Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

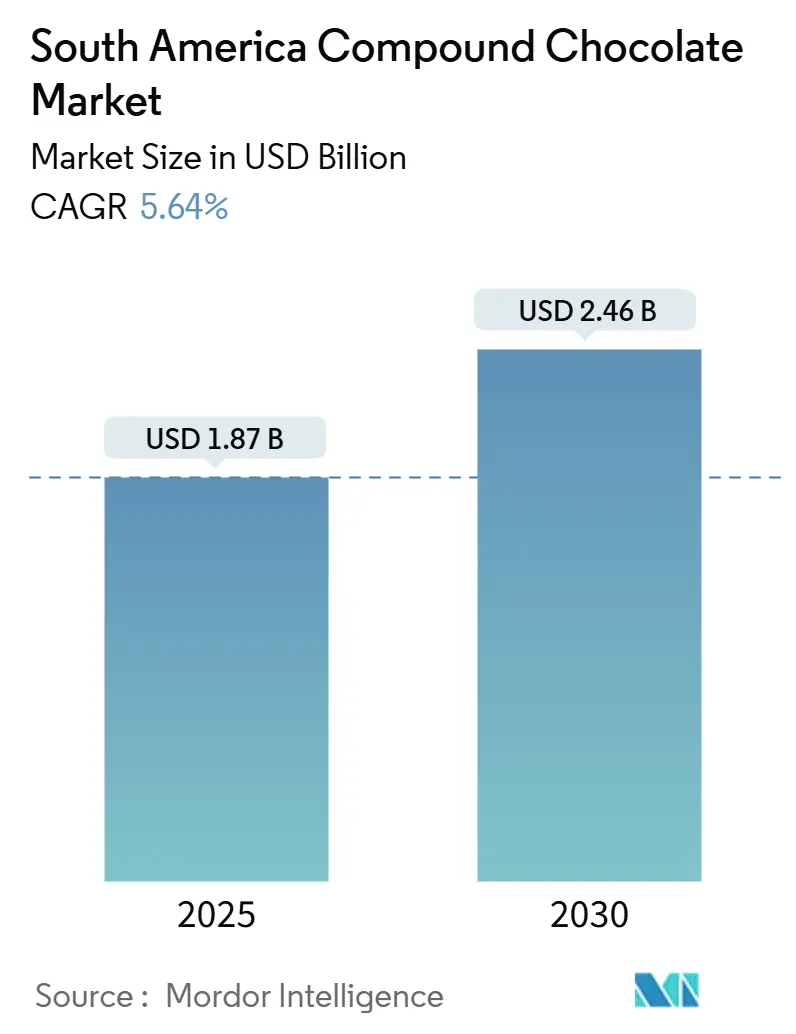

| Market Size (2025) | USD 1.87 Billion |

| Market Size (2030) | USD 2.46 Billion |

| Growth Rate (2025 - 2030) | 5.64% CAGR |

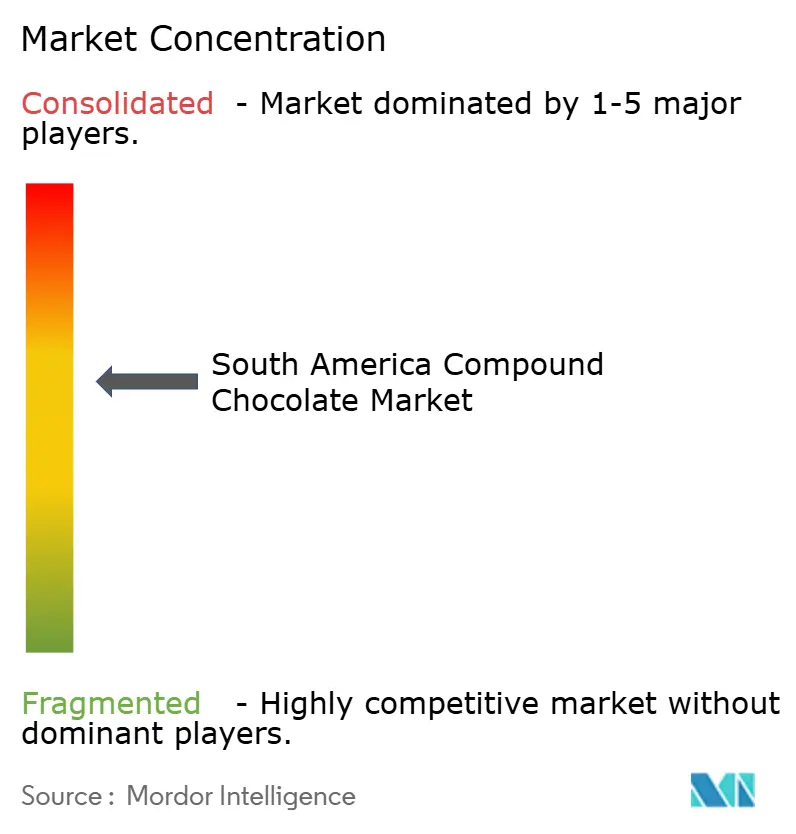

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Compound Chocolate Market Analysis by Mordor Intelligence

The South America compound chocolate market is projected to grow from USD 1.87 billion in 2025 to USD 2.46 billion by 2030, registering a compound annual growth rate (CAGR) of 5.64% during the forecast period. This growth is primarily driven by the unique advantages of compound chocolate, such as its ability to mimic the taste of traditional chocolate, ease of processing, and excellent heat resistance. These features make it particularly suitable for use in warm climates, as it reduces the need for refrigeration, benefiting bakeries, confectioners, and ice cream manufacturers. The increasing demand for convenient, on-the-go snack options, the expansion of dessert offerings in the hospitality and foodservice (HoReCa) sector, and the introduction of innovative flavors inspired by Amazonian fruits are attracting a broader customer base. By product type, dark compound chocolate is gaining popularity due to its perceived health benefits. In terms of form, fillings and spreads are seeing high demand, especially from artisan bakeries. For the ice cream segment, applications are capitalizing on consistent, year-round consumption trends. The market is moderately consolidated, with a mix of established players and emerging competitors driving innovation and competition.

Key Report Takeaways

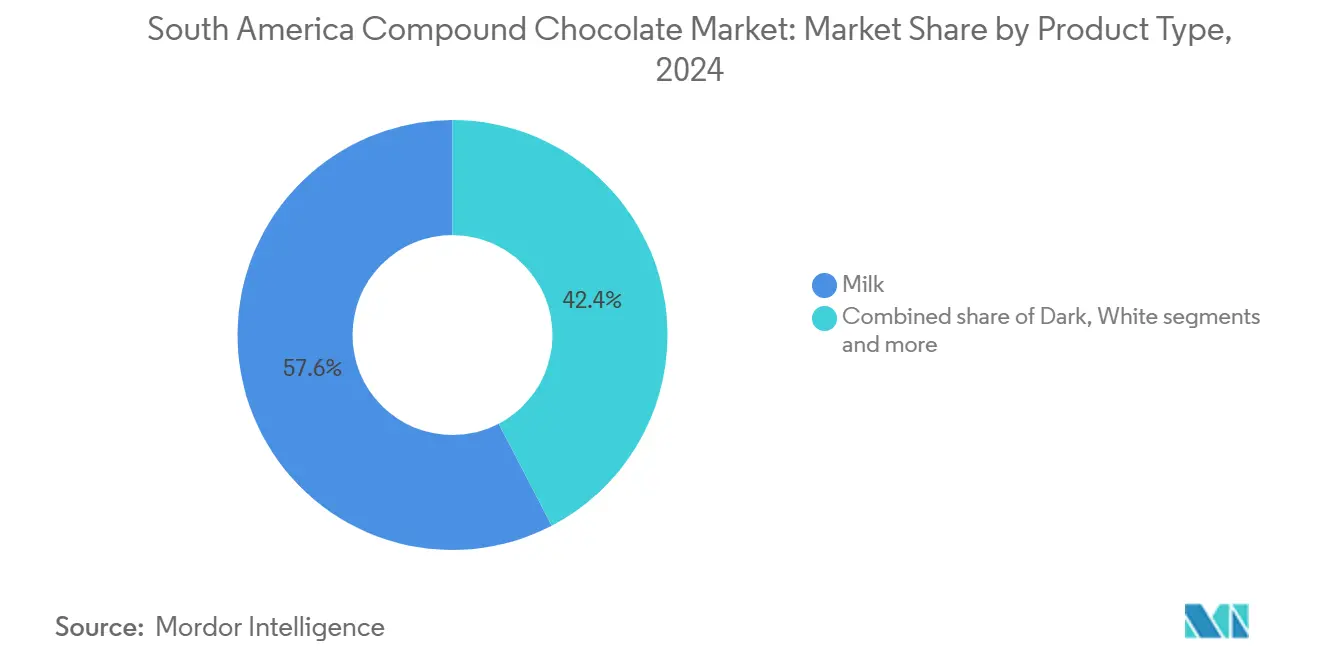

- By product type, milk varieties dominated the South American compound chocolate market with a 57.64% share in 2024, while dark variants are projected to rise at a 7.64% CAGR through 2030.

- By form, chips, drops, and chunks led with 45.28% revenue in 2024, and fillings and spreads are forecast to grow at a 6.34% CAGR to 2030.

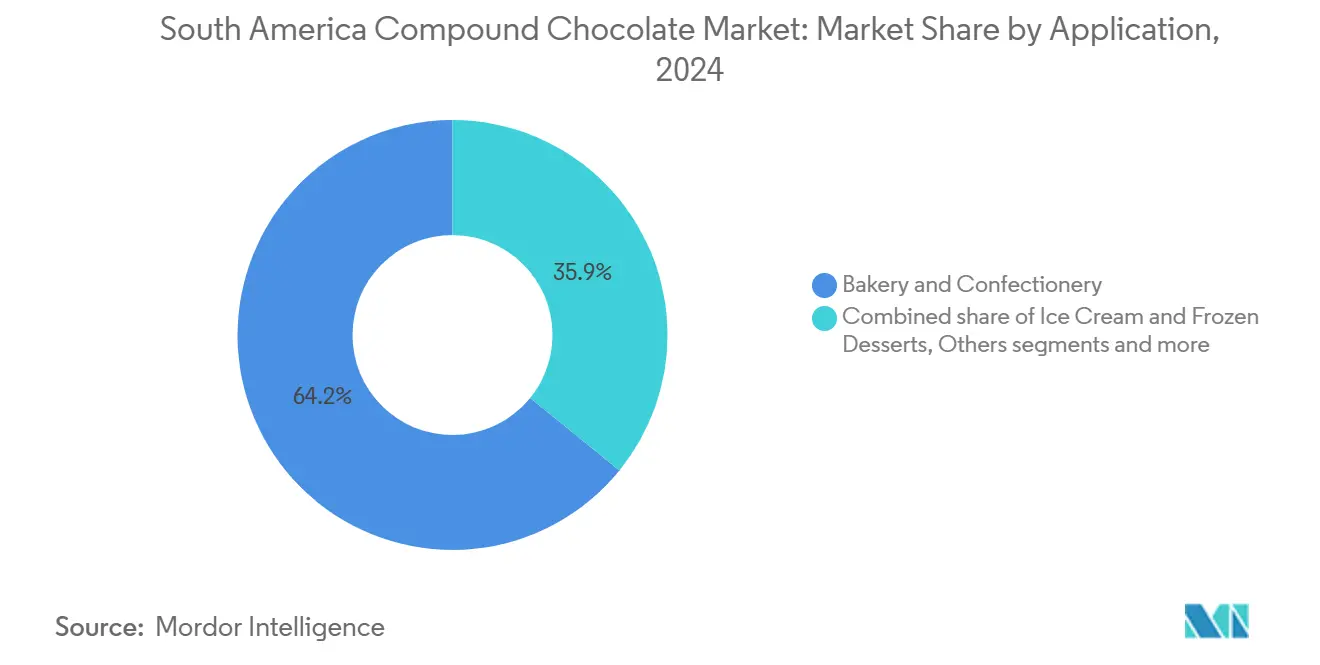

- By application, bakery and confectionery accounted for 64.15% of the 2024 demand, whereas ice cream and frozen desserts are advancing at a 7.11% CAGR over 2025-2030.

- By distribution channel, retail captured 47.84% of 2024 sales, while horeca is expanding at the fastest rate, with a 7.85% CAGR through 2030.

- By country, Brazil contributed 47.36% of the regional 2024 revenue, while Colombia is registering the fastest growth rate of 6.93% from 2024 to 2030.

South America Compound Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing use of compound chocolate in snack bars and cereal-based products | +1.2% | Brazil, Argentina, with spillover to Colombia and Chile | Medium term (2-4 years) |

| Product innovation in flavors, formats, and functional properties | +0.9% | Urban centers across Brazil, Chile, Colombia | Short term (≤ 2 years) |

| Growing production of coated nuts, seeds, and dried fruits | +0.8% | Brazil, Peru, Chile (export-oriented facilities) | Medium term (2-4 years) |

| Longer shelf life and better heat stability make compound chocolate suitable | +1.1% | All South American markets, especially tropical zones | Long term (≥ 4 years) |

| Rising demand for chocolate-flavored bakery mixes and premixes | +0.7% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Use of compound chocolate in seasonal and promotional confectionery | +0.6% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing use of compound chocolate in snack bars and cereal-based products

Snack-bar and cereal-based product manufacturers in South America are increasingly using compound chocolate because it simplifies production and performs well in high temperatures. Unlike regular chocolate, compound chocolate does not require tempering, which simplifies production and reduces costs. It also maintains its texture and quality even in storage and distribution environments where temperatures often exceed 30 °C. This feature is particularly beneficial for mid-sized producers in cities like São Paulo and Buenos Aires, as it enables them to operate without incurring the expense of investing in expensive climate-controlled facilities. Trade data highlights the importance of chocolate in processed foods. For example, Brazil imported USD 185 million worth of chocolate in 2024, making it one of the country’s most traded food products, according to the Observatory of Economic Complexity[1]Source: Observatory of Economic Complexity, "Chocolate in Brazil", oec.world. Furthermore, improved trade within the Mercosur region has facilitated the movement of cereal bars and chocolate-coated snacks.

Rising demand for chocolate-flavored bakery mixes and premixes

The use of chocolate-flavored bakery mixes and premixes is growing steadily across South America, driven by an improving cocoa supply in the region. This increase in cocoa availability is helping to boost the production of compound chocolate, a key ingredient in these mixes. Peru, in particular, is playing a significant role in this trend. The country’s cocoa production is expected to grow at an annual rate of around 7%, reaching approximately 250,000 tons by 2030, according to Coalición por una Producción Sostenible as of June 2023[2]Source: Coalición por una Producción Sostenible, "Cocoa, Forests and Diversity", produccionsostenible.org.pe. This consistent growth in cocoa output ensures a stable supply of raw materials for compound chocolate powders used in bakery premixes. These powders are valued for their ability to provide consistent color, flavor, and shelf life. As bakeries across the region face challenges such as labor shortages and rising costs, they are increasingly turning to premixes as a convenient solution. Premixes simplify the baking process, save time, and reduce the need for skilled labor, making them an attractive option for bakery businesses.

Growing production of coated nuts, seeds, and dried fruits

In Brazil, the growing availability of locally produced nuts is driving an increase in the production of compound-chocolate-coated snacks. Manufacturers are using compound chocolate as a coating because it helps extend the shelf life of these snacks, making them more suitable for export. According to the United States Department of Agriculture, as of May 2024, Brazil produces approximately 38,000 tons of nuts, 147,000 tons of cashews, 5,000 tons of pecans, and 1,100 tons of macadamia nuts annually[3]Source: United States Department of Agriculture, "Opportunities for Tree Nut Exports to Brazil", apps.fas.usda.gov. This abundant supply of nuts provides a strong foundation for creating coated nut and dried fruit products. Compound chocolate is particularly popular for these applications because it can withstand temperature changes, reduces the risk of fat bloom (a common quality issue in chocolate), and allows products to be shipped without the need for refrigeration. This reduces logistics costs and helps position these snacks as premium products in international markets.

Longer shelf life and better heat stability make compound chocolate suitable

Compound chocolate is gaining popularity in South America because it lasts longer and can withstand high temperatures, making it an ideal choice for the region's hot and humid climate, where refrigeration is often expensive or unavailable. Its ability to resist fat bloom means that retailers in cities like Manaus and Cartagena can display chocolate-coated products without needing refrigeration. This not only helps businesses save on energy costs but also enables them to utilize their shelf space more effectively for other products. For e-commerce businesses, this feature is particularly useful as it reduces the risk of chocolates melting or getting damaged during delivery, even in hot weather. In rural areas, where cold storage facilities are often limited or unavailable, compound chocolate provides a practical and reliable solution. It can be transported and stored without refrigeration, enabling businesses to expand their reach into remote regions while maintaining product quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to saturated fats and palm oil usage | -0.9% | Brazil, Chile, Argentina (urban health-conscious segments) | Medium term (2-4 years) |

| Negative consumer perception of compound chocolate as inferior to real chocolate | -0.7% | Premium segments in Brazil, Chile, urban Colombia | Long term (≥ 4 years) |

| Increasing consumer awareness of ingredient quality and cocoa content | -0.5% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Growing clean-label and natural ingredient demand conflicts | -0.6% | Brazil, Chile, Colombia (urban millennials and Gen Z) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns related to saturated fats and palm oil usage

Health-focused labeling regulations are becoming a challenge for the compound chocolate market in Brazil. According to PubMed Central, new Brazilian regulations will require a magnifying glass symbol to be displayed on the front of food packages starting in October 2025[4]Source: PubMed Central, "Brazilian Front-of-Package Nutrition Labeling: Consumer Perceptions on Social Media Platform X", pmc.ncbi.nlm.nih.gov. This symbol will highlight products with high levels of added sugar, saturated fat, or sodium. Many compound chocolate products, especially those made with vegetable fats that are high in saturated fat, are likely to be affected. These regulations aim to increase consumer awareness of the nutritional risks associated with such products. As a result, manufacturers are under pressure to reformulate their products to meet healthier standards, which could lead to higher production costs. If companies fail to adapt, they risk losing consumer trust, facing reduced demand, and struggling to secure shelf space in retail stores. This creates significant challenges for the growth of compound chocolate, particularly in price-sensitive market segments.

Negative consumer perception of compound chocolate as inferior to real chocolate

Negative consumer perception is a significant challenge for the compound chocolate market, as many consumers perceive it as of lower quality compared to genuine chocolate. According to Codex standards, compound chocolate does not meet the formal definition of chocolate, which further reinforces its image as an inferior product. This perception is particularly strong in countries like Brazil and Chile, where gift buyers often associate compound chocolate with being a cheaper or less thoughtful option. Despite its practical benefits, such as better heat resistance in warm climates and suitability for allergen-free formulations, these advantages are not widely recognized by consumers. Compound chocolate is often preferred by manufacturers for its cost-effectiveness and ease of use, especially in regions with high temperatures where real chocolate may melt easily. The lack of consumer awareness about these benefits makes it difficult for manufacturers to position compound chocolate as a viable alternative to real chocolate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Variants Gain Health-Halo Traction

Milk compound chocolate was the leading product in the South America compound chocolate market in 2024, accounting for 57.64% of the total demand. Its widespread use in bakery, confectionery, and snack items is due to its affordable cost, smooth texture, and appealing taste. Products like coated biscuits, wafers, cereal bars, and molded chocolates heavily depend on milk compound chocolate. Its ability to remain stable in warm storage conditions makes it a reliable choice for large-scale production. This strong demand highlights its role as a key ingredient in mainstream and cost-effective product categories across the region.

Dark compound chocolate is expected to grow at the fastest rate, with a projected CAGR of 7.64% from 2025 to 2030, as consumers increasingly prefer richer cocoa flavors and products with lower sugar content. Manufacturers are incorporating dark variants into items such as protein bars, coated nuts, and healthier snack options to meet the growing demand for premium and health-conscious products. Dark compound chocolate also aligns with clean-label trends and offers a high-cocoa perception without the price instability of real chocolate. These factors are driving its adoption in premium and functional snack categories, making it a significant growth area in the South American market.

By Form: Fillings and Spreads Capture Artisan Bakery Demand

In 2024, chips, drops, and chunks accounted for 45.28% of form-based revenue in South America’s compound chocolate market. These formats are popular in large-scale bakery and confectionery production because they are well-suited for use with automated systems. Their uniform size and consistent melting ensure even distribution in products like cookies, muffins, and cereal bars, which improves the overall quality of the final product. Their ability to support fast and efficient production with minimal adjustments makes them a preferred choice for manufacturers aiming to streamline operations and maintain consistency.

Fillings and spreads are projected to grow at a CAGR of 6.34% through 2030, driven by their increasing use in artisan, in-store, and small-scale bakeries. These products are ready to use, eliminating the need for tempering and reducing the dependency on skilled labor, which helps smaller businesses save time and costs. Their stable texture, long shelf life, and ease of application make them ideal for preparing fresh pastries, filled breads, and desserts. As demand for convenient and high-quality bakery solutions grows, these products are expected to see wider adoption across the region.

By Application: Ice Cream Segment Leverages Year-Round Consumption

In 2024, bakery and confectionery applications dominated the South America compound chocolate market, accounting for 64.15% of the total demand. Compound chocolate is widely used in products such as cookies, cakes, pastries, and molded confectionery due to its affordability and ease of use. Industrial bakeries particularly favor it for its compatibility with automated production lines, while retail bakeries appreciate its ability to maintain quality even in warm climates. These features make compound chocolate a key ingredient in a wide range of bakery and confectionery products, enabling manufacturers to efficiently meet consumer demand.

The ice cream and frozen dessert segment is projected to grow at a CAGR of 7.11% from 2025 to 2030. This growth is largely driven by the increasing use of compound chocolate coatings, which are specifically designed to withstand cracking during freeze-thaw cycles and ensure durability in warm weather conditions. These coatings are especially beneficial for smaller outlets and convenience stores that lack advanced cold-chain infrastructure. As frozen desserts and impulse-buy products gain popularity among consumers, the adoption of compound chocolate coatings in this segment is expected to increase steadily, supporting the market's overall growth in South America.

By Distribution Channel: HoReCa Professionalizes Dessert Preparation

In 2024, retail outlets such as supermarkets and convenience stores contributed to 47.84% of compound chocolate sales in South America. This dominance is largely due to the easy availability of these products on shelves and the growing consumer preference for convenient, ready-to-eat chocolate snacks. The heat stability and longer shelf life of compound chocolate allow retailers to store and display these products without requiring extensive refrigeration, making them ideal for impulse purchases. The consistent quality of compound chocolate helps reduce spoilage and product wastage, further solidifying retail outlets as the leading distribution channel in both urban and semi-urban areas.

The HoReCa (Hotels, Restaurants, and Cafés) segment is expected to grow at the fastest rate, with a projected CAGR of 7.85% through 2030. This growth is driven by the increasing adoption of compound chocolate by foodservice operators, who appreciate its ease of use and cost efficiency. Compound chocolate eliminates the need for tempering, simplifies dessert preparation, and minimizes waste, making it a preferred choice for chefs and bakers. Its consistent performance across batches also supports menu standardization, which is crucial for chains and franchises. As the organized foodservice sector continues to expand across South America, the demand for compound chocolate in the HoReCa segment is anticipated to rise significantly.

Geography Analysis

Brazil contributed 47.36% of South America's compound chocolate revenue in 2024, driven by its robust cocoa supply chains and the region's largest confectionery production facilities. Manufacturers in Brazil benefit from their proximity to Bahia’s cocoa-growing regions, which ensures a steady supply of raw materials, and from cost efficiencies achieved through large-scale operations in Minas Gerais. The introduction of front-of-pack labeling regulations in 2024 prompted producers to reformulate their products using alternative fats to meet the new standards. The growing number of hotels, restaurants, and cafés in smaller cities has increased demand for compound chocolate in the HoReCa sector, further driving market growth.

Colombia is expected to experience the fastest growth, with a projected CAGR of 6.93% through 2030, driven by government initiatives that promote the local processing of cacao into higher-value finished products. The increasing popularity of snack bars, particularly among millennials in cities such as Bogotá and Medellín, is driving demand for compound chocolate used in chips and coatings. Meanwhile, Chile and Argentina, though smaller markets, cater to higher-income consumers who are more health-conscious. This has led to innovations in compound chocolate products, such as reduced-sugar and shea-based alternatives, to align with consumer preferences for healthier options.

Other South American countries, including Ecuador, Paraguay, and Uruguay, are in the early stages of adopting compound chocolate, with growth closely tied to the expansion of modern retail outlets. Ecuador, despite its abundant cacao resources, has not yet developed large-scale domestic production of compound chocolate, as much of its cacao is still exported in raw form. However, local entrepreneurs are gradually introducing new product lines aimed at regional exports, signaling potential growth opportunities in these emerging markets. As modern retail infrastructure expands, these countries are likely to see increased adoption of compound chocolate products in the coming years.

Competitive Landscape

The South American compound chocolate market is moderately consolidated, with major players such as Barry Callebaut and Cargill leading the industry. These companies utilize vertical integration to streamline their operations, reduce costs, and efficiently supply multinational bakeries and confectionery companies. Regional companies such as Arcor and Luker Chocolate focus on meeting local preferences by offering region-specific flavors and ensuring faster delivery times. Additionally, start-ups in Brazil are innovating with products made from Amazonian superfruits, which are gaining popularity in export markets despite their smaller domestic presence.

Technological advancements in the market are focused on developing fat blends that replicate the texture and shine of cocoa butter while complying with stricter regulations on saturated fat content. Barry Callebaut is working on enzymatic interesterification techniques, while Cargill is introducing shea-based product lines to address these requirements. Smaller players are emphasizing sustainability and traceability, promoting their fat blends as environmentally friendly alternatives that avoid the negative impacts of palm oil deforestation. These innovations reflect the industry's efforts to strike a balance between functionality, regulatory compliance, and environmental concerns.

Distribution strategies differ across the market, depending on the type of player. Established companies secure long-term contracts with HoReCa (Hotels, Restaurants, and Cafés) businesses, ensuring steady demand through multi-year supply agreements. On the other hand, smaller competitors focus on artisan bakeries by offering smaller quantities of specialized products like chocolate fillings and drops. Additionally, there has been a significant increase in patent filings for heat-resistant coatings since 2024, highlighting the industry's commitment to innovation despite regulatory challenges. These diverse strategies showcase how companies are adapting to capture market share and meet evolving customer needs.

South America Compound Chocolate Industry Leaders

-

Barry Callebaut Group

-

Cargill Inc.

-

Puratos Group

-

Arcor S.A.I.C.

-

Mondelēz International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Barry Callebaut and NotCo AI ("NotCo") formed a partnership to explore the integration of artificial intelligence in chocolate recipe development.

- August 2025: Nestlé SA announced environmental restoration initiatives in collaboration with reforestation startup re.green and chocolatier Barry Callebaut in Brazil. The project aimed to plant millions of trees in regions where the company sources essential ingredients, contributing to sustainability and ecosystem restoration efforts.

- July 2025: Puratosestablished an Innovation Center and Research and Development (R&D) laboratory in Cartago, Costa Rica. This facility aimed to drive product innovation and support local businesses by providing advanced solutions tailored to the region's needs.

South America Compound Chocolate Market Report Scope

In the South America compound chocolate market, dark, milk, white, and others are covered as segments by product type. Chips/drops/chunks, slabs and blocks, coatings, filling and spreads, and others are covered as forms. This application covers bakery and confectionery, ice cream and frozen desserts, beverages, and other related products. Retail, industrial, and HoReCa are covered as distribution channels, and Brazil, Colombia, Chile, Peru, Argentina, and the Rest of South America are covered as countries.

By Product Type

| Dark |

| Milk |

| White |

| Others |

By Form

| Chips/Drops/Chunks |

| Slabs and Blocks |

| Coatings |

| Fillings and Spreads |

| Others |

By Application

| Bakery and Confectionery |

| Ice Cream and Frozen Desserts |

| Beverages |

| Others |

By Distribution Channel

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others | |

| Industrial | |

| HoReCa |

By Country

| Brazil |

| Colombia |

| Chile |

| Peru |

| Argentina |

| Rest of South America |

| By Product Type | Dark | |

| Milk | ||

| White | ||

| Others | ||

| By Form | Chips/Drops/Chunks | |

| Slabs and Blocks | ||

| Coatings | ||

| Fillings and Spreads | ||

| Others | ||

| By Application | Bakery and Confectionery | |

| Ice Cream and Frozen Desserts | ||

| Beverages | ||

| Others | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| Industrial | ||

| HoReCa | ||

| By Country | Brazil | |

| Colombia | ||

| Chile | ||

| Peru | ||

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the South America compound chocolate market?

It is valued at USD 1.87 billion in 2025 with a 5.64% CAGR projected to 2030.

Which product type is growing fastest in South America?

Dark compound chocolate is expanding at a 7.64% CAGR due to its perceived health benefits and affordable price.

Which country will post the highest growth to 2030?

Colombia leads with a 6.93% CAGR, supported by government incentives and rising domestic snack consumption.

What key factor drives ice-cream segment adoption of compound coatings?

What key factor drives ice-cream segment adoption of compound coatings?

Page last updated on: