90% CAGR for this material class.

How dominant is Asia-Pacific in 5G infrastructure PCB production?

Asia-Pacific commands 88.10% of 2025 revenue and is projected to grow at 10.12% CAGR thanks to large HDI and IC substrate capacity in China, Taiwan, and South Korea.

Page last updated on: