Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 26.61 Billion |

| Market Size (2030) | USD 44.59 Billion |

| Growth Rate (2025 - 2030) | 10.88% CAGR |

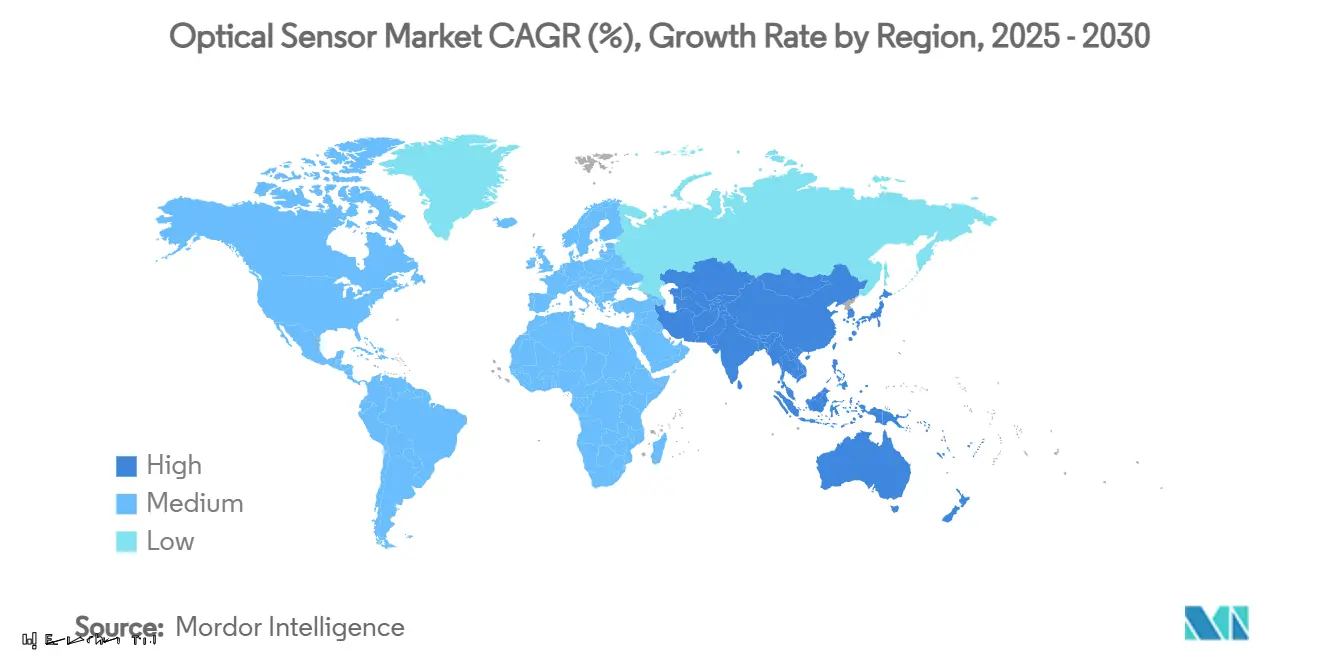

| Fastest Growing Market | Middle East and North Africa |

| Largest Market | Asia Pacific |

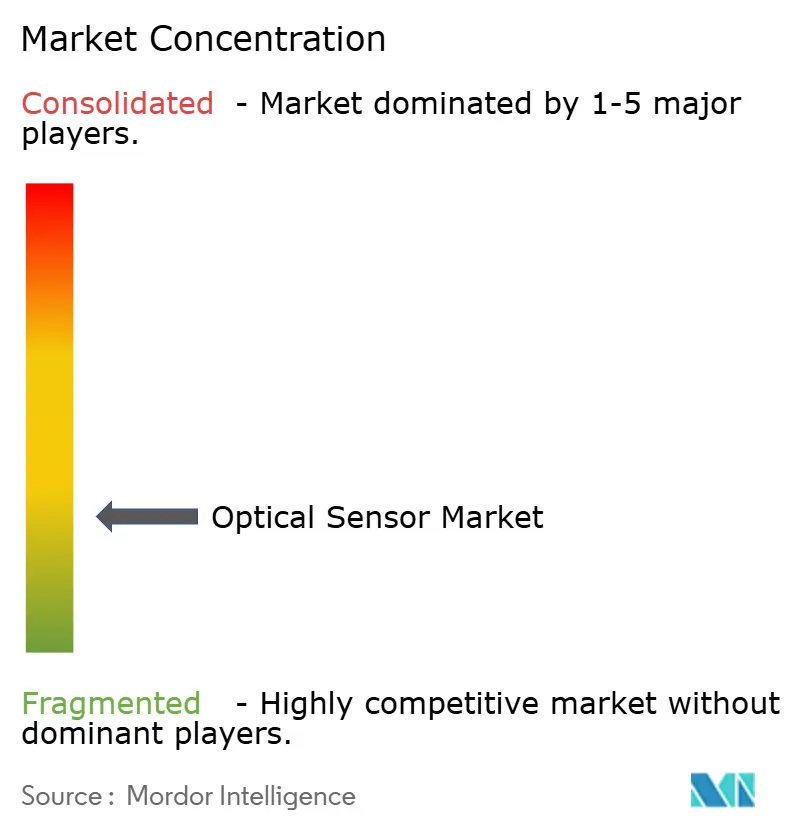

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Optical Sensor Market Analysis by Mordor Intelligence

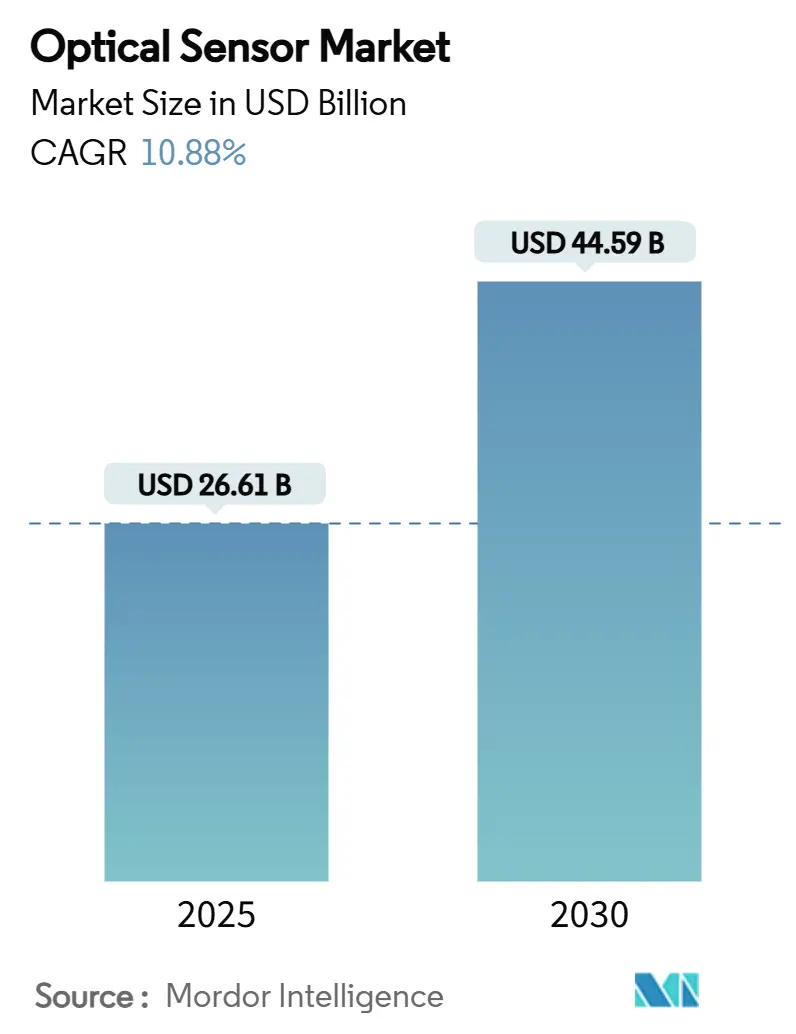

The optical sensors market reached USD 26.61 billion in 2025 and is projected to climb to USD 44.59 billion by 2030, advancing at a 10.88% CAGR. Consistent regulatory pressure on automotive safety, environmental monitoring, and data privacy is steering demand toward integrated, cost-efficient silicon-photonics-based designs. Price drops in wafer-level photonics and the proliferation of AI workloads at the network edge are accelerating sensor adoption in 5G infrastructure, autonomous vehicles, and distributed fiber-optic monitoring. Material-supply risks around high-purity silica and germanium underscore the need for diversified sourcing, while miniaturization requirements in wearables and smartphones continue to shift volume production to Asia-Pacific. Competitive intensity is rising as smaller firms deploy photonic integration to rival long-established semiconductor players. [1]STMicroelectronics, “ST releases first 3D sensor with meta-optics,” Electro Optics, electrooptics.com

Key Report Takeaways

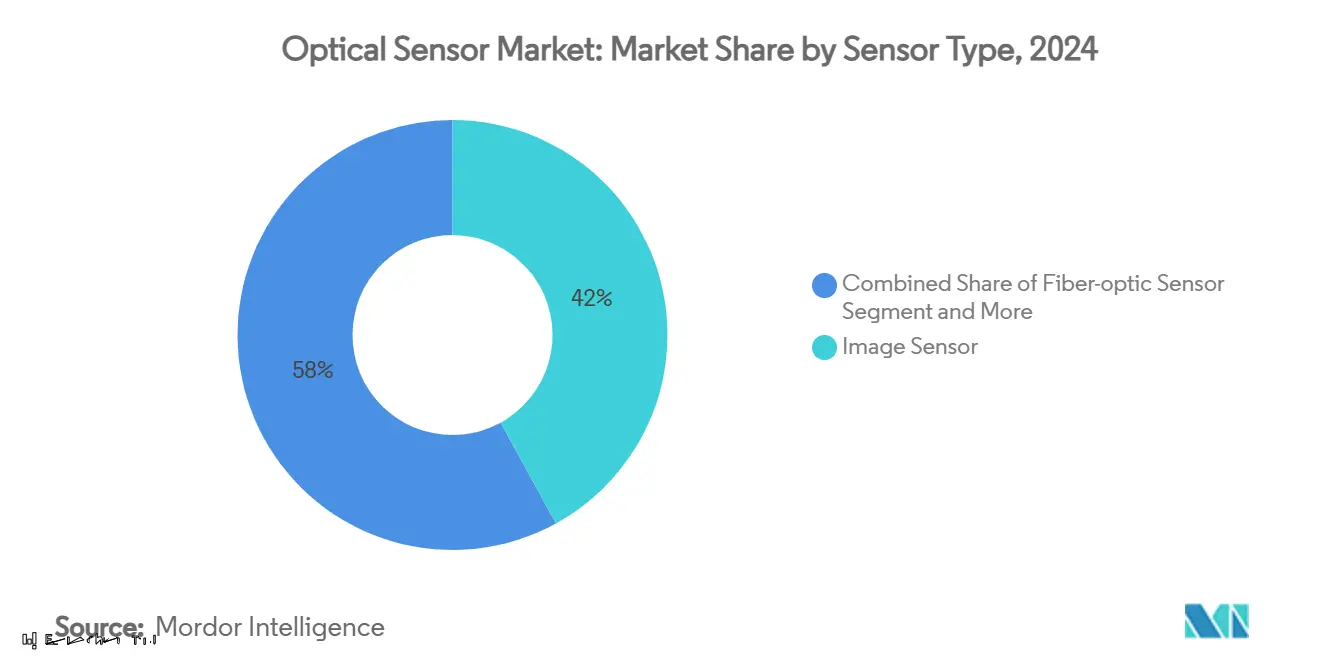

- By sensor type, image sensors led with 42% optical sensors market share in 2024; fiber-optic sensors are on track to expand at a 12.7% CAGR through 2030.

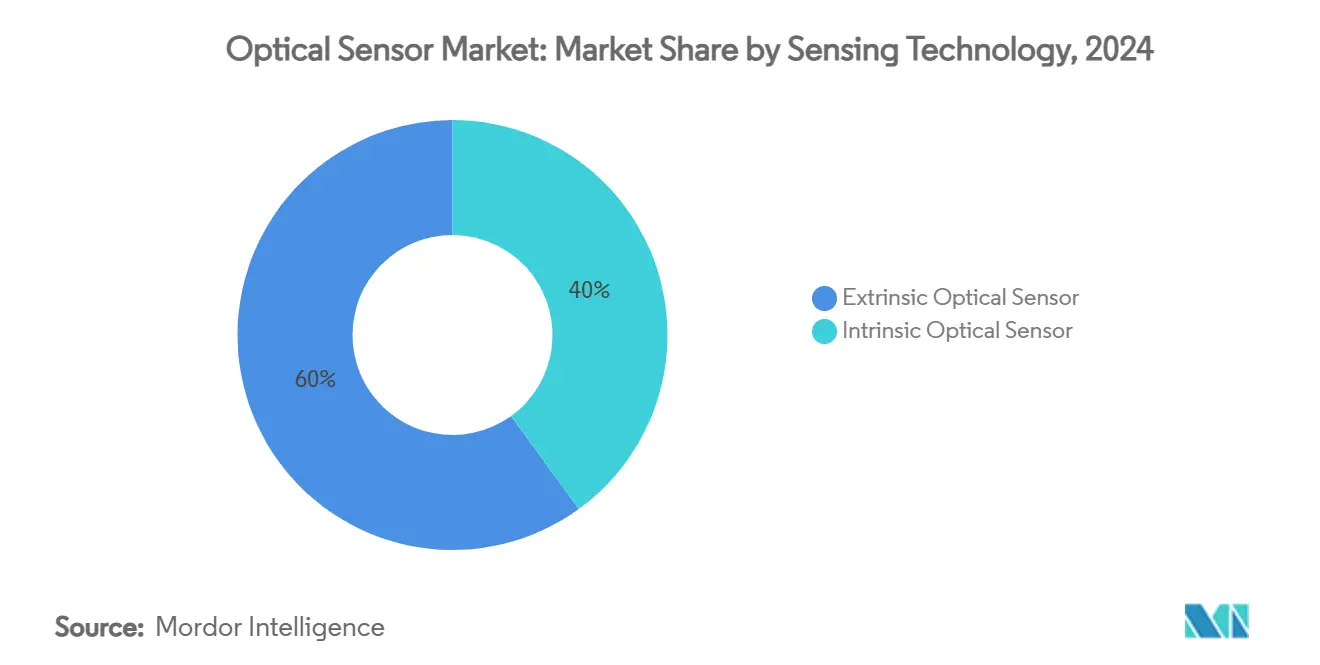

- By sensing technology, extrinsic sensors held 60% of the global total in 2024, while intrinsic designs are set to grow at 11.3% through 2030.

- By end-user, consumer electronics accounted for 28% of the optical sensors market size in 2024; automotive and transportation are forecast to advance at 14.2% CAGR to 2030.

- By geography, Asia-Pacific captured 33% revenue share in 2024; the Middle East is expected to register the fastest regional CAGR at 13.6% to 2030.

- Sony, Hamamatsu, and STMicroelectronics collectively controlled below 25% of global shipments, indicating a moderately fragmented landscape.

Global Optical Sensor Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization Demand for Wearable Optics in APAC Consumer Electronics | 1.80% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Industrial IoT Adoption Fueling Fiber-optic Sensors in Harsh Environments | 2.10% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Automotive ADAS & LiDAR Integration Accelerating NIR Image Sensors in Europe | 1.60% | Europe & North America, expanding to APAC | Medium term (2-4 years) |

| Rapid 5G & Edge-Data-Center Roll-out Requiring High-Speed Optical Sensing | 1.90% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Stricter Environmental-Monitoring Regulations Driving Distributed Fiber Sensing in North America | 1.40% | North America, expanding to Europe | Long term (≥ 4 years) |

| Advances in Silicon Photonics Lowering BOM Cost for Integrated Optical Sensors | 2.20% | Global | Medium term (2-4 years) |

Source: Mordor Intelligence

Miniaturization Demand for Wearable Optics in APAC Consumer Electronics

AR glasses and smart wearables now require sub-millimeter optical stacks that still meet luminous-efficiency targets. Single-layer meta-optics introduced by STMicroelectronics cut lens height by 70%, permitting under-display proximity sensing in flagship smartphones. Indium-phosphide VCSELs are replacing GaAs emitters, delivering tighter beam divergence for space-constrained devices. APAC contract manufacturers leverage these developments to secure design wins from Western brands, reinforcing the region’s 33% revenue share position.

Industrial IoT Adoption Fuelling Fiber-optic Sensors in Harsh Environments

Distributed fiber sensing provides kilometre-scale temperature and strain data immune to electromagnetic interference, enabling predictive maintenance across refineries, pipelines, and high-voltage substations. Rockwell Automation notes that early-warning analytics on such data can eliminate 30% of unplanned downtime in process industries. Coupling AI-based pattern recognition with continuous optical feedback is becoming a cornerstone of Industry 4.0 strategies in North America and Europe. [3]Theresa Houck, “8 Key Industrial Automation Trends in 2025,” Rockwell Automation, rockwellautomation.com

Automotive ADAS & LiDAR Integration Accelerating NIR Image Sensors in Europe

EU mandates for advanced driver-assistance systems are pushing automakers to adopt 905 nm and 1,550 nm NIR sensors built to withstand −40 °C to +125 °C cycles. STMicroelectronics’ automotive-grade global-shutter imagers now achieve 400 cm range with 60 Hz refresh, supporting real-time 3-D mapping. German OEMs are integrating multi-modal sensor fusion that blends NIR cameras with MEMS-LiDAR, opening a high-margin supply avenue for qualified component vendors.

Advances in Silicon Photonics Lowering Bill-of-Materials Cost for Integrated Optical Sensors

Foundry-scale wafer processing unites photodiodes, waveguides, and readout ASICs on a single die, driving optical sensors market unit costs below USD 10 while raising functional consistency. Ayar Labs’ optical interconnect funding round underscores rising confidence in photonic integration for AI servers. These economics encourage mid-tier suppliers to launch highly integrated digital-output modules that directly interface with microcontrollers, narrowing the gap with incumbent multinationals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain Constraints for High-purity Silica Preforms | -1.70% | Global, acute impact in APAC manufacturing | Short term (≤ 2 years) |

| Price Sensitivity in Low-end Smartphones Limiting Advanced Proximity Sensors | -0.90% | APAC & emerging markets | Medium term (2-4 years) |

| Calibration Complexity of Multi-spectral Sensors Deterring SME Uptake | -0.80% | Global, concentrated in Europe & North America SME markets | Long term (≥ 4 years) |

| Data-Privacy Concerns Around Biometric Optical Sensors in EU | -1.10% | Europe, with spillover to privacy-conscious markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Supply-Chain Constraints for High-Purity Silica Preforms

Quartz mined from a handful of Appalachian deposits accounts for most global preform feedstock; Hurricane-induced outages in 2024 exposed how a single locale can squeeze optical-fiber availability. Coupled with China’s export restrictions on germanium, manufacturers are negotiating long-term contracts at price premiums, delaying large-volume deployments of distributed fiber solutions. Synthetic-silica start-ups are emerging, but commercial scaling remains two to three years out.

Data-Privacy Concerns Around Biometric Optical Sensors in EU

The EU AI Act classifies facial-recognition and iris-scanning systems as high-risk, mandating on-device processing and extensive risk logs. Implementing privacy-preserving edge analytics raises bill-of-materials cost by 20-30%, squeezing margins for mass-market OEMs. Sensor vendors that can embed secure on-chip template generation are gaining preferred-supplier status among compliance-focused integrators. [2]European Commission, “Proposal for a Regulation laying down harmonised rules on artificial intelligence,” europa.eu

Segment Analysis

By Sensor Type: Image Sensors Hold Leadership as Fiber-Optic Momentum Builds

Image sensors retained 42% share of the optical sensors market in 2024, buoyed by multi-camera smartphones and ADAS roll-outs. Sony’s stacked CMOS technology pushes 120 fps 4-K capture, meeting machine-vision tolerances for factory automation. Fiber-optic sensors, while smaller in absolute revenue, are forecast to post the highest 12.7% CAGR as infrastructure operators shift toward kilometre-scale structural health monitoring. This traction lifts the optical sensors market size for fiber-optic solutions from USD 4.7 billion in 2025 toward USD 8.6 billion by 2030. Distributed acoustic sensing, pipeline security, and perimeter intrusion systems are the chief volume drivers.

Diversification across photoelectric, ambient light, and proximity sensors remains steady, although ASP erosion pressures component suppliers. Ultra-mini proximity modules like Vishay’s 0.5 mm-thick device cater to bezel-less phone designs, while global-shutter industrial cameras eliminate motion blur in robotic pick-and-place. Multi-spectral imagers within the “Others” bucket are gaining double-digit growth, supporting precision agriculture and food-safety fluorescence assays.

Note: Segment shares of all individual segments available upon report purchase

By Component: Photodetectors Drive Performance Differentiation

Cutting-edge photodetectors such as single-photon avalanche diodes (SPADs) and avalanche photodiodes (APDs) sell at premium prices even though they ship in lower volumes than standard photodiodes. SPAD arrays deliver picosecond-level time-of-flight data that LiDAR systems rely on for accurate distance readings in self-driving cars. On the emitter side, design teams are moving from LEDs to VCSELs and edge-emitting lasers to gain higher optical power and tighter spectral control; VCSELs also couple easily into fiber while meeting consumer eye-safety rules.

Optics and filters contribute the most value per gram because their precision coatings and tight tolerances are hard for new entrants to match. Meta-optics is shaking up lens design by replacing multi-element stacks with single, patterned layers that keep performance but trim size and weight. Processing electronics are following the same path: more functions now sit on the sensor die, so edge AI can run locally, cutting latency and easing bandwidth demands.

By Sensing Technology: Intrinsic Integration Closes the Gap with Extrinsic Designs

Extrinsic configurations, where the fiber guides light to an external transducer, controlled 60% of 2024 shipments, but intrinsic devices are accelerating at 11.3% CAGR thanks to silicon-photonics wafer bonding that co-locates detection and processing on a monolithic substrate. That trajectory narrows the performance gap and simplifies calibration, enabling integrated solutions for UAV-borne gas analysis and OEM-installed structural monitoring.

The optical sensors market size for intrinsic devices is projected to reach USD 18.9 billion by 2030, supported by wafer-level testing that boosts throughput and curtails per-lot variance. Extrinsic sensors will retain niches in high-temperature oil-and-gas wells and corrosive chemical reactors, where remote sensing heads shield electronics from hostile conditions. Hybrid designs that switch between intrinsic and extrinsic modes via reconfigurable photonic circuits are beginning to surface in prototype deployments.

By Output: Digital Integration Accelerates System Simplification

Digital-output sensors are growing faster because they drop straight into microcontrollers and need little or no external analog circuitry. Many now house their own analog-to-digital converters plus basic signal processing, cutting parts count and design time. Features such as programmable gain and thresholds let one device cover multiple jobs without hardware tweaks.

Analog options still matter when systems need continuous readings or microsecond-level response, for example in high-speed control loops. In those settings, skipping digital conversion avoids the latency that could upset system stability. Ultimately, whether designers pick analog or digital hinges on the larger system architecture, not on raw sensor capability.

Geography Analysis

Asia-Pacific accounted for 33% of 2024 revenue, reflecting its tight coupling of component fabs, module assembly, and consumer electronics brands. Contract manufacturers in China and Vietnam now produce proximity-sensor die at sub-USD 0.09 ASP, reinforcing the region’s cost leadership. Japan’s precision optics ecosystem supports automotive LiDAR modules meeting AEC-Q102 grade, while South Korea’s foundries push the envelope on stacked-image-sensor yields.

Europe’s outlook centers on regulatory-driven applications. German Tier-1 suppliers are booking long-term contracts for NIR imaging arrays that comply with Euro NCAP vision-system mandates. Fiber-optic gas-leak monitoring around North Sea platforms is expanding as EU methane-emissions rules tighten. GDPR compliance is steering OEMs toward on-device biometric analysis, supporting intrinsic sensor adoption.

North America continues to test emerging concepts ahead of other regions. Venture funding into photonic start-ups exceeded USD 700 million in 2024-2025, with a focus on edge-AI optical links. Environmental agencies deploy distributed fiber networks for methane quantification, often financed through green-bond issuances. Meanwhile, Saudi Arabia and the UAE are installing hyperspectral camera arrays across smart-city projects, driving the Middle East’s 13.6% CAGR outlook.

Competitive Landscape

The playing field remains moderately fragmented. Sony holds leadership in smartphone imaging, Hamamatsu dominates scientific photomultiplier tubes, and STMicroelectronics is scaling silicon-photonics TOF modules. However, their combined shipments account for less than one-quarter of the optical sensors market, leaving room for niche disruptors. Integrated-photonic start-ups leverage foundry access and AI-acceleration blocks to address emerging needs such as chip-to-chip optical links and in-situ environmental analytics.

Strategic activity favours acquisition over greenfield R&D. Teledyne’s purchase of Excelitas’ aerospace division broadens space-qualified sensing portfolios, while the Hamamatsu-NKT Photonics merger secures laser-source supply continuity. Partnerships between sensor players and AI-edge-compute vendors aim to deliver turnkey modules for autonomous vehicles and industrial robots. Branding now emphasizes security-by-design to satisfy privacy regulations.

Pricing pressure persists at the low end, particularly in analog photoelectric devices, yet the integrated-digital segment enjoys stable margins linked to system-level savings. Suppliers with captive wafer fabs and optics-coating lines retain resilience against raw-material fluctuations, whereas fab-less firms focus on differentiated design IP and flexible supply agreements.

Optical Sensor Industry Leaders

-

Sony Group Corporation

-

ams-OSRAM AG

-

Hamamatsu Photonics K.K.

-

ON Semiconductor Corp.

-

Keyence Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Ruhr-University Bochum and Fraunhofer Institute unveiled HyperNIR hyperspectral imaging for real-time microplastics detection in recycling streams.

- February 2025: Teledyne Technologies acquired Excelitas Technologies’ aerospace and defense business for USD 710 million, enlarging its space-sensor portfolio.

- January 2025: Ayar Labs raised USD 155 million Series C to advance chip-to-chip optical interconnects for AI accelerators.

- December 2024: Nokia closed its USD 2.3 billion purchase of Infinera, integrating optical-network expertise for 5G backhaul.

Global Optical Sensor Market Report Scope

Optical sensors are light-based biosensors based on the change in wavelength measurement after the analyte's interaction with the bio-recognition element. The purpose of an optical sensor is to measure a physical quantity of light and, depending on the type of sensor, then translate it into a form readable by an integrated measuring device.

The Optical Sensor Market is segmented by Type (Extrinsic Optical Sensor, Intrinsic Optical Sensor), Sensor Type (Fiber Optic Sensor, Image Sensor, Photoelectric Sensor, Ambient Light, and Proximity Sensor), Application (Industrial, Medical, Biometric, Automotive, Consumer Electronics), and Geography (North America, Europe, Asia Pacific, Latin America, MEA). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments. The impact of Covid-19 on the market and its impacted components are also covered under the scope of the study. Further, the disruption of the factors affecting the market's expansion has been covered in the survey regarding drivers and restraints.

| By Sensor Type | Image Sensor | ||

| Fiber-optic Sensor | |||

| Photoelectric Sensor | |||

| Ambient Light & Proximity Sensor | |||

| Others (Position, Touch, Multi-spectral) | |||

| By Sensing Technology | Extrinsic Optical Sensor | ||

| Intrinsic Optical Sensor | |||

| By Component | Photodetectors (Photodiodes, APDs, SPADs) | ||

| Light Sources (LED, VCSEL, Laser) | |||

| Optics and Filters | |||

| ICs and Processing Electronics | |||

| By Wavelength | Ultraviolet (100-400 nm) | ||

| Visible (400-700 nm) | |||

| Near-Infrared (700-1400 nm) | |||

| Short-Wave IR / Mid-IR (>1400 nm) | |||

| By Output | Analog | ||

| Digital | |||

| By End-user Application | Consumer Electronics | ||

| Industrial Automation and Robotics | |||

| Automotive and Transportation | |||

| Healthcare and Medical Devices | |||

| Biometrics and Security | |||

| Aerospace and Defense | |||

| Energy and Environmental Monitoring | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East | Israel | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

By Sensor Type

| Image Sensor |

| Fiber-optic Sensor |

| Photoelectric Sensor |

| Ambient Light & Proximity Sensor |

| Others (Position, Touch, Multi-spectral) |

By Sensing Technology

| Extrinsic Optical Sensor |

| Intrinsic Optical Sensor |

By Component

| Photodetectors (Photodiodes, APDs, SPADs) |

| Light Sources (LED, VCSEL, Laser) |

| Optics and Filters |

| ICs and Processing Electronics |

By Wavelength

| Ultraviolet (100-400 nm) |

| Visible (400-700 nm) |

| Near-Infrared (700-1400 nm) |

| Short-Wave IR / Mid-IR (>1400 nm) |

By Output

| Analog |

| Digital |

By End-user Application

| Consumer Electronics |

| Industrial Automation and Robotics |

| Automotive and Transportation |

| Healthcare and Medical Devices |

| Biometrics and Security |

| Aerospace and Defense |

| Energy and Environmental Monitoring |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the optical sensors market?

The optical sensors market size reached USD 26.61 billion in 2025 and is forecast to hit USD 44.59 billion by 2030.

Which sensor type is growing fastest?

Fiber-optic sensors are projected to grow at 12.7% CAGR through 2030, the highest among all sensor categories.

Why are silicon-photonics-based sensors gaining traction?

Wafer-level photonic integration cuts per-unit cost below USD 10 while combining detection, signal routing, and processing on the same die, enabling affordable high-performance modules.

How is regulation shaping demand in Europe?

EU safety rules accelerate adoption of NIR image sensors for ADAS, and GDPR/AI Act provisions are pushing on-device biometric processing, favouring integrated optical designs.

Which region will grow fastest through 2030?

The Middle East leads regional growth with a 13.6% CAGR, driven by smart-city infrastructure and security deployments.

What is the main supply-chain risks?

High-purity silica and germanium shortages pose short-term constraints, necessitating diversification into synthetic silica and alternative IR detector materials.

Page last updated on: July 9, 2025