Starter Fertilizer Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 8.20 Billion |

| Market Size (2030) | USD 11.90 Billion |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

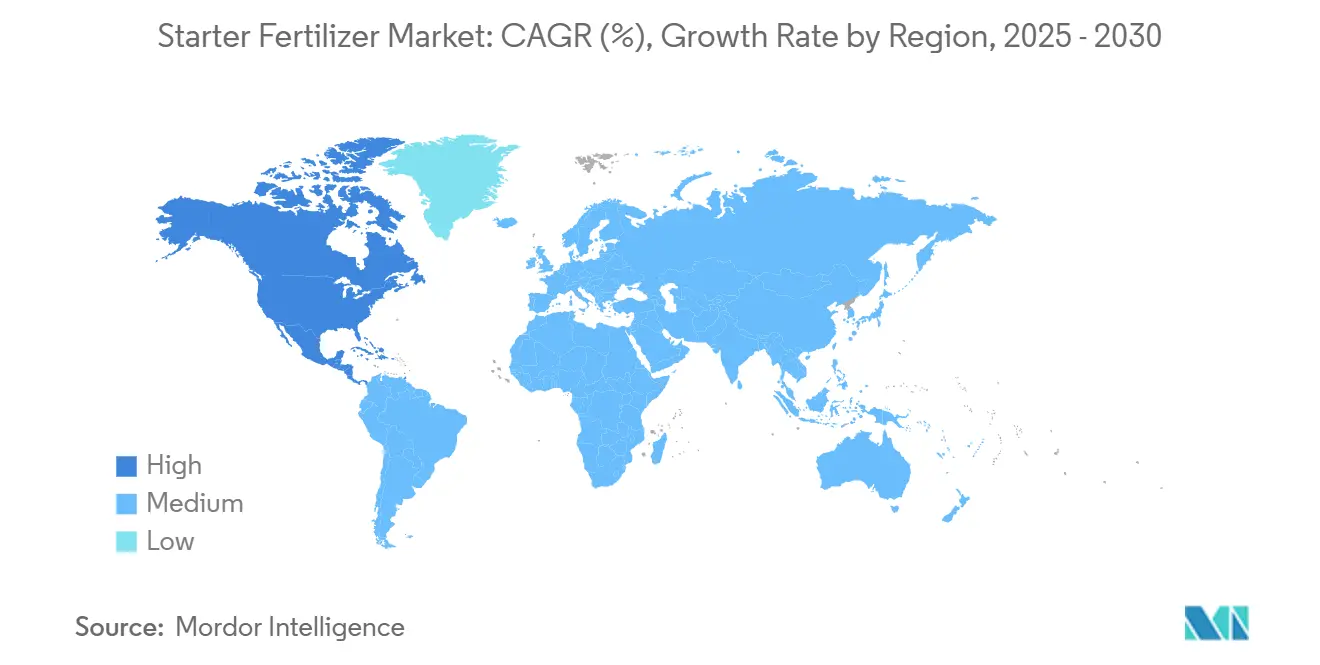

| Fastest Growing Market | Africa |

| Largest Market | North America |

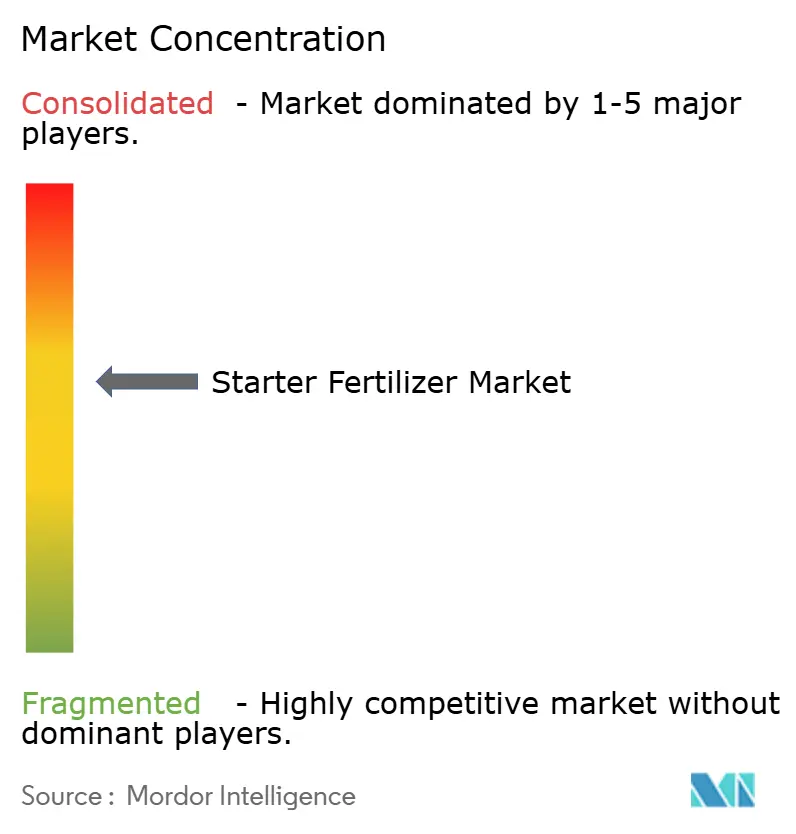

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Starter Fertilizer Market Analysis by Mordor Intelligence

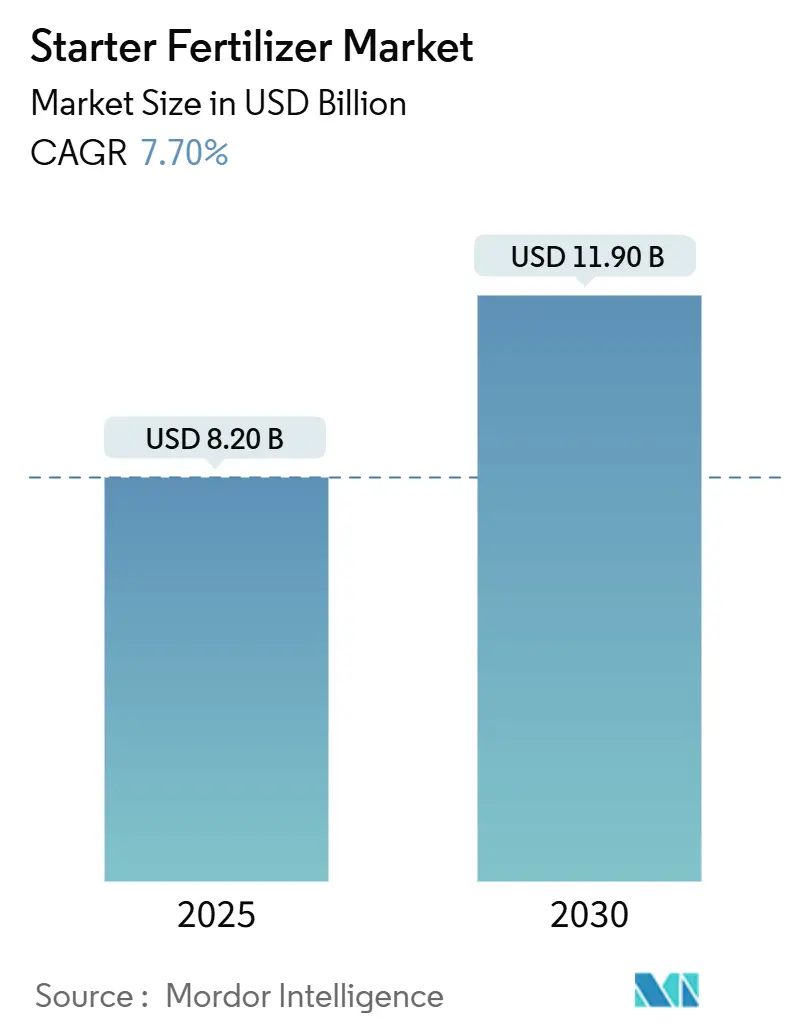

The starter fertilizer market size is valued at USD 8.2 billion in 2025 and is projected to increase to USD 11.9 billion by 2030, advancing at a 7.7% CAGR. The persistent adoption of precision planting technologies, the wider use of conservation agriculture, and the expansion of crop acreage in emerging regions underpin this growth. Liquid formulations dominate because they flow cleanly through high-speed planters, while micro-granulated and micronutrient-enriched products are outpacing the overall starter fertilizer market due to their placement accuracy and higher nutrient-use efficiency. North America remains the largest regional contributor, but Africa delivers the fastest growth as fertilizer-access programs expand.

Key Report Takeaways

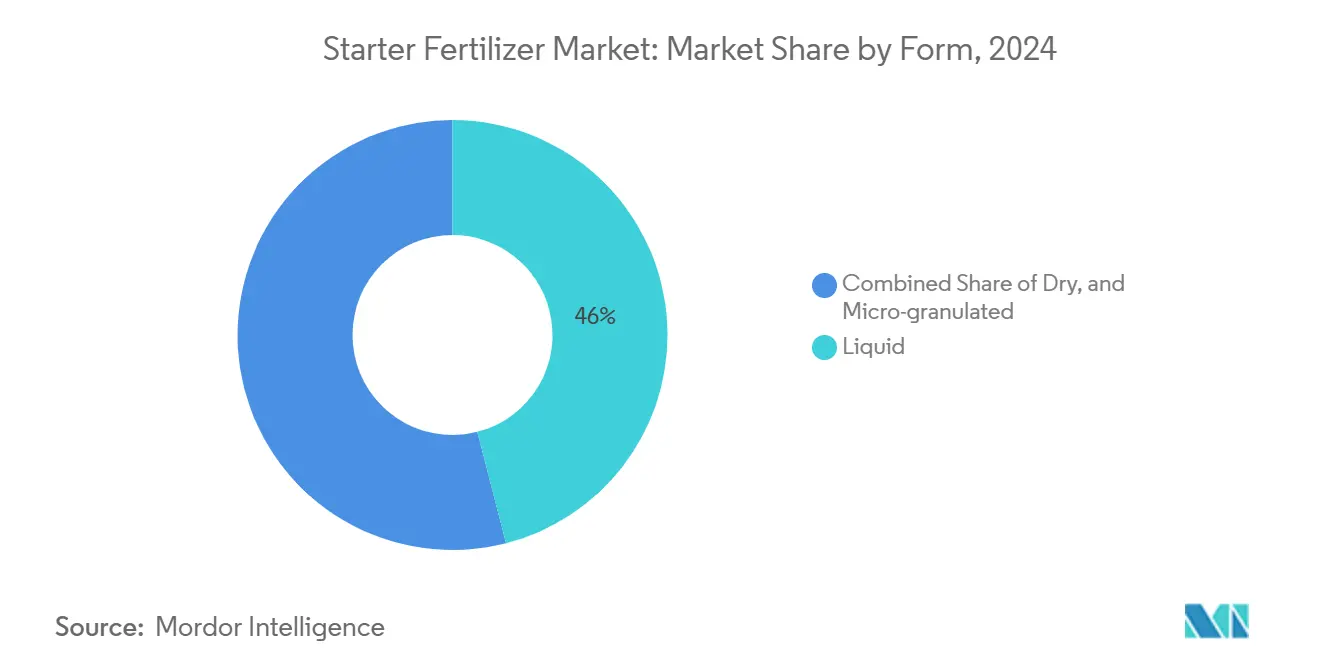

- By form, liquid products held 46% of the starter fertilizer market share in 2024, while micro-granulated grades are set to expand at a 10.4% CAGR through 2030.

- By nutrient composition, phosphorus-dominant 10-34-0 led with a 38% revenue share in 2024, while micronutrient-enriched blends are forecasted to grow at a 11.8% CAGR to 2030.

- By crop type, corn accounted for 52% of the starter fertilizer market size in 2024, while oilseeds and pulses are projected to grow at a 9.2% CAGR between 2025 and 2030.

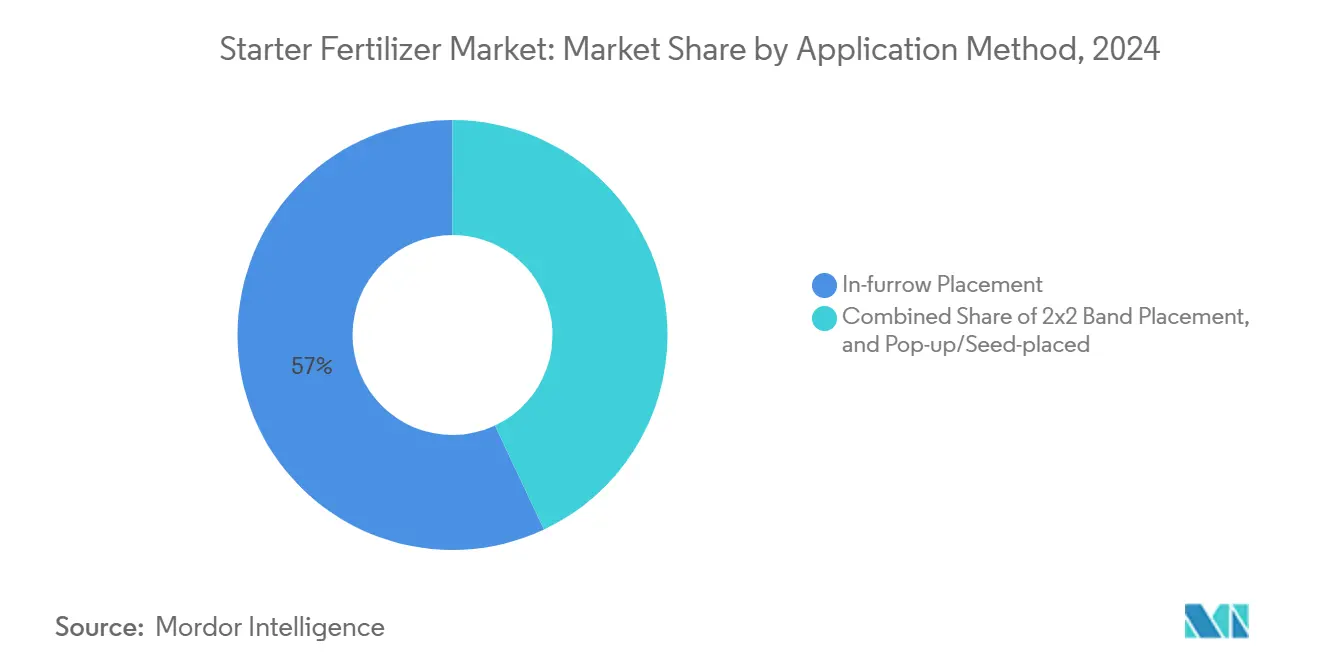

- By application method, in-furrow placement accounted for 57% of 2024 demand, while 2x2 banding is poised for a 12.5% CAGR through 2030.

- By region, North America held the largest market share at 32.0%, while Africa is the fastest-growing geography, with a 9.6% CAGR (2025-2030).

Global Starter Fertilizer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision Planting Adoption Raises Early-Season Nutrient Demand | +2.1% | North America, Europe, and expanding globally | Medium term (2–4 years) |

| No-Till and Cold-Soil Acreage Expansion | +1.8% | North America, South America, and Europe | Long term (≥4 years) |

| Maize and Soybean Feedstock Growth | +1.5% | North America and Asia-Pacific | Medium term (2–4 years) |

| Micro-Granulated and Seed-Coating Innovations | +1.2% | Developed markets worldwide | Short term (≤2 years) |

| Phosphate Price Volatility Favors Low-Rate Starters | +0.9% | Import-dependent regions worldwide | Short term (≤2 years) |

| Carbon-Footprint Incentives for Low-Salt Fertilizers | +0.8% | Europe, North America, and Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Precision Planting Adoption Raises Early-Season Nutrient Demand

High-speed, GPS-guided planters, such as John Deere’s ExactShot, place nutrients precisely on the seed, cutting fertilizer use by up to 66% while amplifying early-season uptake. The rapid spread of variable-rate application systems is therefore expanding the starter fertilizer market as growers need seed-safe, low-salt liquids compatible with precision hardware. Demand is strongest in the North American corn and soybean belts, but European sugar beet and cereal producers are close followers. Fertilizer suppliers are responding with low-viscosity formulations that maintain flow at high planting speeds and meet seed safety standards, thereby advancing the development and uptake of starter fertilizers across major global markets.

No-Till and Cold-Soil Acreage Expansion

Conservation farming reduces soil disturbance while cooling the seedbed, thereby delaying nutrient mineralization. In these systems, phosphorus-rich starters boost corn yields by up to 11 bushels per acre in northern zones [1]USDA, “No-Till Yield Responses to Phosphorus Starters,” usda.gov. No-till farming is entrenched on 32 million hectares in Brazil and is gaining traction in Europe under carbon-credit incentives. Starter fertilizer demand, therefore, rises in tandem with the acreage shift, especially for liquids that flow in cool spring weather and micro-granules that deliver nutrients in a tight soil band.

Maize and Soybean Feedstock Growth

With projected corn acreage reaching 95.3 million acres in the U.S. and soybean output anticipated to hit 166.3 million tons by 2025 in Brazil, starter fertilizer demand is set to rise accordingly [2]USDA, "US Farmers Expect to Plant More Corn and Less Soybean Acres," usda.gov. Both crops exhibit reliable yield gains from early applications of phosphorus and zinc, thereby directly increasing starter fertilizer market demand through acreage expansion. South America shows increased adoption of integrated nutrient solutions that combine chemical and biological starter packages. These solutions combine nitrogen-fixing inoculants with N-P-K formulations in a single-pass application. Precision planting technologies enable the targeted application of starter fertilizers, making these solutions vital in modern farming systems.

Micro-Granulated and Seed-Coating Innovations

Micro-granules, sized 0.5–2 mm, disperse evenly along the row and release nutrients over a longer window, thereby improving phosphorus availability in alkaline soils. Seed-coating polymers now contain zinc, iron, or manganese and meter release by temperature, promoting micronutrient-enriched starters to achieve double-digit growth. Nanotechnology research has shown a 34% increase in wheat yield with zinc-oxide-coated urea, reinforcing the trend. Innovations in micronutrient-enriched starter fertilizers, particularly those utilizing nanotechnology such as zinc-oxide-coated urea, are driving double-digit growth rates and have shown notable improvements in wheat yield.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Raw-Material Cost Pressure | −2.3% | Global, strongest in import-dependent regions | Short term (≤2 years) |

| Equipment Compatibility Gaps for Smallholders | −1.1% | Africa, Asia-Pacific, and parts of South America | Medium term (2–4 years) |

| Salt-Load Scrutiny Near the Seed Zone | −0.8% | Europe, North America, and spreading globally | Long term (≥4 years) |

| Biological Inoculant Cannibalization | −0.6% | South America first, and spreading globally | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material Cost Pressure

Nitrogen production relies on natural gas, at USD 2.80 per MMBtu, ammonia costs roughly USD 140 per metric ton. Price spikes in 2024-2025 lifted urea and MAP sharply, squeezing starter fertilizer margins. Phosphate supply remains concentrated in Morocco, China, and the United States, so disruptions to freight or geopolitics ripple through global pricing. These dynamics restrain discretionary upgrades to premium starter products despite clear agronomic paybacks.

Salt-Load Scrutiny Near the Seed Zone

Regulators impose maximum metal and salt levels to protect germination. California’s fertilizer code caps arsenic, cadmium, and lead, while industry guidelines warn against seed-placed potash because of a 116 salt index[3]California Department of Food and Agriculture, “Fertilizer Metal Limits,” cdfa.ca.gov. The regulations compel manufacturers to adopt lower-salt alternatives, particularly potassium phosphates. This transition increases production costs and formulation complexity, limiting the growth of the starter fertilizer market.

Segment Analysis

By Form: Liquid Dominance Drives Application Precision

Liquid products held 46% of the starter fertilizer market share in 2024, and remain the backbone of the starter fertilizer market because they integrate seamlessly with high-speed planters. A liquid starter fertilizer is usually composed of two or more nutrients. Under most situations, a combination of nitrogen and phosphorus constitutes an effective starter material. Dry granular blends kept a moderate share where bulk handling infrastructure is mature. Growing interest in sustainability also favors liquids: Lower rates reduce freight costs, and sealed totes minimize dust exposure.

Micro-granules, with only a limited share now, are the fastest-growing, increasing at a 10.4% CAGR through 2030, as they spread nutrients uniformly even at low rates. The starter fertilizer market size linked to liquids is projected to rise, reflecting both acreage expansion and premium pricing. Meanwhile, micro-granules attract horticultural and high-value field crops, where every kilogram of applied phosphorus must be translated into yield. Suppliers invest in specialized prilling and coating lines, indicating that micro-granules will capture an incremental share of the starter fertilizer market after 2027.

Note: Segment shares of all individual segments available upon report purchase

By Nutrient Composition: Phosphorus-Dominant Formulations Lead Market

Phosphorus-rich 10-34-0 aled with a 38% revenue share in 2024, as crops demand immediate phosphorus at germination. Balanced N-P-K held a significant share, fitting regions with multiple soil deficiencies. Phosphorus-focused blends remain popular because they stimulate early root establishment, a crucial step for uniform plant emergence. Increasing soil nutrient depletion is prompting growers to shift toward multi-nutrient starter solutions instead of single-nutrient formulations. Increasing soil nutrient depletion is prompting growers to shift toward multi-nutrient starter solutions instead of single-nutrient formulations

Micronutrient-enriched starters are projected to post an 11.8% CAGR through 2030, as intensive systems reveal hidden zinc and manganese gaps. Chelated zinc and iron additives avoid soil fixation, boosting early vigor in corn and small grains. Seed-coating routes further accelerate micronutrient uptake, shortening the payback period for growers and lifting adoption. Micronutrient-enhanced fertilizers are gaining traction as farmers adopt precision agriculture, which highlights hidden micronutrient deficiencies. The move toward chelated micronutrients reflects a broader trend toward higher nutrient-use efficiency and reduced environmental loss.

By Crop Type: Corn Applications Dominate Usage Patterns

Corn accounted for 52% of the starter fertilizer market size in 2024 due to its sensitivity to cold soils and rapid early growth. Soybean followed a significant share, although its salt sensitivity restricts seed-placed rates. Wheat and other cereals accounted for a significant share, while vegetables, fruits, and other specialty crops made up the balance. Rising oilseed and pulse production will increase their share, driving the starter fertilizer market to diversify beyond corn. Corn’s dominance in the segment is also driven by farmers’ focus on maximizing early-season growth to protect final yield potential.

Oilseeds and pulses are projected to grow at a 9.2% CAGR through 2030, aided by the adoption of microbial co-packaging and premium prices for sustainable supply chains. High-value horticulture utilizes smaller tonnage but commands premium unit prices, significantly contributing to revenue. The adoption of microbially enriched starters is expanding because many crops now target regenerative agriculture practices, raising demand for biologically active inputs. The adoption of microbially enriched starters is expanding because many crops now target regenerative agriculture practices, raising demand for biologically active inputs.

By Application Method: In-Furrow Placement Maintains Leadership

In-furrow placement accounted for 57% of 2024 demand by putting nutrients directly with the seed, maximizing early uptake. Precision hardware upgrades are crucial, and OEMs nowadays integrate fertilizer coulters with down-force sensors, giving growers confidence to apply bands even in rocky soils. This hardware trend reinforces 2x2 growth inside the starter fertilizer market. In-furrow systems support uniform emergence, especially in fields with variable soil temperatures, helping growers reduce early-season stand variability.

2x2 banding is poised for a 12.5% CAGR through 2030, as it allows higher rates without salt injury. Pop-up placements accounted for 8%, limited by equipment constraints and salt risks. 2x2 placement appeals to high-yield programs, as it enables growers to apply complementary products, such as biologicals and slow-release nitrogen, alongside starters. The rising interest in low-salt, high-purity formulations makes pop-up applications more viable for specialty crops, despite ongoing equipment limitations.

Geography Analysis

North America generated the largest share at 32.0% in 2024, supported by vast corn and soybean acreage, sophisticated retail networks, and the early embrace of precision technologies. Regional demand is projected to expand as growers integrate low-carbon fertilizers that qualify for incentives in the ethanol and grain supply chains. The adoption of starter fertilizers is high due to advanced precision planting systems, which enable accurate in-furrow and 2x2 applications. Corn and soybean growers prioritize starters to enhance early-season vigor, especially in cold soil zones across the Midwest.

Africa is the fastest-growing region, with a 9.6% CAGR through 2030, driven by donor-backed fertilizer access programs and mechanization services for smallholders. Micro-dosing techniques, coupled with low-rate liquids, align with the continent’s resource constraints and enhance input-output efficiency. Governments and NGOs support the use of these practices through subsidy programs and soil fertility initiatives, especially in East and Southern Africa. The Asia-Pacific region follows with a significant share, led by China and India’s push for balanced nutrient management in rice and wheat systems to mitigate environmental impacts.

South America holds the second-largest position, driven by the expansion of Brazilian soybeans and corn. Brazil’s 2024-2025 soybean harvest was 166.3 million tons, sustaining a strong demand for phosphorus-based starters and microbial blends. Argentine adoption is slower due to macroeconomic volatility, yet the country’s technological know-how underpins the continued uptake of liquid starters among export-oriented growers. Rising commercial farming in the region increases demand for high-efficiency, precision-applied starters that reduce nutrient losses.

Competitive Landscape

The top five suppliers, Nutrien Ltd., Yara International ASA, The Mosaic Company, ICL Group Ltd, and Marubeni Corporation, accounted for 41.9% of 2024 revenue, indicating moderate market concentration. Koch strengthened its Midwestern presence in 2024 through the acquisition of the USD 3.6 billion Wever plant, which added 3.5 million metric tons of nitrogen capacity. Nutrien is expanding its South American presence through the pending Casa do Adubo acquisition, which will add 39 retail outlets and approximately USD 400 million in annual sales.

Strategic pivots favor sustainability. CF Industries and POET are piloting low-carbon ammonia fertilizers aimed at cutting ethanol emissions by 10%. ICL introduced soybean inoculants after acquiring Nitro 1000, signaling a shift toward integrated chemical-biological solutions. Haifa Group is investing USD 350 million to double its specialty fertilizer capacity, focusing on premium micro-granules and controlled-release products that meet precision-placement needs.

New entrants are focusing on seed-coating polymers and nanotechnology to carve out niches in micronutrient delivery. Because intellectual property barriers are lower than in bulk nitrogen, multiple regional players can emerge, keeping the starter fertilizer market competitive.

Starter Fertilizer Industry Leaders

-

Nutrien Ltd.

-

Yara International ASA

-

The Mosaic Company

-

ICL Group Ltd

-

Marubeni Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Grupa Azoty S.A. expanded its multinutrient fertilizer portfolio by introducing MultiCorn NP (Nitrogen-Phosphorus) (S) 14-34 (+23) with zinc enrichment. The fertilizer, produced by Grupa Azoty Police, is specifically formulated for maize cultivation. Maize plants face challenges during early growth stages due to limited nutrient availability and underdeveloped root systems. MultiCorn's balanced composition provides immediate access to nitrogen, phosphorus, and zinc, supporting optimal plant development during this starting phase.

- March 2024: Eurochem Group AG inaugurated a phosphate fertilizer production facility in Serra do Salitre, Minas Gerais. The USD 1 billion investment comprises an open-pit phosphate mine with reserves exceeding 350 million metric tons, as well as a manufacturing plant. This development ensures a stable, long-term phosphate supply, a crucial nutrient for starter fertilizers, enabling the company to optimize production efficiency.

- February 2024: The Mosaic Company's Esterhazy mine in Saskatchewan is implementing a HydroFloat expansion project at its K2 mill to increase potash production by 400,000 metric tons per year. The company aims to increase its phosphate production from 6.4 million metric tons in 2024 to 7.4-7.6 million metric tons in 2025. This expansion will increase the availability of phosphorus, a key raw material used in starter fertilizers and other phosphate-based blends.

Global Starter Fertilizer Market Report Scope

Starter fertilizer is a small amount of fertilizer applied at planting time, placed near the seed to provide essential nutrients for a plant's early growth and development. The Starter Fertilizer Market Report is Segmented by Form (Liquid, Dry, and More), by Nutrient Composition (Nitrogen-Phosphorus-Potassium (Balanced) and More), by Crop Type (Cereals and Grains, and More), by Application Method (In-Furrow Placement, and More), and by Region (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Liquid |

| Dry |

| Micro-granulated |

| Nitrogen-Phosphorus-Potassium (Balanced) |

| Phosphorus-Dominant (10-34-0, 11-52-0, etc.) |

| Micronutrient-Enriched |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| In-furrow Placement |

| 2x2 Band Placement |

| Pop-up/Seed-placed |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Form | Liquid | |

| Dry | ||

| Micro-granulated | ||

| By Nutrient Composition | Nitrogen-Phosphorus-Potassium (Balanced) | |

| Phosphorus-Dominant (10-34-0, 11-52-0, etc.) | ||

| Micronutrient-Enriched | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| By Application Method | In-furrow Placement | |

| 2x2 Band Placement | ||

| Pop-up/Seed-placed | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the starter fertilizer market ?

The starter fertilizer market size stands at USD 8.2 billion in 2025 and is forecast to reach USD 11.9 billion by 2030.

Which formulation type leads the market?

Liquid starters lead with 46% share in 2024, mainly because they integrate smoothly with high-speed precision planters.

Why are micro-granulated starters growing so quickly?

Micro-granules distribute nutrients evenly at low rates, improving efficiency and driving a 10.4% CAGR through 2030 .

Which region is expanding fastest?

Africa posts the highest regional growth at 9.6% CAGR, supported by fertilizer-access programs and smallholder mechanization.

Which crop consumes the most starter fertilizer ?

Corn accounts for 52% of global usage due to its high early-season nutrient demand and responsiveness.