Market Overview

| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

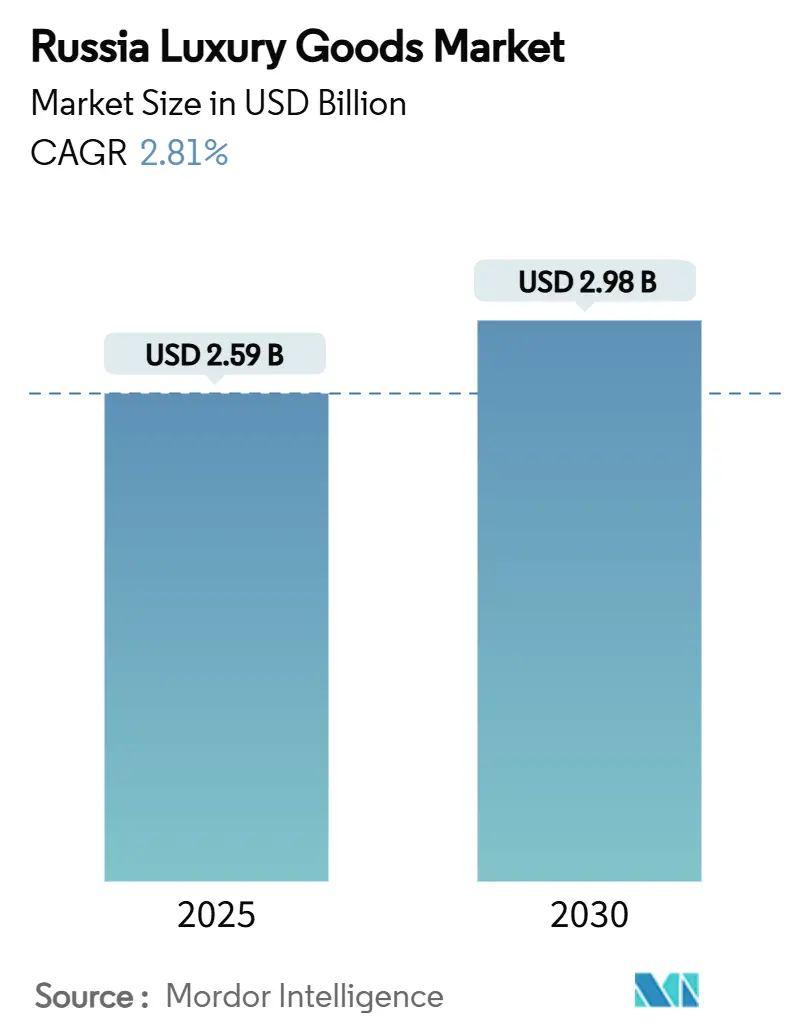

| Market Size (2025) | USD 2.59 Billion |

| Market Size (2030) | USD 2.98 Billion |

| Growth Rate (2025 - 2030) | 2.81% CAGR |

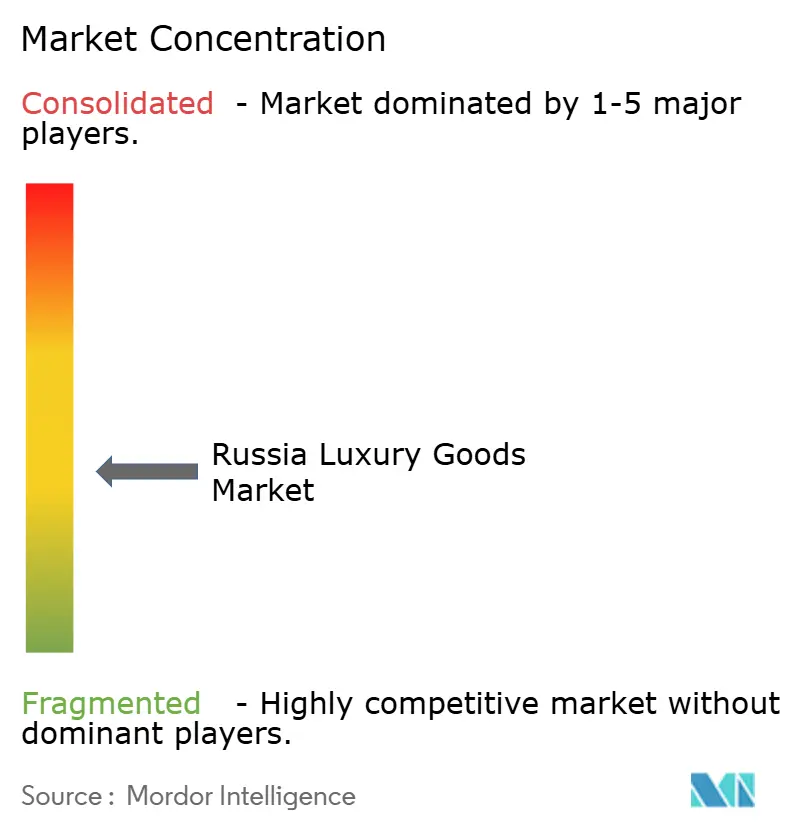

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Russia Luxury Goods Market Analysis by Mordor Intelligence

The Russian luxury goods market is valued at USD 2.59 billion in 2025 and is projected to reach USD 2.98 billion by 2030, advancing at a 2.81% CAGR. The modest yet positive trajectory demonstrates how affluent Russians continue to allocate discretionary income to premium products even as sanctions, inflation, and shifting brand footprints redefine supply routes. Parallel import channels, personal shopping services, and cross-border purchases keep high-demand items flowing despite the official suspension of many Western labels. Domestic retailers and Asian brands are capitalizing on this gap, re-stocking popular lines and introducing collections designed for local tastes, while Moscow and St Petersburg boutiques still offer the theatrical in-store experiences that many luxury buyers prefer. Social media is amplifying brand storytelling, influencing younger segments, and helping limited runs sell out quickly. Finally, expanded e-commerce logistics are bringing curated selections to regional cities, gradually broadening the geographic footprint of the Russian luxury goods market.

Key Report Takeaways

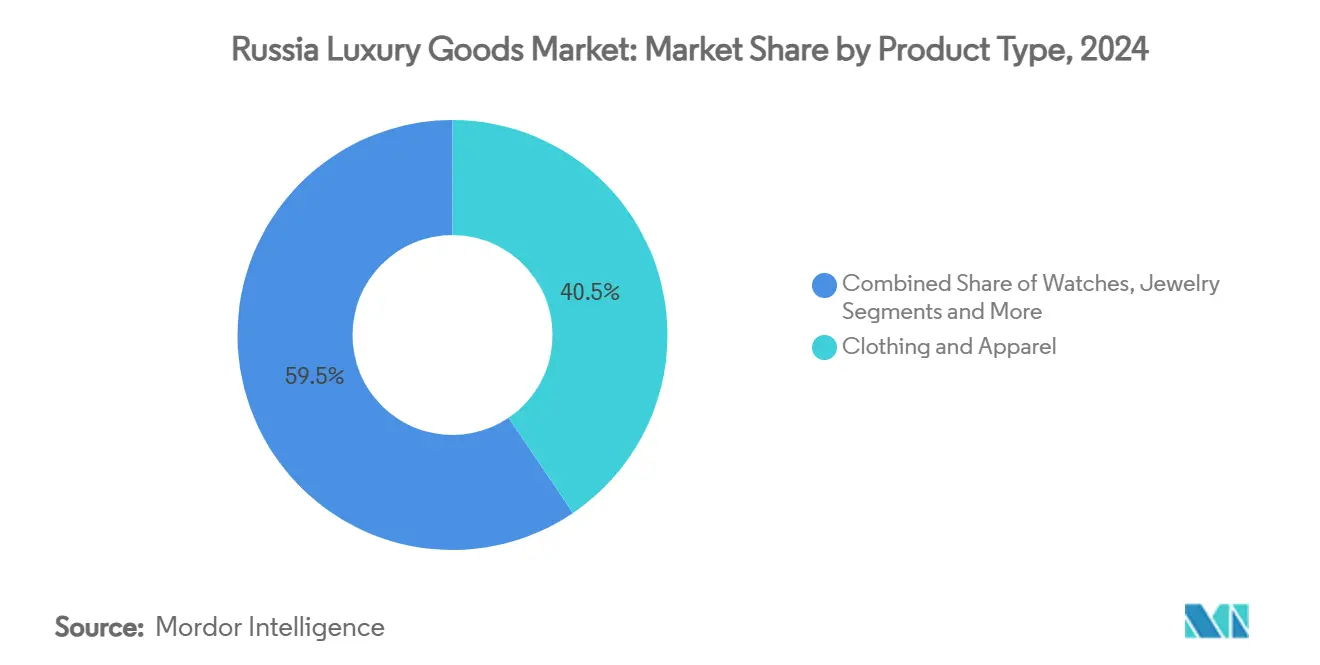

By product type, clothing and apparel led with 40.52% of the Russia luxury goods market share in 2024, whereas watches are forecast to grow the fastest at a 3.27% CAGR through 2030.

By end user, women accounted for 54.04% of purchases in 2024, while men’s buying is set to accelerate at 3.75% CAGR to 2030.

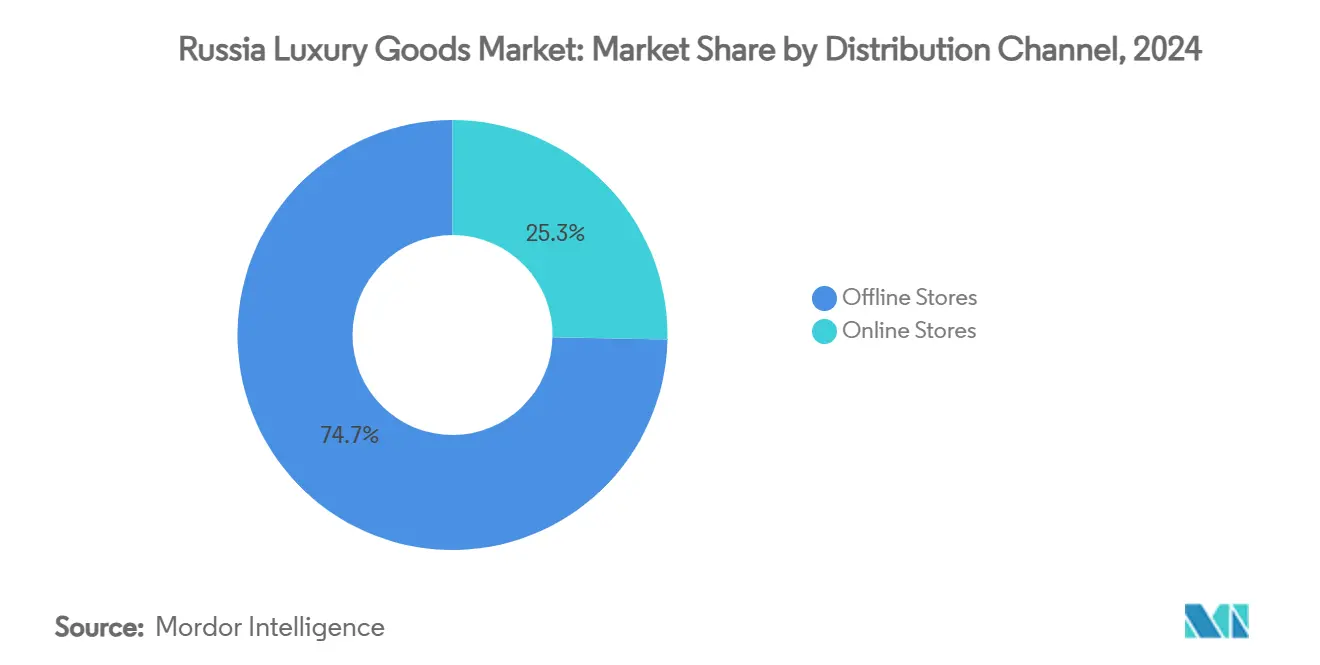

By distribution channel, offline stores retained 74.66% share of the Russia luxury goods market in 2024; online platforms hold the top growth outlook at a 3.91% CAGR.

Russia Luxury Goods Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Shift Toward Sustainable & Eco-Certified Luxury Products | +0.4% | National, with early gains in Moscow, St. Petersburg | Medium term (2-4 years) |

| Influence of Social Media and Celebrity Endorsement | +0.6% | National, spill-over to regional cities | Short term (≤ 2 years) |

| Consumers Inclination Towards Limited Edition Products | +0.3% | Moscow, St. Petersburg core markets | Short term (≤ 2 years) |

| Product Innovation in terms of Raw Material and Design | +0.5% | National, with premium segment focus | Medium term (2-4 years) |

| Globalization of Luxury Brands | +0.2% | National, despite sanctions constraints | Long term (≥ 4 years) |

| Expansion of E-Commerce Platforms | +0.7% | National, with rural penetration gains | Medium term (2-4 years) |

Source: Mordor Intelligence

Consumer Shift Toward Sustainable and Eco-Certified Luxury Products

In Russia, younger luxury consumers are placing a premium on sustainability credentials, often viewing eco-certification as a badge of honor. This marks a significant generational shift, with millennials and Gen Z who wield increasing purchasing power in the luxury market demanding transparency in sourcing and production. These demographics are not only concerned with the environmental impact but also associate sustainable practices with social responsibility and ethical consumption, further elevating the importance of eco-friendly initiatives. The trend has gained momentum, especially after the exit of international luxury brands, paving the way for domestic and Asian alternatives that champion sustainable practices. These alternatives are leveraging this opportunity by integrating eco-conscious strategies into their branding, product development, and marketing efforts, aligning with the values of this younger, environmentally aware consumer base.

Influence of Social Media and Celebrity Endorsement

In Russia, social media platforms now serve as the main avenue for discovering luxury goods. Domestic influencers and celebrities have stepped in to replace international brand ambassadors. This shift has opened fresh avenues for brand awareness and purchase consideration, especially among younger consumers who turn to digital channels for luxury insights. According to Levadu, 89% of respondents under 24 years of age visit social networks daily or almost daily [1]Source: Levadu, "Audience of Internet users, social networks, instant messengers and VPN services", www.levada.ru, underscoring the critical role of social media in shaping the preferences and purchasing decisions of this demographic. Younger audiences, who are highly active on these platforms, are more likely to engage with localized content that resonates with their cultural and social context. The trend has gained momentum with the emergence of Russian-language luxury content creators, who highlight both international and local luxury products. These creators not only showcase products but also build authentic connections with their audience by tailoring content to reflect local tastes and preferences. This dynamic has made social media an indispensable tool for luxury brands aiming to capture the attention of Russia's younger, digitally savvy consumers.

Consumers Inclination Towards Limited Edition Products

Russian consumers are increasingly favoring limited edition and exclusive luxury items, signaling a significant shift in their purchasing behavior. This trend underscores a psychological reaction to the dwindling availability of goods, with exclusivity now more than ever symbolizing social status and access to rare products. Limited edition releases are now viewed as highly coveted, often fetching premium prices due to their scarcity. Collaborations with Russian artists or cultural institutions amplify the allure of these products, sparking heightened consumer interest and driving demand. This trend isn't confined to traditional luxury items; it also permeates everyday luxury goods. According to Rossat, real disposable incomes of Russians increased by 8.5% in 2024 [2]Source: Rosstat, "Mishustin reported an 8.5% increase in real incomes of Russians in 2024", www.rbc.ru, significantly influencing purchasing decisions. In response, Russian luxury retailers are crafting exclusive collections and rolling out limited-time offerings, aligning with consumers' quest for uniqueness. Such strategies not only cater to the rising demand for distinctive items but also bolster retailers' market positions, resonating with consumers' aspirations for exclusivity.

Product Innovation in terms of Raw Material and Design

Brands are accelerating innovation in luxury product development to stand out in a highly competitive market. Russian luxury consumers actively seek products that integrate advanced materials, cutting-edge technological features, and designs that align with both global luxury standards and local cultural preferences. This demand is particularly strong in the watches and jewelry segments, where consumers highly value technical innovation and exceptional craftsmanship. The exit of some international brands has opened opportunities for creating luxury products that merge traditional craftsmanship with modern materials and contemporary design sensibilities. Domestic luxury brands are heavily investing in R and D to compete directly with international alternatives. They are focusing on developing unique materials and design elements that cater to Russian consumers' dual appreciation for innovation and cultural heritage.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Counterfeit Products | -0.8% | National, with concentration in major cities | Short term (≤ 2 years) |

| Lesser Demand from Price Sensitive Consumers | -0.6% | National, with regional variation | Medium term (2-4 years) |

| Geopolitical Tensions Affecting Supply Chain | -0.9% | National, with border region impacts | Long term (≥ 4 years) |

| Limited Market Transparency | -0.4% | National, affecting online channels | Medium term (2-4 years) |

Source: Mordor Intelligence

Availability of Counterfeit Products

Counterfeit luxury goods pose a major challenge to the growth of the Russian luxury goods market, as evidenced by the substantial volumes of counterfeit products circulating through both online and offline channels. This market restraint significantly impacts the revenue streams of legitimate luxury brands operating in Russia, eroding their brand equity and diminishing consumer trust. The proliferation of counterfeit goods is further fueled by the increasing accessibility of e-commerce platforms, which often lack stringent monitoring mechanisms, and the prevalence of unregulated offline markets. These counterfeit products not only divert consumer spending away from authentic luxury goods but also create an uneven competitive landscape, making it difficult for genuine players to maintain their market share. Moreover, the presence of counterfeit goods undermines the exclusivity and premium positioning of luxury brands, which are critical factors driving consumer demand in this market.

Geopolitical Tensions Affecting Supply Chain

Ongoing geopolitical tensions and international sanctions have fundamentally disrupted traditional luxury goods supply chains, forcing brands and retailers to develop alternative sourcing and distribution networks. The complexity of these new supply chains has increased costs and reduced reliability, impacting both product availability and pricing structures. Luxury car imports through neighboring countries like Kyrgyzstan demonstrate how sanctions have created new, more expensive distribution channels that ultimately affect consumer pricing. The Center for Strategic and International Studies notes that while Russia's economy has shown resilience, the luxury goods sector faces particular challenges due to its reliance on international supply chains and brand relationships. These disruptions have created long-term structural changes in how luxury goods reach Russian consumers, with implications for pricing, availability, and brand positioning.

Segment Analysis

By Product Type: Apparel Dominance Amid Brand Departures

Clothing and apparel commands the largest market share at 40.52% in 2024, reflecting Russian consumers' continued prioritization of fashion as a primary luxury expression despite international brand departures. The segment's resilience stems from the availability of alternative brands and the rise of domestic luxury fashion labels that have filled gaps left by departing Western brands. Watches emerge as the fastest-growing segment with a 3.27% CAGR through 2030, driven by their status as investment pieces and their relative immunity to fashion cycles. This growth reflects Russian consumers' appreciation for Swiss and German timepieces, which continue to enter the market through parallel import channels.

Footwear maintains steady demand as consumers seek premium leather goods and designer shoes, while eyewear benefits from both fashion and functional needs. The jewelry segment shows consistent performance, supported by Russia's traditional appreciation for precious metals and gemstones, particularly given the country's significant domestic production capabilities. Leather goods face challenges from reduced availability of premium European brands but benefit from increased interest in domestic alternatives. Beauty and personal care products represent the most dynamic segment, with Russian consumers increasingly interested in premium cosmetics and skincare products, supported by the growth of domestic beauty brands that have gained market share following international departures.

Note: Segment shares of all individual segments available upon report purchase

By End User: Women Lead Despite Men's Acceleration

Women account for 54.04% of luxury goods purchases in 2024, maintaining their traditional dominance in luxury consumption patterns across most product categories. This leadership reflects women's higher engagement with fashion, beauty, and lifestyle luxury products, as well as their role as primary household purchasing decision-makers for luxury items. However, men's luxury consumption is accelerating at 3.75% CAGR through 2030, representing the fastest-growing end-user segment as male consumers increasingly embrace luxury fashion, grooming, and lifestyle products.

The men's segment growth is driven by changing social attitudes toward male luxury consumption and the influence of social media in normalizing men's interest in premium fashion and grooming products. Unisex products represent a smaller but growing category, reflecting broader trends toward gender-neutral luxury offerings and shared consumption patterns among couples and families. The shift toward men's luxury consumption aligns with global trends but is particularly pronounced in Russia due to increasing disposable income among male professionals and changing cultural attitudes toward luxury consumption as a form of self-expression rather than purely status signaling.

By Distribution Channel: Offline Resilience Amid Digital Growth

In 2024, offline stores command a significant 74.66% market share, highlighting Russian consumers' strong preference for hands-on luxury experiences and the importance they place on personalized service. This preference is further reinforced by concerns over the authenticity of online luxury purchases, as well as the social and experiential aspects of luxury shopping, which remain integral to consumer behavior in Russia. Additionally, the dominance of offline channels reflects the resilience of established luxury retailers, such as Mercury Group and L'Etoile, which have continued to maintain their physical operations and cater to local demand, even as several international brands have exited the market.

Online stores are set to grow at a brisk pace of 3.91% CAGR through 2030, fueled by enhanced logistics and a broader range of luxury products on prominent Russian e-commerce sites. This surge in online luxury sales is bolstered by Russia's impressive internet penetration, which reached 92.2% in 2023, according to data from the Federal Reserve Bank St. Louis [3]Source: Federal Reserve Bank of St.Louis, "Internet users for the Russian Federation" www.fred.stlouisfed.org. The high internet penetration enables a larger consumer base to access digital platforms, making online channels a critical component of the luxury market. Digital platforms have become vital for Russians, not only in accessing international luxury brands via parallel imports but also in uncovering new domestic luxury options. These platforms are increasingly sophisticated, offering tailored customer experiences, seamless payment options, and efficient delivery services.

Geography Analysis

Russia's luxury goods market demonstrates significant regional concentration, with Moscow and St. Petersburg accounting for the majority of luxury consumption due to their higher concentration of affluent consumers and established retail infrastructure. These metropolitan areas benefit from the highest disposable incomes and the most developed luxury retail ecosystems, including flagship stores, luxury shopping centers, and premium service providers. The capital cities also serve as entry points for new luxury brands and as testing grounds for luxury market innovations.

Regional cities show growing luxury consumption as economic development spreads beyond the traditional centers, supported by the expansion of e-commerce platforms that make luxury goods more accessible to consumers outside major metropolitan areas. The growth in regional luxury consumption is facilitated by improved logistics networks and the increasing sophistication of Russian consumers' luxury preferences across different geographic markets. Cities like Novosibirsk, Yekaterinburg, and Kazan represent emerging luxury markets with growing populations of affluent consumers who seek premium products and services.

The geographic distribution of luxury consumption reflects broader economic patterns in Russia, where natural resource wealth and industrial development have created pockets of affluence across the country. However, the luxury market remains concentrated in areas with the highest economic activity and international connectivity, which provide both the consumer base and the infrastructure necessary for luxury retail operations. The development of luxury consumption in regional markets represents a significant growth opportunity, particularly as domestic luxury brands expand their geographic reach and international brands seek new distribution strategies.

Competitive Landscape

The Russian luxury goods market demonstrates moderate fragmentation. This fragmentation stems from the departure of international brands and the emergence of alternative distribution networks, creating a dynamic competitive environment. These shifts have opened up opportunities for established local retailers and new entrants capable of navigating the evolving regulatory framework and supply chain complexities. The market's structure reflects a blend of challenges and opportunities, where adaptability and strategic foresight are critical for success.

Three distinct categories of players define the competitive landscape. First, established Russian luxury retailers have shown resilience by adapting to the transformed market conditions, leveraging their local expertise and customer loyalty. Second, international brands, despite their official exit, continue to operate through parallel import networks, maintaining a presence and catering to the demand for global luxury products. Lastly, emerging domestic luxury brands are gaining traction, aiming to capture market share by offering unique, locally inspired products that resonate with Russian consumers. These players are reshaping the market dynamics, each contributing to the evolving competitive environment.

Technology adoption has emerged as a critical factor in determining competitive success. Leading players are investing heavily in e-commerce platforms, customer relationship management systems, and supply chain optimization to enhance operational efficiency and customer engagement. The market is also witnessing a shift toward greater domestic participation and alternative sourcing strategies, driven by the need to mitigate supply chain disruptions and regulatory challenges. As new players enter and existing ones refine their strategies, the competitive dynamics are expected to remain fluid, fostering innovation and further transformation in the Russia luxury goods market.

Russia Luxury Goods Industry Leaders

-

Kering SA

-

Rolex SA

-

Hermès International SCA

-

Patek Philippe SA

-

Sokolov Jewelry

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: ADAMAS, a Russian jewelry brand with over 30 years of history, has opened its flagship store in St. Petersburg on the first floor of the Nevsky Center shopping mall. The new store near the city’s main square will feature a wide range of both classic jewelry and daring new items: unique collections of rings and earrings, personalized necklaces, stylish pendants, and other jewelry made of gold and precious stones.

- November 2024: Konstantin Chaykin, an independent watchmaker from Moscow, has unveiled his latest prototype, the ThinKing. In a clever design move, the mechanisms for winding the watch and adjusting its dials are housed in a separate 5.4-millimeter-thick carrier case, optimizing space. Crafted from stainless steel and tungsten carbide, the watch boasts a lightweight yet remarkably rigid composition.

- August 2024: RS 1912 RUSSIAN GEMS has unveiled its flagship store at the "MEGA Teply Stan" shopping center in Moscow. The store features an extensive display of the brand's premier jewelry collections, offering customers a comprehensive experience of their craftsmanship and design excellence.

Russia Luxury Goods Market Report Scope

Luxury goods are products that are not essential but are highly desired and associated with wealthy or affluent people. The Russian luxury goods market is segmented by product type and distribution channel. By product type, the market is segmented into clothing & apparel, footwear, jewelry, watches, bags, and other types. By distribution channel, the market is segmented into single-brand stores, multi-brand stores, online stores & other distribution channels. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| By Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Leather Goods | |

| Jewelry | |

| Watches | |

| Beauty and Personal Care | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Offline Stores |

| Online Stores |

By Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Leather Goods |

| Jewelry |

| Watches |

| Beauty and Personal Care |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Offline Stores |

| Online Stores |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Russia luxury goods market?

The market stands at USD 2.59 billion in 2025 and is projected to grow to USD 2.98 billion by 2030.

Which product segment leads the Russia luxury goods market?

Clothing and apparel dominate with 40.52% share in 2024.

How fast is online luxury retail growing in Russia?

Online channels are forecast to expand at a 3.91% CAGR through 2030, the highest among distribution formats.

Why are parallel imports important for luxury supply in Russia?

They bypass official brand suspensions, channeling watches, leather goods, and apparel through third-country routes to satisfy ongoing domestic demand.

Page last updated on: July 5, 2025