Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

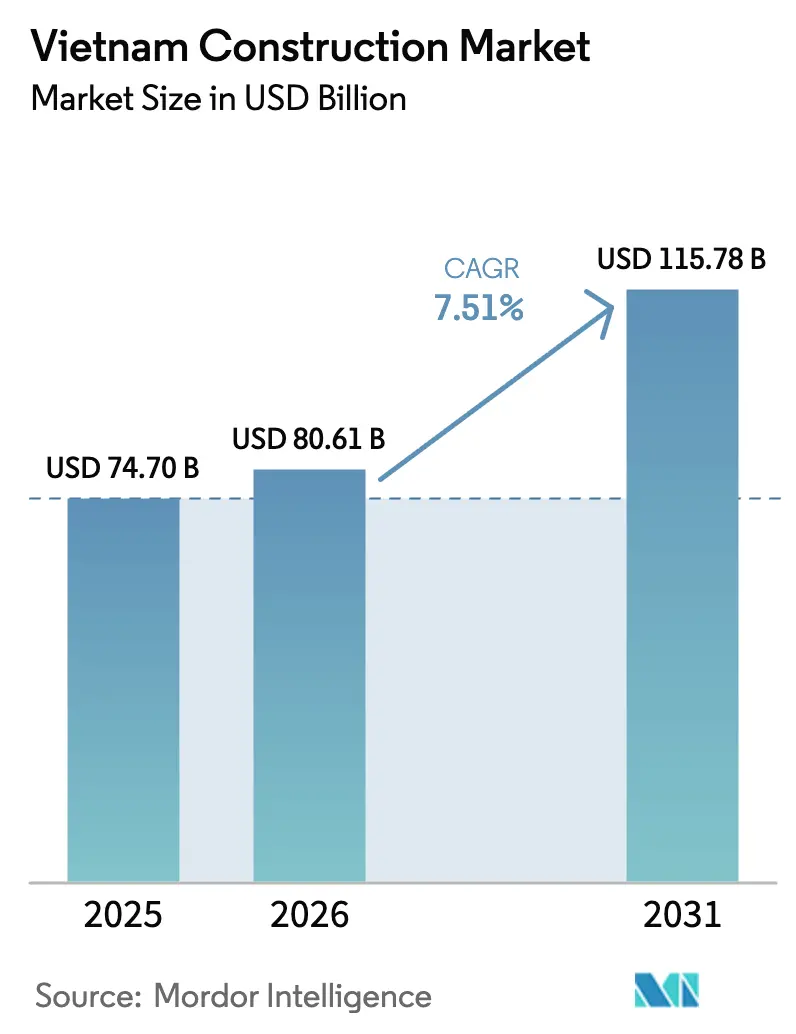

| Base Year Market Size (2025) | USD 74.70 Billion |

| Market Size (2026) | USD 80.61 Billion |

| Market Size (2031) | USD 115.78 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Construction Market Analysis by Mordor Intelligence

The Vietnam construction market size is USD 80.61 billion in 2026 and is projected to reach USD 115.78 billion by 2031 at a 7.51% CAGR. The current upcycle is anchored by a government-led infrastructure program, a rebound in foreign direct investment to a five-year high in 2025, and the implementation of new real estate laws that together improve project bankability and execution visibility. Regulatory changes that took effect in 2024 are unlocking stalled projects and enabling more predictable permitting, which supports faster private capital mobilization into transportation, energy, and urban development. Public investment commitments for 2025 are sizable relative to GDP and are being channeled into expressways, airports, and rail corridors that prioritize national connectivity. Lower mortgage rates and a large social housing mandate are stabilizing residential demand, while manufacturing-led FDI continues to pull through industrial and logistics construction.[1]https://www.mof.gov.vn/

Key Report Takeaways

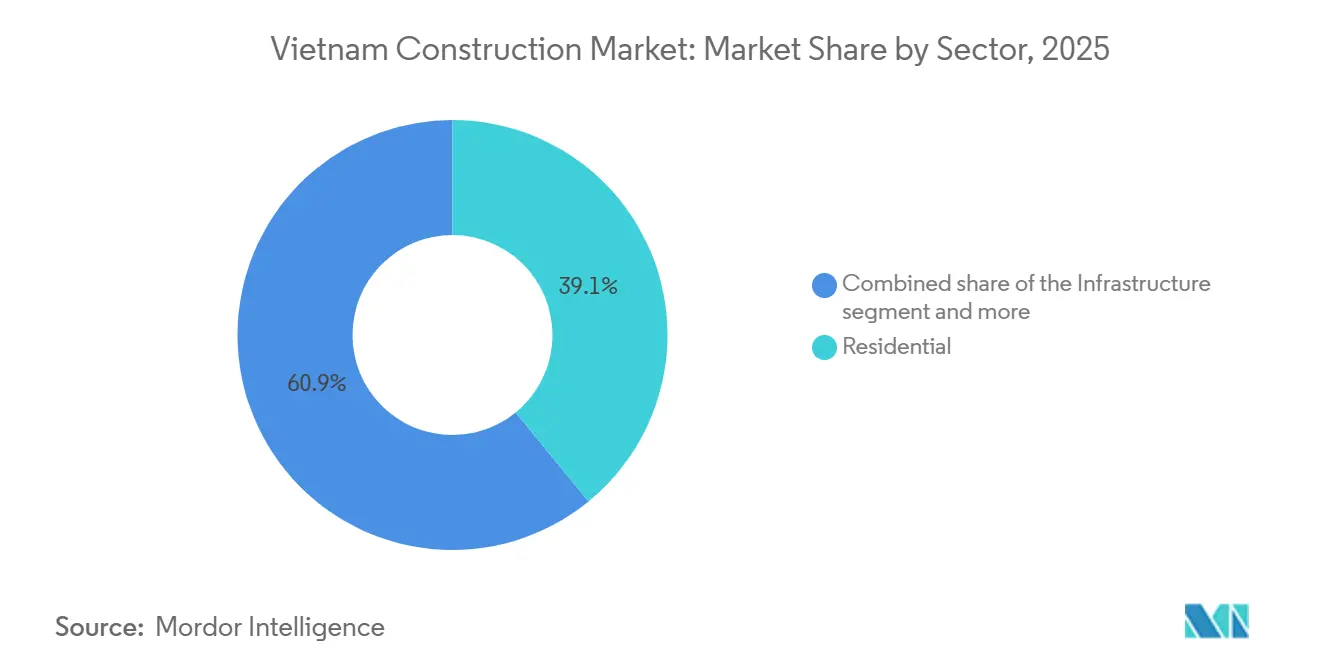

- By sector, residential captured 39.10% of the Vietnam construction market share in 2025, while infrastructure is set to expand at an 8.88% CAGR through 2031.

- By construction type, new builds accounted for 67.76% of the Vietnam construction market in 2025; renovations are advancing at a 7.70% CAGR through 2031.

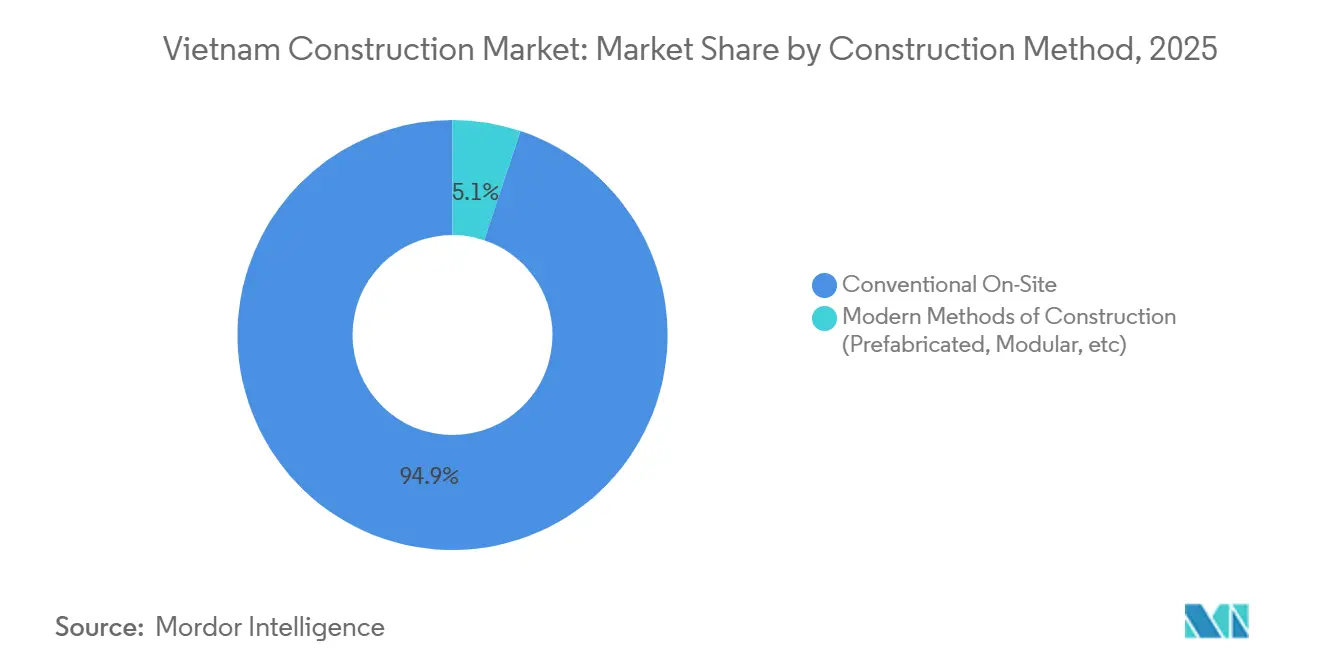

- By construction method, conventional on-site techniques held 94.55% of the revenue share in 2025, yet modern methods are projected to grow at a 9.87% CAGR through 2031.

- By investment source, public funding led with a 62.34% share in 2025, whereas private capital records the highest forecast CAGR at 8.89% to 2031.

- By geography, Ho Chi Minh City commanded 36.88% of the 2025 value; the Rest-of-Vietnam region posts the fastest 7.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Construction Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure and PPP pipeline | +2.3% | National, with early gains in northern expressways (Lao Cai-Hanoi-Hai Phong), Long Thanh Airport zone, and HCMC metro network | Long term (≥ 4 years) |

| Rapid urbanization and housing demand | +1.8% | Global, strongest in Ho Chi Minh City, Hanoi, and Da Nang urban corridors | Medium term (2-4 years) |

| Rising FDI-led industrial construction | +1.5% | APAC core (northern provinces Bac Ninh, Thai Nguyen, Hai Phong), spillover to southern industrial parks | Medium term (2-4 years) |

| Expansion of renewable-energy projects | +1.0% | Central coast (Ninh Thuan, Binh Thuan wind corridors), Mekong Delta solar/wind, national transmission grid | Long term (≥ 4 years) |

| Digital e-permitting accelerating approvals | +0.7% | National, with pilot rollout in major cities (Hanoi, HCMC, Da Nang) before nationwide expansion | Short term (≤ 2 years) |

| Modular construction uptake by local conglomerates | +0.6% | Global, concentrated in FDI industrial corridors (northern provinces) and high-rise residential (major cities) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Housing Demand

Urbanization and new real estate laws are improving supply timelines in 2026, yet affordability and location dynamics are shaping a segmented recovery. The Ministry of Construction recorded a large affordable housing gap and reported that 102,633 social housing units were completed in 2025 toward the nationwide program, while mortgage rates remained in the 5% to 6% range to support end-user demand. Major pipeline additions are concentrated in Hanoi and Ho Chi Minh City, with several large projects moving forward post-2026, while select northern provinces are drawing new residential investment linked to manufacturing corridors. Real estate FDI picked up in 2024 and included commitments from established Asian developers such as Nomura Real Estate and local partners, reinforcing long-term housing and township plans near industrial zones. A rising share of projects target green certification pathways, which can command price premiums but also require supply chain readiness for low-carbon materials in line with Vietnam’s net-zero ambitions.[2]https://www.sbv.gov.vn/vi/trang-chu

Government Infrastructure and PPP Pipeline

Vietnam has enhanced its PPP framework with higher viability gap funding and revenue-sharing provisions to improve project bankability for transport, urban, and energy assets. Implementation still hinges on demand certainty for user-pay projects, and large rail proposals require substantial state support alongside private participation to proceed at scale. The model functions as co-financing in practice, with state-owned enterprises and diversified conglomerates providing anchor sponsorship on priority corridors and airports to manage delivery risk. Transit-oriented development requirements attached to new metro sections are intended to improve asset monetization, but value realization often lags until operations stabilize, which can create timing gaps for investors. Regulatory constraints on land and security interests for foreign lenders also shape financing structures and can raise all-in costs unless mitigated through local banking partnerships. Emerging green financing standards from multilaterals are pushing projects to adopt environmental management systems and product carbon verification for eligible supply chains.[3]https://www.ifc.org/en/home

Rising FDI-led Industrial Construction

Manufacturing-led FDI realized in 2025 remained high and is shifting toward higher value production in electronics and energy components, which lifts requirements for precision facilities. Global manufacturers such as Samsung and LG continued to expand their footprints, which increases demand for cleanrooms, vibration-controlled foundations, and high-bay automated warehouses. Specialty capability building is visible through moves like Coteccons acquiring a foundation specialist and EPC firms such as LILAMA delivering complex LNG-to-power packages. The pipeline of new industrial parks approved in 2025 positions northern and north-central provinces to capture supplier ecosystems linked to electronics, semiconductors, and renewable components. Industrial park developers increasingly embed sustainability and ready-built utilities to meet tenant standards and shorten the time to production for incoming manufacturers.

Expansion of Renewable-Energy Projects

Power Development Plan VIII sets ambitious capacity targets for wind, solar, LNG-to-power, and storage by 2030, which will require large-scale construction across generation and grid systems. Transmission readiness is a binding constraint in several regions and select 500 kV nodes face load risks without accelerated upgrades in the 2026 to 2030 window. Legacy FIT and acceptance certificate issues from past waves have slowed investment decisions for new greenfield projects despite long-term demand signals. New rules enable direct power purchase for large users and allow private grid links in defined cases, which can unlock industrial offtake where public grid capacity is congested. Storage requirements for utility-scale renewables and supply concentration in battery systems call for careful procurement planning to meet performance and reliability targets. Offshore wind could draw significant capital if licensing, survey, and offtake processes shorten and if enabling grid capacity is prioritized.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortage and aging workforce | -1.2% | Global, acute in northern industrial zones (Bac Ninh, Hai Phong) and central highlands | Short term (≤ 2 years) |

| Construction-material price volatility | -0.9% | National, with spikes concentrated in post-disaster zones (Gia Lai, Quang Tri) and cement/steel-producing provinces | Short term (≤ 2 years) |

| Fragmented land-acquisition processes | -0.7% | National, with delays most severe in Dong Nai, Lam Dong, Khanh Hoa (renewable-energy corridors), and HCMC/Hanoi metro TOD zones | Medium term (2-4 years) |

| High risk-premium on long-term project finance | -0.5% | National, with elevated spreads for PPP transport projects and renewable-energy assets lacking PPA certainty | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Shortage and Aging Workforce

A limited pool of certified trades and steady outflows of workers to overseas markets are tightening labor availability for complex builds. The share of workers with formal vocational credentials remains low, which raises on-site training needs for contractors and lengthens mobilization for specialized scopes. Wage inflation for certified welders and specialized crews increased in 2025, and leading contractors reported margin pressure despite healthy order books. Youth underemployment and societal preferences for university tracks over technical pathways add friction to replenishing core trades. Policy measures to expand high-tech training incentives take effect in 2026 and are intended to accelerate skill localization for advanced projects.

Construction-Material Price Volatility

Late-2025 storm damage and input cost increases triggered sharp spikes in roof tiles and rebar, highlighting exposure for lump-sum contractors without price-adjustment clauses. Cement producers faced cost pressures from electricity and fuel, and some announced price increases in early 2025 as financial performance weakened in 2024. Electricity tariffs rose in late 2024, which disproportionately affected energy-intensive materials like cement and contributed to persistent pricing risk for infrastructure packages. Domestic steel procurement remains concentrated among a few players, and anti-dumping duties have reduced low-cost import options, adding to volatility. Contract adjustment provisions in the amended Construction Law apply from mid-2026 and are expected to clarify relief conditions for abnormal price swings. Developers with partial vertical integration into materials and aggregates report more stable unit costs through shocks compared to spot buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Accelerates as FDI and PPP Pipelines Converge

Residential construction held a 39.10% share of the Vietnam construction market in 2025, while infrastructure recorded the fastest trajectory with an 8.88% CAGR expected through 2031. The housing program for one million social units, combined with mortgage rates at 5% to 6%, stabilizes end-user activity even as affordability limits weigh on mid-tier segments in certain provinces. Large-scale infrastructure builds include the North-South high-speed railway plan, the Long Thanh International Airport program, and expressway expansion toward a 2030 target, which together lift engineering and construction workloads. The industrial and logistics subsegment is benefiting from realized manufacturing FDI in 2025, which is the main driver for new factories, ready-built facilities, and supplier parks. Developers and EPC firms that align with tenant sustainability requirements and cleanroom or high-bay specifications are capturing the higher-value scopes.

Transportation is the central node within infrastructure, as new road, rail, and airport capacity is prioritized on economic corridors that link northern and southern regions. New rail links from border provinces to seaports and wider metro plans in both Hanoi and Ho Chi Minh City are moving through phased execution as land clearance and funding packages are sequenced. Energy and utilities require capital at scale under PDP VIII, with LNG power, wind, solar, and storage needs translating into a broad EPC opportunity set. Transmission grid projects are a critical unlock for new renewable capacity, and designated 500 kV backbones remain a priority in the current plan period. Compliance with international standards for turbines, safety systems, and monitoring is increasingly a prerequisite for financing and procurement, shaping vendor selection across energy packages.

By Construction Type: Renovation Gains Momentum as Asset Owners Retrofit for Net-Zero Mandates

New construction accounted for 68.10% of the Vietnam construction market in 2025, and renovation is projected to grow at a 7.99% CAGR to 2031 as owners prioritize retrofit strategies. Public investment is supporting greenfield expressways, airports, and rail, while the manufacturing pipeline sustains new industrial builds across core regions. Renovation demand is rising with the need to upgrade state-built assets and private portfolios to meet energy performance, digital infrastructure, and compliance expectations. Housing support mechanisms for social and workers’ housing and policies to improve the quality and safety of older apartment stock are reinforcing the retrofit trend. Financial incentives that lower borrowing costs for eligible housing projects also encourage upgrades alongside new supply additions.

Within new construction, capital and order books are concentrated in projects above the USD 38 million threshold for transport and mega mixed-use, which account for a large value share despite a smaller project count. Renovation specialists with capabilities in adaptive reuse, energy-efficient MEP upgrades, and digital retrofits are securing premium pricing where they can lock in delivery certainty for operational sites. The policy push to digitize real estate transactions and assign digital IDs to properties will nudge owners to lift documentation, safety, and performance standards before listing or refinancing assets. The Vietnam construction industry is also seeing data infrastructure upgrades in offices, parks, and campuses to support connectivity and edge computing workloads. Projects that align with environmental management standards are better positioned to access international financing linked to climate objectives.

By Construction Method: Modular Systems Gain Share as Labor Costs Surge and Timelines Compress

Conventional on-site execution held 94.88% of the Vietnam construction market in 2025, while modern methods of construction are on track to grow at a 9.55% CAGR through 2031 from a low base. A large workforce and widespread adoption of cast-in-place concrete keep conventional methods dominant for heavy civil and large structural work. Modular and prefabricated solutions are gaining traction as contractors respond to tighter schedules in industrial builds and to sustainability targets that favour off-site fabrication. Technology investments by leading firms and product innovations by materials suppliers signal a shift to standardized systems where feasible. Examples include specialized scaffolding and advanced transfer slab techniques applied to high-rise projects and modular plumbing systems with recognized third-party certifications.

Barriers to adoption include upfront investment for precast plants, logistics costs for moving large components, and site constraints in urban settings that limit staging for modules. Even so, repetitive residential units, high-bay warehouses, and data center shells are well suited to modern methods that yield consistent quality and shorter cycle times. The Vietnam construction industry is seeing competitive differentiation around foundation engineering and floor flatness tolerances as semiconductor and data center projects set tighter benchmarks. Policy emphasis on high technology adoption and BIM is expected to accelerate digital workflows and factory-controlled production in the next build cycle. Developers and contractors that integrate design, manufacturing, and install teams are positioned to capture savings and reduce schedule risk for time-sensitive FDI projects.

By Investment Source: Private Capital Pivots Toward Transit-Oriented and Industrial Mixed-Use

Public investment held 63.10% of the Vietnam construction market in 2025, while private capital is projected to grow at a 9.07% CAGR through 2031 as PPP rules and credit programs improve access. Government disbursement is targeted at expressways, rail, and airports, and budget execution remains a focus as authorities work to simplify procedures and accelerate site handover. Private sponsors are increasingly active in transit-oriented mixed-use and in industrial platforms where real estate and infrastructure are developed in tandem. High-profile PPP proposals in Ho Chi Minh City and new metro phases illustrate how private partners can monetize adjacent land and services alongside core transport assets. Preferential credit windows for national key projects and strategic technology programs are designed to draw in long-term loans at lower rates in 2026.

Public funds dominate cross-border rail and national corridors where strategic goals outweigh near-term commercial returns, while private flows concentrate on recoverable cash flows linked to land value and industrial demand. Conglomerates with integrated ecosystems across housing, retail, and transport are using internal cross-subsidies to unlock complex projects and manage early-stage cash flow gaps. Foreign direct investment reached USD 27.62 billion disbursed in 2025, and manufacturing remained the leading destination, reinforcing demand for industrial and logistics assets. Compliance with ISO-based management systems and product stewardship rules, combined with green building certifications, is becoming a selection factor in both public procurement and PPPs. Sponsors that meet these criteria improve their ability to secure blended finance and development bank support for capital-intensive programs.

Geography Analysis

Ho Chi Minh City held 36.88% of the Vietnam construction market share in 2025 and continues to anchor large PPP proposals in urban rail and major bridges alongside a robust mixed-use pipeline. The city’s program includes additional metro connectivity, major ring road works, and selective large-scale sports and cultural venues that catalyze surrounding development. Despite a healthy volume of housing under construction, prime office vacancy remained elevated in 2024, pushing repositioning strategies in secondary submarkets. Execution challenges from land clearance and input price volatility persisted through late 2025, which required tighter cost management on public works and private builds. Digitization of real estate transactions and property IDs is expected to improve transparency and support better portfolio curation across the city in 2026.

Hanoi and Da Nang show distinct growth drivers that complement Ho Chi Minh City’s scale. Hanoi drew sizable foreign commitments in 2025, much of it into real estate, and is advancing an extensive metro vision supported by new interprovincial rail construction that started in December 2025. Northern satellites, including Bac Ninh and Thai Nguyen, are attracting industrial spillover and advancing major transport and airport proposals to support manufacturing clusters. Japanese developers have moved forward with new industrial parks and residential projects that emphasize sustainability features to meet tenant standards. Da Nang remains a central-coast gateway with growing energy logistics and coastal mixed-use activity that leverages its strategic location on the East-West Economic Corridor. Regional seaport and LNG projects in neighboring provinces complement Da Nang’s tourism and logistics footprint and create workstreams for specialized contractors.

The Rest of Vietnam is forecast to grow at a 7.77% CAGR through 2031, outpacing the main hubs as national expressway and coastal corridor projects improve market access for logistics and agro-industry. The Mekong Delta offers a large wind and solar opportunity set but needs coordinated transmission upgrades to integrate new capacity under PDP VIII. In the central highlands and along the central coast, tourism-oriented infrastructure and new industrial platforms are adding construction demand in second-tier provinces. Northern border provinces benefit from rail plans that link to seaports and enable a manufacturing-export corridor aligned with China-facing trade. Industrial parks in secondary provinces are positioned to capture value where labor pools are available and where green power access can be arranged for anchor tenants.

Competitive Landscape

Vietnam’s construction sector remains moderately fragmented, with a long tail of regional contractors and a top tier of diversified firms that together account for a modest share of total revenues. Strategic differentiation is visible in three areas, namely vertical integration across development and construction, technical specialization for advanced industrial and energy projects, and ecosystem orchestration that aligns design, procurement, fabrication, and O&M. Conglomerates such as Vingroup and Sun Group can back transport and complex mixed-use proposals with real estate cash flows, which support aggressive bidding on flagship PPPs. Technical leaders such as Coteccons have expanded into deep foundation specialty through acquisition, and LILAMA continues to demonstrate EPC credentials on LNG-to-power assets within Vietnam’s power roadmap. Industrial clients increasingly require ISO-based quality and environmental systems as well as LEED or EDGE pathways for facilities, raising the bar for contractor selection.

Competition intensity is bifurcated by project scale. Mega-projects above USD 38 million in transport and aviation tend to be awarded to state-owned enterprises and capitalized conglomerate consortia, while small and medium-sized works in housing, warehouses, and fit-outs remain highly contested. Margin pressure is most pronounced on lump-sum infrastructure packages during input cost swings, which has motivated selective bidding and stronger risk-sharing terms from capable primes. Digital procurement and BIM adoption are spreading through bid and delivery processes, reducing design-to-build timelines for firms that can invest in systems and training. The push for green construction methods and materials is also creating room for product innovators and for contractors who can quantify embodied carbon reductions. Ready-built industrial products with integrated utilities are gaining share among park developers targeting electronics and broader manufacturing supply chains.

Strategic moves in 2025 and 2026 reflect capability acceleration and capital access. Coteccons acquired GEO Foundations Vietnam to strengthen precision foundation engineering ahead of the 2026 to 2030 public investment cycle, and it also approved a program to expand working capital for subcontractor and supplier payments. LILAMA and partners inaugurated key milestones at the Nhon Trach 3 and 4 LNG-to-power project, which aligns with PDP VIII’s LNG capacity goal for 2030. Japanese partners advanced both industrial park and ready-built factory platforms in Thanh Hoa and Hai Phong to serve electronics and semiconductor suppliers, reinforcing a northward shift in high-spec industrial construction. Policy-linked financing channels for national key projects are widening in 2026, and sponsors that combine compliance, transparency, and delivery track records are best placed to benefit.

Vietnam Construction Industry Leaders

Coteccons Construction JSC

Hoa Binh Construction Group JSC

Central Construction JSC

Delta Construction Group

Vinaconex JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Coteccons Construction JSC officially approved the acquisition of 100% equity in GEO Foundations Vietnam Company Limited

- December 2025: The Nhon Trach 3 and 4 Gas Power Project, where LILAMA is the joint-venture EPC contractor with Samsung C&T, was inaugurated. The high-tech LNG-to-power plant synchronized Nhon Trach 3 into the national power grid in February 2025 and achieved first firing for Nhon Trach 4 in June 2025, supporting PDP VIII’s LNG capacity targets to 2030.

- May 2025: Sumitomo Corporation obtained a development permit from Thanh Hoa Province to proceed with Thang Long Industrial Park Thanh Hoa Corporation, a 100%-owned project spanning approximately 167 hectares in Phase 1, with total initial investment of 17 billion yen. Construction is scheduled to begin in fall 2025 with tenant occupancy targeted by end-2026 and an emphasis on supplying green electricity.

Vietnam Construction Market Report Scope

Construction is the installation, maintenance, and repair of buildings and other stationary structures, as well as the construction of roadways and service facilities that form fundamental components of structures and are required for their operation. Construction encompasses the processes involved in constructing buildings, infrastructure, and industrial facilities, as well as related operations, from start to finish.

The Vietnam construction market is segmented by sector (commercial construction, residential construction, industrial construction, infrastructure (transportation) construction, and energy and utilities construction).

The report offers market size and forecasts for the Vietnam construction market in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Ho Chi Minh City |

| Hanoi |

| Da Nang |

| Rest of Vietnam |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Ho Chi Minh City | |

| Hanoi | ||

| Da Nang | ||

| Rest of Vietnam | ||

Key Questions Answered in the Report

What is the Vietnam construction market size in 2026, and how fast will it grow to 2031?

The Vietnam construction market size is USD 80.61 billion in 2026 and is projected to reach USD 115.78 billion by 2031 at a 7.51% CAGR.

Which sector is growing the fastest within Vietnam’s construction space to 2031?

Infrastructure is the fastest growing sector with an 8.88% CAGR through 2031, supported by rail, expressways, and airport programs.

How is private capital participation changing in Vietnam’s construction ecosystem?

Private capital is projected to grow at a 9.07% CAGR through 2031, helped by PPP enhancements and preferential credit windows for national key projects.

Which city commands the largest share in Vietnam’s construction activity?

Ho Chi Minh City leads with 36.88% share, anchored by metro, bridge, and large mixed-use proposals aligned with the public investment cycle.

What are the main constraints Vietnam construction faces in 2026?

Skilled labor shortages and construction material price volatility are near-term restraints, with policy responses focusing on training, contract adjustments, and grid capacity for energy projects.

How are modern methods of construction evolving in Vietnam?

Modern methods of construction are expected to grow at a 9.55% CAGR from a low base as contractors invest in modular systems, BIM, and off-site fabrication to meet schedule and sustainability targets.

Page last updated on: