3D Bioprinting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

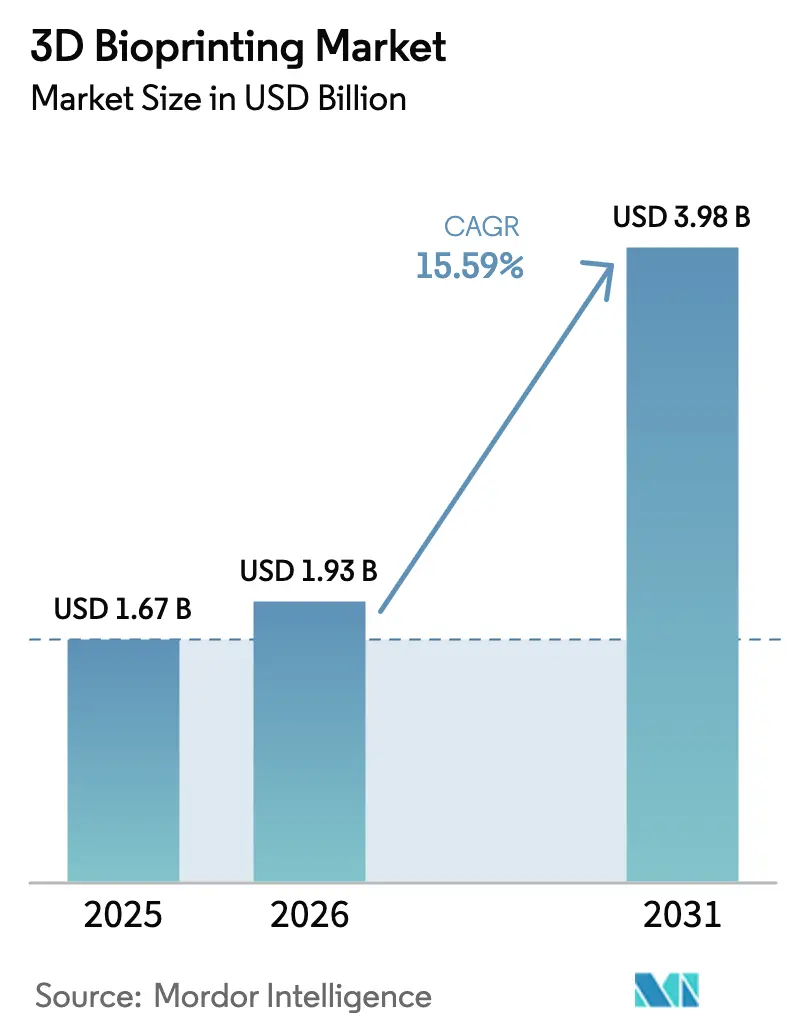

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 3.98 Billion |

| Growth Rate (2026 - 2031) | 15.59% CAGR |

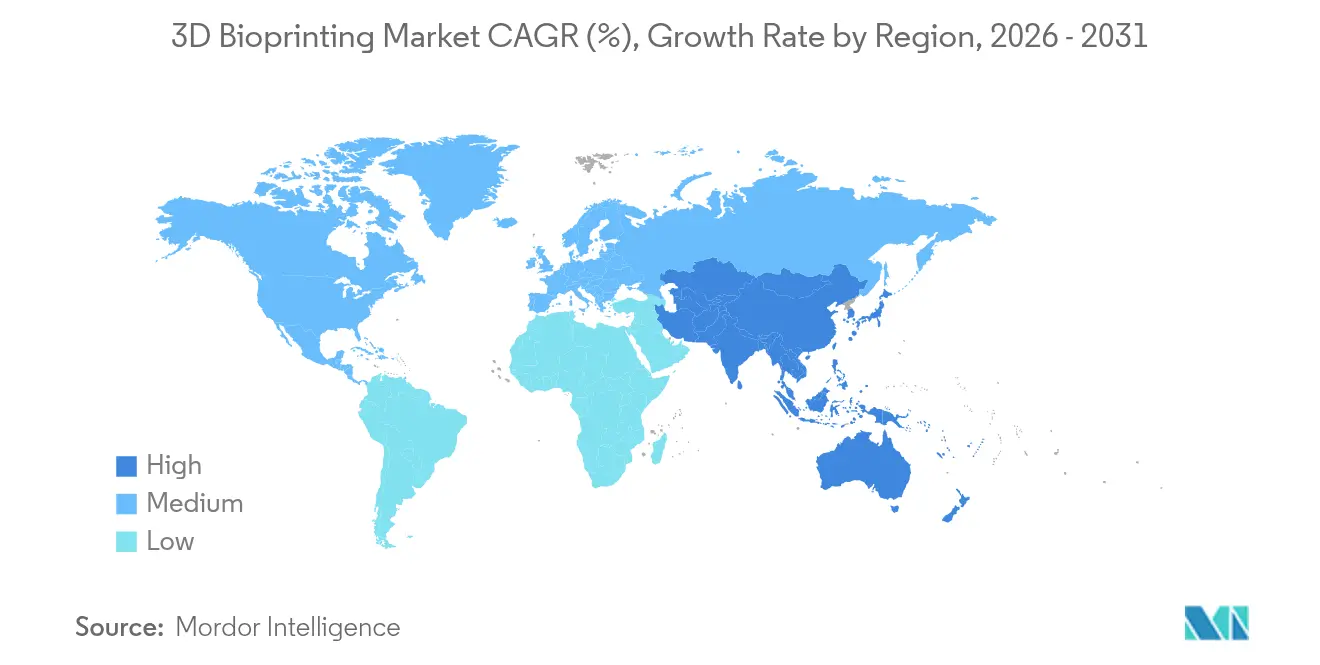

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Bioprinting Market Analysis by Mordor Intelligence

The 3D bioprinting market size was valued at USD 1.67 billion in 2025 and estimated to grow from USD 1.93 billion in 2026 to reach USD 3.98 billion by 2031, at a CAGR of 15.59% during the forecast period (2026-2031). Growth hinges on the convergence of AI-driven design automation, clarified regulatory pathways, and breakthroughs in vascularization that enable bioprinted tissues to transition from bench to bedside. The ARPA-H PRINT program’s USD 65 million grant in March 2024, along with NASA’s five-year BioNutrients experiments, illustrates how public capital is accelerating toward clinical goals. Aging populations in high-income economies, the expansion of public–private research consortia, and off-Earth healthcare initiatives add tailwinds. North America held 38.70% of the 3D bioprinting market in 2024, while the Asia-Pacific region is the fastest-growing, with an 18.35% CAGR to 2030, driven by policy reforms in India and Japan that support regenerative medicine.

Key Report Takeaways

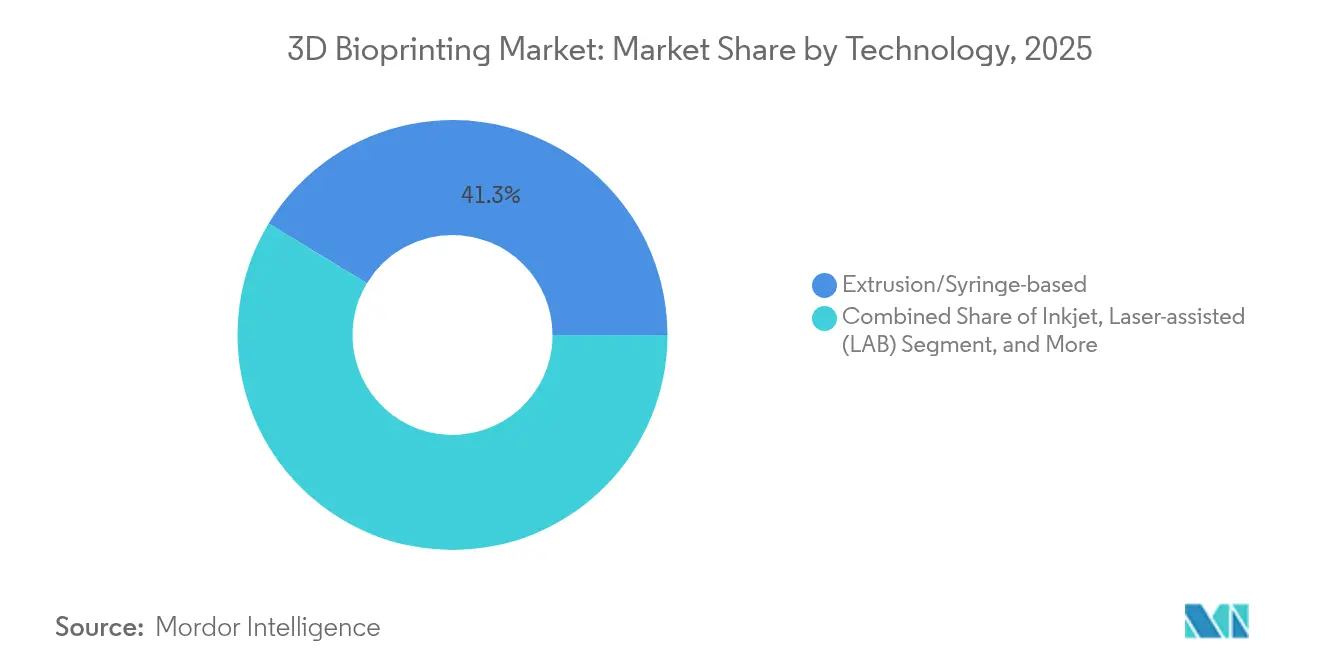

- By technology, extrusion/syringe systems led with 41.33% revenue share in 2025; Digital Light Processing is projected to post the highest 15.94% CAGR through 2031.

- By component, 3D bioprinters captured 45.28% of the value in 2025; biomaterials are set to expand at an 17.33% CAGR through 2031.

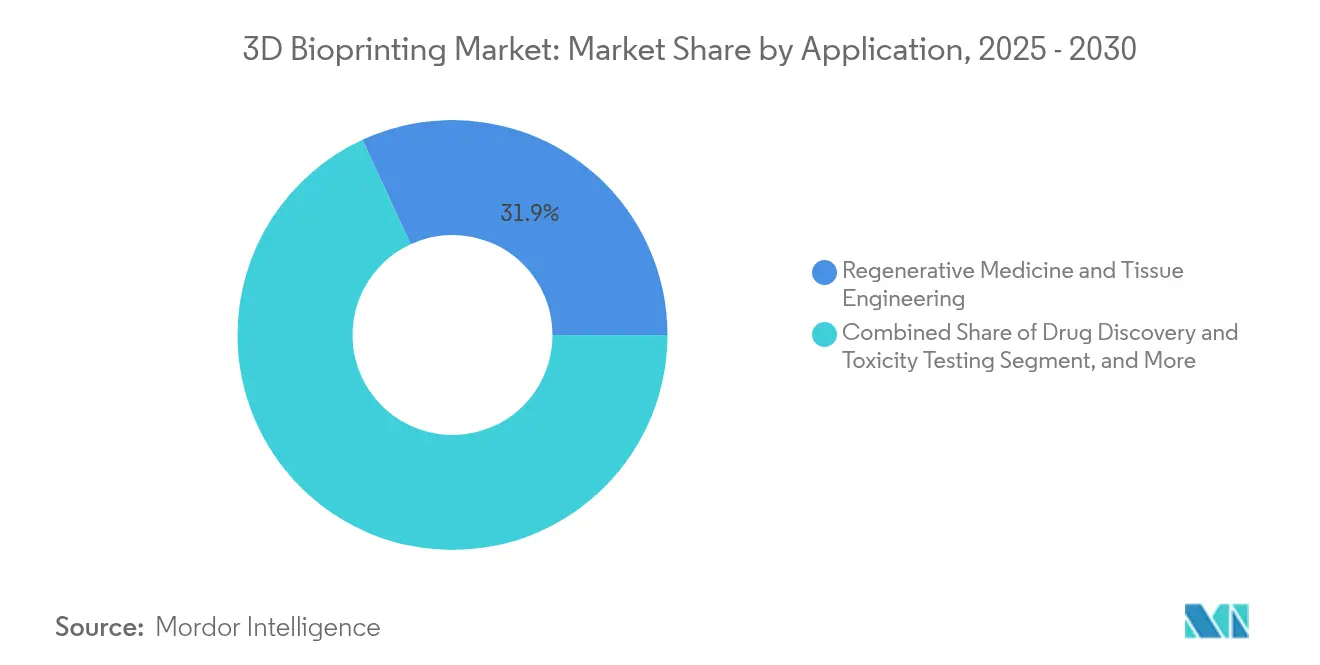

- By application, regenerative medicine and tissue engineering accounted for 31.88% of the 3D bioprinting market share in 2025; precision medicine applications are expected to grow at a 16.21% CAGR through 2031.

- By end user, academic and research institutes accounted for 47.42% of demand in 2025; contract research organizations are expected to advance at a 16.77% CAGR through 2031.

- By geography, North America dominated the 3D bioprinting market with a 38.24% share of the market size in 2025, while the Asia-Pacific region recorded the fastest 17.72% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Bioprinting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population and chronic diseases | +2.80% | North America, Europe | Long term (≥4 years) |

| Growing R&D funding and public–private partnerships | +3.20% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Advances in multi-material/high-resolution printing | +2.10% | Global; early adopters in North America | Short term (≤2 years) |

| Demand for transplant alternatives and regenerative medicine | +3.50% | Global; highest in North America and Europe | Long term (≥4 years) |

| Space and defence agency investment for off-earth healthcare | +1.40% | North America, Europe, select Asia-Pacific | Long term (≥4 years) |

| AI-driven design automation enabling personalised tissues | +2.60% | Global; early adopters in North America and Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population and Chronic Diseases

Developed economies face organ donor backlogs, spurring hospitals to trial bioprinted vascular grafts, such as Symvess, which secured FDA approval in December 2024 for trauma care.[1]U.S. Food & Drug Administration, “FDA clears first tissue-engineered vascular graft,” fda.gov Japan’s Development Bank invested 1 billion yen (USD 6.8 million) in metal-printing firm 3DEO during January 2024 to prepare for an aging society’s healthcare burden. The world’s first point-of-care facial implant, printed at University Hospital Basel in March 2025, illustrates how clinical adoption is meeting demographic necessity.

Growing Research and Development Funding and Public–Private Partnerships

ARPA-H’s PRINT program earmarked USD 65 million for liver, kidney, and heart constructs. The University of Sydney inaugurated a Biomanufacturing Incubator in August 2024 to combine cell science with scale-up printing. Europe gained momentum through the EC-funded REBORN cardiac tissue project, utilizing Newcastle University’s ReJI platform. Private tie-ups, such as CELLINK’s renewed drug-discovery pact with a global pharmaceutical giant in June 2024, demonstrate industry integration.

Advances in Multi-Material/High-Resolution Printing

Digital Light Processing (DLP) bioprinters deliver micron-scale fidelity that allows Stanford engineers to algorithmically design 500-branch vascular networks 200 times faster than prior methods. Penn State’s HITS-Bio process cuts tissue-assembly time by 90% using spheroids at high cell density. Partnerships such as Nanoscribe and Advanced BioMatrix released four TPP bioresins tailored for cell-laden constructs in May 2024.

Demand for Transplant Alternatives and Regenerative Medicine

Regenerative medicine accounted for 32.40% of the 3D bioprinting market in 2024, while precision medicine is the fastest-growing segment. The FDA cleared PrintBio’s resorbable 3DMatrix surgical mesh in May 2025, offering a template for future biologics approvals. Wythenshawe Hospital reported 100% union rates in hindfoot surgeries using platelet-rich fibrin-coated scaffolds by 2024. Organovo’s USD 10 million FXR program sale to Eli Lilly in March 2025 underlined drug-screening value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and consumable costs | -2.10% | Global; steepest in emerging markets | Medium term (2–4 years) |

| Stringent regulatory and ethical hurdles | -1.80% | Worldwide; jurisdiction-specific | Long term (≥4 years) |

| Medical-grade hydrogel supply-chain bottlenecks | -1.40% | Global; most acute in Asia-Pacific and LATAM | Medium term (2–4 years) |

| Cross-lab reproducibility and standards gaps | -1.70% | Global; stronger effect in emerging ecosystems | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs

3D Systems’ 2024 revenue dipped to USD 440 million after customers deferred printer purchases; the firm launched a USD 50 million cost‐cut plan while preserving R&D budgets. Hydrogels imported from specialty vendors increase unit costs, and volumetric additive manufacturing, such as LLNL’s NASA-funded “Replicator” cartilage system, still requires high initial outlays. New entrants such as Biological Lattice Industries raised USD 1.8 million to produce lower-cost desktop biofabricators.

Stringent Regulatory and Ethical Hurdles

The European Commission’s March 2024 biotech communiqué calls for coherent rules, yet it underscores the ethical complexity of bioprinting. India revised clinical-trial guidelines in 2023 to allow alternative testing, encouraging local bioprinting firms.[2]Nature News, “India Updates Clinical-Trial Rules to Allow Alternative Testing,” nature.com In the United States, simple devices like surgical meshes often gain clearance faster than full organ constructs, thereby prolonging the time-to-market and increasing investor risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: DLP accelerates clinical translation

Extrusion platforms maintained a 41.33% revenue hold in 2025, while DLP systems are projected to achieve a 15.94% CAGR, as they replicate capillary-size geometries essential for kidney tissue viability. Inkjet and laser techniques serve research niches where cell placement fidelity outweighs throughput. Freeform Reversible Embedding (FRESH), used by Carnegie Mellon’s group, produces collagen constructs relevant to diabetes therapies. NASA-backed volumetric systems expect to shorten build times for cartilage in microgravity conditions.

Clinical demand for multi-material constructs favors DLP’s photopolymer approach even at higher price points. Magnetic levitation and micro-valve printers occupy specialized niches, such as neuro-tissue modeling. Over the forecast horizon, DLP suppliers are likely to integrate AI-guided print-path optimization and closed-loop imaging for real-time defect correction, reinforcing the 3D bioprinting market’s technology shift.

By Component: Biomaterials drive innovation

Biomaterials hold 45.65% revenue share in the 3D bioprinting market in 2025 and will post the fastest 17.33% CAGR as researchers pivot from single-polymer gels to composite hydrogels loaded with signaling peptides. Meanwhile, 3D bioprinters, which already account for 45.28% of sales, will diversify from desktop research models to GMP-compliant hospital units.

Next-generation scaffolds favor bioresorbable metals, such as Bioretec’s RemeOs, which were FDA-cleared in 2023, thereby eliminating the need for explant surgeries. Manufacturers are vertically integrating to capture sales of powder, hydrogel, and printers under one umbrella, thereby tightening ecosystem control and safeguarding print-quality reproducibility.

By Application: Precision medicine emerges

Regenerative medicine kept 31.88% of revenue in 2025, yet precision oncology models, advancing at a 16.21% CAGR, underscore where hospitals see immediate ROI. POSTECH’s vascularized gastric-cancer construct reached 90% viability, enabling patient-specific drug sensitivity screening. The 3D bioprinting market size for drug-testing platforms is projected to grow at a prominent rate through 2031.

Food technology is another fast fringe. The Osaka-Kansai Expo 2025 will showcase home-cultured meat using bioprinted scaffolds, and Cocuus aims to produce 1,000 tonnes of plant-based bacon per year. The cosmetic and veterinary niches add incremental revenue by exploiting less stringent regulatory pathways.

By End-User: CROs accelerate adoption

Academic labs still account for 47.42% of revenue in 2025, supported by grants such as ARPA-H PRINT. Yet contract research organizations will rise at 16.77% CAGR as pharma outsources organ-on-chip assays. For instance, CN Bio and Pharmaron partnered in April 2025 to globalize PhysioMimix systems. Hospitals are procuring MDR-compliant units such as the Basel PEEK implant line, signaling the leap toward bedside manufacturing.

Training deficits present commercial opportunities for courseware vendors and service bureaus that offer print-on-demand solutions for hospitals with limited capital budgets. As CROs scale, they embed quality management modules essential to winning FDA and EMA study approvals.

Geography Analysis

North America’s 38.24% hold stems from federal programs, such as NASA’s BioNutrients initiative and ARPA-H’s PRINT, coupled with FDA precedents, including Symvess and 3DMatrix device clearances. Stanford and Penn State supply algorithmic and process breakthroughs that firms rapidly license. Clinical sites, such as University Hospital Basel, apply U.S.-developed printer hardware, underscoring the cross-Atlantic influence.

The Asia-Pacific region, projected to grow at an 17.72% CAGR, benefits from India’s regulatory amendments allowing non-animal testing and Japanese sovereign-fund backing for additive manufacturing. China ties with the United States in terms of scientific papers, while South Korea’s POSTECH champions precision-tumor models. Despite lower labor costs, the region is importing GMP scripting from Western vendors to comply with global standards for drug approval.

Europe prizes harmonized regulation; the EC’s 2024 biotech plan and ESOT’s ATMP roadmap streamline approvals yet demand rigorous datasets. Newcastle University’s ReJI platform and Nanoscribe’s TPP resins exemplify academic-industry coupling. The United Kingdom leads in pet food, cultured meat clearances, and cardiac tissue prototypes. Germany and Switzerland provide engineering depth and clinical pilots, respectively.

Competitive Landscape

Established vendors occupy the middle ground between niche start-ups and diversified industrial groups. BICO Group maintained its leadership by bundling CELLINK printers, proprietary bioinks, and software, which delivered SEK 2.2 billion in net sales in 2023, while extending a multi-year drug-discovery alliance with a global pharmaceutical partner. 3D Systems reported USD 440 million in revenue for 2024 and launched a USD 50 million cost-reduction plan that preserved core R&D budgets, enabling the first MDR-compliant PEEK facial implant to be manufactured at the point of care in Basel. Stratasys agreed to a USD 1.8 billion all-stock combination with Desktop Metal in June 2024, creating a multi-process additive platform that now spans metal and photopolymer technologies. Nano Dimension, followed by the purchase of Markforged for USD 115 million, signals that scale and portfolio breadth are becoming prerequisites for global account penetration.

Specialist challengers target narrow pain points that incumbents struggle to address. Biological Lattice Industries has raised USD 1.8 million to develop compact biofabrication units priced for university labs, a move aimed at lowering the adoption barrier created by the high price tags of six-figure printers. FluidForm Bio, spun out of Carnegie Mellon’s FRESH research, focused on pancreas-like constructs that promise shorter print times and higher cell viability, positioning the firm for early clinical trials. Biomedicines secured a USD 1 billion collaboration with Novartis in September 2024, combining AI-driven protein design with bioprinted tissue scaffolds to accelerate the screening of drug candidates. Patent activity surrounding universal donor cells intensified as CRISPR Therapeutics filed multiple applications seeking to secure key intellectual property for immune-evasive tissues.

Competitive positioning increasingly hinges on full-stack integration. Companies that pair AI design software, multi-material print heads, and GMP-grade bioinks gain an efficiency edge, which clients value when navigating FDA and EMA regulatory pathways. Service revenues are rising as hospitals and CROs outsource qualification, calibration, and validation tasks that accompany on-site manufacturing. Hardware vendors now bundle cloud-based quality-management systems to secure recurring income and reinforce customer lock-in. This convergence of hardware, software, and services suggests that market leadership will belong to platforms capable of shepherding clinicians from CAD file to cleared implant within a unified workflow.

3D Bioprinting Industry Leaders

Cellink

3D Systems Corporation

3D Bioprinting Solutions

REGEMAT 3D

Aspect Biosystems Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Carnegie Mellon’s FRESH method printed insulin-producing pancreatic tissue; FluidForm Bio eyes clinical trials.

- March 2025: 3D Systems and University Hospital Basel delivered the first MDR-compliant PEEK facial implant printed in-house.

- August 2024: University of Sydney opened a Biomanufacturing Incubator to bridge lab innovation with market needs.

- June 2024: Stratasys and Desktop Metal announced an all-stock merger valued at USD 1.8 billion.

Global 3D Bioprinting Market Report Scope

The 3D Bioprinting Market Report is Segmented by Technology (Syringe/Extrusion-based, Inkjet, Laser-Assisted (LAB), Magnetic Levitation, Micro-Valve, Digital Light Processing (DLP), Freeform Reversible Embedding (FRE), and Other Technologies), Component (3D Bioprinters, Biomaterials, and Scaffolds), Application (Regenerative Medicine and Tissue Engineering, Drug Discovery and Toxicity Testing, Personalised and Precision Medicine, Food and Alternative Protein Research, Academic Research, and Other Applications), End-User (Academic and Research Institutes, Pharmaceutical and Biotechnology Cos., Hospitals and Surgical Centres, and Contract Research and Manufacturing Organisations), and Geography (North America, Europe, South America, Asia Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Extrusion/Syringe-based |

| Inkjet |

| Laser-assisted (LAB) |

| Magnetic Levitation |

| Micro-valve |

| Digital Light Processing (DLP) |

| Freeform Reversible Embedding (FRE) |

| Other Technologies |

| 3D Bioprinters | Desktop |

| Industrial/Commercial | |

| Biomaterials | Hydrogels |

| Nanofibrillated Cellulose | |

| Decellularised ECM | |

| Synthetic Polymers | |

| Scaffolds |

| Regenerative Medicine and Tissue Engineering |

| Drug Discovery and Toxicity Testing |

| Personalised and Precision Medicine |

| Food and Alternative Protein Research |

| Academic Research |

| Other Applications |

| Academic and Research Institutes |

| Pharmaceutical and Biotechnology Cos. |

| Hospitals and Surgical Centres |

| Contract Research and Manufacturing Organisations |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Technology | Extrusion/Syringe-based | |

| Inkjet | ||

| Laser-assisted (LAB) | ||

| Magnetic Levitation | ||

| Micro-valve | ||

| Digital Light Processing (DLP) | ||

| Freeform Reversible Embedding (FRE) | ||

| Other Technologies | ||

| By Component | 3D Bioprinters | Desktop |

| Industrial/Commercial | ||

| Biomaterials | Hydrogels | |

| Nanofibrillated Cellulose | ||

| Decellularised ECM | ||

| Synthetic Polymers | ||

| Scaffolds | ||

| By Application | Regenerative Medicine and Tissue Engineering | |

| Drug Discovery and Toxicity Testing | ||

| Personalised and Precision Medicine | ||

| Food and Alternative Protein Research | ||

| Academic Research | ||

| Other Applications | ||

| By End-user | Academic and Research Institutes | |

| Pharmaceutical and Biotechnology Cos. | ||

| Hospitals and Surgical Centres | ||

| Contract Research and Manufacturing Organisations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the 3D bioprinting market?

The 3D bioprinting market stands at USD 1.93 billion in 2026 and is forecast to reach USD 3.98 billion by 2031.

Which technology segment is growing fastest?

Digital Light Processing bioprinters are expanding at a 15.94% CAGR thanks to their ability to replicate capillary-scale structures vital for organ viability.

Why is Asia-Pacific the fastest-growing region?

Reforms such as India’s clinical-trial amendments, Japanese investment in additive manufacturing, and cost-competitive manufacturing ecosystems drive an 17.72% regional CAGR.

What restraints hinder wider adoption?

High equipment and bioink costs, regulatory ambiguity, and hydrogel supply bottlenecks collectively trim the market’s potential CAGR by about 6.1 percentage points.

Which end-user group will see the quickest uptake?

Contract research organizations are poised for a 16.77% CAGR as pharmaceutical firms outsource organ-on-chip and toxicity testing workloads.

How is AI influencing 3D bioprinting?

AI accelerates design automation, evidenced by Stanford’s algorithm that cuts vascular network design time 200-fold, hastening the path to clinically functional organs.

Page last updated on: