2D Chromatography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 695.88 Million |

| Market Size (2031) | USD 965.75 Million |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

2D Chromatography Market Analysis by Mordor Intelligence

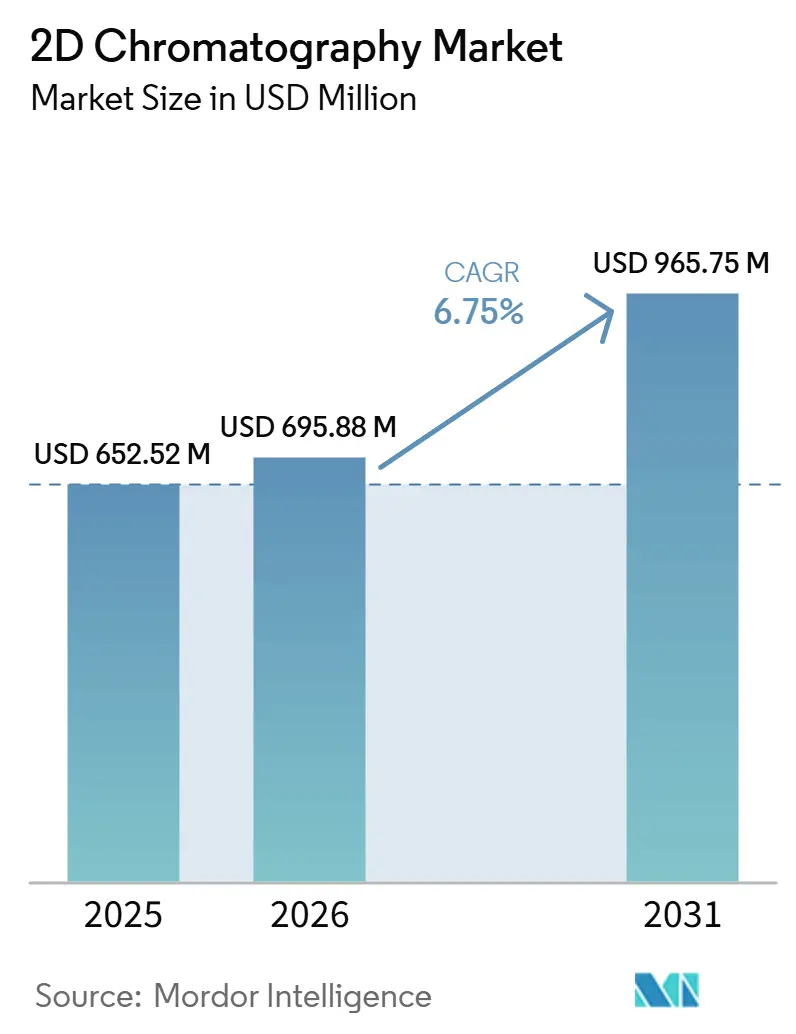

The 2D Chromatography Market size is projected to be USD 652.52 million in 2025, USD 695.88 million in 2026, and reach USD 965.75 million by 2031, growing at a CAGR of 6.75% from 2026 to 2031.

The market is moving further into routine analytical use because many laboratories now need more separation depth than one-dimensional systems can reliably deliver in biologics, omics, environmental, and food testing settings. Regulatory expectations are also becoming stricter, which is pushing laboratories to adopt workflows that can separate complex impurity pairs and generate stronger method documentation for audits and submissions. Demand is also strengthening because biologics pipelines, host cell protein analysis, and multi-omics programs all require broader selectivity and better identity confirmation than legacy single-dimension setups usually provide. Vendors in the 2D chromatography market are protecting installed positions through software-led ecosystems, integrated data handling, and instrument-service-consumable linkages that raise switching barriers after a platform is validated. The strongest opportunity remains in laboratories that now need multidimensional resolution but are still looking for easier automation, faster method transfer, and lower implementation friction than early systems allowed.

Key Report Takeaways

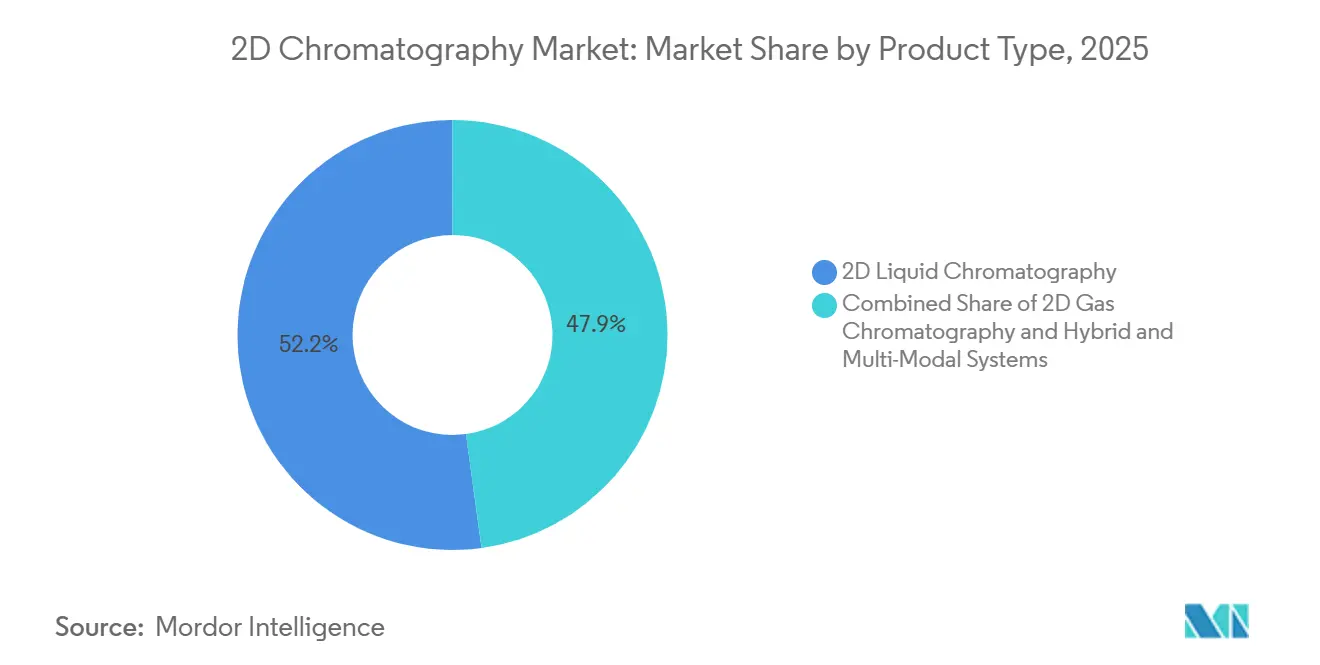

- By product type, 2D liquid chromatography held 52.15% of the 2D chromatography market share in 2025, while it is also projected to post the fastest CAGR at 7.38% through 2031.

- By application, pharmaceutical and biotechnology accounted for 35.37% of the 2D chromatography market size in 2025, while life science research is forecast to advance at an 8.01% CAGR through 2031.

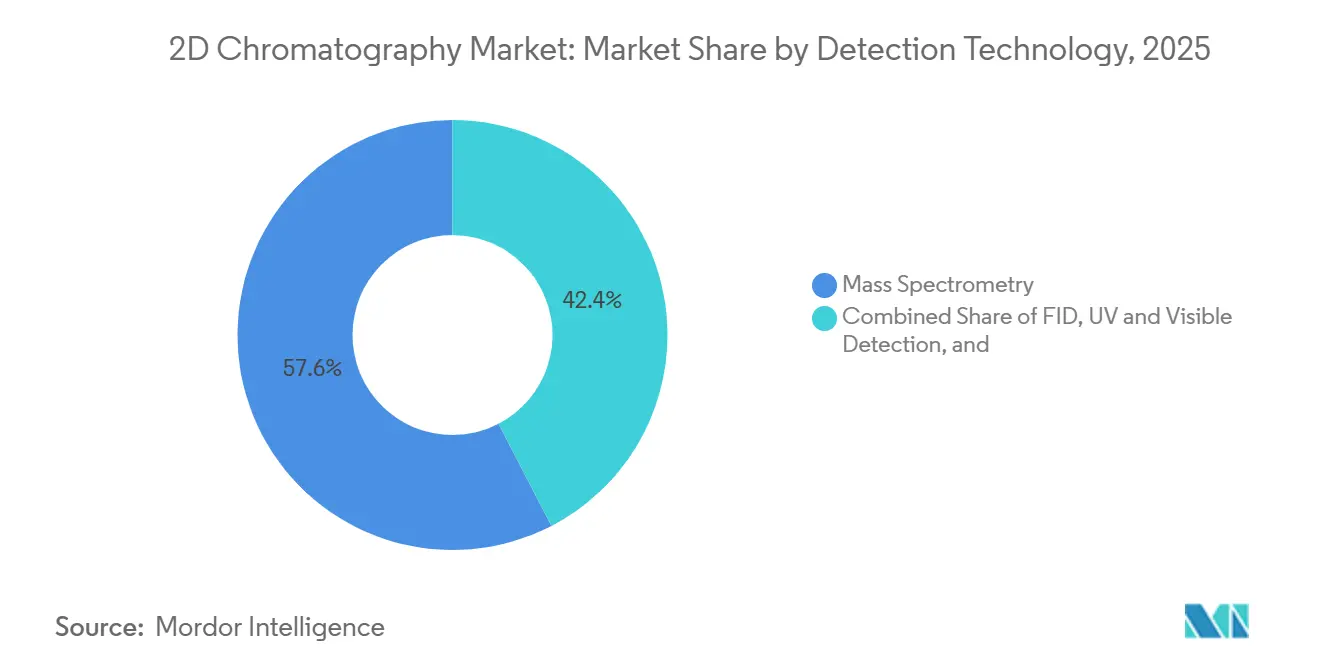

- By detection technology, mass spectrometry led with a 57.61% share in 2025 and is also expected to expand at the fastest CAGR of 7.91% through 2031.

- By end use, pharmaceutical and biotechnology companies represented 28.05% share in 2025, while the same group is expected to record the highest CAGR of 8.13% through 2031.

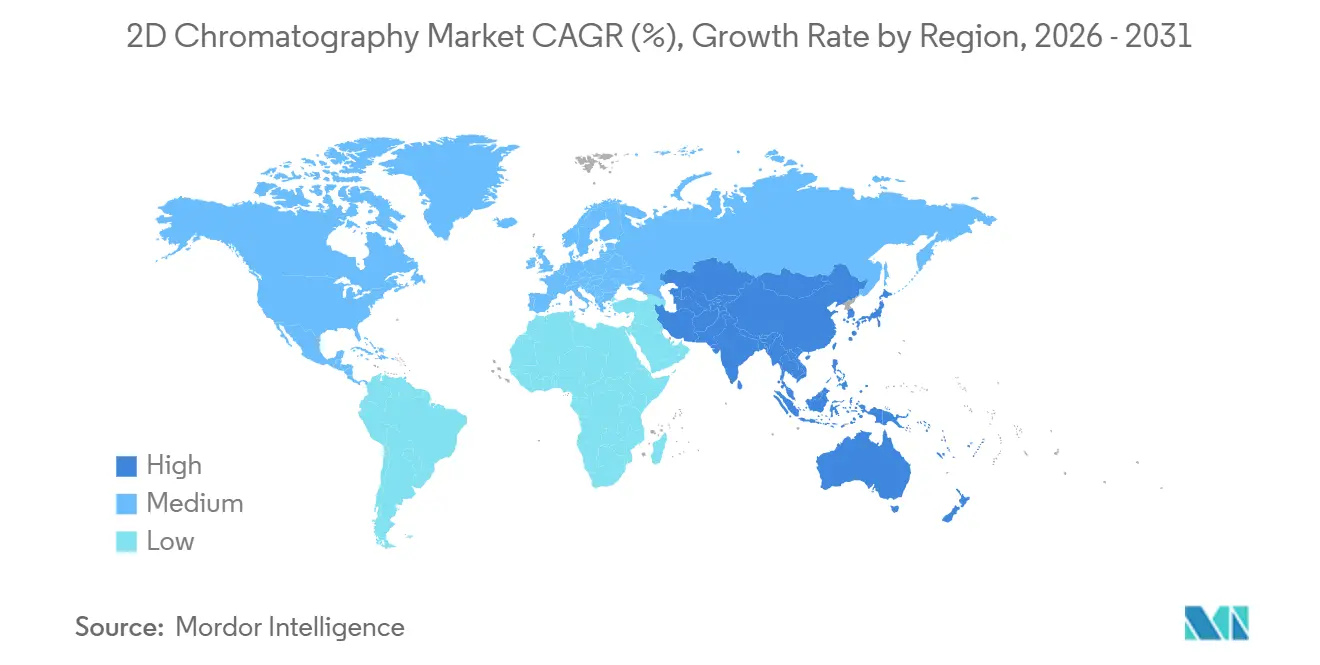

- By geography, North America captured 41.23% share in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 8.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 2D Chromatography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for High-Resolution Separation in Complex Samples | +1.2% | Global | Medium term (2-4 years) |

| Expansion of Biologics, Proteomics, and Metabolomics Workflows | +1.5% | North America, Europe, APAC core | Long term (≥ 4 years) |

| Tightening Quality and Impurity Profiling Requirements in Regulated Testing | +1.1% | North America & EU | Medium term (2-4 years) |

| Growth of Hyphenated 2D Chromatography and Mass Spectrometry Workflows | +1.0% | Global | Medium term (2-4 years) |

| Miniaturized and Automated Platforms Lowering Method Development Friction | +0.8% | North America, EU, APAC | Short term (≤ 2 years) |

| AI-Assisted Peak Deconvolution and Retention Alignment Improving Analytical Throughput | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Need for High-Resolution Separation in Complex Samples

Complex samples are becoming a core growth driver for the 2D chromatography market because co-elution problems now appear in biologics, proteomics extracts, environmental water samples, and food volatile analysis. In many of these matrices, a one-dimensional run can leave low-abundance compounds buried under stronger signals, which weakens impurity profiling, biomarker discovery, and trace contaminant detection. The technical case for multidimensional separation is strong because a 500-peak first dimension combined with a 50-peak second dimension yields a theoretical peak capacity of 25,000 compounds.[1]PubMed Central, “Comprehensive Two-Dimensional Liquid Chromatography High-Resolution Mass Spectrometry for Complex Protein Digest Analysis Using Parallel Gradients,” PubMed Central, pmc.ncbi.nlm.nih.gov That level of separation matters when laboratories must show that difficult impurity pairs or closely related analytes have been resolved well enough for regulatory or scientific review. As a result, the 2D chromatography market is benefiting from replacement demand as laboratories move from legacy single-dimension platforms toward heart-cut or comprehensive configurations. The same shift is also widening adoption across regulated and research settings because the separation problem is no longer limited to specialist laboratories.

Expansion of Biologics, Proteomics, and Metabolomics Workflows

The 2D chromatography market is also expanding because biologics development is increasing the need for broader protein variant characterization, impurity assessment, and process-related monitoring. Regulatory frameworks for biotechnological and biological products require orthogonal characterization of critical quality attributes, which makes multidimensional liquid chromatography more relevant as protein modalities become more complex. This requirement is extending beyond monoclonal antibodies into antibody-drug conjugates, biosimilars, and newer therapy classes, where simple immunoassay approaches are often not enough. In metabolomics, a 2025 comparison of offline 2D-LC strategies for untargeted human urine profiling showed that HILIC-based second-dimension methods with dilution-based reinjection could maintain feature counts while supporting full automation. That matters for the 2D chromatography market because automation reduces one of the main practical barriers that kept multidimensional systems inside expert-only environments. The same trend is helping move these workflows into larger clinical research programs and higher-throughput academic facilities.

Tightening Quality and Impurity Profiling Requirements in Regulated Testing

The 2D chromatography market is gaining support from a more demanding regulatory environment for analytical procedure development and lifecycle management. ICH Q14 pushed regulated laboratories toward science-based and risk-based method development, which increases the value of platforms that can separate critical impurity pairs with greater confidence and document that performance more clearly.[2]ICH Secretariat, “ICH Q14 Analytical Procedure Development,” International Council for Harmonisation, ich.org This changes investment timing because manufacturers are now more likely to build multidimensional methods earlier in development instead of waiting for failures in late-stage validation. The burden is even more direct in host cell protein work, where LC-MS/MS-based workflows are becoming more central to biologics quality control and related submissions. That is pushing originators and service providers to add better separation depth, stronger software support, and more defensible data packages to their analytical infrastructure. In turn, the 2D chromatography market is drawing demand not only from large drug companies but also from CDMOs that need validated capabilities to remain competitive for biologics contracts.

Growth of Hyphenated 2D Chromatography and Mass Spectrometry Workflows

The 2D chromatography market is also being shaped by the spread of hyphenated workflows that combine multidimensional separation with high-resolution mass spectrometry. A 2024 Analytical Chemistry study showed that a mass-filtering plus multivariate curve resolution workflow applied to LC×LC-HRMS wastewater data identified 25 suspect compounds, outperforming other data-processing approaches examined in the study. This shows that value creation in the 2D chromatography market now depends not only on separation hardware but also on how well the resulting data can be deconvoluted, aligned, and interpreted. The same pattern appears in environmental testing, where a 2025 study validated GC×GC-TOFMS for nine semi-volatile PFAS in soil at sub-part-per-billion levels using thermal desorption sampling. As data handling tools improve, laboratories that once avoided multidimensional systems because of analytical complexity are finding them more practical to deploy. This is broadening the commercial case for integrated LC×LC-MS and GC×GC-MS systems across both discovery and compliance testing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Instrument and Method Validation Cost | -1.0% | Global, acute in MEA and South America | Long term (≥ 4 years) |

| Shortage of Skilled Analysts and System Integrators | -0.8% | APAC, MEA, South America | Medium term (2-4 years) |

| Integration Complexity with Legacy Laboratory Workflows | -0.7% | Global | Medium term (2-4 years) |

| Validation Burden for Regulated and Multi-Site Deployments | -0.6% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Instrument and Method Validation Cost

High capital cost remains one of the clearest restraints on the 2D chromatography market, especially for mid-sized contract laboratories, public testing agencies, and research groups with fixed procurement cycles. Comprehensive LC×LC-MS or GC×GC-TOFMS systems require not only instrument purchase but also software licenses, accessories, service coverage, and ongoing consumable commitments. The validation side is equally demanding because ICH Q2(R2) requires repeatability, intermediate precision, linearity, specificity, and robustness evidence across the full analytical procedure. In practice, that means the cost difference versus one-dimensional HPLC is much larger than the instrument list price alone suggests. The result is that the 2D chromatography market still concentrates fastest adoption among organizations that can absorb both acquisition cost and method qualification time. This also leaves a sizable middle tier of users interested in the capability but slower to commit to full-system deployment.

Shortage of Skilled Analysts and System Integrators

The 2D chromatography market also faces a talent bottleneck because successful deployment requires method development skills, column orthogonality knowledge, detector familiarity, and strong data-processing capability. That combination is still uncommon even in well-funded analytical environments, which slows implementation and raises the risk of underused installed systems. The skills gap is more visible in Asia-Pacific, the Middle East and Africa, and South America, where university and industry training pipelines have not yet scaled at the same pace as instrumentation needs. This affects the 2D chromatography market beyond hiring because laboratories can delay purchase decisions when they are unsure they can support validation, routine operation, and troubleshooting internally. It also extends project timelines after installation, since early runs, transfer work, and workflow optimization can take longer than planned. Until software, automation, and vendor training narrow this gap further, talent availability will remain a practical brake on wider diffusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 2D Liquid Chromatography Stays at the Center While Hybrid Formats Expand

2D liquid chromatography held 52.15% share in 2025, which made it the largest product category in the 2D chromatography market. The segment is also projected to expand at 7.38% CAGR through 2031, which keeps it ahead of other product types on both current scale and forward momentum. Its strength comes from broad compatibility with proteins, peptides, and polar metabolites, especially in workflows tied to biopharma quality control and omics analysis. The installed base is also being supported by online valve-switching formats that reduce analysis cycle time and make routine deployment more feasible than earlier generations. This keeps 2D-LC at the core of the 2D chromatography industry as laboratories seek more practical ways to move beyond single-dimension HPLC. It also helps explain why the segment remains the default entry point for buyers who need multidimensional separation but want operational familiarity.

2D gas chromatography still has an important role in petrochemical profiling, flavor and fragrance work, and environmental screening, where volatile or semi-volatile compounds dominate the matrix. That base is stable because GC×GC paired with TOFMS continues to serve hydrocarbon speciation and non-target contaminant analysis with strong performance in complex samples. A 2025 study also showed that multi-2D LC×LC using a pentafluorophenyl first dimension and 2 complementary second-dimension columns delivered a 91% gain in peak capacity and 30% better peak distribution than standard LC×LC for European medicinal plants.[3]“The Benefits of Multi-2D LC × LC Compared to LC × LC for the Analysis of European Herbal Remedies,” Analytical and Bioanalytical Chemistry, springer.com This supports the view that hybrid and multi-modal systems are becoming a meaningful high-end growth layer within the 2D chromatography market rather than a niche experiment. Shimadzu’s Nexera UC-2D platform also shows how vendors are linking LC×LC with supercritical fluid chromatography to widen use in chiral separations and biopolymer analysis. The broader pattern is that the 2D chromatography industry is deepening around established 2D-LC demand while also widening into more configurable system architectures.

By Application: Life Science Research Rises Faster While Pharma and Biotech Hold the Largest Base

Pharmaceutical and biotechnology applications generated 35.37% share in 2025, which gave them the largest application position in the 2D chromatography market size. Life science research is forecast to record the fastest CAGR at 8.01% through 2031, supported by proteomics, metabolomics, and multi-omics programs that require higher peak capacity than one-dimensional systems can provide. The difference between the two leaders is important because it shows how the 2D chromatography market is being supported by both routine regulated demand and expanding discovery demand. Drug release testing, stability studies, and impurity profiling continue to give pharmaceutical and biotechnology laboratories a steady workflow base. At the same time, grant-backed academic centers and specialist institutes are creating new placements for deeper proteome coverage, biomarker discovery, and systems biology analysis. This makes application growth more balanced than a purely pharma-dependent cycle.

Environmental analysis is also advancing because PFAS monitoring and other non-target screening demands are pushing laboratories toward more capable GC×GC and LC×LC workflows. Food and beverage testing remains relevant for flavor volatiles, pesticide residues, mycotoxins, and adulterant measurement under evolving safety thresholds. Petrochemical and natural gas analysis contributes to a more stable demand, since comprehensive GC-based workflows are already well established for hydrocarbon speciation and process control. The life science research case is being strengthened by expanding evidence on automated and high-content multidimensional methods, including work that supports systematic multi-component profiling of complex formulations with online comprehensive 2D-LC-QTOF-MS. That kind of evidence helps the 2D chromatography market move from expert-only adoption toward broader institutional use across pharmaceutical science, translational medicine, and advanced natural product characterization. It also reduces the risk that future growth will depend on a single end application.

By Detection Technology: Mass Spectrometry Leads Both Current Demand and Future Expansion

Mass spectrometry accounted for 57.61% share in 2025, which made it the dominant detection technology across the 2D chromatography market. It is also projected to grow at 7.91% CAGR through 2031, reflecting its role in identity-confirmed and quantitative analysis across both research and regulated settings. This leadership is closely tied to the spread of workflows where separation alone is not enough, and confirmation at the detector stage is required. As the 2D chromatography market moves into more biologics, exposomics, and contaminant-screening use cases, laboratories are favoring detector setups that strengthen confidence in compound assignment. That preference is especially strong when samples contain many low-abundance or structurally similar analytes. It explains why mass spectrometry now anchors both premium system sales and long-term workflow design.

FID still holds a firm place in GC×GC use, particularly in petrochemical analysis, where linear response, regulatory familiarity, and calibration simplicity remain valuable. UV and visible detection also remain relevant in pharmaceutical settings where target analytes absorb strongly, and the separation itself provides enough selectivity to keep cost per sample under control. The 2D chromatography market, therefore, remains multi-detector in practice even while mass spectrometry captures the center of spending. A 2025 study showed that comprehensive 2D-LC paired with cyclic ion mobility and QTOF-MS added a collision cross-section dimension for profiling phenolic constituents in shea, increasing selectivity beyond both chromatographic dimensions. That kind of detector innovation matters because it expands the performance ceiling for food authentication, natural product work, and other challenging identification tasks. Vendors that support detector-agnostic system design will likely be better placed to serve the widening application range of the 2D chromatography market.

By End Use: Pharmaceutical and Biotech Companies Remain the Largest and Fastest-Growing Buyer Group

Pharmaceutical and biotechnology companies held 28.05% share in 2025, which kept them at the top of end-use demand within the 2D chromatography market. The same group is projected to expand at 8.13% CAGR through 2031, which shows that present leadership and future growth are concentrated in the same buyer category. Their demand base is reinforced by biologics manufacturing, clinical development pipelines, and the analytical burden attached to process impurities, product variants, and release testing. This makes the 2D chromatography market highly responsive to changes in biologics complexity, regulatory documentation, and quality control standards. It also means platform validation, software traceability, and method robustness carry unusual weight in purchasing decisions. In effect, this user group continues to define the highest-value demand center for the 2D chromatography industry.

Academic and research institutes form the next important layer because they drive methodological innovation that later diffuses into industrial laboratories. Clinical and diagnostic laboratories are becoming more important as LC-MS/MS-based testing expands in therapeutic drug monitoring, toxicology, and specialized clinical assays. Bruker’s majority investment in RECIPE in 2025 signals that vendors see diagnostic assay ecosystems as a meaningful extension for chromatography-linked analytical platforms. Environmental laboratories, food testing laboratories, and petrochemical facilities provide additional steady demand, though their growth patterns differ by regulation, contaminant thresholds, and capital availability. This mix broadens the 2D chromatography market beyond one buyer class, even though pharmaceutical and biotech companies remain the strongest source of revenue concentration. It also creates room for vendors to tailor product depth, software, and services around distinct operating environments.

Geography Analysis

North America held 41.23% share in 2025, giving the region the largest position in the 2D chromatography market. The region benefits from a dense biopharmaceutical R&D base, a large installed analytical instrument fleet, and a compliance culture that supports faster adoption of higher-resolution methods. The United States remains the center of that demand because biologics development, host cell protein analysis, and LC-MS/MS-based quality control work continue to expand in both originator and outsourced settings. Regulatory frameworks for analytical procedure development and biological product characterization also reinforce the need for stronger method defensibility and orthogonal separation. This keeps the 2D chromatography market well supported across pharmaceutical companies, contract laboratories, and academic medical centers that contribute to technology development. Canada adds a smaller but stable base through research institutions and regulated testing laboratories that increasingly require advanced analytical platforms.

Europe remained the second-largest regional block in the 2D chromatography market, supported by pharmaceutical manufacturing depth in Germany, France, Italy, and the UK. Public research modernization and advanced omics programs are also helping sustain demand for 2D-LC platforms in university and research institute settings. The region’s demand profile is shaped by strong biologics quality expectations and a continued willingness to invest in high-specification analytical infrastructure when workflow benefits are clear. Germany stands out because solvent efficiency and sustainability are becoming more relevant in institutional procurement, which favors platforms designed to reduce solvent burden over long operating cycles. This makes Europe an important market for both premium system replacement and specialized hybrid configurations that serve advanced separations.

Asia-Pacific is projected to grow at 8.45% CAGR through 2031, which makes it the fastest-expanding regional block in the 2D chromatography market. China is the main volume engine because biosimilar manufacturing scale-up and pharmacopoeial recognition of heart-cut and comprehensive 2D-LC are reducing hesitation around adoption. Agilent’s simultaneous Infinity III LC Series launch in Dalian, the United States, and Germany also signaled that China now ranks as a first-tier launch market for high-precision analytical instruments.[4]Agilent Technologies, “Agilent Revolutionizes HPLC with the Launch of the Agilent Infinity III LC Series,” Agilent Technologies, agilent.com India, Japan, and South Korea add further momentum through contract research, orthogonal characterization needs, and biosimilar quality investment, while Southeast Asia and Australia are benefiting from broader GCxGC deployment in food, environmental, fragrance, and petrochemical testing.

Competitive Landscape

The 2D chromatography market is moderately consolidated at the integrated-system level, with Thermo Fisher Scientific, Agilent Technologies, Waters Corporation, Shimadzu, and LECO Corporation holding strong positions in instrument placements and surrounding software ecosystems. Their advantage is not only hardware depth but also the way proprietary platforms tie together acquisition, processing, auditability, and long-term service support. This raises switching costs after methods are established, which helps these companies defend installed bases and sustain recurring revenue from consumables, software, and maintenance. The 2D chromatography market, therefore, behaves less like a pure instrument sale and more like an ecosystem competition shaped by validation history and workflow continuity. That structure also makes customer retention especially important in regulated laboratories where requalification costs can be high.

Strategic consolidation is reinforcing this position. Waters completed its combination with BD’s Biosciences & Diagnostic Solutions businesses in February 2026, which broadened its reach into clinical and diagnostic testing and expanded the scale of regulated LC-related opportunity around its core analytical portfolio. Bruker secured full ownership of TOFWERK in January 2026, adding ultra-fast TOF-MS capability for environmental chemistry, food testing, air quality, and semiconductor monitoring, all of which align well with multidimensional workflows. Shimadzu then added a 75% stake in Plasmion in March 2026 to secure soft-ionization capability for next-generation mass spectrometers relevant to complex sample analysis. These moves show that leading suppliers are building broader analytical stacks around multidimensional separation rather than treating 2D capability as a narrow instrument niche.

Open space remains strongest in the mid-market, where laboratories need better separation but cannot easily justify full enterprise-scale systems. That is where modular vendors and compact architectures can compete more effectively on price, flexibility, and ease of implementation. Software is becoming an even stronger differentiator in this part of the 2D chromatography market because data alignment, deconvolution, and statistical interpretation now shape user productivity as much as raw instrument performance. LECO’s ChromaTOF Sync 2D launch in March 2025 reflected that shift by focusing on aligned 1D and 2D review, contour visualization, and statistical analysis for non-targeted GC×GC work. Vendors that pair strong data tools with validated workflows and lower-friction automation are likely to widen adoption faster than those relying on hardware specifications alone. This keeps the 2D chromatography market competitive even though the leadership tier remains fairly concentrated.

2D Chromatography Industry Leaders

Agilent Technologies, Inc.

LECO Corporation

Shimadzu Corporation

Thermo Fisher Scientific Inc.

Waters Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Shimadzu Corporation acquired a 75% majority stake in Plasmion GmbH (Augsburg, Germany), securing SICRIT (Soft Ionization by Chemical Reaction In Transfer) ion source technology to develop next-generation mass spectrometers integrated with multidimensional chromatography platforms. The move strengthens Shimadzu's MS business with proprietary ambient ionization capability applicable to complex sample matrices.

- February 2026: Waters Corporation completed its combination with BD's Biosciences & Diagnostic Solutions businesses in a transaction valued at USD 17.5 billion, creating a global life sciences and diagnostics leader. The deal doubles Waters' total addressable market to USD 40 billion, deepening its clinical and diagnostic reach alongside its established LC and MS analytical portfolio.

- January 2026: Bruker Corporation consolidated 100% ownership of TOFWERK AG (Thun, Switzerland) through an additional 60% stake acquisition, adding ultra-fast time-of-flight mass spectrometry for environmental chemistry, air quality monitoring, food and flavor testing, and semiconductor monitoring, all sectors served by GCxGC-TOFMS configurations.

- March 2025: Shimadzu Corporation unveiled its next-generation Nexera UC-2D system, integrating supercritical fluid chromatography (SFC) with LC×LC hybridization for enhanced bioseparation of complex biomolecules, expanding use cases in chiral separation and biopolymer analysis for pharmaceutical and research laboratories in Japan.

Global 2D Chromatography Market Report Scope

The 2D Chromatography Market comprises advanced chromatographic systems that employ two distinct separation mechanisms to achieve superior resolution, sensitivity, and peak capacity for the analysis of complex chemical and biological samples. These systems enable comprehensive characterization of compounds that cannot be effectively resolved using conventional one-dimensional chromatography, supporting high-precision analytical workflows. The market is driven by increasing demand for advanced separation technologies in pharmaceutical and biopharmaceutical research, proteomics, metabolomics, environmental testing, food safety analysis, and petrochemical applications, along with continuous advancements in chromatography instrumentation and detection technologies.

The 2D chromatography market is segmented by product type, application, detection technology, end use, and geography. By product type, it is further divided into 2D gas chromatography, 2D liquid chromatography, and hybrid and multi-modal systems. By application, it is segmented into pharmaceutical and biotechnology applications, environmental analysis, food and beverage testing, life science research, petrochemical and natural gas analysis, and other applications. By detection technology, the market is segmented into mass spectrometry, flame ionization detection, UV and visible detection, and others. By end use, the market is segmented into pharmaceutical and biotechnology companies, academic and research institutes, clinical and diagnostic laboratories, environmental testing laboratories, food and beverage laboratories, petrochemical and industrial testing facilities, and other end users. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| 2D Gas Chromatography |

| 2D Liquid Chromatography |

| Hybrid and Multi-Modal Systems |

| Pharmaceutical and Biotechnology Applications |

| Environmental Analysis |

| Food and Beverage Testing |

| Life Science Research |

| Petrochemical and Natural Gas Analysis |

| Other Applications (Forensic Science, Clinical Toxicology, etc.) |

| Mass Spectrometry |

| Flame Ionization Detection |

| UV and Visible Detection |

| Others (Charged Aerosol Detector (CAD), Fluorescence Detection (FLD), etc.) |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Clinical and Diagnostic Laboratories |

| Environmental Testing Laboratories |

| Food and Beverage Laboratories |

| Petrochemical and Industrial Testing Facilities |

| Other End Uses (CDMOs, CROs, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | 2D Gas Chromatography | |

| 2D Liquid Chromatography | ||

| Hybrid and Multi-Modal Systems | ||

| By Application | Pharmaceutical and Biotechnology Applications | |

| Environmental Analysis | ||

| Food and Beverage Testing | ||

| Life Science Research | ||

| Petrochemical and Natural Gas Analysis | ||

| Other Applications (Forensic Science, Clinical Toxicology, etc.) | ||

| By Detection Technology | Mass Spectrometry | |

| Flame Ionization Detection | ||

| UV and Visible Detection | ||

| Others (Charged Aerosol Detector (CAD), Fluorescence Detection (FLD), etc.) | ||

| By End Use | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Clinical and Diagnostic Laboratories | ||

| Environmental Testing Laboratories | ||

| Food and Beverage Laboratories | ||

| Petrochemical and Industrial Testing Facilities | ||

| Other End Uses (CDMOs, CROs, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the 2D chromatography space by 2031?

It is forecast to reach USD 965.75 million by 2031, rising from USD 695.88 million in 2026 at a 6.75% CAGR over 2026-2031.

Which product category currently leads revenue?

2D liquid chromatography led with 52.15% share in 2025 and also recorded the fastest product CAGR at 7.38% through 2031.

Why are pharmaceutical and biotechnology users so important?

They held 28.05% share in 2025 and are expected to grow at 8.13% CAGR because biologics pipelines and regulated quality control require deeper analytical characterization.

Which application is expanding the fastest?

Life science research is the fastest-growing application with an 8.01% CAGR through 2031, driven by proteomics, metabolomics, and wider multi-omics adoption.

Which region offers the strongest near-term demand?

North America remains the largest regional base with 41.23% share in 2025, while Asia-Pacific offers the fastest expansion at 8.45% CAGR through 2031.

What is the biggest barrier to wider adoption?

High system cost and the added validation burden remain the main barriers, especially for mid-sized labs that must fund instruments, software, service, and multidimensional method qualification together.

Page last updated on: