Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

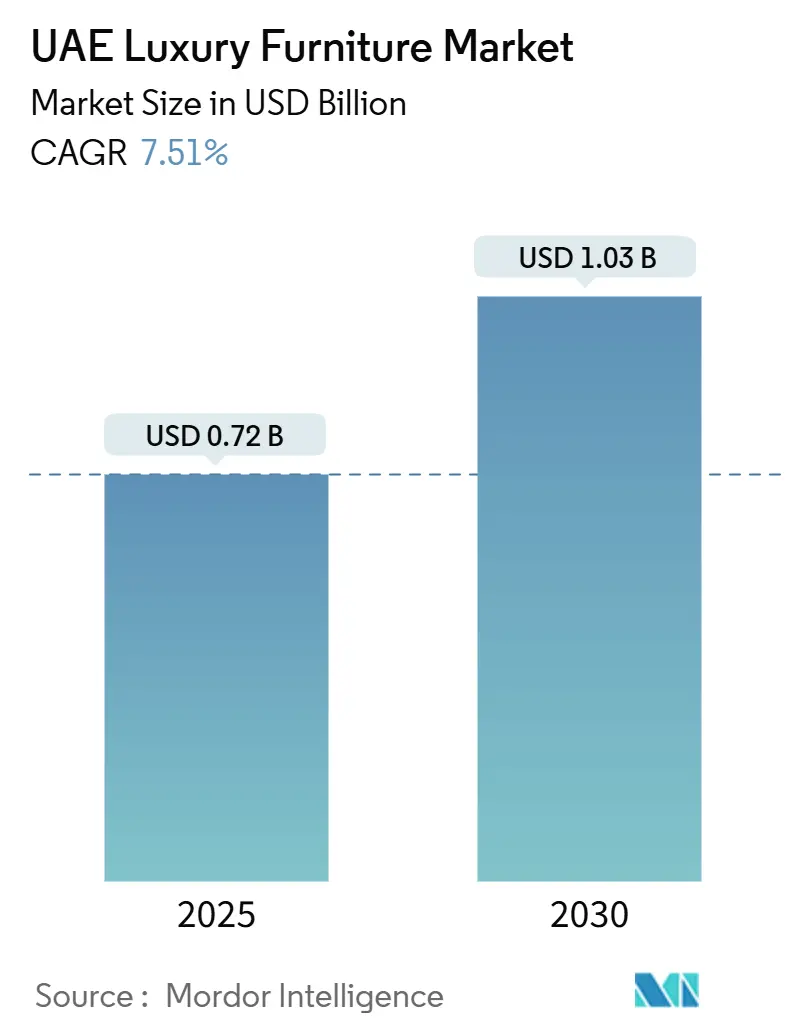

| Market Size (2025) | USD 0.72 Billion |

| Market Size (2030) | USD 1.03 Billion |

| Growth Rate (2025 - 2030) | 7.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Luxury Furniture Market Analysis by Mordor Intelligence

The UAE luxury furniture market size stands at USD 0.72 billion in 2025 and is projected to reach USD 1.03 billion by 2030, registering a 7.51% CAGR over 2025-2030. Steady inflows of ultra-high-net-worth (UHNW) households, robust branded-residence pipelines, and sustained government investment in mega-projects underpin demand growth for bespoke interiors and premium furnishings. Digital transformation is reshaping buyer journeys, with augmented-reality (AR) showrooms and unified commerce platforms encouraging higher-ticket online transactions. Product innovation around smart, wellness-oriented features, especially circadian lighting and IoT-enabled seating, continues to justify premium pricing. Supply-side players improve resiliency through duty-suspension free-zone logistics and selective local assembly, partially mitigating import-cost volatility while accelerating speed to project sites.

Key Report Takeaways

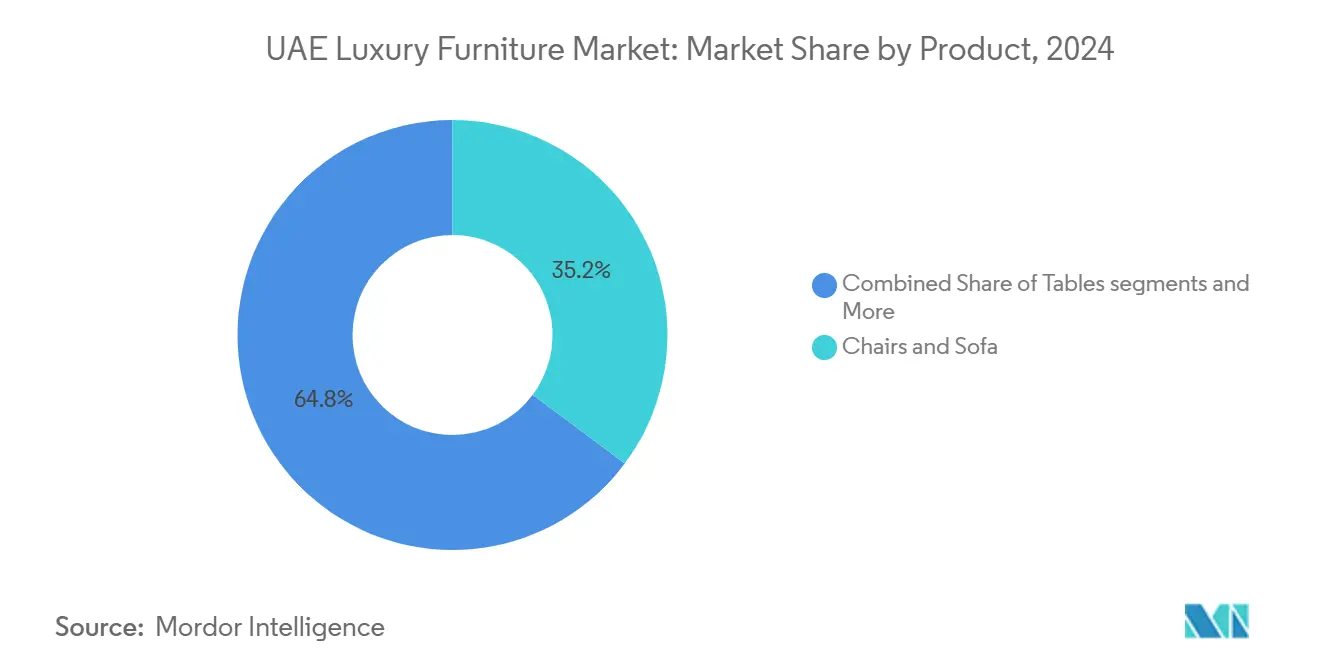

- By product, chairs & sofas captured 35.24% of the UAE luxury furniture market share in 2024, while smart lighting is forecast to expand at a 10.27% CAGR through 2030.

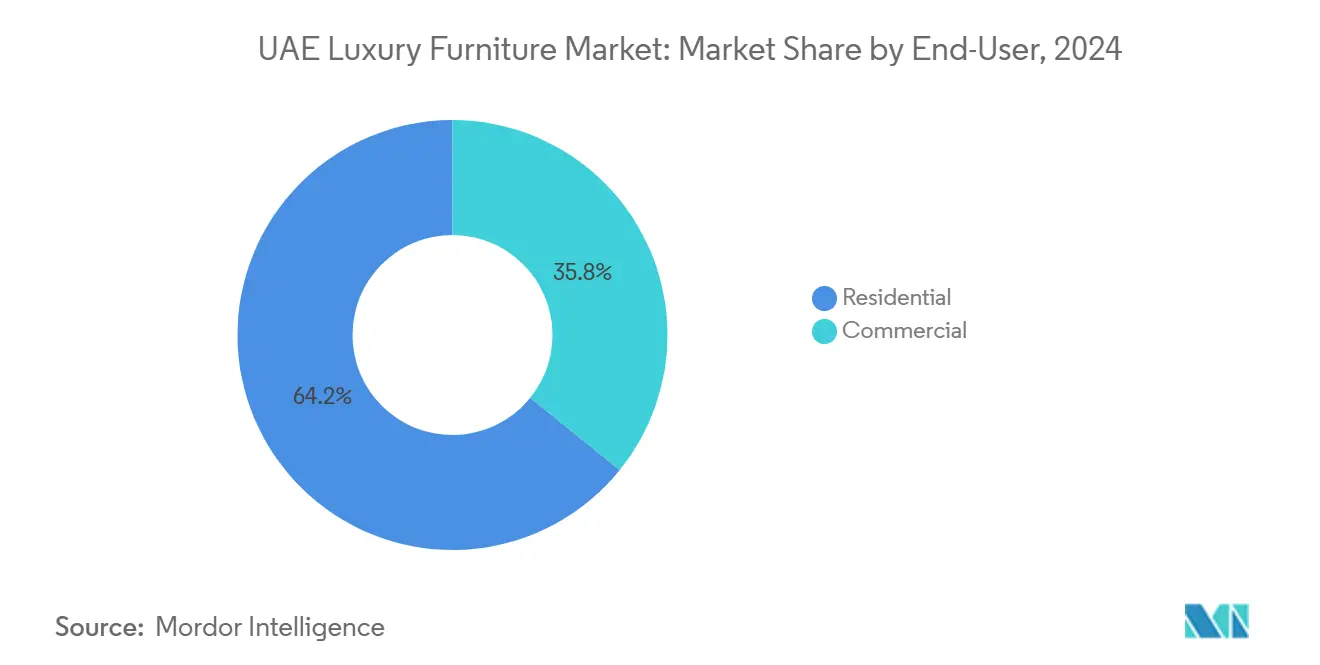

- By end user, residential held 64.24% share of the UAE luxury furniture market size in 2024 and commercial applications are projected to grow at a 9.27% CAGR to 2030.

- By distribution channel, flagship stores accounted for a 37.33% share of the UAE luxury furniture market size in 2024, whereas online channels are advancing at a 13.24% CAGR through 2030.

- By geography, Dubai led with 56.37% share of the UAE luxury furniture market size in 2024, and Ras Al Khaimah is expected to post the fastest 11.73% CAGR to 2030.

UAE Luxury Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in ultra-high-net-worth households | +1.8% | UAE-wide (Dubai & Abu Dhabi focus) | Medium term (2-4 years) |

| Government visa reforms boosting real estate | +1.2% | National | Short term (≤ 2 years) |

| Expansion of branded residential projects | +0.9% | Dubai, Abu Dhabi, Ras Al Khaimah | Medium term (2-4 years) |

| Growth of design-led retail districts | +0.7% | Dubai Design District, Abu Dhabi cultural quarter | Long term (≥ 4 years) |

| Digital-nomad influx | +0.6% | Dubai Marina, Business Bay, Downtown | Short term (≤ 2 years) |

| ESG-focused interiors | +0.5% | UAE-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Ultra-High-Net-Worth Households

Millionaire migration to the UAE hit record levels in 2025, with a net inflow of 9,800 UHNW residents[1]Al Arabiya English, “Sheikh Mohammed approves Phase II of Dubai 2040 Urban Master Plan,” english.alarabiya.net.. Their preference for multi-property portfolios amplifies furniture procurement because each residence demands a complete interior solution. Expenditure per UHNW buyer is three to five times higher than standard luxury purchasers, expanding the value pool even though the customer base is comparatively small. Demand tilts toward bespoke seating, artisanal woodwork, and heritage brand collaborations that signal status. Secondary-home furnishing often occurs simultaneously with primary-home projects, smoothing revenue seasonality for suppliers. Forward pipelines suggest continued migration from Europe and North America seeking political stability and tax efficiency, reinforcing the UAE luxury furniture market trajectory.

Government Visa Reforms Fuelling Real Estate Purchases

Golden Visa eligibility for investors, entrepreneurs, and specialized talent has reclassified UAE property from a transient asset to a long-term residence. Transaction records indicate that visa holders spend 40% more on luxury furnishings than short-term expatriates, reflecting longer tenures and lifestyle anchoring. The issuance expansion planned for 2025 will widen the pool of qualified buyers, sustaining a pipeline of new homes needing complete interiors. Tax rebates totalling USD 871.46 million (AED 3.2 billion) granted to UAE nationals building residences unlock incremental budgets for premium finishes[2]“Guides, References & Public Clarifications,” Federal Tax Authority, tax.gov.ae.. Furniture brands collaborate with real-estate brokers to bundle design services at the point of sale, capturing demand before competing discretionary categories. Digital documentation of visa status simplifies financing for large-ticket furniture purchases, further enlarging the addressable market.

Rapid Expansion of Branded Residential Projects

Projects such as Six Senses Residences Dubai Marina and Fairmont Residences Solara Tower impose strict brand-aligned design codes that mandate specific furniture aesthetics and performance standards. Supply contracts often run into multi-million-dollar values, offering high visibility and volume. Wellness-centric layouts call for circadian lighting, biophilic materials, and ergonomic seating that merge hospitality specifications with private living requirements. Automotive-branded towers like Mercedes-Benz Places demand furniture reflecting automotive cues, creating niches for bespoke metalwork and leather craftsmanship. Developers centralize procurement to ensure consistency across units, enabling suppliers to secure repeat orders over multi-year construction timelines. Brands that demonstrate compliance with LEED and WELL standards gain competitive leverage, as sustainability now intersects with luxury positioning. The cumulative effect is a structural uplift in premium categories, particularly smart lighting and modular seating systems.

Growth of Design-Led Retail Districts

Dubai Design District's evolution into a comprehensive design ecosystem creates unique distribution advantages for luxury furniture brands while elevating customer expectations for experiential retail. The district's integration of showrooms, design studios, and cultural venues generates cross-pollination effects where furniture purchases become part of broader lifestyle experiences rather than isolated transactions. Poltrona Frau's dedicated showroom within the district exemplifies how premium brands leverage the environment to justify higher price points through immersive brand experiences. The district model influences customer behaviour by encouraging longer engagement periods and higher transaction values, as buyers can visualize complete interior concepts rather than individual pieces. Government investment in cultural programming and design events within the district creates regular traffic flows that benefit all participants, reducing individual marketing costs while elevating the overall market perception.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependency | −1.4% | UAE-wide | Short term (≤ 2 years) |

| Volatile real-estate cycles | −0.8% | Dubai & Abu Dhabi | Medium term (2-4 years) |

| Sustainability scrutiny on exotic woods | −0.6% | UAE-wide | Long term (≥ 4 years) |

| Talent shortage in bespoke artisanship | −0.5% | Dubai & Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Dependency on Imported Luxury Furniture

All high-end pieces arrive from China, Thailand, Germany, India, and Malaysia, exposing the UAE luxury furniture market to freight rate volatility and currency swings. Dubai’s lower courier duty-free threshold from USD 81.68 – USD 264.18 (AED 970 to AED 300) raises landed costs for e-commerce orders, curbing impulse upgrades. Supply chain shocks delay fit-out schedules for branded residences, risking penalty clauses for developers. Duty suspension in free zones offers partial relief but limits domestic consumption because re-export rules apply. The Make it in the Emirates initiative earmarks USD 4.36 billion (AED 16 billion) for local manufacturing, but upscale production also requires artisans and design intellectual property that need time to cultivate[3]“Fourth Edition of Make it in the Emirates Forum 2025,” Ministry of Industry and Advanced Technology, moiat.gov.ae. . Meanwhile, sellers must hedge currency exposures and diversify logistics partners to maintain margin stability.

Volatile Real-Estate Transaction Cycle

Luxury furniture sales correlate closely with property handovers. Historical data show sharp swings aligned with oil prices and global liquidity, affecting order pacing. Although Grade-A office occupancy hit 94% in Dubai and 96% in Abu Dhabi in 2024, sudden sentiment shifts can freeze discretionary spending. Developers attempt to smooth cycles by phasing releases under the Dubai 2040 Urban Master Plan, yet high-end buyers remain sensitive to equity market corrections. Furniture suppliers counteract volatility through service contracts, storing finished goods for scheduled fitouts, and targeting government-funded projects less exposed to private financing risk. Multi-year mega-projects such as Meydan One create baseline demand that partly cushions cyclical dips. However, maintaining skilled labour during slow periods remains costly, underscoring structural vulnerability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Integration Elevates Premium Categories

Chairs & sofas anchor luxury living areas, holding 35.24 % of the UAE luxury furniture market share in 2024. High-back sectional designs and modular seating accommodate large majlis-style spaces common in Emirati villas. Smart lighting, the fastest-growing category at a 10.27% CAGR, marries IoT sensors with wellness analytics to adjust kelvin temperature by time of day [4]Hospitality Net, “Six Senses Residences Dubai Marina Engineered with Integrated Wellness,” hospitalitynet.org.. Buyers consider circadian-optimized fixtures integral to branded-residence wellness promises. Tables and cabinets benefit from open-plan kitchens where entertaining merges dining with show cooking, spurring demand for statement marble islands and hidden-storage buffets. Bedroom suites continue to command steady replacements as developers’ pre-fit penthouse shells for turnkey sales. Accessories, particularly limited-edition objects d’art, help retailers cross-sell during end-of-project styling phases.

The UAE luxury furniture market size for smart lighting was valued at USD 0.08 billion in 2024 and is set to climb alongside home-automation penetration. Italian and Scandinavian makers now embed voice-activated drivers that link to UAE-based telecom smart-home hubs, reducing latency and elevating perceived quality. Local integrators bundle seating, lighting, and AV controls into a single mobile-app dashboard, creating ecosystem lock-in that reduces churn. Importantly, ESG-driven interior requirements boost demand for FSC-certified timber lamps and energy-efficient LED modules. Retailers allocate prominent in-store space to demo zones where architects can program scenes for client walkthroughs. The tightening link between design intent and technology specification reinforces supplier relationships early in project tender stages.

By Distribution Channel: Omnichannel Innovation Escalates Online Adoption

Flagship stores captured 37.33% share in 2024, anchoring brand equity through immersive displays and personalized consultation. Online channels are forecast to post a 13.24% CAGR, reflecting the maturity of AR-powered visualization that reduces hesitation toward big-ticket digital purchases. Specialty stores in design districts thrive on curated assortments and collaborations with local artisans. Home centers leverage a coordination scale to stock fast-moving luxury basics and offer same-day delivery to metropolitan districts. Pop-up galleries and private appointment-only salons comprise other channels that appeal to discreet UHNW clients who prefer intimate shopping environments.

Digital transformation strategies focus on unified inventory visibility between the warehouse, the storefront, and the e-commerce portals. Consumers increasingly research online and complete transactions in-store, or vice versa, necessitating consistent pricing and promotional messaging. Retailers invest in CRM tools to personalize outreach with fabric samples shipped directly to client homes. Exclusive online collections launch to capture tech-savvy expatriates abroad who plan home décor before relocating. The channel mix demonstrates that convenience, experience, and trust co-exist rather than cannibalize one another in the UAE luxury furniture market.

By End User: Commercial Momentum Complements Residential Core

The residential segment held 64.24% revenue in 2024, supported by continuous villa and branded-apartment deliveries. Nevertheless, commercial demand is forecast to grow at a 9.27% CAGR as corporate headquarters relocate to free-zone districts with wellness-compliant office specifications. The UAE luxury furniture market size allocated to commercial projects benefits from technology firms like Microsoft investing USD 1.5 billion in AI infrastructure, which includes premium executive suites. Hospitality refurbishments parallel tourism recovery, with luxury hotel pipelines mandating contract-grade finishes. Retail flagships within design districts adopt gallery-style fitting stations that require custom cabinetry and flexible lighting. Education and healthcare developments also specify high-end furnishings to enhance institutional branding.

Commercial clients value lifecycle cost over sticker price, favouring suppliers that provide post-installation maintenance. Sustainability certifications such as LEED and Fitwel increasingly gate tender participation. Long replacement cycles generate steady aftermarket service revenue, partially offsetting economic slowdowns. Suppliers offering acoustic solutions integrated into furniture align with hybrid work trends, emphasizing quiet zones. Cross-segment synergies arise when UHNW individuals who are company owners replicate office aesthetic preferences at home, multiplying purchase volume for consistent brands.

Geography Analysis

Dubai's market leadership at 56.37% share in 2024 reflects its established position as the UAE's luxury capital, supported by concentrated UHNW populations, extensive retail infrastructure, and ongoing mega-project developments worth over USD 100 billion through the Dubai 2040 Urban Master Plan. The emirate benefits from unique advantages, including Dubai Design District's ecosystem of showrooms and design studios, established relationships with international luxury brands, and infrastructure supporting complex logistics requirements for high-value furniture imports. Major developments, including Meydan One's 550 retail outlets and Six Senses Residences Dubai Marina, create sustained demand for both residential and commercial luxury furnishing. The emirate's tourism infrastructure, attracting up to 25 million visitors by 2040, drives hospitality furniture demand through hotel expansions and luxury retail environments.

Abu Dhabi represents 25% market share in 2024, driven by government sector procurement, cultural district developments, and sovereign wealth fund investments in luxury real estate and hospitality projects. The emirate's focus on cultural institutions, including the expanded Louvre Abu Dhabi and planned Guggenheim Abu Dhabi, creates specialized demand for museum-quality furniture and exhibition fixtures that meet international conservation standards. Abu Dhabi's emphasis on sustainability through initiatives supporting UAE Net Zero 2050 targets influences procurement specifications toward certified materials and circular economy principles. The emirate benefits from concentrated government spending on prestige projects and diplomatic facilities that require premium furnishing to reflect the national image and support international relations.

Ras Al Khaimah emerges as the fastest-growing geography at 11.73% CAGR through 2030, benefiting from luxury tourism developments, including the Wynn resort project and Al Marjan Island residential communities that attract international buyers seeking alternatives to Dubai's premium pricing. The emirate's strategic positioning offers cost advantages while maintaining proximity to Dubai's infrastructure and services, creating appeal for luxury residential projects targeting price-sensitive UHNW buyers. The smaller emirates of Sharjah, Ajman, Fujairah, and Umm Al Quwain collectively represent emerging opportunities as federal infrastructure investments and tourism initiatives create new luxury residential and hospitality projects. These markets benefit from spillover effects from Dubai and Abu Dhabi, where established luxury furniture suppliers can leverage existing relationships and distribution networks to serve new geographic markets with low additional investment requirements.

Competitive Landscape

The UAE luxury furniture market shows moderate concentration, with the top five players controlling a significant share of the market. This structure leaves room for both well-established international brands and agile new entrants to compete effectively. Market leaders such as Roche Bobois and Marina Home Interiors adopt distinct strategies Roche Bobois emphasizes its French design heritage and flagship retail experiences, while Marina Home leverages deep local market knowledge built over two decades. The competitive landscape is shifting toward technology integration, where features like smart furniture and IoT capabilities are becoming essential. As a result, players who innovate in tech-driven product offerings are gaining an edge over traditional brands.

White-space opportunities are emerging in the sustainable luxury segment, where few current players meet rising ESG expectations. Increasing demand for certified materials, circular economy practices, and sustainable procurement opens the door for differentiated offerings. Traditional luxury brands often face challenges in digitization, giving tech-savvy disruptors a chance to carve out market share. Companies investing in AR showrooms, virtual interior design tools, and smart home integration are better positioned to capture evolving consumer preferences. These digital capabilities are no longer optional but central to maintaining relevance in a tech-forward market.

The UAE’s regulatory environment is also shaping the market, especially with the introduction of the UAE Climate Law and stricter building certification standards. These changes are pushing furniture suppliers to align with sustainability benchmarks and offer documentation suitable for ESG reporting. Additionally, the rise of branded residential developments is introducing new demands, blending luxury retail expectations with hospitality-grade functionality. This shift favors companies capable of offering both bespoke craftsmanship and scalable production for large projects. Overall, success in the UAE luxury furniture market depends on combining aesthetic excellence with technological innovation, regulatory compliance, and operational agility.

UAE Luxury Furniture Industry Leaders

Roche Bobois

Marina Home Interiors

Natuzzi Italia

Poltrona Frau

Ethan Allen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Fairmont Residences Solara Tower Dubai announced scheduled completion for Q3 2027, featuring 251 luxury residences in Downtown Dubai with integrated wellness amenities requiring specialized furniture for biophilic design and wellness-focused living spaces.

- November 2024: Ministry of Industry and Advanced Technology announced the fourth Make it in the Emirates Forum for May 2025, featuring a dedicated Emirati handicrafts pavilion. The forum signals government support for local luxury furniture production and offers financing solutions for technology adoption and manufacturing capacity expansion.

- October 2024: Six Senses Residences Dubai Marina announced as the world's tallest residential tower, scheduled for Q1 2026 completion with 122 stories and 251 wellness-focused residences requiring specialized furniture for integrated wellness wardrobes, biohacking equipment storage, and sensory art installations.

- April 2024: Microsoft announced USD 1.5 billion investment in G42's AI infrastructure projects across the UAE, driving demand for premium office furniture and executive suites in new data center facilities and corporate headquarters expansions.

UAE Luxury Furniture Market Report Scope

By Product

| Lighting |

| Tables |

| Chairs and Sofas |

| Accessories |

| Bedroom |

| Cabinets |

| Other Products |

By End User

| Residential |

| Commercial |

By Distribution Channel

| Home Centers |

| Flagship Stores |

| Specialty Stores |

| Online |

| Other Distribution Channels |

By Geography

| Dubai |

| Abu Dhabi |

| Sharjah |

| Ras Al Khaimah |

| Ajman |

| Fujairah |

| Umm Al Quwain |

| By Product | Lighting |

| Tables | |

| Chairs and Sofas | |

| Accessories | |

| Bedroom | |

| Cabinets | |

| Other Products | |

| By End User | Residential |

| Commercial | |

| By Distribution Channel | Home Centers |

| Flagship Stores | |

| Specialty Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | Dubai |

| Abu Dhabi | |

| Sharjah | |

| Ras Al Khaimah | |

| Ajman | |

| Fujairah | |

| Umm Al Quwain |

Key Questions Answered in the Report

How large will premium furniture demand be in the UAE by 2030?

The UAE luxury furniture market is forecast to reach USD 1.03 billion by 2030, supported by a 7.51% CAGR over 2025-2030.

Which product category is expanding fastest?

Smart lighting leads growth, advancing at a 10.27% CAGR thanks to wellness-oriented IoT integration and branded-residence specifications.

Why does Dubai dominate high end furniture sales in the Emirates?

Dubai holds 56.37% share due to its dense UHNW population, robust retail infrastructure, and ongoing mega-projects that continually refresh demand.

What distribution model is gaining momentum?

Online channels are accelerating at a 13.24% CAGR as AR showrooms blend digital discovery with white-glove fulfilment.

Which emirate offers the fastest growth potential outside Dubai?

Ras Al Khaimah is expected to post an 11.73% CAGR through 2030, buoyed by luxury tourism projects and competitively priced waterfront developments.

Page last updated on: