Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

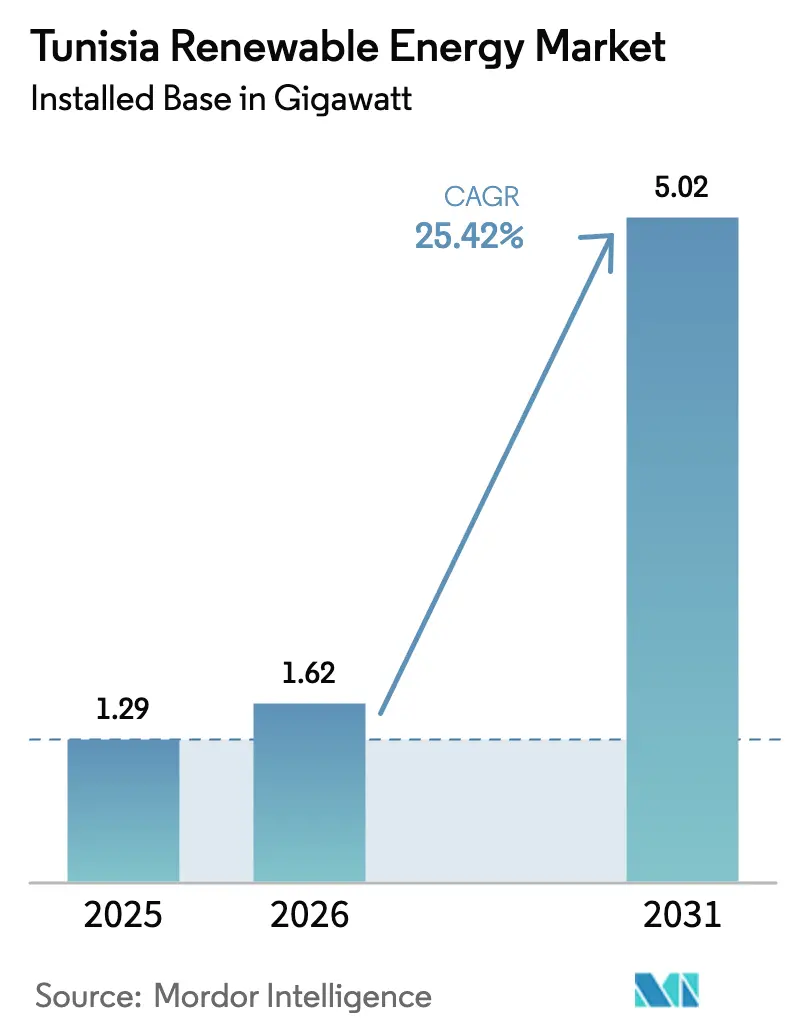

| Base Year Market Size (2025) | 1.29 gigawatt |

| Market Volume (2026) | 1.62 gigawatt |

| Market Volume (2031) | 5.02 gigawatt |

| Growth Rate (2026 - 2031) | 25.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tunisia Renewable Energy Market Analysis by Mordor Intelligence

Tunisia Renewable Energy Market size in 2026 is estimated at 1.62 gigawatt, growing from 2025 value of 1.29 gigawatt with 2031 projections showing 5.02 gigawatt, growing at 25.42% CAGR over 2026-2031.

Utility-scale auctions are lined up through 2026, along with new incentives for hybrid solar-plus-storage plants, which underpin capacity additions and attract global developers such as Scatec, TotalEnergies, and Chinese engineering consortiums.(1)Reuters Staff, “Tunisia’s renewable tenders draw record-low solar bids,” reuters.com The policy goal of 30% renewable penetration by 2030 is supported by Law No. 2015-12, which simplified permitting and invited private capital, while multilateral lenders finance grid upgrades that will unlock export opportunities through the 600 MW ELMED interconnector to Italy. Technology choice remains led by solar PV, yet concentrated solar power (CSP) is scaling rapidly because its thermal storage pairs well with Tunisia’s ambition to supply green hydrogen to Europe via the proposed SoutH2 Corridor (totalenergies.com). Rooftop systems for factories and commercial buildings are gaining momentum under dedicated World Bank credit lines, signaling a broader democratization of clean-energy access across the country’s industrial hubs.

Key Report Takeaways

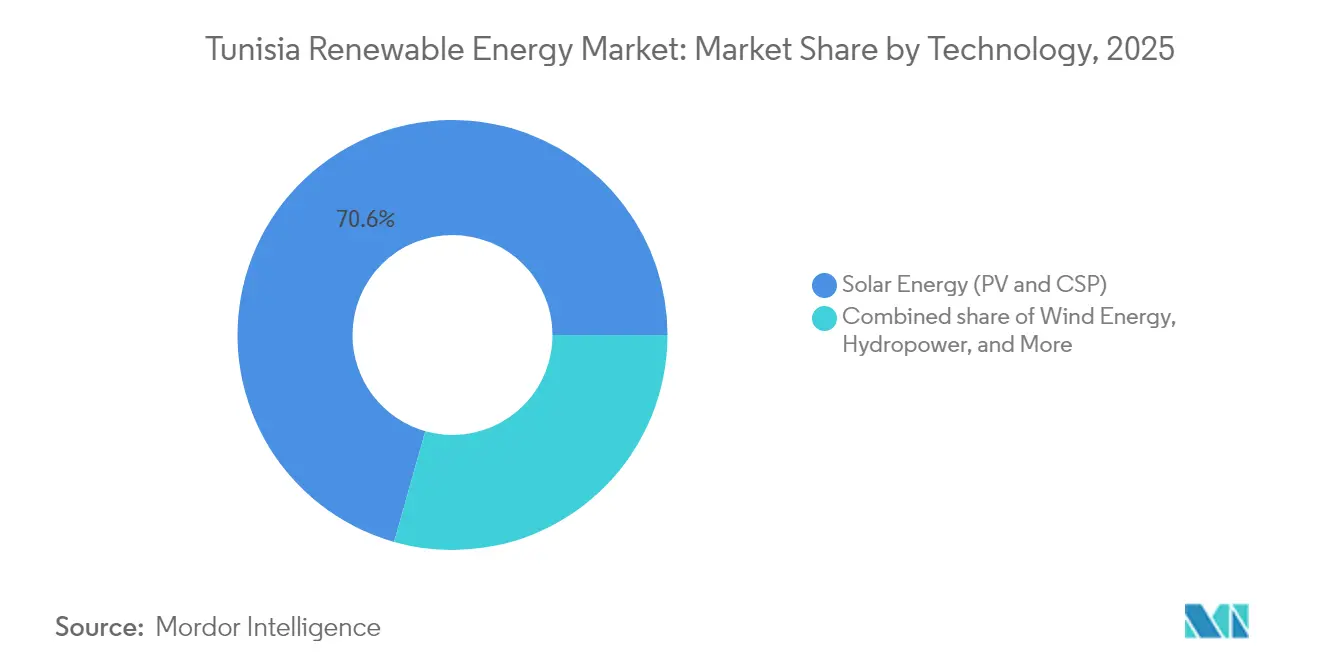

- By technology, solar energy commanded 70.62% share of the Tunisia renewable energy market size in 2025, while onshore wind is projected to post the fastest 34.76% CAGR through 2031.

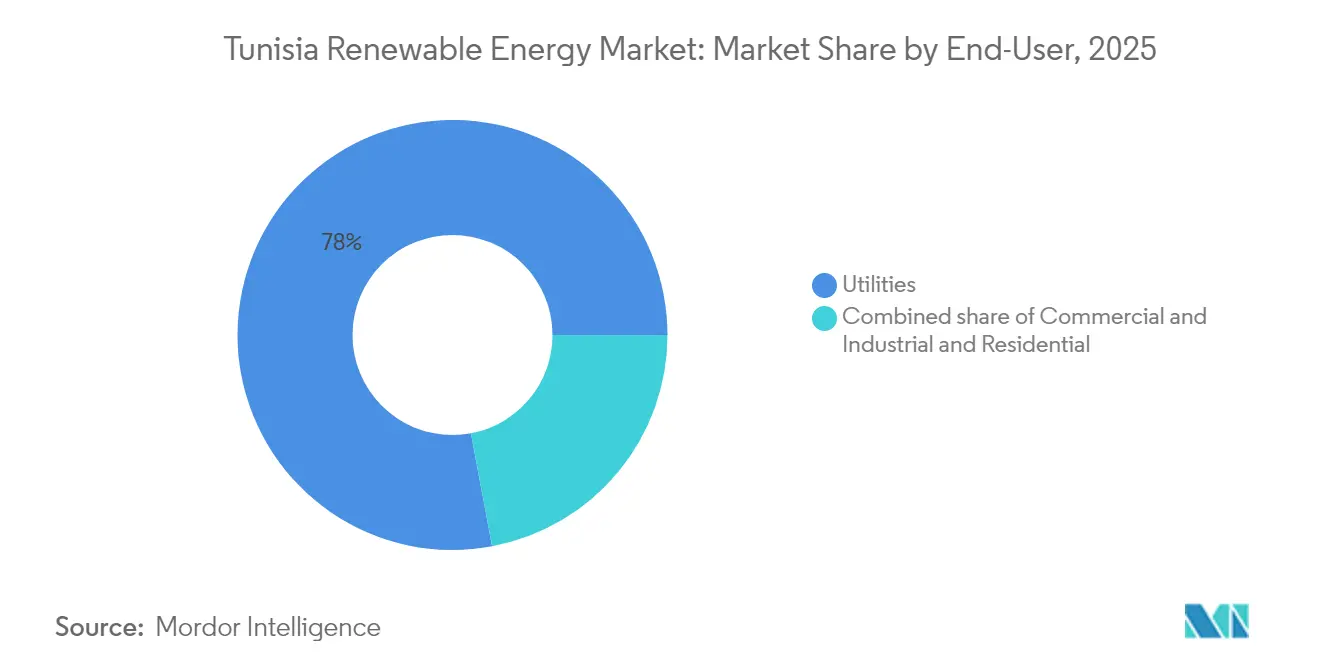

- By end-user, utilities held 77.95% of the Tunisia renewable energy market share in 2025, whereas the commercial-industrial segment is forecast to expand at a 27.14% CAGR thanks to liberalized self-consumption rules.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Tunisia Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility-scale solar PV auction roll-outs 2024–2026 | 8.50% | Sidi Bouzid, Gafsa, Tataouine, Kairouan | Short term (≤ 2 years) |

| Lower LCOE for hybrid PV + storage plants | 4.20% | Coastal industrial zones | Medium term (2-4 years) |

| EU–Africa HVDC interconnection incentives | 3.80% | Cap Bon to Sicily export corridor | Medium term (2-4 years) |

| Green-hydrogen export memoranda | 5.10% | Gabès, Kébili, Tozeur | Long term (≥ 4 years) |

| World Bank DER finance for C&I rooftops | 2.90% | Greater Tunis and coastal belts | Short term (≤ 2 years) |

| Agrivoltaic water-saving pilots | 1.30% | Interior governorates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Utility-scale Solar PV Auction Roll-outs 2024-2026

Systematic auctions covering 1,700 MW of new capacity guarantee 20- to 30-year PPAs with sovereign backing, enabling projects such as Qair’s 298 MW plant and Voltalia’s 130 MW facility in Gafsa at tariffs below USD 0.04/kWh.(2)PV Tech Editorial, “Qair wins 298 MW solar PPA in Tunisia,” pv-tech.org Annual output from awarded capacity is expected to reach 1,000 GWh, avoiding 250,000 t of natural-gas consumption worth USD 125 million and placing the Tunisia renewable energy market on a firm near-term growth path.(3)Zawya Staff, “Tunisia approves 1.7 GW of renewable tenders,” zawya.com Irradiation surpassing 2,000 kWh/m² in Tozeur and Sidi Bouzid drives capacity factors close to 25%, yet evacuation hinges on transmission upgrades co-financed by the EUR 113 million Siemens-led smart-grid program.

Lower LCOE for Hybrid (PV + Storage) Plants

Hybrid solar-plus-storage systems now operate at levelized costs below USD 0.06/kWh in high-resource areas, making them cheaper than gas-fired peaking turbines while supplying evening demand peaks. Lithium-ion battery prices declined by roughly 15% in 2024, and developers embed 2- to 4-hour storage to lift capacity factors above 40% and capture premium dispatch payments. Industrial estates around Tunis, Sfax, and Gabès have adopted the model to secure predictable electricity costs, spurring a secondary market for behind-the-meter energy management services.

EU-Africa HVDC Interconnection Incentives

The 600 MW ELMED submarine link, backed by EUR 268 million in concessional financing, will establish a physical export route to Europe and alter domestic merit-order dynamics. Once operational, Tunisian generators can tap higher Northern-Mediterranean wholesale prices, improving returns on large-scale solar and wind farms and reinforcing investor appetite for the Tunisia renewable energy market.

Green-hydrogen Export MoUs with EU Utilities

MoUs between ACWA Power, TotalEnergies, and European offtakers target 600,000 t of green hydrogen per year in the first phases, implying up to 12 GW of new renewable capacity dedicated to electrolysis by 2035. CSP plants with molten-salt storage gain preference because they deliver round-the-clock electricity to electrolyzers, reinforcing technology diversification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiscal stress at state utility STEG | –3.7% | Nationwide | Short term (≤ 2 years) |

| Grid congestion in coastal governorates | –2.4% | Tunis, Sfax, Sousse, Bizerte | Medium term (2-4 years) |

| Land-bank bottlenecks for onshore wind | –1.8% | Bizerte, Tataouine, Sidi Bouzid | Medium term (2-4 years) |

| Sovereign-risk premium on IPP financing | –4.1% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fiscal Stress at State Utility STEG

STEG’s debt reached TND 4 billion (≈ approximately USD 1.32 billion) in 2024, driving deferred grid upgrades and raising doubts about the bankability of the PPA. Subsidies consumed 5.3% of GDP in 2022, and multilateral guarantees, such as MIGA’s USD 23.5 million cover for the 120 MW Kairouan plant, have become essential. Recapitalization or subsidy reform is needed to restore credit and lower WACC.

Grid Congestion in Coastal Governorates

With 70% of demand on the coast and the best resources inland, transmission shortfalls hinder the commissioning of projects. Studies show that integrating 20% variable renewables requires a 5-8% increase in reserve capacity, yet STEG’s roadmap remains unfunded. Developers increasingly accept lower-irradiance sites near existing substations to sidestep delays, shaving IRRs by up to 100 basis points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Dominance Meets Wind Acceleration

Solar held 70.62% of the Tunisia renewable energy market in 2025, anchored by auctions that delivered the lowest tariff globally at 2.9 euro cents per kWh. Utility-scale wins totaling 498 MW in January 2025 keep solar's pipeline robust, and the Tunisia renewable energy market size for solar is forecast to exceed 3.4 GW by 2031. Yet wind's 34.76% CAGR will lift its share from 29.38% to nearly 36%, propelled by 600 MW of tenders and a 75 MW Chenini farm breaking ground in 2025. Floating offshore feasibility studies in the Gulf of Gabès hint at a future diversification path.

Solar's mature developer ecosystem, including Scatec, Voltalia, and Qair, benefits from pre-cleared land, rapid permitting, and proven O&M track records, while TuNur's 4.5 GW CSP export concept remains stalled due to the lack of Italian offtake. Wind advances face land-use complexity; yet, an eventual fast-track permitting regime could cut lead times by a year and support Tunisia's gains in renewable energy market share for wind equipment suppliers. Hybrid PV-plus-storage projects, now in the design stage, will enhance capacity factors and grid stability, reinforcing solar's lead while enabling wind to supply round-the-clock blends that appeal to future hydrogen electrolyzers.

By End-User: Utility Dominance With C&I and Residential Scaling

Utilities controlled 77.95% of installations in 2025 and are projected to sustain a 26.37% CAGR, reflecting STEG’s central dispatch and 20-25 year PPAs that lock in risk-adjusted returns for IPPs. The Tunisian renewable energy market size attributable to utilities could reach 3.9 GW by 2031, as the 1,700 MW December 2024 program is implemented. The C&I segment has 381 MW authorized but only 30 MW commissioned, a gap that TEREG aims to narrow by offering ten-year credit at 5-6% interest, thereby lifting IRRs and accelerating rooftop adoption. Large cement and phosphate processors are installing captive plants to buffer tariff hikes and curtailment risk.

Residential growth stems from the PROSOL Elec scheme, which financed 315 MW across 90,000 homes and secured TND 370 million (≈ approximately USD 121 million) for rebates in 2024-2026. New low-income pilots in Tozeur will showcase agrivoltaic-linked rural electrification. If net-metering credits fall below retail tariffs, middle-income adoption could slow, underscoring the need for a clear, long-term tariff policy to maintain the momentum in the residential renewable energy market share in Tunisia.

Geography Analysis

Southern governorates, such as Gafsa, Tozeur, and Sidi Bouzid, already account for more than 55% of operational solar capacity, taking advantage of DNI levels above 2,000 kWh/m² and land prices that are one-third of those in coastal zones. Voltalia’s 130 MW Gafsa plant and Scatec’s 120 MW Tozeur facility typify the region’s large-scale profile, but both depend on 400 kV lines that route power northwards, underscoring the transmission imperative.

In the north, Sidi Daoud’s 53.6 MW wind farm achieves capacity factors exceeding 25% and supplies power directly into the Tunis bulk supply point; however, terrain limitations curb further expansion. Offshore wind prospects in the Gulf of Hammamet remain exploratory, pending bathymetry studies and clarity on offtake. Central zones, such as Kairouan and Kasserine, are emerging as second-tier solar hubs. China Energy Engineering Group began constructing a 100 MW plant in Kairouan in 2024, highlighting the spread of investment beyond the traditional southern regions.

Coastal governorates face chronic grid congestion, where load density is highest. Smart-grid automation and reactive-power compensation will relieve some pressure, but physical reinforcement of east-west corridors is indispensable. The 600 MW ELMED interconnector, which lands at Cap Bon on the northeast coast, will create new nodal pricing dynamics once exports commence. Interior agricultural areas are testing agrivoltaic arrays that reduce irrigation demand and align with rural development goals.

Competitive Landscape

International developers anchor the Tunisia renewable energy market, yet must partner with domestic firms for permitting, land aggregation, and grid-access negotiations. Scatec collaborates with the Toyota Tsusho Group on a 100 MW project across Sidi Bouzid and Tozeur, pooling EPC skill sets with Japanese supplier credit. TotalEnergies partnered with VERBUND in the H₂ Notos project, which combines onshore wind, CSP, and desalination to feed electrolyzers, illustrating the convergence of electric and hydrogen value chains.

Chinese EPC groups leverage cost efficiency and state-bank backing to compete aggressively in auctions; the 100 MW Kairouan plant led by China Energy Engineering secured a PPA at USD 0.039/kWh, setting a market benchmark. European B-O-O specialists such as Voltalia and Qair differentiate through bankable long-term O&M records and structured finance from DFIs. Domestic integrators focus on C&I rooftops, where local content exceeds 35% in mounting systems and switchgear.

Competition now centers on hybrid plant design and readiness for ancillary services, rather than the lowest generation tariff alone. Developers offering co-located storage or synchronous condensers fetch higher evaluation points in recent tenders. Service niches are forming around asset-performance analytics and cyber-secure SCADA, areas where Tunisian tech start-ups partner with foreign OEMs.

Tunisia Renewable Energy Industry Leaders

Société Tunisienne de l’Électricité et du Gaz (STEG)

Eni SpA

Scatec ASA

TotalEnergies SE

Nur Energie Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Qair secured a 298 MW solar PPA with STEG, the largest single renewable contract to date, extending 30 years at a record tariff.

- March 2025: The Ministry of Energy shortlisted four firms for 500 MW of solar capacity under the 2025 tender round.

- February 2025: ENI committed EUR 24 billion to North African energy projects, placing Tunisia among its priority renewable energy targets.

- December 2024: Two tenders, totaling 1,700 MW, were approved, promising an annual output of 1,000 GWh and USD 125 million in gas savings.

Tunisia Renewable Energy Market Report Scope

Renewable energy is the energy collected from renewable resources, such as sunlight, wind, water movement, and geothermal heat, which are naturally replenished.

The Tunisia renewable energy market report includes:

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large is the Tunisia Renewable Energy Market today?

Installed capacity stood at 1.62 GW in 2026 and is projected to reach 5.02 GW by 2031 at a 25.42% CAGR.

Which technology leads current deployment?

Solar energy accounts for 70.62% of capacity, thanks to favorable irradiance and low auction tariffs.

What role will wind play by 2031?

Onshore wind is expected to grow at 34.76% CAGR, lifting its share to almost one-third of national renewables.

How is Tunisia financing new capacity?

Multilateral support from the World Bank, EBRD, and MIGA lowers risk, while auctions attract private IPPs with 20-25 year PPAs.

Will Tunisia export green hydrogen?

Memoranda with ACWA Power and TotalEnergies envision up to 600,000 t / yr before 2031, subject to pipeline completion and desalinated water availability.

What is the main barrier to faster growth?

STEG's debt burden and resulting grid deferrals increase financing costs and slow project connection timelines.

Page last updated on: