Market Overview

| Study Period | 2019 - 2030 |

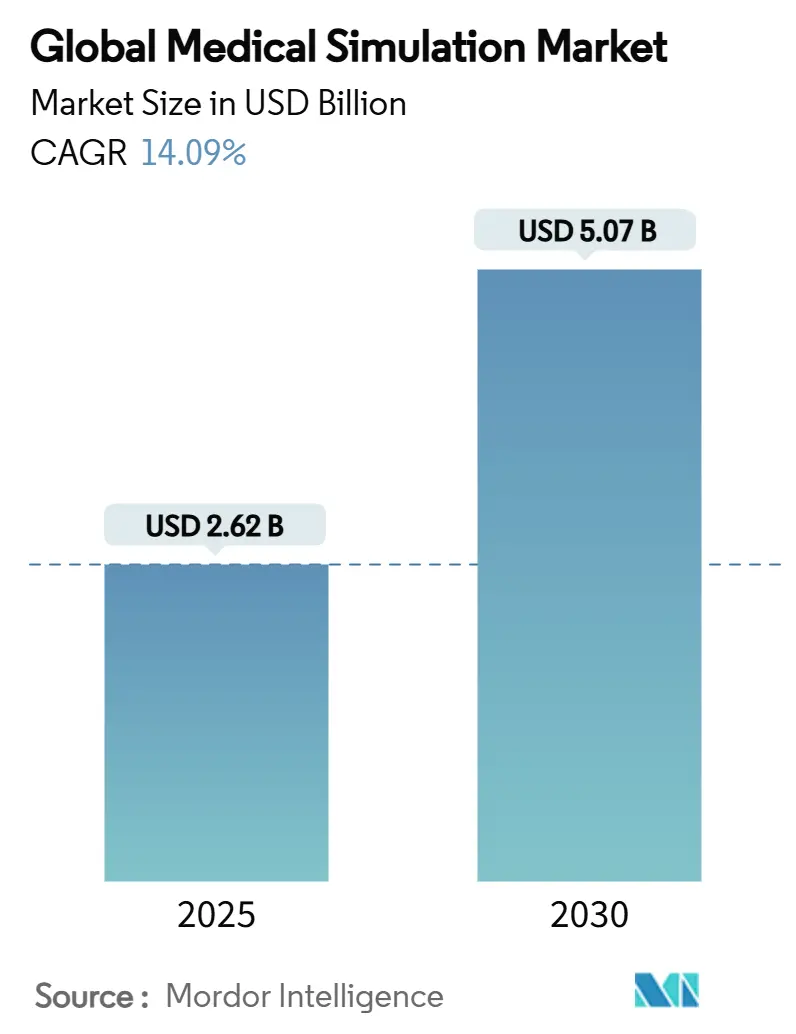

| Market Size (2025) | USD 2.62 Billion |

| Market Size (2030) | USD 5.07 Billion |

| Growth Rate (2025 - 2030) | 14.09% CAGR |

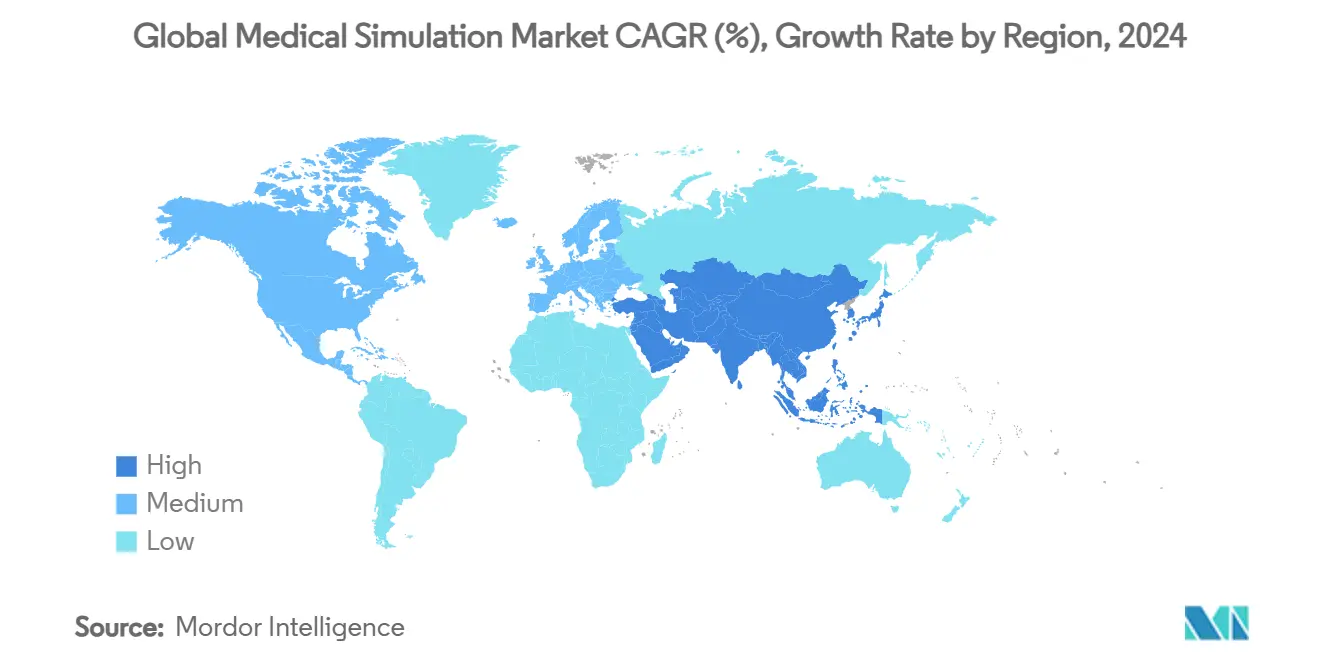

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Medical Simulation Market Analysis by Mordor Intelligence

The medical simulation market stands at USD 2.62 billion in 2025 and is forecast to reach USD 5.07 billion in 2030, advancing at a 14.09% CAGR. A convergence of haptic-enabled virtual reality, artificial-intelligence competency analytics and tightening patient-safety mandates is reshaping how clinicians acquire and maintain skills. Institutions are migrating from hardware-centric labs toward flexible, cloud-supported platforms that extend training beyond campus walls. Consolidation among technology suppliers is accelerating, led by Madison Industries’ 2024 purchase of CAE Healthcare, as vendors seek scale to fund R&D in haptics, force feedback and predictive analytics. North America remains the largest regional customer for the medical simulation market, yet Asia-Pacific is growing faster on the back of hospital expansion and government-funded medical-education capacity upgrades.

Key Report Takeaways

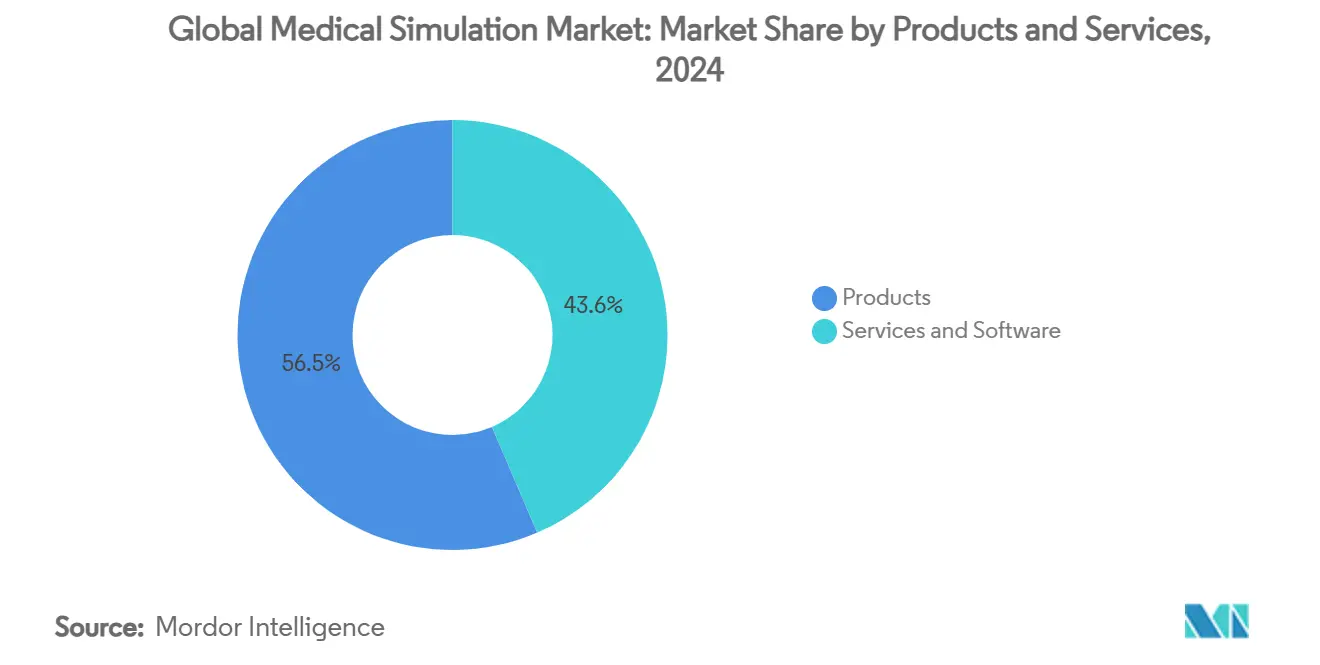

- By product & service, Products led with 56.45% revenue share of the medical simulation market in 2024; Services & Software are projected to grow at a 14.71% CAGR through 2030.

- By fidelity, low-fidelity platforms captured 44.35% of the medical simulation market share in 2024, while high-fidelity solutions are expected to expand at a 14.61% CAGR to 2030.

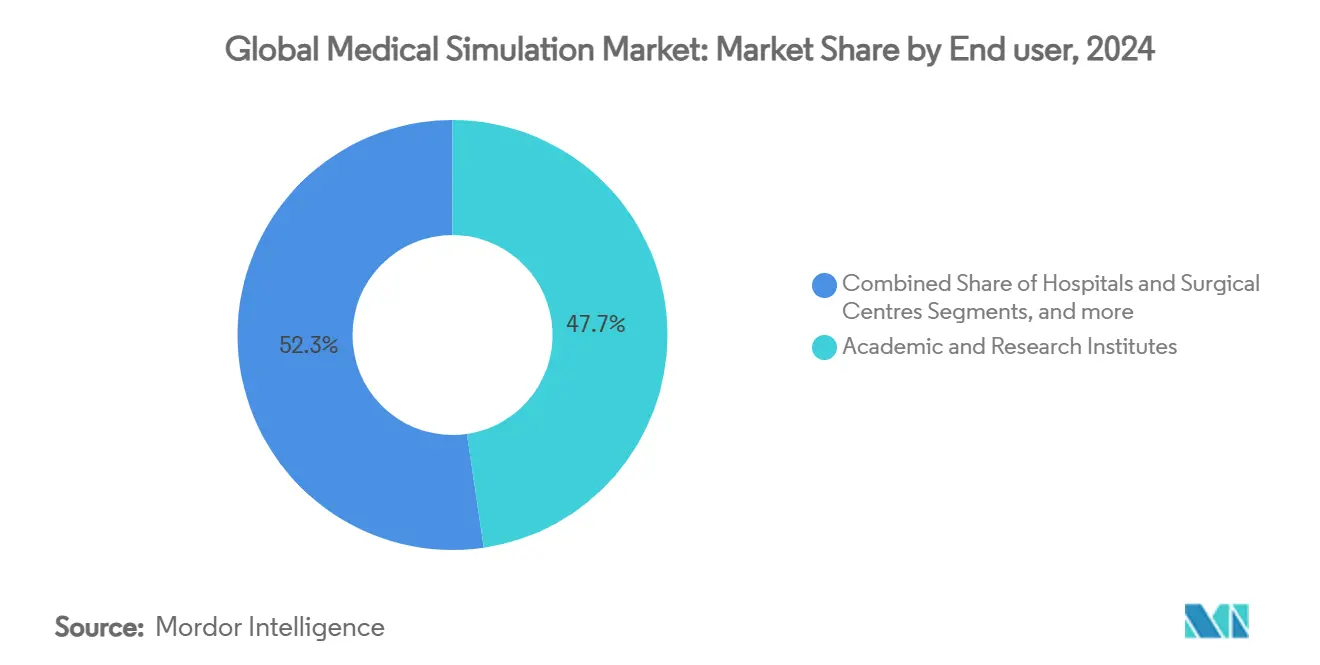

- By end user, Academic & Research Institutes held 47.67% of the medical simulation market size in 2024; Hospitals & Surgical Centres record the fastest CAGR at 14.68% to 2030.

- By delivery mode, on-premise simulation labs accounted for 54.56% of the medical simulation market size in 2024, yet cloud-based platforms are advancing at a 14.56% CAGR.

- By geography, North America commanded 41.45% of 2024 revenue, whereas Asia-Pacific is poised for a 14.78% CAGR through 2030.

Global Medical Simulation Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in haptic-enabled & VR/AR simulators | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing focus on patient-safety mandates & "zero-harm" initiatives | +2.1% | Global, led by developed markets | Short term (≤ 2 years) |

| Rising demand for minimally-invasive & robotic procedures | +1.9% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Expansion of simulation accreditation programs (SSH, ASPIRE) | +1.4% | Global, with emphasis on academic institutions | Medium term (2-4 years) |

| AI-driven competency analytics for personalised skill-scoring | +1.6% | North America & Europe initially, global expansion | Long term (≥ 4 years) |

| Government incentives for carbon-neutral remote simulation labs | +0.8% | Europe & North America, selective APAC markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Technological Advances in Haptic-Enabled & VR/AR Simulators

Haptic feedback and immersive visualisation have moved from research labs into mainstream curricula. A global survey of 156 dental schools confirmed strong interest but highlighted technical and cost barriers, with 35% citing system complexity and 28% flagging budget shortfalls. Successful early adopters now use superior training outcomes as a recruitment tool for both students and faculty. NVIDIA’s joint work with GE HealthCare on the Isaac for Healthcare platform illustrates crossover into diagnostic imaging, broadening the addressable medical simulation market. Portable units such as RetinaVR are also lowering entry costs, signalling that hardware constraints are diminishing.

Growing Focus on Patient-Safety Mandates & Zero-Harm Initiatives

Simulation has shifted from optional enhancement to compliance requirement as regulators tighten safety metrics. The Society for Simulation in Healthcare has accredited more than 240 centres that must satisfy debriefing and professional-integrity standards. Endorsement programs from INACSL are creating a premium tier of certified providers that command higher tuition fees. A multi-centre study recorded competency scores rising from 6.3 to 25.7 out of 30 after simulation intervention, reinforcing budget justification for new labs. Health systems now treat simulation budgets as core infrastructure rather than discretionary expenditure.

Rising Demand for Minimally-Invasive & Robotic Procedures

Robot-assisted surgery magnifies the urgency for scalable training. Workforce forecasts warn of a 55,000–150,000 shortfall of surgeons qualified for robotic procedures by 2030. VR curricula have delivered stronger psychomotor scores than traditional methods, yet high device prices confine adoption to well-funded centres. Synthetic organ models produced by 3D printing are replacing animal models, improving repeatability and reducing ethical concerns. Vendors able to bundle simulators with robotics service contracts are carving out durable revenue streams, particularly in APAC where procedure volumes are catching up rapidly.

AI-Driven Competency Analytics for Personalised Skill-Scoring

AI algorithms are now classifying surgical expertise with 92% accuracy and 100% sensitivity in spinal-task assessment. The US Department of Defense catalogued 120 medical AI use cases and embedded simulation into its MHS Digital Health Strategy, underscoring institutional commitment. Multi-agent platforms cut scenario-development time by up to 80%, but require strong governance to avoid algorithmic bias. Explainable-AI frameworks, such as the Virtual Operative Assistant, improve trainee acceptance by revealing performance-grading logic.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & lifecycle costs of full-mission simulators | -2.3% | Global, particularly acute in developing markets | Short term (≤ 2 years) |

| Funding gaps in developing economies' training budgets | -1.8% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Faculty-training & curriculum-integration complexity | -1.2% | Global, with emphasis on academic institutions | Medium term (2-4 years) |

| Cyber-security & learner-data privacy concerns in cloud platforms | -0.9% | Global, heightened in regulated markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

High Capital & Lifecycle Costs of Full-Mission Simulators

Start-up costs for a comprehensive simulation centre range from USD 165 to 17,000 per square foot, restricting access in resource-constrained regions. This price wedge has fuelled R&D into hybrid models that blend VR screens with 3D-printed components, reducing hardware outlays while preserving tactile cues. Improvised task trainers are bridging gaps temporarily, although maintenance and calibration expenses remain a hurdle. Budget pressure is compounded by the rise in cybersecurity spending, forecast to reach 12-15% of hospital IT allocations, further squeezing capital availability.

Cyber-Security & Learner-Data Privacy Concerns in Cloud Platforms

Healthcare ranks among the most targeted industries for cyberattacks, and simulation vendors must now meet stricter FDA cybersecurity disclosure rules. India’s hospital network alone has entered the global top five for attack volume, prompting institutions to ring-fence sensitive learner data with on-premise solutions despite higher costs. US Department of Defense red-team testing exposed vulnerabilities and bias in medical AI stacks, reinforcing market caution. Smaller providers struggle to finance the required security controls, slowing cloud simulation rollouts, particularly in high-regulation regions.

Segment Analysis

By Products & Services: Software Solutions Drive Market Evolution

Products accounted for 56.45% of revenue in 2024, yet Services & Software are growing 14.71% annually as institutions pivot toward content libraries and analytics-as-a-service. The medical simulation market size for Services & Software is projected to expand at 14.71% CAGR between 2025 and 2030. Web-hosted platforms enable multi-site deployments without replicating costly manikins, reducing per-learner spend. AI-based scenario builders mitigate faculty shortages by auto-generating objectives, scripts and assessment rubrics. Within hardware, interventional simulators remain premium-priced due to laparoscopic and robotic curriculum demand. Task trainers, meanwhile, appeal to cost-sensitive buyers focusing on discrete competencies. Patient simulators retain a foothold in undergraduate programs but face slower replacement cycles. Vendors increasingly bundle force-feedback patents into surgical offerings, raising switching costs and locking in maintenance revenue streams.

Second-generation cloud modules now integrate directly with learning-management systems for single-sign-on, easing adoption. Subscription pricing shifts capital expenditure to operating budgets, pleasing finance departments that seek predictable cash flows. Open-API architectures enable hospital IT teams to feed performance data into broader workforce analytics dashboards, creating cross-departmental value. As software ecosystems mature, providers differentiate through fidelity of physics engines and real-time data capture granularity rather than raw polygon count. Competitive intensity is rising among pure-play SaaS entrants that undercut legacy hardware-centric suppliers.

Note: Segment shares of all individual segments available upon report purchase

By Fidelity: High-Fidelity Innovation Accelerates Despite Low-Fidelity Dominance

Low-fidelity solutions kept 44.35% share of the medical simulation market in 2024 because they are affordable, portable and easy to maintain. High-fidelity systems, however, deliver superior cognitive immersion and are growing at 14.61% CAGR through 2030. Studies show experimental groups using high-fidelity manikins achieved mean competency scores of 73.3, outperforming control cohorts at 61.4. The medical simulation market size for high-fidelity platforms will therefore outpace general market growth. Medium-fidelity devices fill a niche for institutions balancing realism and budget, often serving as a stepping stone toward full immersive suites.

R&D focus has shifted from mannequin mechanics to software-defined fidelity where physics-based engines generate realistic tissue response in VR settings. Hybrid configurations marry head-mounted displays with 3D-printed organ blocks so learners gain both spatial orientation and tactile cues. As sensor prices fall, even low-fidelity task trainers are adding motion-tracking modules, blurring segmentation lines. The market trend toward outcome-based procurement prompts buyers to evaluate fidelity on learning gains rather than technical specification sheets. Vendors that publish peer-reviewed validation studies are strengthening their go-to-market propositions, especially in accreditation-driven regions.

By End User: Hospital Adoption Accelerates Training Transformation

Academic & Research Institutes held 47.67% revenue in 2024 and remain core customers, yet hospitals are the fastest-growing buyers at 14.68% CAGR. Rising litigation risk and value-based reimbursement models push hospitals to invest in competency management. Cleveland Clinic’s VR initiative demonstrated unified training across multiple campuses but exposed staff bandwidth limitations that vendors now address with turnkey services. The medical simulation market share of hospitals will therefore rise steadily during the forecast window. Military and defence agencies continue to pioneer extreme environment scenarios, influencing civilian trauma curricula through technology transfer agreements. Medical-device firms leverage simulation labs for surgeon credentialing and product testing, an under-penetrated niche with high willingness to pay. Certara’s biosimulation business already serves 2,300 pharma clients, validating cross-industry applicability.

Hospitals also use simulation metrics to support Magnet recognition and Joint Commission requirements, tying training investment to institutional reputation. Integration with electronic health record data enables teams to recreate near-miss incidents for root-cause analysis. Vendor-hosted cloud portals facilitate multi-site benchmarking, accelerating best-practice diffusion. As staff retention becomes a strategic KPI, immersive training is marketed internally as a professional-development benefit, helping HR teams attract and keep talent in competitive labour markets.

Note: Segment shares of all individual segments available upon report purchase

By Delivery Mode: Cloud Migration Reshapes Training Access

On-premise labs still account for 54.56% of spending, chosen for data sovereignty and equipment control. Cloud and remote modules, however, are rising 14.56% per year and will surpass on-premise growth beyond 2027. The medical simulation market size for cloud platforms is expanding as institutions deploy virtual desktops that host full physics engines without local GPUs. Pandemic-era pilots proved that students can achieve equivalent knowledge scores through remote VR sessions, opening permanent budget lines for hybrid delivery. Provider partnerships, such as the GigXR-CAE alliance, overlay AI voice agents onto manikin sessions, synchronising physical and virtual learners in real time.

Carbon-neutral lab concepts resonate with sustainability commitments and help institutions meet scope-2 emission targets. Bandwidth optimisation remains a constraint in rural regions; vendors tackle this with edge-rendering nodes that cache scenarios locally. Security features including zero-trust architectures and encrypted learner databases are fast becoming tender prerequisites. Clients now seek platforms that integrate device-agnostic authoring tools, ensuring content persists even as VR hardware cycles shorten to 24 months.

Geography Analysis

North America commands 41.45% of the medical simulation market in 2024. The region benefits from a deep roster of accredited centres and defence grants that underwrite AI-powered training pilots. Federal agencies itemised 120 medical AI projects as part of the 2025 Digital Health Strategy, ensuring sustained investment. Yet rising capital costs and cybersecurity spending dilute operating margins for hospital buyers. Canada’s training sector is realigning after CAE divested its healthcare unit, signalling further consolidation[1]CAE Inc., “Divestiture of Healthcare Business,” cae.com.

Asia-Pacific is the fastest-growing region at 14.78% CAGR, supported by modernising hospitals and expanding medical-school enrolments. McKinsey forecasts a USD 225 billion medtech market by 2030 despite recent venture-funding contractions[2]BioWorld, “Asia-Pacific Medtech Funding Trends,” bioworld.com. Multinational suppliers partner with local distributors to navigate fragmented import regulations. Colleges in China and India adopt low-footprint VR kits to offset budget constraints, boosting remote training adoption. Preferential procurement rules favour vendors that localise manufacturing or open regional tech-support centres.

Europe maintains consistent expansion anchored in environmental regulations that push toward energy-efficient simulation labs. The region’s Horizon funding streams back research into carbon-neutral training infrastructures. Hospitals weigh cloud migration against General Data Protection Regulation compliance and often adopt hybrid topologies. Middle East and Africa markets benefit from sovereign-wealth investment in flagship medical cities but face uneven internet infrastructure that limits high-fidelity cloud streaming. South America develops capabilities through university partnerships that import curriculum content and share language-localised assessment tools.

Competitive Landscape

The medical simulation market is moderately fragmented, yet recent deals indicate rising consolidation. Madison Industries’ USD 229 million purchase of CAE Healthcare in 2024 removed a top brand from the independent pool and could trigger copy-cat acquisitions among mid-tier vendors[3]CAE Inc., “Sale of Healthcare Segment to Madison Industries,” cae.com. Hardware incumbents defend share through ecosystem strategies that couple proprietary manikins with closed-loop analytics. Software-only entrants disrupt on price and release cadence, adding AI scoring and natural-language debriefing to differentiate.

Technology priorities centre on haptics, cloud orchestration and predictive analytics. Partnerships such as GigXR with CAE bundle head-mounted AR visuals onto physical task trainers, offering multimodal experiences that raise customer switching costs. NVIDIA’s alliance with GE HealthCare extends simulation into diagnostic-device design, signalling adjacency expansion[4]NVIDIA Corporation, “Isaac for Healthcare Platform Overview,” nvidia.com. Cost-effective portable units target emerging markets where capital budgets remain tight, creating a two-tier competitive arena split between premium ecosystems and value platforms.

Regulatory accreditation acts as both barrier and moat. Vendors that attain INACSL or SSH endorsements leverage those seals to win institutional tenders. Artificial-intelligence transparency becomes a selling point as explainable-AI modules ease faculty concerns about black-box scoring. Price competition intensifies in software licences, prompting suppliers to bundle content libraries and learner-management dashboards at marginal cost. Over the forecast window, strategic themes will revolve around full-stack offerings, region-specific manufacturing footprints and data-security certifications.

Global Medical Simulation Industry Leaders

-

3D Systems Inc.

-

CAE Inc.

-

Gaumard Scientific Company Inc.

-

Laerdal Medical

-

Kyoto Kagaku Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: NVIDIA and GE HealthCare announced a collaboration to develop autonomous imaging systems using the NVIDIA Isaac for Healthcare simulation platform.

- March 2025: The US Department of Defense finalised the MHS Digital Health Strategy, cataloguing 120 AI use cases across military medicine.

- February 2024: CAE Inc. agreed to sell its Healthcare business to Madison Industries for CAD 311 million (USD 229 million).

- January 2024: GigXR and CAE Healthcare formed a strategic alliance to integrate physical, digital and immersive simulation using generative AI.

Global Medical Simulation Market Report Scope

As per the scope of the report, medical simulation is the modern-day methodology for training healthcare professionals through advanced educational technology. Medical simulation is experiential learning that every healthcare professional may need, but cannot be consistently engaged in during real-life patient care. The Medical Simulation Market is segmented by Products and Services (Products, Services and Software), Technology (High-fidelity Simulators, Medium-fidelity Simulators, and Low-fidelity Simulators), End User (Academic and Research Institutes, and Hospitals), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| By Products & Services | Products | Interventional/Surgical Simulators | Laparoscopic |

| Robotic & Endoscopic | |||

| Orthopaedic | |||

| Patient Simulators | |||

| Task Trainers | |||

| Other Products | |||

| Services & Software | Web-based Simulation | ||

| Simulation Software Licences | |||

| Training & Consulting Services | |||

| By Fidelity | High-fidelity | ||

| Medium-fidelity | |||

| Low-fidelity | |||

| By End User | Academic & Research Institutes | ||

| Hospitals & Surgical Centres | |||

| Military & Defence Organisations | |||

| Medical-device & Pharma Companies | |||

| By Delivery Mode | On-premise Simulation Labs | ||

| Cloud-based / Remote Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

By Products & Services

| Products | Interventional/Surgical Simulators | Laparoscopic |

| Robotic & Endoscopic | ||

| Orthopaedic | ||

| Patient Simulators | ||

| Task Trainers | ||

| Other Products | ||

| Services & Software | Web-based Simulation | |

| Simulation Software Licences | ||

| Training & Consulting Services |

By Fidelity

| High-fidelity |

| Medium-fidelity |

| Low-fidelity |

By End User

| Academic & Research Institutes |

| Hospitals & Surgical Centres |

| Military & Defence Organisations |

| Medical-device & Pharma Companies |

By Delivery Mode

| On-premise Simulation Labs |

| Cloud-based / Remote Platforms |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the medical simulation market?

The market is valued at USD 2.62 billion in 2025 and is projected to reach USD 5.07 billion by 2030.

How fast is the medical simulation market expected to grow?

It is forecast to expand at a 14.09% compound annual growth rate from 2025 to 2030.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing geography, advancing at a 14.78% CAGR thanks to hospital expansion and government support for medical-education capacity.

What segment leads by product type?

Hardware products hold the largest 2024 revenue share, but Services & Software are seeing the quickest growth at a 14.71% CAGR.

Why are cloud-based simulation platforms gaining traction?

Institutions favor cloud delivery for remote access, scalability and lower upfront capital needs, even as they balance data-privacy and cybersecurity requirements.

What is driving hospital adoption of simulation?

Patient-safety mandates, continuous professional development needs and the shift toward minimally invasive and robotic procedures are pushing hospitals to invest rapidly in simulation training tools.

Page last updated on: July 2, 2025