Market Trends of Thin Wafer Processing and Dicing Equipment Industry

This section covers the major market trends shaping the Thin Wafer Processing & Dicing Equipment Market according to our research experts:

Increasing Need for Miniaturization of Semiconductors to Drive the Market

- Due to increasing demand for compact electronic devices in segments such as consumer electronics, healthcare, and automotive, semiconductor IC manufacturers are forced to reduce the size of ICs. It has, therefore, given rise to miniaturization in the market, which is expected to experience a surge in its demand during the forecast period.

- Across geographies, the fabless business model is the major contributor to the prominent position of various Asian countries in semiconductor sales across the world. Fabless firms typically outsource fabrication to pure-play foundries and outsourced assembly and test (OSAT) firms. According to the report published by the Semiconductor Industry Association (SIA), in 2021, the dominance of the United States has decreased severely from 1990 and accounted for only 12% of the semiconductor manufacturing capacity. The rise of East Asia, especially China, is credited to various incentives and subsidies offered by the governments of various countries.

- According to Fujifilm, the miniaturization of semiconductor devices continues as the increasing use of AI, IoT, next-generation communication standard '5G', and the advancement of autonomous driving technology are expected to increase further demand and performance boost for semiconductors. The factors mentioned above have led to the rise in demand for small and lightweight consumer devices that rely on 3D circuit architecture built onto ultra-thin silicon wafers in order to perform at peak capacity.

- These wafers are extremely thin and flat. At the same time, miniaturization has resulted in the need to integrate several features on a single chip. Due to the large-sized wafers (with a diameter of up to 12 inches), there is a new trend in wafer technology.

- In May 2021, with the invention of the first chip using 2 nanometers (nm) nanosheet technology, IBM announced a breakthrough in semiconductor design and process. Semiconductors are used in a wide range of applications, including computers, appliances, communication devices, transportation systems, and critical infrastructure. Chip performance and energy efficiency are in high demand, particularly in the age of hybrid cloud, AI, and the Internet of Things. IBM's innovative 2 nm chip technology contributes to advancing the semiconductor industry's state-of-the-art, answering this expanding demand. It's expected to deliver 45% better performance and 75% lower energy consumption than today's most advanced 7 nm node chips.

Understand The Key Trends Shaping This Market

Download Sample

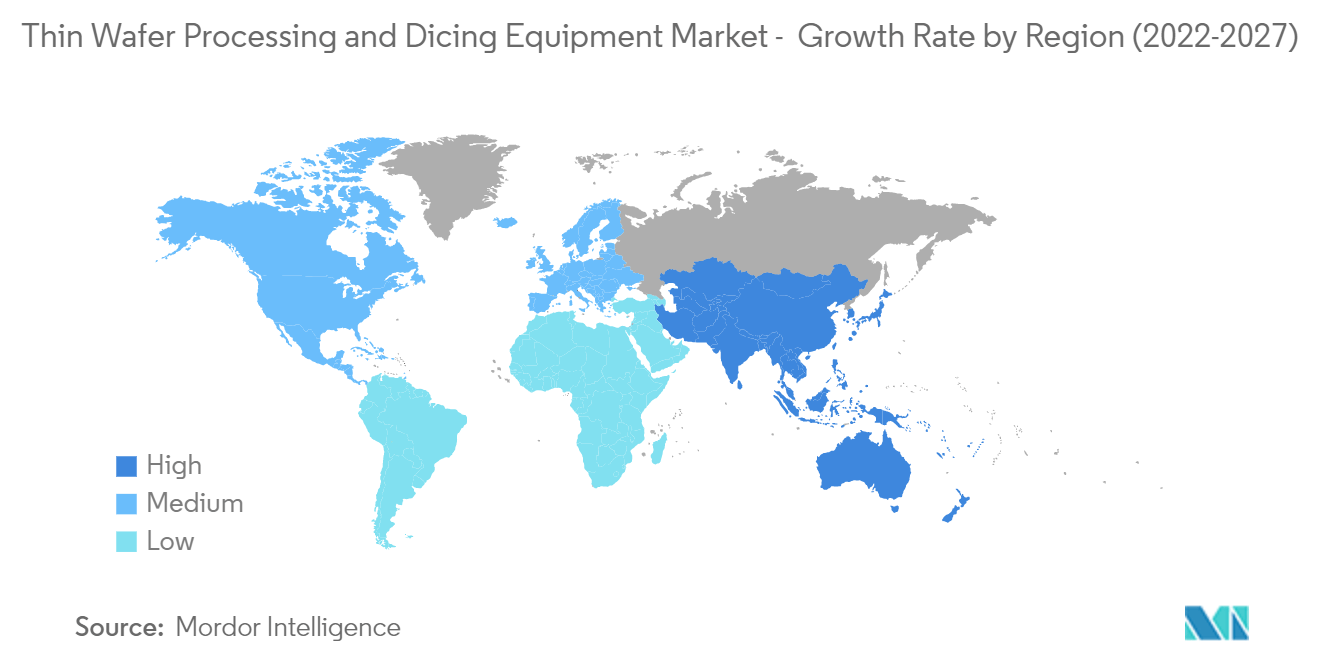

Asia Pacific to Hold the Largest Market Share

- The Asia Pacific is the largest and fastest-growing semiconductor market in the world. Significant demand for smartphones and other consumer electronics devices from countries such as China, the Republic of Korea, and Singapore, are encouraging many vendors to set up production establishments in the region.

- China's various players in the market are focusing on expanding business through acquisitions and mergers. For instance, in August 2021, Wingtech acquired Newport Wafer Fab for around EUR 63 million through a Dutch subsidiary called Nexperia. The deal was announced in July, confirming the terms of the agreement, according to a Wingtech statement filed with the Shanghai Stock Exchange. Wingtech is a listed manufacturer that assembles smartphones and other home appliances.

- Japan occupies an essential position in the semiconductor industry as it is home to several major manufacturers and the electronics industry. The government is expected to begin an investigation to assess the potential for bringing major chip makers into the country. Meanwhile, Japan-based organizations are considered the significant suppliers of most of the critical materials consumed in semiconductor manufacturing and packaging. For Japanese-based suppliers, Japanese exchange rates and high production costs make materials more expensive and open up opportunities for other suppliers for low-end applications.

- In Australia, the growing electronics manufacturing sector and the increasing adoption of advanced devices among various end-user industries are influencing the market growth. The sales of televisions and smartphones have primarily driven the growth in consumer electronics.

- In October 2021, in Australia, India, the United States, and Japan, the Quad Alliance also launched a semiconductor supply chain initiative aimed at capacity mapping, vulnerability identification, and enhanced supply chain security for semiconductors and their critical components. Together with NSW's Semiconductor Sector Service Bureau, these are the proper steps to establish Australia as a player in the Asia Pacific region and secure its position in the global semiconductor supply chain.

- Currently, India's semiconductor demand is majorly met by imports. Therefore, it was necessary to incentivize the value chain to make India economically independent and technologically leading. The government envisioned a comprehensive program in December 2021 to develop India's semiconductor and display manufacturing ecosystem with a budget of over INR 76,000 crores. Financial support efforts under the new program amounted to INR 230,000, covering the entire electrical device supply chain and more.

- The growth trajectory of fully-autonomous automobiles is heavily influenced by factors in Asia-Pacific, including technology advancements, consumer willingness to accept fully-automated vehicles, pricing, and suppliers' and OEMs' capacity to address significant concerns about vehicles safety. According to these factors, the automotive and semiconductor industries are always concentrating on enhancing technologies, negotiating raw material prices, and finally combining cars with reliable technology.

Get Analysis on Important Geographic Markets

Download Sample