Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

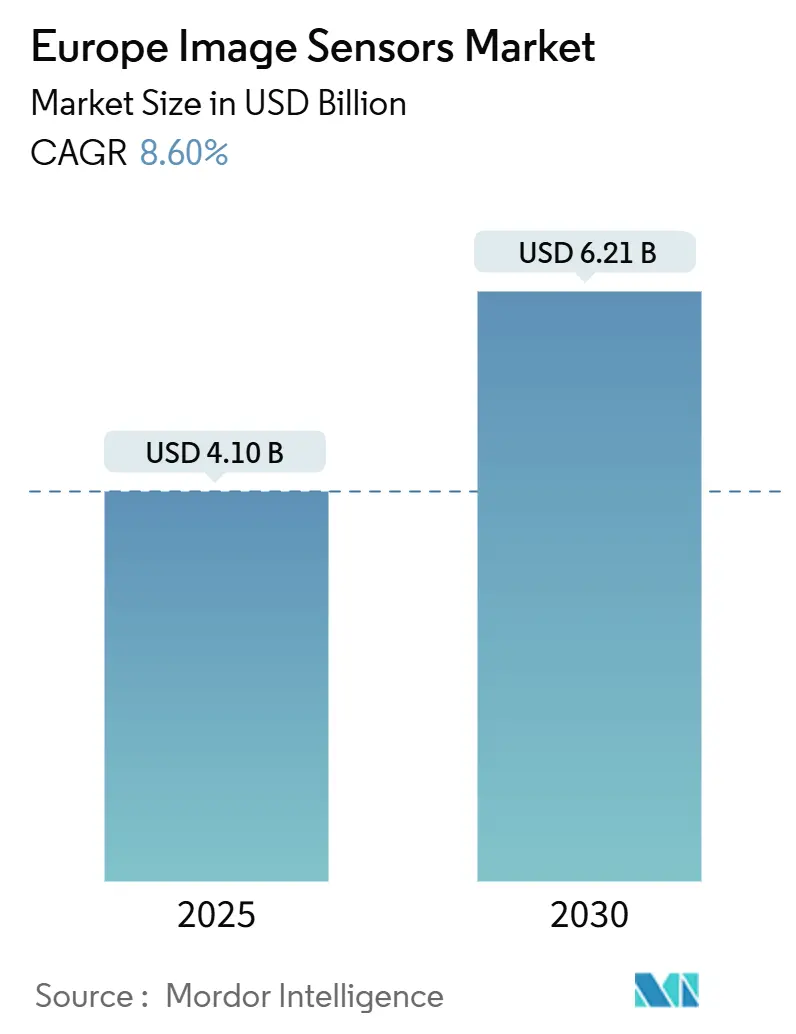

| Market Size (2025) | USD 4.10 Billion |

| Market Size (2030) | USD 6.21 Billion |

| Growth Rate (2025 - 2030) | 8.60% CAGR |

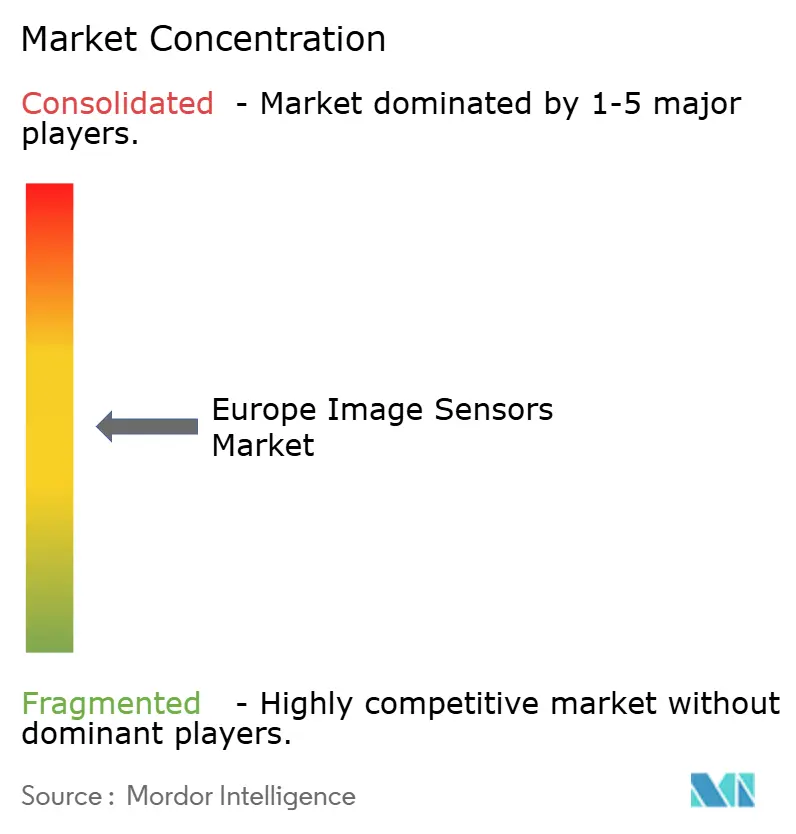

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Image Sensors Market Analysis by Mordor Intelligence

The Europe image sensors market stands at USD 4.1 billion in 2025 and is projected to reach USD 6.21 billion by 2030, reflecting an 8.66% CAGR. Pent-up automotive safety demand, smart-phone camera innovation and EU semiconductor re-shoring policies combine to move value creation from consumer electronics toward high-reliability automotive and industrial niches. Wafer-level optics stacked CMOS imaging sensor (CIS) architectures and quantum-dot materials increase performance ceilings while keeping form factors slim. Regional players leverage proximity to automakers and industrial OEMs to validate functional-safety requirements faster than distant suppliers can. At the same time, export-control uncertainty around lithography tools and high European energy prices temper near-term capacity expansion, pushing firms to prioritize premium segments where technical leadership outweighs cost.

Key Report Takeaways

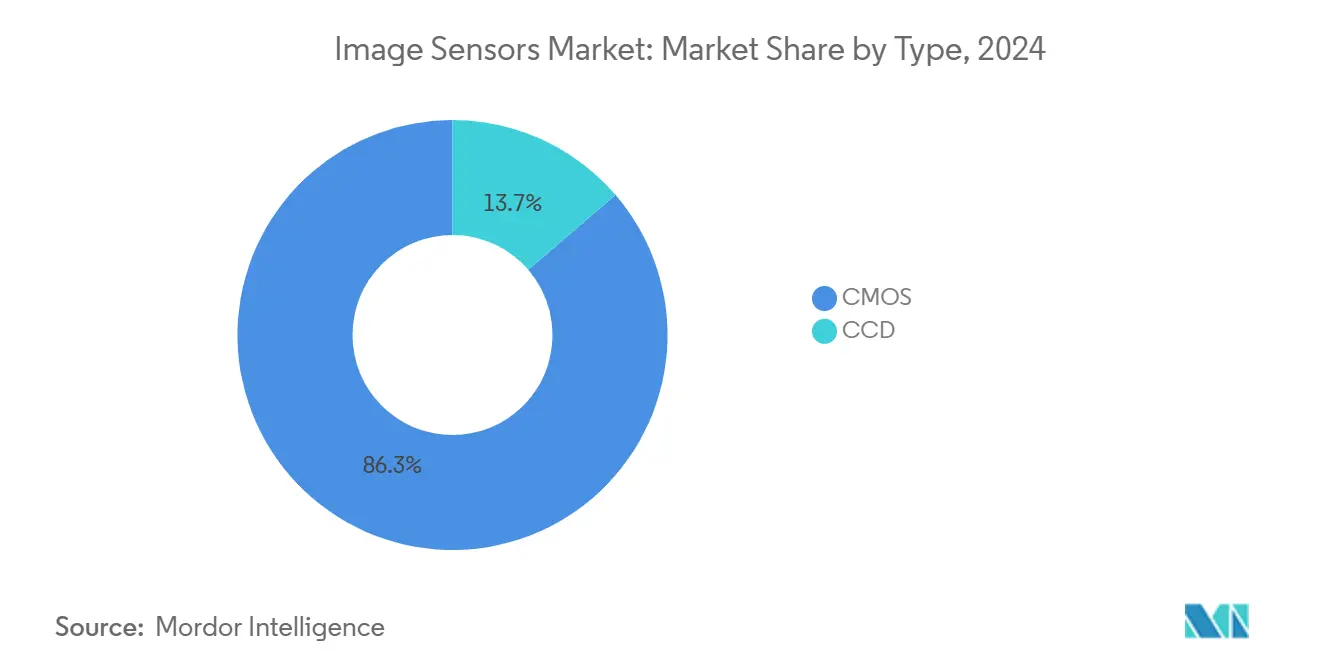

- By type, CMOS commanded 86.30% of Europe image sensors market share in 2024, while global-shutter CMOS is forecast to grow at 9.30% CAGR through 2030.

- By resolution, the 25-64 MP segment led with 28.44% revenue share in 2024; sensors above 200 MP are set to expand at 12.33% CAGR to 2030.

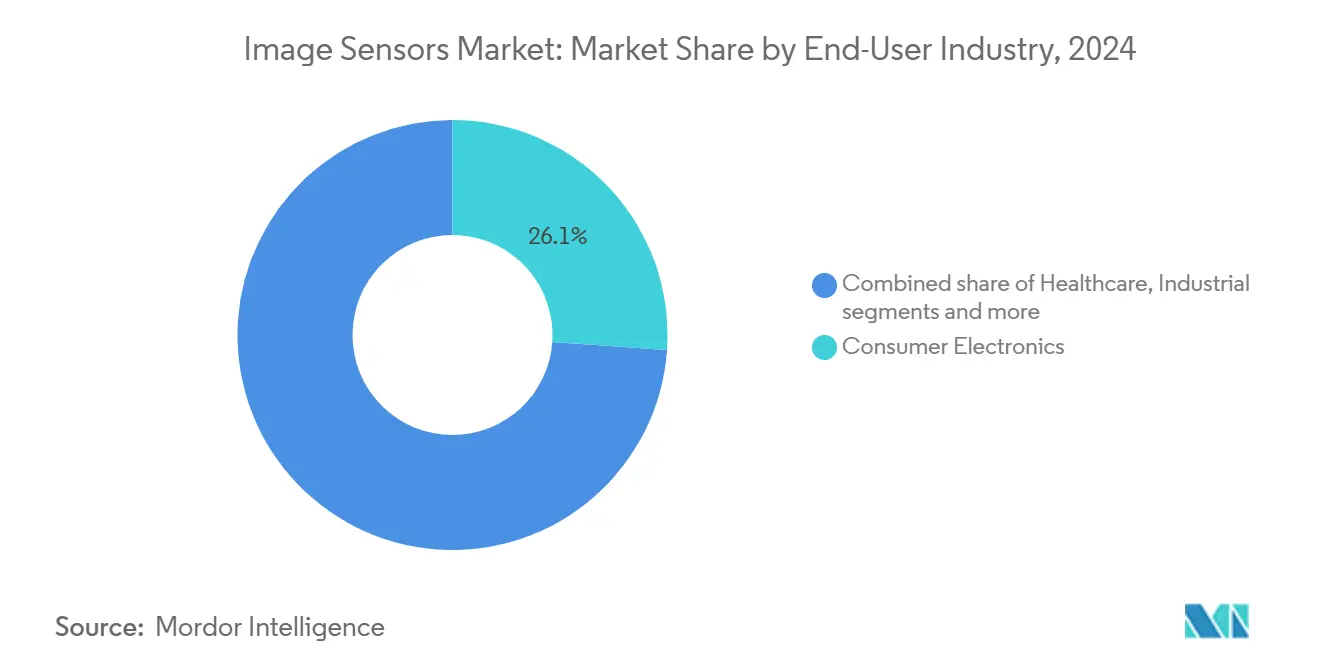

- By end-user industry, consumer electronics held 26.11% share of the Europe image sensors market size in 2024, whereas automotive applications are advancing at a 12.40% CAGR between 2025-2030.

- By geography, Germany accounted for 24.00% share of the Europe image sensors market size in 2024, while Italy is the fastest climber at 10.30% CAGR to 2030.

Europe Image Sensors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-camera smartphone race beyond 200 MP | 1.80% | Germany, France, UK | Medium term (2-4 years) |

| Euro NCAP front-camera mandate (AEB) | 2.10% | EU-wide, strongest in Germany | Short term (≤ 2 years) |

| Wafer-level optics & stacked CIS migration | 1.50% | Germany, Netherlands, France | Long term (≥ 4 years) |

| AI-enabled industrial machine-vision grants | 1.20% | Germany, Italy, Netherlands | Medium term (2-4 years) |

| Disposable chip-on-tip medical endoscopy | 0.90% | Germany, France, UK | Long term (≥ 4 years) |

| EU smart-city surveillance tenders | 0.70% | Major metropolitan areas EU-wide | Medium term (2-4 years) |

Source: Mordor Intelligence

Multi-camera smartphone race >200 MP

European brands escalate sensor resolution beyond 200 MP to counter Asian rivals. Pixel-binning improves low-light results without ballooning file sizes, while wafer-level optics keeps camera bumps in check. OmniVision’s 0.56 µm pixels prove technical feasibility and highlight thermal-management trade-offs. Device makers now value European packaging specialists that co-design optics, DSP and AI pipelines in tight form factors. Adoption is set to widen from 2026 as algorithms mature and cost curves bend. [1]OmniVision Technologies, “OMNIVISION Commercializes World's Smallest Pixel in New 200 MP Image Sensor,” ovt.com

Euro NCAP AEB front-camera mandate

Euro NCAP’s updated star-rating system makes forward-facing cameras compulsory for Automatic Emergency Braking across new models launched from 2026. The rule extends to cyclist and pedestrian detection, increasing sensor resolution and dynamic-range targets. OnSemi’s Hyperlux family delivers 150 dB HDR tuned for glare-filled road scenes, lowering validation time for German and Italian OEMs. European tier-1 suppliers benefit from geographical proximity to test tracks and regulatory bodies, shortening loop times between prototype and series production. [2]OnSemi Technical Blog, “How Far Should Automatic Emergency Braking Mandate Be Pushed,” onsemi.com

Wafer-level optics and stacked CIS migration

Thin, high-precision lens stacks fabricated at wafer scale shave millimetres off module height while boosting MTF. When coupled with 3D-stacked CIS where photodiode and logic are on separate layers, frame rates rise and power drops. EV Group and Fraunhofer IZM-ASSID push bonding-debonding know-how that underpins this shift, positioning continental fabs to sell performance rather than cost. Licensing fees for stacked IP tighten smaller firms’ margins, adding impetus for joint-ventures or consolidation.

AI-enabled industrial machine-vision grants

Horizon Europe funnels grant into hyperspectral and neuromorphic projects that promise real-time inspection with 100× lower energy draw. The EUR 5.7 million MULTIPLE projects in steel and food plants shows scrap reduction and energy savings, while the NimbleAI consortium targets 50× latency cuts. VDMA projects machine-vision turnover of EUR 13.8 billion by 2025, reinforcing a structural shift toward AI-rich sensors sourced from European labs close to production lines. [3]VDMA Machine Vision, “Machine Vision,” vdma.org

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High EU energy & clean-room utility costs | -1.40% | Germany, Netherlands, France | Short term (≤ 2 years) |

| Limited 300mm CIS-grade capacity | -0.80% | EU-wide manufacturing | Medium term (2-4 years) |

Source: Mordor Intelligence

High EU energy and clean-room utility costs

Electricity and ultra-pure water bills in Europe sit 30-50% above Asian averages. Carbon-neutrality pledges force fabs to pre-pay for renewable power contracts and HVAC upgrades. STMicroelectronics’ roadmap to reach carbon neutrality by 2027 exemplifies the capital drag. Smaller foundries lacking volume to offset these overheads either exit or pivot to fab-lite models. Europe image sensors market players see near-term margin squeeze yet gain reputational leverage with ESG-focused buyers.

Limited 300 mm CIS-grade capacity

The continent trails Asia in 300 mm volume, and ASML export curbs funnel more scanners toward non-EU customers. Intel’s and TSMC’s Dresden and Magdeburg projects will add wafers, but most capacity is earmarked for logic rather than CIS. Sensor specialists must reserve slots years ahead or partner with Asian fabs, raising IP-leak concerns. Until new lines open, tight wafer supply keeps lead times long and prices firm, dampening high-volume consumer deals.

Segment Analysis

By Type: CMOS dominance accelerates global-shutter adoption

CMOS sensors captured 86.30% of Europe image sensors market share in 2024 on the back of lower power draw and logic integration. Global-shutter variants, vital for motion-heavy automotive and robotics tasks, are pacing at 9.30% CAGR and will command a larger slice of the Europe image sensors market by 2030. Rolling-shutter CMOS stays relevant for price-sensitive phones and laptops, while CCD retreats into scientific niches where ultra-low noise still matters.

European firms exploit close ties with automakers to co-design ASIL-B qualified global-shutter parts, gaining early design-wins for Euro NCAP 2026 models. Wafer-level optics and deep-trench isolation raise quantum efficiency without inflating die size. Consequently, Europe image sensors market size for global-shutter devices is projected to climb steadily, lifting regional revenue resilience even if consumer cycles soften.

Note: Segment shares of all individual segments available upon report purchase

By Resolution: Ultra-high megapixel race transforms mobile imaging

The 25-64 MP class led revenue with 28.44% share in 2024, balancing file-size economy and computational workload. However, >200 MP parts rise at 12.33% CAGR, fuelled by flagship phones that tout lossless digital zoom and 8K video crops. Europe image sensors market size for these ultra-resolution devices will expand fastest in 2025-2030 as pixel-binning algorithms mature.

Packaging advances that align wafer-level optics with sub-µm pixels curb lens aberration, letting European module makers enter premium handset SKUs. The Europe image sensors market observes OEMs procuring specialty glass and IR filters domestically to hedge against Asian supply shocks. Entry-level handsets still rely on ≤8 MP chips, keeping a floor under high-volume rolling-shutter production.

By Spectrum: Near-infrared momentum beyond visible light

Visible RGB accounted for 54.00% of 2024 shipments, yet near-infrared (NIR) is sprinting at 13.40% CAGR as ADAS night vision, face unlock, and machine-vision inspection spread. SWIR sensors with quantum-dot films integrate into standard CMOS flows, cutting cost versus III-V hybrids. Europe image sensors market vendors tap local photonics institutes to refine material stacks that extend spectral reach while retaining wafer-level economies.

Thermal long-wave infrared remains pricier due to exotic materials but wins contracts in pedestrian detection and building diagnostics when stringent safety or ESG audits demand it. Diversification across spectra cushions revenue swings linked to handset replacement cycles, giving Europe image sensors industry leaders steadier cash flow.

By Shutter Technology: Global-shutter migration curbs motion artifacts

Rolling-shutter chips still held 71.00% unit share in 2024 because mobile phones tolerate minor skew. Yet Europe image sensors market demand for artifact-free capture in self-driving and robotics scenarios lifts global-shutter volumes at 12.90% CAGR. Pixel architectures such as dual-conversion gain and backside deep-trench isolation help marry speed with low noise.

Automotive design-rules like AEC-Q100 and ISO 26262 push suppliers to validate across –40 °C to 125 °C. European test labs with climatic chambers near OEM RandD hubs shorten qualification loops, locking in multi-year supply contracts that insulate against consumer price wars.

By End-User Industry: Automotive transformation reshapes demand

Consumer electronics retained 26.11% revenue share in 2024, but autos will expand fastest at 12.40% CAGR through 2030. Component count per vehicle climbs as HD surround-view, driver monitoring and interior occupant sensing become standard. Europe image sensors market size tied to automotive thus scales structurally with EU safety rules rather than discretionary spending.

Healthcare gains momentum via disposable chip-on-tip endoscopes that marry 0.55 mm sensors with LED illumination. Industrial players install AI-ready cameras on production lines to limit scrap and energy waste, qualifying for Horizon Europe green grants. This broadened mix diversifies earnings and lowers sensitivity to single-sector downturns across the Europe image sensors industry.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Germany, with 24.00% share in 2024, anchors the Europe image sensors market through its automotive giants and 130-member machine-vision cluster. Even after a 10% sales dip in 2024, VDMA projects factory-automation rebound powered by AI cameras. Dresden’s budding fab-corridor and car-maker proximity sustain bilateral feedback loops that speed part validation.

Italy grows quickest at 10.30% CAGR as northern clusters serving Ferrari and Lamborghini add Level 2+ camera systems. National smart-city rollouts in Milan and Rome tender high-resolution surveillance contracts that lean on European suppliers for data-sovereignty assurances. STMicroelectronics’ silicon-carbide investment north of Naples also underpins local sensor packaging capacity.

France and the UK together add scale: aerospace and defense primes specify radiation-hard CMOS, while telcos roll fiber-to-home backed by camera-equipped field tools. Eastern EU states, funded by cohesion policy grants, fit NIR traffic-monitoring cameras to curb congestion and pollution. Across all zones, OEMs weight supplier selection toward Europe image sensors market incumbents that offer shorter logistics, GDPR alignment and transparent ESG reporting.

Competitive Landscape

The market shows moderate concentration. STMicroelectronics leads regional output yet saw its imaging revenue fall 10% year-on-year in Q2 2024, prompting cost cuts and a pivot to automotive electrification. AMS-Osram exploits micro-optics prowess for 1 mm² NanEyeM modules that play in single-use endoscopy where sterilization costs vanish. Emerging French firm Prophesee pushes event-driven vision that slices latency for robot arms.

Asian giants Sony, Samsung and OmniVision still supply European handset OEMs but face IP scrutiny under new EU chip-security rules. Photonics Management’s 2024 buy-out of BAE Systems’ imaging unit reflects consolidation toward firms with aerospace heritage and trusted-supplier flags. Litigation around stacked-CIS patents underscores why Europe image sensors market participants double-down on proprietary bonding stacks and local foundry access to secure differentiation.

Europe Image Sensors Industry Leaders

-

Sony Semiconductor Solutions

-

STMicroelectronics

-

Samsung System LSI (ISOCELL)

-

On Semiconducto

-

OmniVision Technologies

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: STMicroelectronics posted USD 2.52 billion Q1 sales; Analog, MEMS and Sensors slid 23.9% YoY as handset softness lingered.

- March 2025: Sony confirmed 200 MP sensor for Xperia 1 VII to counter Samsung HP2, widening ultra-high-resolution race.

- January 2025: Dutch export controls on advanced lithography start April 2025, squeezing ASML’s China sales and tightening EU capacity.

- December 2024: Photonics Management acquired BAE Systems’ Imaging Solutions division, adding aerospace-grade CMOS lines.

Europe Image Sensors Market Report Scope

An image sensor is an electronic device that transforms an optical image into an electronic signal.

The Europe Image Sensors Market is Segmented by Type (CMOS, CCD), End-User Industry (Consumer Electronics, Healthcare, Industrial, Security and Surveillance, Automotive and Transportation, Aerospace and Defense), and Country.

| By Type | CMOS |

| CCD | |

| By Resolution | 8 MP |

| 924 MP | |

| 2564 MP | |

| 65200 MP | |

| > 200 MP | |

| By Spectrum | Visible (RGB) |

| Near-Infrared (NIR) | |

| Short-Wave IR (SWIR) | |

| Ultraviolet (UV) | |

| Thermal / LWIR | |

| By Shutter Technology | Rolling-Shutter CMOS |

| Global-Shutter CMOS | |

| By End-User Industry | Consumer Electronics |

| Healthcare | |

| Industrial | |

| Security and Surveillance | |

| Automotive and Transportation | |

| Aerospace and Defense | |

| Other End-user Industries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe |

By Type

| CMOS |

| CCD |

By Resolution

| 8 MP |

| 924 MP |

| 2564 MP |

| 65200 MP |

| > 200 MP |

By Spectrum

| Visible (RGB) |

| Near-Infrared (NIR) |

| Short-Wave IR (SWIR) |

| Ultraviolet (UV) |

| Thermal / LWIR |

By Shutter Technology

| Rolling-Shutter CMOS |

| Global-Shutter CMOS |

By End-User Industry

| Consumer Electronics |

| Healthcare |

| Industrial |

| Security and Surveillance |

| Automotive and Transportation |

| Aerospace and Defense |

| Other End-user Industries |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe image sensors market?

The market is valued at USD 4.1 billion in 2025 and is forecast to reach USD 6.21 billion by 2030.

Which segment is growing fastest within the market?

Automotive applications lead with a 12.40% CAGR thanks to Euro NCAP safety mandates and ADAS proliferation.

Why are global-shutter CMOS sensors important for automotive use?

They eliminate motion-induced distortions, ensuring accurate object detection for Automatic Emergency Braking and other safety features.

How is the EU Chips Act influencing regional supply?

Subsidies and capacity incentives aim to raise Europe’s global semiconductor share to 20% by 2030, supporting local image-sensor lines amid export-control uncertainty.

Which country currently leads the market in Europe?

Germany holds 24.00% share due to its strong automotive and industrial automation sectors.

What role do wafer-level optics play in sensor design?

They reduce module thickness and improve optical performance, allowing high-resolution cameras to fit slim smartphones and ADAS housings.

Page last updated on: July 6, 2025