Europe Metal Fabrication Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

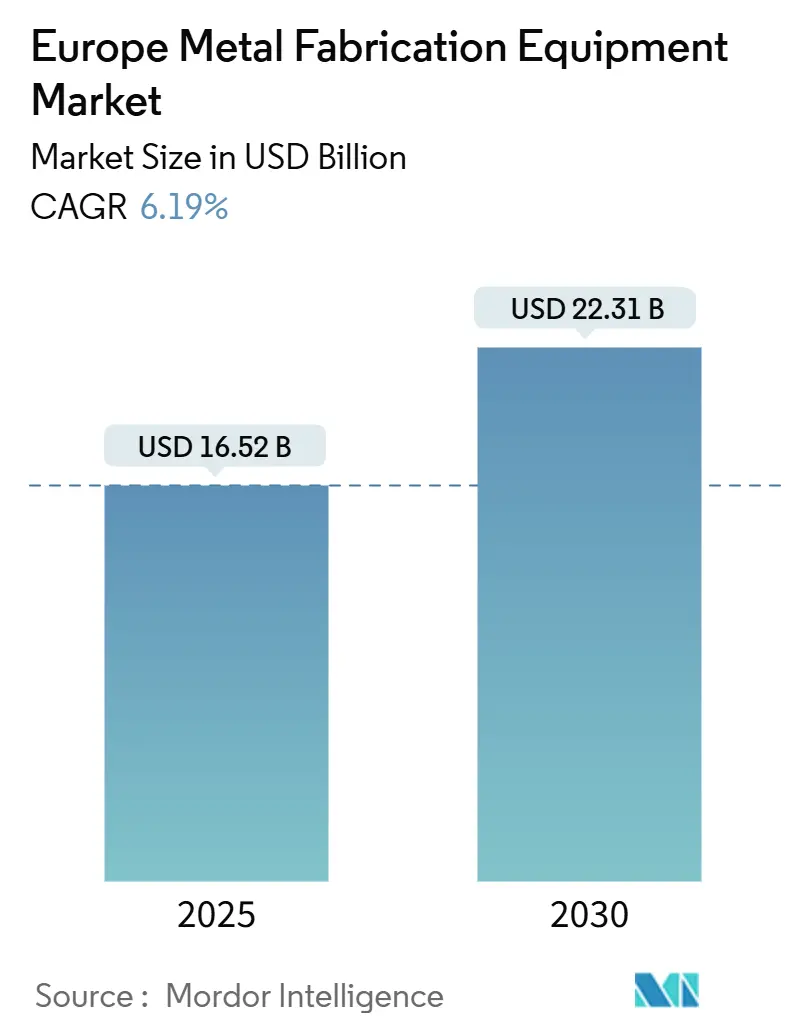

| Market Size (2025) | USD 16.52 Billion |

| Market Size (2030) | USD 22.31 Billion |

| Growth Rate (2025 - 2030) | 6.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Metal Fabrication Equipment Market Analysis by Mordor Intelligence

The Europe Metal Fabrication Equipment Market size is estimated at USD 16.52 billion in 2025, and is expected to reach USD 22.31 billion by 2030, at a CAGR of 6.19% during the forecast period (2025-2030). The upward trajectory is powered by nearshoring policies, decarbonization rules, and the migration toward automated, data-rich production lines in automotive, aerospace, and renewable-energy supply chains. Intensifying local-content targets embedded in the EU’s Net-Zero Industry Act are steering capital toward Central European corridors, while rising energy prices are accelerating the replacement of legacy CO₂ lasers with energy-efficient fiber-laser systems. OEMs are embedding IoT modules and digital twins in new equipment to unlock predictive maintenance and serialized traceability advantages, a capability that now influences bid-qualification in automotive and medical-device contracts. Competition is sharpening as robotics integrators bundle turnkey automation cells that bypass traditional machine-tool distributors, forcing incumbents to pivot toward software-as-a-service revenue streams. Mid-tier fabricators in Eastern Europe and Iberia present white-space opportunities, yet skilled-labor shortages and carbon-compliance expenses temper conversion rates, creating a nuanced risk-reward landscape.

Key Report Takeaways

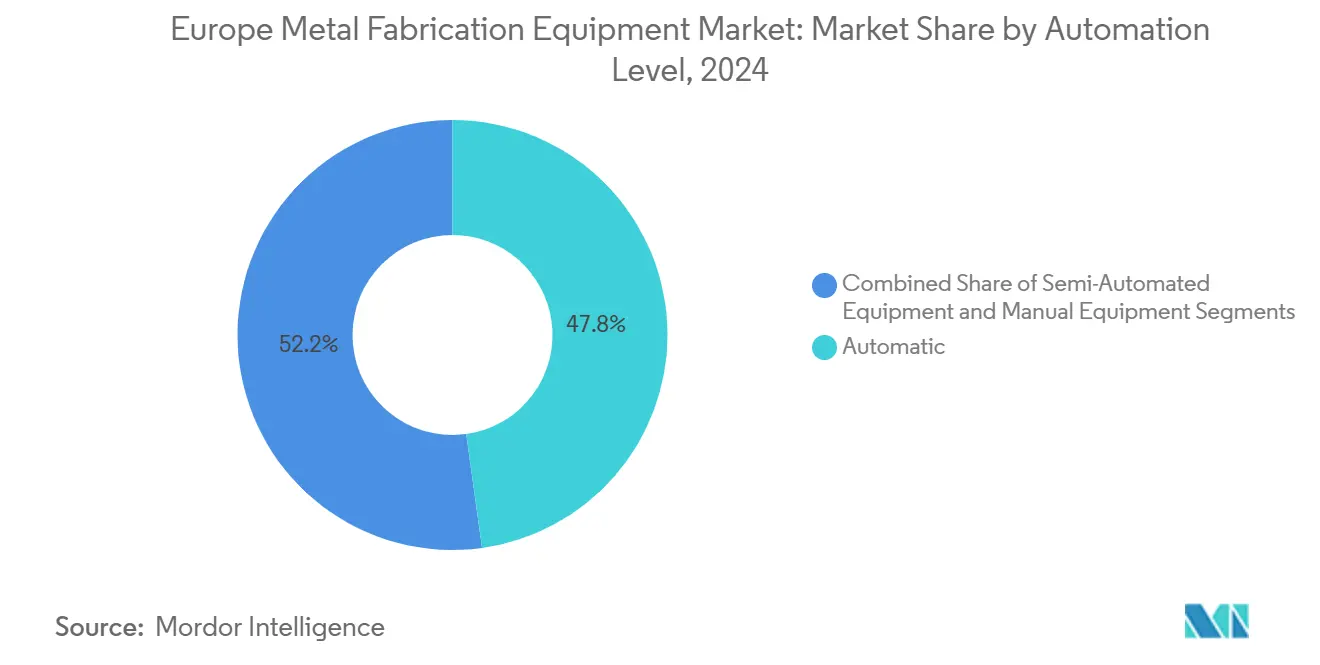

- By automation level, automatic equipment led with 47.8% of Europe metal fabrication equipment market share in 2024, while the automatic category is also the fastest-growing at a 6.91% CAGR through 2030.

- By equipment type, cutting systems accounted for 45.9% of the Europe metal fabrication equipment market size in 2024, whereas welding equipment records the highest 7.09% CAGR to 2030.

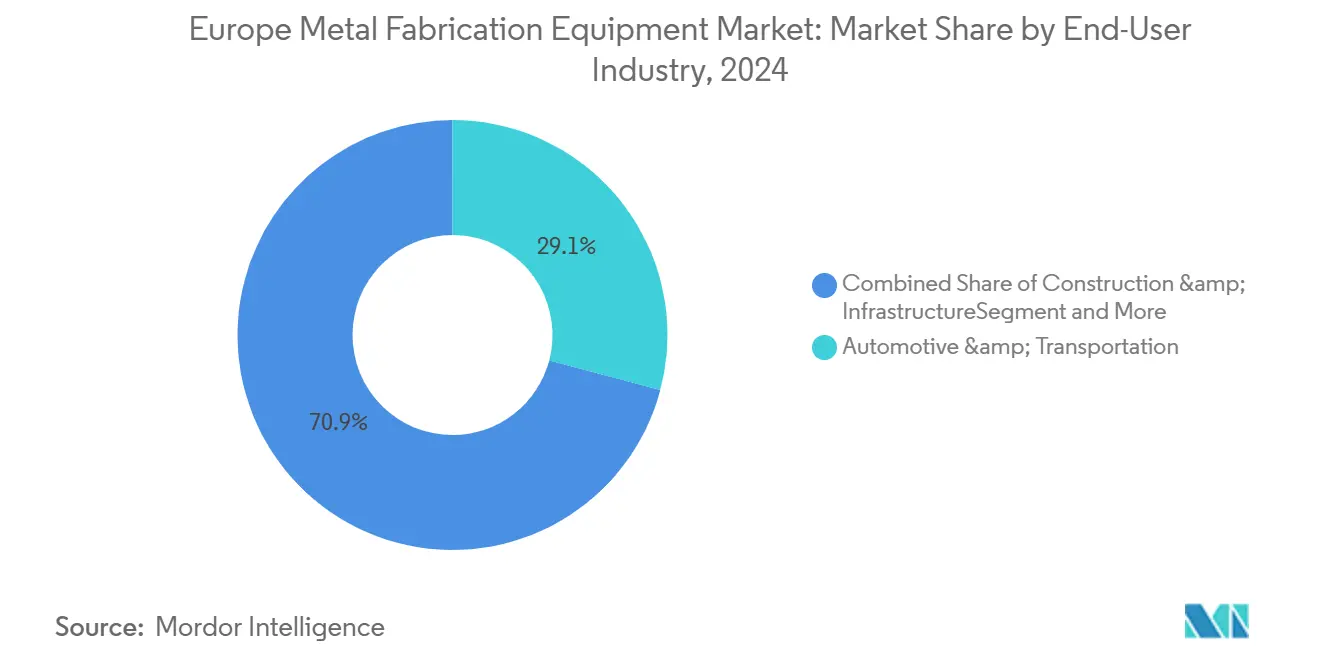

- By end-user, automotive and transportation held 29.1% revenue share in 2024; aerospace and defense are set to expand at a 7.31% CAGR to 2030.

- By geography, Germany captured 28.6% of 2024 revenue; Spain posts the quickest 7.55% CAGR through 2030.

Europe Metal Fabrication Equipment Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring and EU industrial policy spurring capex in cutting, forming, and welding lines | +1.4% | Germany, France, Spain, Poland, Czech Republic | Medium term (2-4 years) |

| EV, battery, and renewables build-out boosting demand for precision sheet/plate fabrication | +1.6% | Germany, Spain, France, Sweden, Hungary | Medium term (2-4 years) |

| Aerospace & defense backlog recovery driving high-spec machining and automated welding | +1.2% | France, UK, Germany, Italy, Spain | Long term (≥ 4 years) |

| Industry 4.0 upgrades—robotics, CNC, and IoT—raising throughput and quality traceability | +1.3% | Germany, Italy, France, Netherlands, Austria | Short term (≤ 2 years) |

| Shift to high-strength/lightweight materials requiring advanced laser, bending, and joining tech | +1.0% | Germany, UK, France, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nearshoring And EU Industrial Policy Spurring Capex In Cutting, Forming, And Welding Lines

The 2024 Net-Zero Industry Act mandates that 40% of strategic-technology demand be locally produced by 2030, unleashing USD 33 billion in new factory announcements across Central and Southern Europe[1]European Commission, “Net-Zero Industry Act Press Release,” ec.europa.eu . Tier 1 suppliers are migrating stamping and laser-cutting operations from Asia to Polish and Czech sites to secure local-content credits and compress lead times. Germany earmarked USD 1.32 billion of co-investment grants in 2024 under its “Industriestrategie 2030,” prioritizing projects that integrate digital twins and energy analytics. Consequently, large OEMs order fully automated multi-axis laser cells with inline inspection, whereas mid-tier shops prefer modular, semi-automated lines that retain flexibility. The investment wave underpins demand resilience even during macro volatility, anchoring the Europe metal fabrication equipment market across the medium term.

EV, Battery, And Renewables Build-Out Boosting Demand For Precision Sheet/Plate Fabrication

Continental battery-cell capacity is forecast to climb from roughly 150 GWh in 2024 to more than 700 GWh by 2030, with giga-plants in Germany, Hungary, and Spain driving local sourcing of precision-cut enclosures and cooling plates. Offshore wind projects across the North Sea and Baltic Sea further amplify the need for plasma-cut and submerged-arc-welded monopile sections. Fabricators targeting these segments now invest in ≥10 kW fiber-laser cutters and robotic welding cells with adaptive seam tracking, technologies formerly reserved for aerospace applications. Cross-sector adoption is compressing the capability gap between mid-tier and top-tier shops, heightening price competition. As renewables scale quickly, this driver exerts the single-largest positive bump on future equipment demand.

Aerospace & Defense Backlog Recovery Driving High-Spec Machining And Automated Welding

Airbus and Boeing ended 2024 with a combined 14,000-aircraft backlog—about 10 years of production at current rates—while European defense ministries allocated an extra USD 13.2 billion for fighter-jet upgrades and armored-vehicle programs. Tier 1 suppliers respond by ordering 5-axis CNC centers and laser-welding systems compliant with EN 9100 quality standards. The UK’s Advanced Manufacturing Research Centre notes 18- to 24-month lead times for precision-machined aerospace parts, prompting dual-sourcing in Portugal and Romania. Spillover emerges as friction-stir welding gains traction in rail and heavy machinery, widening technology transfer. The robust aerospace recovery reinforces long-cycle demand for high-specification equipment within the Europe metal fabrication equipment market.

Industry 4.0 Upgrades—Robotics, CNC, And IoT—Raising Throughput And Quality Traceability

Digital-twin adoption reached 22% of European shops in 2024, up from 12% two years earlier, as customers insist on real-time production data and predictive-maintenance insight. Equipment OEMs embed IoT sensors directly in CNC controllers, enabling every cut and weld to be logged against downstream quality escapes. Platform Industrie 4.0 released common interoperability standards in 2024 that slash integration costs. Shops achieving full traceability command 8–12% price premiums when bidding for automotive and medical contracts, offsetting capital burden. For lagging midsize fabricators, turnkey Industry 4.0 retrofits can top USD 550,000; supplier-backed leasing and EU Innovation-Fund grants therefore remain critical enablers of market uptake.

Restraints Impact Analysis

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated energy costs and carbon compliance increasing operating expenses for shops | –0.9% | Germany, Italy, Belgium, Netherlands, France | Short term (≤ 2 years) |

| Skilled-labor shortages and training gaps limiting adoption of advanced equipment | –0.7% | Germany, France, UK, Italy, Spain | Medium term (2-4 years) |

| Capex caution amid rate/price volatility and uneven construction/manufacturing demand | –0.6% | UK, France, Italy, Spain, Poland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Energy Costs And Carbon Compliance Increasing Operating Expenses For Shops

German industrial electricity averaged USD 0.22 per kWh in early 2024, more than twice pre-2022 levels, while the EU Emissions Trading System now adds USD 88–110 per ton of CO₂ for metal-working facilities[2]Reuters, “European Industrial Power Prices 2024,” reuters.com . Energy-intensive plasma and oxy-fuel cutting consume up to five times the electricity of fiber lasers, putting immediate margin pressure on legacy fleets. Operators in Belgium and the Netherlands face limited access to low-cost renewables, triggering capacity rationalization or relocation toward Spain and Portugal, where solar PPAs dip below USD 0.09 per kWh. Consequently, procurement increasingly favors fiber-laser cutting, servo-electric press brakes, and high-frequency inverter welding, all reducing per-part energy load by up to 50%. Although efficiency upgrades moderate the pain, elevated input costs remain a near-term drag on the Europe metal fabrication equipment market.

Skilled-Labor Shortages And Training Gaps Limiting Adoption Of Advanced Equipment

Vacancy rates for CNC machinists, robotic programmers, and welding technicians surpassed 8% in Germany, France, and the UK during 2024, with median hiring cycles exceeding 120 days. Without qualified staff, fabricators cannot exploit the full throughput or quality potential of automated cells, stalling return-on-investment calculations. Germany’s USD 220 million apprenticeship program, launched in 2024, will take until 2027 to graduate a meaningful cohort, leaving skills pipelines tight. Larger OEMs insulate themselves via in-house academies and VR-based simulators—KUKA introduced a virtual-reality welding tool in 2024—but midsize shops often defer equipment purchases or order downgraded semi-automated packages requiring less specialized expertise. The skills gap therefore imposes a medium-term ceiling on adoption velocity in the Europe metal fabrication equipment market.

Segment Analysis

By Automation Level: Robotics and IoT Drive Automatic Equipment Dominance

Automatic systems held a commanding 47.8% revenue share in 2024, underscoring their role as the performance benchmark across the Europe metal fabrication equipment market share. Payback periods have compressed below 24 months amid falling cobot prices and rising wages, which rose 6–8% annually in Central Europe between 2023 and 2024[3]McKinsey & Company, “Europe Advanced Manufacturing Survey 2024,” mckinsey.com . Automotive Tier 1 suppliers led uptake, embedding IoT-ready CNC and robotic modules that deliver serialized traceability for every cut, bend, and weld, a prerequisite for battery-electric vehicle contracts. ABB’s 2024 vision-guided welding cell exemplifies this shift, adjusting seam paths in real time to compensate for part variability. Small and medium shops maintain a foothold in semi-automated cells, especially for high-mix, low-volume orders requiring ≥10 changeovers per shift. Vendors now offer field-upgrade kits that add cloud connectivity to legacy punches and lasers, effectively blurring categorical lines and widening the upgrade funnel. The automatic category is forecast to rise at a 6.91% CAGR through 2030, outpacing manual and semi-automated cohorts as EU grants and vendor leasing ease capital constraints.

Semi-automated solutions cater to fabricators prioritizing flexibility over throughput. Retrofittable IoT boxes allow these lines to generate real-time dashboards, securing traceability without full robotic conversion. Manual stations have receded to niche prototype and repair jobs where automation economics remain weak. Industry consolidation looms: private-equity funds package multiple semi-automated shops into platforms that justify enterprise-wide digital-twin deployment, slashing overhead and standardizing training. As remote diagnostics and over-the-air updates proliferate, the Europe metal fabrication equipment market expects an inflection in 2027 when over half of new installations integrate predictive-maintenance modules at commissioning.

Note: Segment shares of all individual segments available upon report purchase

By Equipment Type: Cutting Leads, Welding Accelerates

Cutting technologies captured 45.9% of 2024 revenue, confirming their foundational role in fabrication process chains. Within this cohort, fiber-laser cutters continue to displace CO₂ lasers owing to threefold speed gains and 30–40% lower running costs. Plasma remains favored for heavy-plate above 40 mm, though fume-emission limits in urban zones compress its addressable market. Waterjet demand is growing among aerospace and composite shops pursuing burr-free, heat-neutral edges, with Bystronic posting 12% order growth for its ByJet line in 2024. Oxy-fuel’s relevance shrinks annually as environmental compliance tightens. The fastest growth, however, belongs to welding systems, forecast at 7.09% CAGR through 2030, reflecting aerospace backlog recovery and the shift to lightweight alloys requiring laser-beam and friction-stir techniques. Lincoln Electric’s cloud-connected power sources with real-time amperage logging help fabricators satisfy ISO 3834 data mandates and qualify for high-margin aerospace and medical bids.

Machining and forming equipment trails in absolute value yet enjoys tailwinds from high-strength materials that push tolerances below ±0.1 mm. Servo-electric press brakes deliver precision without hydraulic oil waste, aligning with ESG goals and drawing EU Innovation-Fund subsidies. Meanwhile, ancillary categories—deburring, surface finishing, autonomous material handling—gain momentum as shops chase labor substitution and cycle-time compression. By 2030, integrated work cells that chain cutting, forming, and welding modules under a single IoT umbrella are expected to represent one-third of new line installs, redefining procurement from discrete machines to connected ecosystems across the Europe metal fabrication equipment market.

By End-User Industry: Automotive Dominates, Aerospace Surges

Automotive and transportation held 29.1% of 2024 demand, mirroring the region’s retooling from internal-combustion platforms to battery-electric architectures. German automakers allocated USD 9 billion of capex in 2024 toward EV body-in-white upgrades, roughly 30% of which flowed directly into laser-cutting and robotic welding equipment. The transition to multiple low-volume battery-electric variants favors flexible automation and quick-change tooling over dedicated transfer lines. Construction-sector headwinds trimmed short-cycle orders in 2024, yet public rail electrification projects and offshore-wind foundations offer a counterweight.

Aerospace and defense spending rises fastest at a 7.31% CAGR through 2030, as Airbus targets 75 A320 builds per month, and NATO members expand procurement pipelines. This vertical demands 5-axis CNC machining centers, laser-beam welding, and friction-stir capabilities to meet stringent fatigue-life and traceability standards. Oil and gas players pivot to renewable infrastructure, notably offshore-wind monopiles that require thick-plate plasma cutting and submerged-arc welding. Heavy-machinery OEMs repatriate production for supply-chain resilience, reinforcing baseline equipment demand. Niche segments—rail, marine, and white goods—grow in line with the aggregate market, yet often trail on automation, presenting retrofit opportunities for vendors serving the Europe metal fabrication equipment market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Germany retained 28.6% of regional revenue in 2024, buoyed by its dense Mittelstand machine-tool cluster, Tier 1 automotive suppliers, and a thriving aerospace component base. The federal government co-financed USD 1.32 billion of advanced equipment under the “Industriestrategie 2030,” prioritizing digital-twin and energy-monitoring integration. High electricity prices, however, averaged USD 0.22 per kWh in early 2024, and skilled-labor vacancies exceeded 8%, prompting many fabricators to pivot toward energy-efficient fiber lasers and servo-electric brakes. Despite these hurdles, Germany remains the benchmark for Industry 4.0 implementation, with over 30% of cutting lines now connected to cloud analytics platforms.

Spain is projected to grow at a 7.55% CAGR through 2030, the swiftest in Europe's metal fabrication equipment market, underpinned by EV-battery module plants in Extremadura and Catalonia and aerospace machining clusters near Seville. The PERTE VEC program channels USD 4.73 billion into automotive modernization, roughly one-quarter tagged for fabrication and automation upgrades. Fabricators leverage lower labor costs—about 60% of German levels—and USD 0.09 per kWh solar PPAs to sharpen cost positions. Italy follows, with Emilia-Romagna and Lombardy investing in 5-axis machining centers targeting construction-equipment and agricultural-machinery OEMs. UK and France navigate post-Brexit friction and aerospace ramp-ups, respectively, while Central and Eastern European nations gain from nearshoring as suppliers establish proximity hubs to satisfy local-content mandates.

Regulatory convergence is evident. ISO 3834 documentation and CE marking under the Machinery Regulation now require real-time quality validation, elevating compliance hurdles for shops lacking IoT data capture. Germany’s Platform Industrie 4.0 interoperability standards, published in 2024, facilitate mixed-vendor communication, accelerating legacy retrofits. Consequently, the continent is bifurcating into digitally mature fabricators and laggards reliant on external systems integrators, a divide that influences supplier selection and speeds consolidation across the European metal fabrication equipment market.

Competitive Landscape

The European metal fabrication equipment market exhibits moderate concentration, with the top 10 OEMs accounting for roughly 55–60% of 2024 revenue, yet no firm exceeding a 12% individual share. Japanese and German machine-tool stalwarts such as TRUMPF, Bystronic, Amada, DMG MORI, and Mazak defend installed-base service contracts while rolling out cloud dashboards and predictive-maintenance subscriptions. Robotics specialists—KUKA, FANUC, ABB—penetrate deeper by packaging laser cutting, bending, and welding into turnkey cells that reduce commissioning risk. This encroachment forces traditional builders to offer full-stack automation or partner with integrators, shifting competitive emphasis from spindle speed to software connectivity.

Strategic moves center on capacity expansion and M&A. TRUMPF earmarked USD 165 million to boost fiber-laser output by 30% at its Ditzingen campus, betting on thick-plate demand from offshore-wind monopiles. Lincoln Electric’s 2025 acquisition of Tecnomatic deepens its European turnkey welding footprint and accelerates the roll-out of cloud-connected power sources. ABB’s OmniVance autonomous mobile robot unites material handling and welding in a single station, slashing setup time by 40% and targeting floor-space-constrained SMEs. Vendors also court mid-tier fabricators via modular IoT retrofits—LVD’s 2025 ISO 14001 certification highlights a wider pivot toward sustainability credentials in bid processes.

White-space opportunities arise among Eastern European and Iberian fabricators lacking capital for full line refreshes yet facing data-traceability mandates. Smaller OEMs such as Prima Industrie and LVD carve niche share with laser systems optimized for high-mix, small-batch runs, aligning with the fragmentation of automotive BEV variants. Software-first startups supply digital-twin and generative-design tools that reduce scrap by optimizing tool paths—capabilities progressively bundled into OEM offerings. As private-equity groups consolidate sub-scale shops into regional platforms, bargaining power tilts toward equipment vendors offering standardized training, financing, and cloud analytics, reshaping future value pools inside the European metal fabrication equipment market.

Europe Metal Fabrication Equipment Industry Leaders

TRUMPF

Bystronic

Amada

DMG MORI

Mazak

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TRUMPF announced a USD 165 million expansion of fiber-laser production in Ditzingen, Germany, targeting a 30% capacity lift by 2027 for thick-plate cutting applications in offshore wind and heavy machinery.

- February 2025: ABB Robotics launched the OmniVance autonomous mobile robot in Europe, combining material handling and robotic welding in a single turnkey cell for space-constrained SMEs.

- January 2025: Lincoln Electric acquired Italy-based Tecnomatic to broaden its turnkey-automation service network and accelerate roll-out of cloud-connected welding analytics.

Europe Metal Fabrication Equipment Market Report Scope

| Automatic |

| Semi-Automated Equipment |

| Manual Equipment |

| Cutting Equipment | Laser Cutting |

| Plasma Cutting | |

| Waterjet Cutting | |

| Oxy-fuel Cutting | |

| Machining Equipment | |

| Forming Equipment | |

| Welding Equipment | |

| Other Equipment Types |

| Automotive & Transportation |

| Construction & Infrastructure |

| Oil & Gas / Energy |

| Aerospace & Defense |

| Heavy Machinery & Industrial Equipment |

| Others |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Automation Level | Automatic | |

| Semi-Automated Equipment | ||

| Manual Equipment | ||

| By Equipment Type | Cutting Equipment | Laser Cutting |

| Plasma Cutting | ||

| Waterjet Cutting | ||

| Oxy-fuel Cutting | ||

| Machining Equipment | ||

| Forming Equipment | ||

| Welding Equipment | ||

| Other Equipment Types | ||

| By End-User Industry | Automotive & Transportation | |

| Construction & Infrastructure | ||

| Oil & Gas / Energy | ||

| Aerospace & Defense | ||

| Heavy Machinery & Industrial Equipment | ||

| Others | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe metal fabrication equipment market?

The Europe metal fabrication equipment market size is USD 16.52 billion in 2025.

What is the expected growth rate for metal fabrication equipment demand by 2030?

Revenue is projected to rise at a 6.19% CAGR, reaching USD 22.31 billion by 2030.

Which country is the largest buyer of fabrication equipment in Europe?

Germany leads with 28.6% revenue share, supported by a dense machine-tool ecosystem and strong automotive demand.

Which segment is growing fastest within the market?

Welding equipment is forecast to advance at a 7.09% CAGR thanks to aerospace and battery-pack applications.

What key factor drives investment in automatic fabrication lines?

Falling robot prices alongside stricter traceability mandates shorten payback periods, spurring adoption across European plants.

How are energy costs influencing equipment choices?

Elevated electricity prices push shops toward fiber-laser cutting and servo-electric press brakes that slash power consumption by up to 50%.