Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

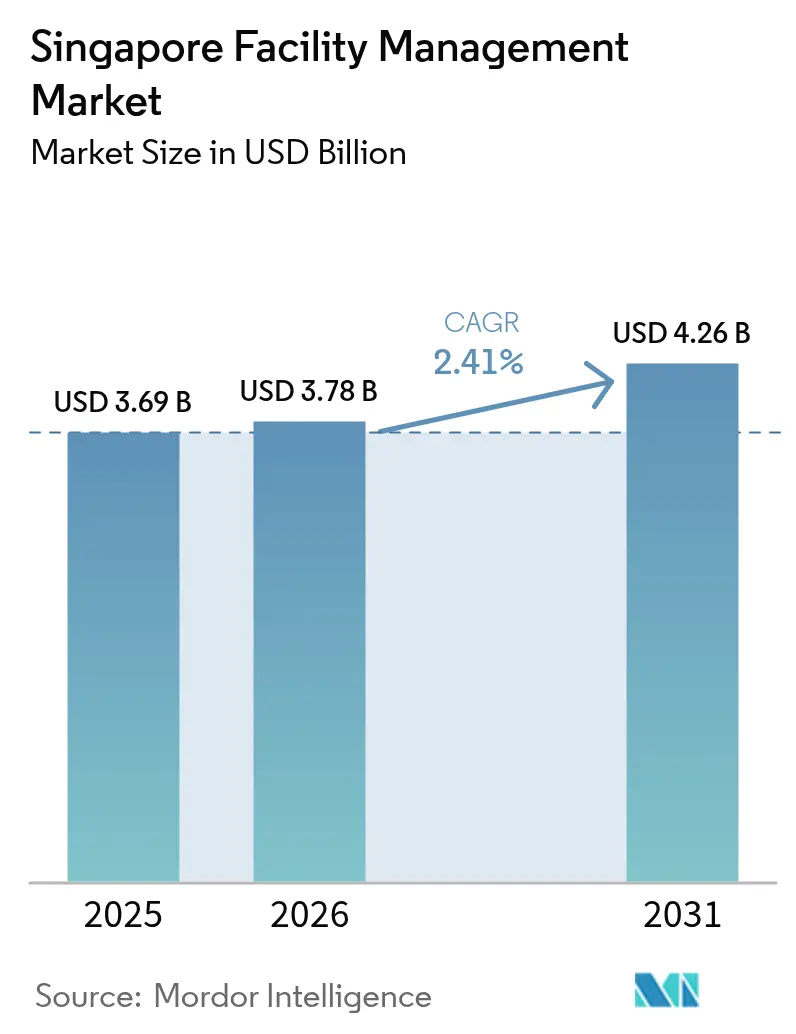

| Base Year Market Size (2025) | USD 3.69 Billion |

| Market Size (2026) | USD 3.78 Billion |

| Market Size (2031) | USD 4.26 Billion |

| Growth Rate (2026 - 2031) | 2.41% CAGR |

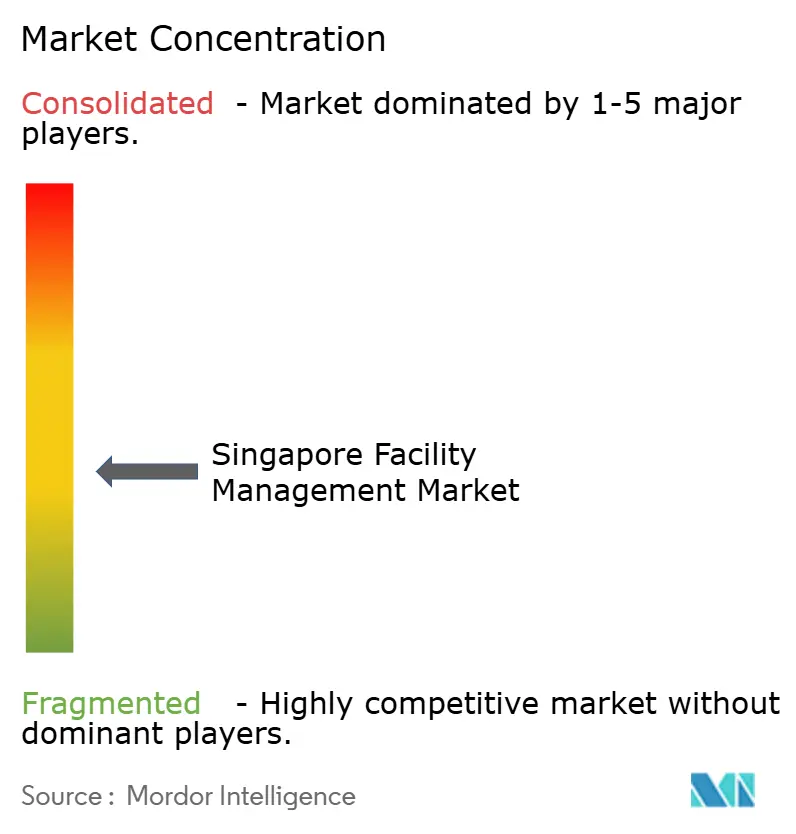

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Facility Management Market Analysis by Mordor Intelligence

The Singapore facility management market size was valued at USD 3.69 billion in 2025 and estimated to grow from USD 3.78 billion in 2026 to reach USD 4.26 billion by 2031, at a CAGR of 2.41% during the forecast period (2026-2031). Growth is steady rather than explosive because Singapore’s built environment is already well-developed, so demand pivots toward smarter service delivery instead of new square footage. Widespread deployment of IoT sensors, cloud dashboards, and data-driven workflows under the Smart Nation program is reshaping service contracts, nudging customers toward longer-tenure, outcome-based agreements. Tighter foreign-worker quotas and escalating wages continue to push automation, while mandatory BCA Green Mark Plus rules accelerate investment in energy-efficient retrofits. Competition is shifting from price-led bidding to technology-rich value propositions as clients expect seamless hard and soft service integration with guaranteed key-performance outcomes.

Key Report Takeaways

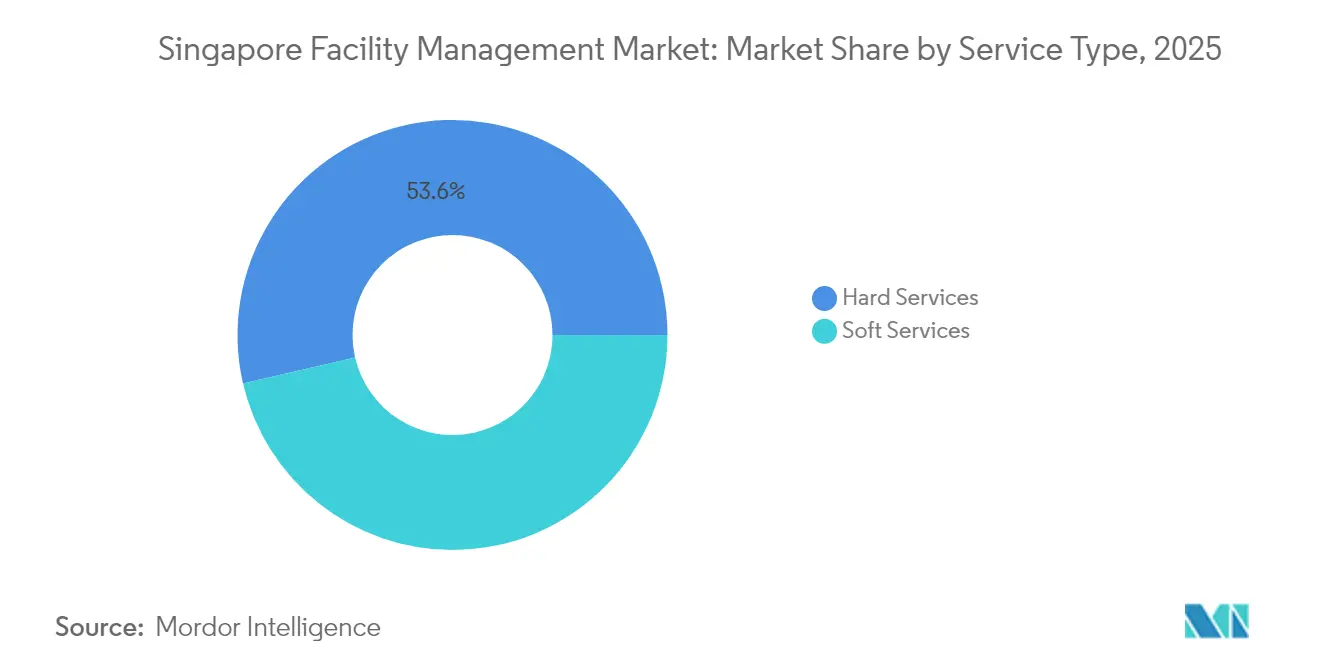

- By service type, hard services held 53.62% of the Singapore facility management market share in 2025; soft services are expanding at a 2.99% CAGR through 2031.

- By offering type, outsourced models commanded 62.98% of the Singapore facility management market size in 2025, while in-house delivery is projected to advance at a 3.88% CAGR to 2031.

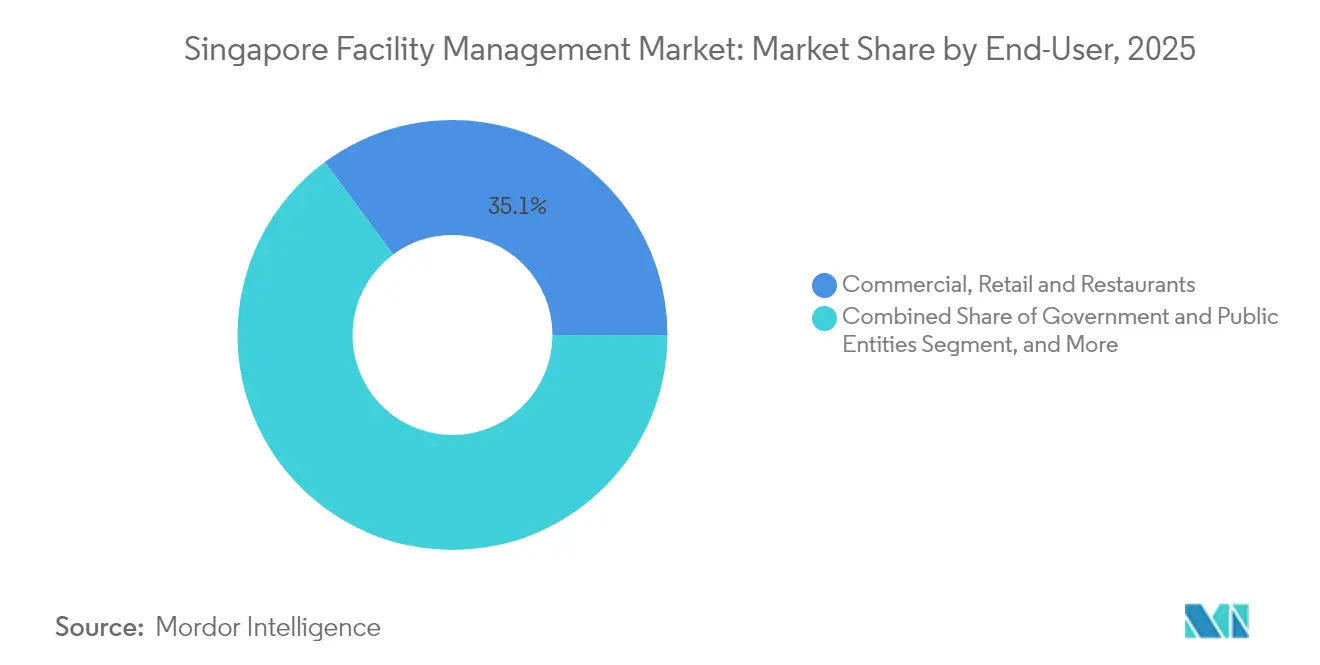

- By end-user, commercial, retail, and restaurants contributed 35.12% revenue in 2025; government, infrastructure, and public entities represent the fastest trajectory at 3.31% CAGR.

- By facility type, commercial buildings generated 37.55% of the 2025 value, yet public infrastructure is poised for a 5.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing of Non-core Operations Accelerating | +0.60% | Singapore-wide, with spillover to regional operations | Medium term (2-4 years) |

| Infrastructure Boom in MRT-Linked Districts | +0.80% | Singapore, concentrated in western and central regions | Long term (≥ 4 years) |

| Mandatory BCA Green Mark Plus Compliance | +0.50% | Singapore commercial and institutional buildings | Short term (≤ 2 years) |

| Ageing Commercial Stock Requiring Lifecycle Upgrades | +0.30% | Singapore CBD and mature commercial districts | Medium term (2-4 years) |

| Smart Estates under Singapore Smart Nation Drive | +0.20% | Singapore-wide with pilot implementations | Long term (≥ 4 years) |

| Integrated Facilities Contracts in Public Healthcare | +0.10% | Singapore healthcare facilities and polyclinics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Outsourcing of Non-core Operations Accelerating

Organizations are handing off building operations so they can focus on core revenue drivers. Since May 2020, every public-sector contract for security has had to comply with Security Outcome-Based Contracting, forcing bidders to prove technology capabilities rather than supply headcount.[1]Singapore Police Force, “Security Outcome-Based Contracting,” police.gov.sg CapitaLand Integrated Commercial Trust illustrates how extensive outsourcing can become: property management for its USD 17.9 billion portfolio is handled by specialist subsidiaries that run leasing, engineering, and sustainability programs end-to-end.[2]CapitaLand Integrated Commercial Trust Management Limited, “Annual Report 2022,” investor.cict.com.sg Access to advanced analytics, computer-vision patrols, and predictive maintenance tools that would be cost-prohibitive to build in-house further strengthens the outsourcing rationale. As environmental disclosure rules tighten, clients also rely on external FM partners for carbon-reporting expertise. Collectively, these dynamics raise the bar for service providers while expanding contract scope and duration within the Singapore facility management market.

Infrastructure Boom in MRT-Linked Districts

Singapore is adding entire rail corridors, each embedding long-term O&M obligations. The Land Transport Authority’s USD 355.2 million Maju station civil package for Cross Island Line Phase 2 and the nine-year Jurong Region Line operating license awarded to the SBS Transit and RATP Dev consortium require AI-driven condition monitoring from day one.[3]Land Transport Authority, “Maju Station Civil Contract Award,” lta.gov.sg Asset owners, therefore, lock in integrated FM partners early, guaranteeing multi-decade revenue streams for vendors proficient in track-side facilities, station utilities, and crowd-flow analytics. Knock-on effects spread to retail podiums, office towers, and residential projects clustered around new stations, all of which demand unified building systems to ensure a frictionless commuter experience. This rail-centric development model underpins service line diversification and regional spillover growth for the Singapore facility management market.

Mandatory BCA Green Mark Plus Compliance

Since 2024, the updated Green Mark Plus framework mandates measurable year-on-year energy performance gains. The BCA–Microsoft pilot retrofitted 30 buildings with sensor-enabled chiller analytics that cut annual electricity consumption by up to 30%.[4]Attune, “Microsoft and BCA’s Chiller Efficiency Portal,” attuneiot.com Owners now require FM bidders to demonstrate live dashboards, anomaly detection, and guaranteed savings contracts. Financing tools such as BREEF allow providers to front capital expenditure and recoup it through verified utility savings, shifting FM from a cost center to an investment partner. Compliance deadlines over the next two years accelerate spend on smart meters, fault detection systems, and engineer upskilling programs. Vendors that can bundle energy audits with project management secure a competitive edge in the Singapore facility management market.

Ageing Commercial Stock Requiring Lifecycle Upgrades

Roughly 40% of CBD floor area predates current efficiency codes, driving retrofit demand. CapitaLand’s SGD 62 million (USD 45.9 million) overhaul of CQ @ Clarke Quay allocated 34% of capex solely to green features such as façade shading and high-efficiency chillers. These multiphase projects create complexity that favours FM firms proficient in coordinating contractors, reallocating tenants, and maintaining safety compliance during works. Predictive asset-condition assessments further extend building lifespan, aligning with owners’ ESG disclosure commitments. As more Grade A stock approaches renewal cycles, lifecycle-upgrade contracts will reinforce revenue stability for the Singapore facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly Fragmented Local Vendor Base | -0.40% | Singapore-wide, affecting service standardization | Short term (≤ 2 years) |

| Tight Foreign-Worker Quotas and Rising Labour Costs | -0.30% | Singapore-wide, concentrated in labor-intensive services | Medium term (2-4 years) |

| Complex Tender Regulations for Government Sites | -0.20% | Singapore government and statutory board facilities | Medium term (2-4 years) |

| Limited Scalability in Island-State Geography | -0.10% | Singapore-wide, affecting growth strategies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Highly Fragmented Local Vendor Base

Hundreds of micro-scale cleaning and security firms make contract administration cumbersome. Each additional subcontractor adds onboarding time, cybersecurity exposure, and interface risk, prompting large owners to consolidate suppliers. BCA now offers competency-based accreditations, but public-agency acceptance remains partial. Until aggregation or certification gains speed, disparate standards will temper efficiency gains in the Singapore facility management market.

Tight Foreign-Worker Quotas and Rising Labour Costs

In 2025, levies for S-Pass holders rose again, and dependency-ratio ceilings tightened. While Approved Training and Testing Centers subsidize upskilling, capacity falls short of market demand. Providers respond with robotics, for instance, autonomous floor-scrubbers and AI-driven HVAC optimization that cut manual interventions by 30% at CEVA Logistics’ warehouses. Still, wage inflation outpaces cost recovery in cleaning and security, squeezing margins across the Singapore facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Dominance with Soft Catch-Up

Hard services represented 53.62% of 2025 revenue within the Singapore facility management market share because mechanical, electrical, and plumbing systems must operate flawlessly in a humid tropical climate. Regulatory obligations for fire-safety certifications and lift-maintenance logs sustain baseline demand. Momentum toward predictive analytics is palpable, exemplified by the Green Mark chiller portal that digests vibration and temperature data to prevent downtime. Clients increasingly value lifecycle-cost optimization over reactive fixes, prompting bundled hard-FM contracts with outcome guarantees.

Soft services are expanding at 2.99% CAGR as outcome-based contracting decouples pricing from headcount. Security Outcome-Based Contracting compels guards to use drones, video analytics, and incident-reporting apps, redefining manpower deployment. Cleaning vendors adopt real-time quality sensors, while tenant-engagement apps coordinate catering and concierge tasks. Although soft services still trail hard services in absolute value, their technology-enabled rebound illustrates how the Singapore facility management market evolves from labour-intensive routines to data-validated experiences.

By Offering Type: Outsourced Strength and In-house Resurgence

Outsourcing held 62.98% of the Singapore facility management market size in 2025 because clients prefer one-stop specialists for compliance, warranty management, and sustainability reporting. Integrated FM contracts that fuse engineering, environmental, and hospitality tasks gain traction, with CapitaLand bundling leasing, technical, and ESG services under single-vendor accountability. Automated ticketing platforms and SLA dashboards lock in performance transparency, which owners increasingly treat as a risk-transfer mechanism.

In-house delivery, though just 37.02% in 2025, is forecast to grow 3.88% CAGR as data-center operators and government agencies seek tighter control over cybersecurity and critical systems. BCA Academy’s new smart-building curricula underpin this shift by supplying certified engineers versed in digital twins, IoT cybersecurity, and fault diagnostics. Hybrid models are also emerging where owners retain analytics and strategy while outsourcing boots-on-ground execution, reflecting nuanced demand patterns in the Singapore facility management market.

By End-User Industry: Commercial Leadership and Public-Sector Upswing

Commercial, retail, and restaurant sectors accounted for 35.12% of the 2025 value, thanks to Singapore’s role as an Asia-Pacific headquarters hub. High-rise office towers along Marina Bay rely on sophisticated energy dashboards to satisfy tenant sustainability pledges. Retail landlords integrate footfall analytics, predictive cooling, and tenant-service kiosks to enhance dwell time. Restaurants emphasize food-safety automation and smart waste tracking to comply with National Environment Agency guidelines, underscoring the segment’s digital maturity.

Government, infrastructure, and public entities are accelerating at a 3.31% CAGR. Multi-line contracts tied to MRT extensions, polyclinic expansions, and public-housing precinct upgrades embed 20-year maintenance scopes from inception. Outcome-based KPIs such as platform-temperature regulation and commuter-safety scores replace traditional unit-rate schedules, upgrading contract complexity. These long-horizon engagements, coupled with strict data-sovereignty clauses, elevate barriers to entry and expand opportunity within the Singapore facility management market.

By Facility Type: Commercial Building Scale and Infrastructure Velocity

Commercial buildings delivered 37.55% of 2025 revenue, anchoring the Singapore facility management market size through Grade A towers, malls, and mixed-use hubs. Vertical complexity demands advanced façade-cleaning robots, demand-responsive elevators, and AI-enabled air-distribution systems that cut cooling loads up to 15%. Property owners also deploy tenant-experience apps that amalgamate access control, e-payments, and community events, embedding FM providers deeper into the value chain.

Public infrastructure is expected to grow 5.05% CAGR, the fastest of any facility type, as MRT-linked megaprojects and fast-charging EV hubs proliferate. Volt, Keppel’s mobility unit, will run Southeast Asia’s largest public EV fast-charging hub, opening a new frontier for asset-intensive FM services in power management and uptime optimization. Stations, depots, and charging plazas require 24/7 monitoring, cybersecurity, and lifecycle asset-replacement programs, broadening service menus across the Singapore facility management market.

Geography Analysis

Singapore’s entire facility stock sits on just 720 square kilometres, enabling rapid response times and dense task clustering. That proximity supports multi-site patrol loops and centralized command centers, improving resource utilization. Yet the compact geography constrains capacity expansion, so providers pivot to cross-border growth by exporting best practices to Indonesia, Vietnam, and Malaysia after honing solutions locally. CapitaLand’s USD 74–111 million planned outlays for Vietnam industrial assets exemplify this outward push while maintaining a Singapore-based operational nerve center.

Smart Nation projects permeate every neighbourhood. IoT nodes monitor humidity and equipment vibration, while AI routines auto-dispatch technicians based on predictive alerts. The BCA–Microsoft initiative illustrates how real-time data becomes table stakes rather than a premium add-on. Tropical weather exacerbates Mold, corrosion, and equipment failures, necessitating constant dehumidification and proactive varnish inspections, especially in coastal districts.

Regulation is both a shield and a moat. Uniform codes streamline compliance across the island, but high standards covering energy intensity, fire safety, and accessibility favour incumbents familiar with local statutory nuances. Although the market’s physical reach is finite, the Singapore facility management market leverages its regulatory sophistication and tech adoption to influence regional benchmarks, positioning local vendors as preferred partners for emerging Southeast Asian smart-city ventures.

Competitive Landscape

The market hosts global giants such as CBRE, ISS, and Cushman and Wakefield alongside local stalwarts like Certis CISCO and CBM. Global firms deploy enterprise-grade platforms and cross-border key-account programs, serving multinational tenants that mandate uniform SLA metrics across APAC. Local champions draw on intimate knowledge of Singapore’s legislative labyrinth and maintain strong ties with public agencies, winning sensitive contracts that require security clearances and social-enterprise labour schemes.

Outcome-based contracting and technology infusion act as catalysts for consolidation. Providers capable of integrating asset-performance analytics, energy-guarantee financing, and workforce-management robotics are snapping up niche specialists to fill capability gaps. The recent Security Outcome-Based Contracting framework favours capital-rich firms that can shoulder upfront investment in smart-patrol infrastructure. Meanwhile, tight labour quotas make scale matter: larger operators negotiate better robotics leasing terms and can absorb wage shocks, whereas smaller vendors risk margin compression.

White-space remains in high-growth verticals: data centers, healthcare facilities, and EV-charging networks. AWS’s USD 8.88 billion cloud-infrastructure expansion requires uptime tiers that few providers can meet, opening opportunities for mission-critical FM specialists. Hospitals and polyclinics shift to integrated contracts that bundle infection control, biomedical engineering, and facility security, further differentiating service propositions within the Singapore facility management market.

Singapore Facility Management Industry Leaders

ISS A/S

CBRE Group Inc.

CBM Pte Ltd

ENGIE Services Singapore (ENGIE SA)

Sodexo Singapore Pte. Ltd. (Sodexo Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: SBS Transit partnered with RATP Dev to operate the Jurong Region Line, adding 24 stations with AI-based condition monitoring.

- September 2025: Ascott secured 28 new property signings across Southeast Asia, expanding hospitality FM demand including multiple Singapore projects.

- July 2025: Keppel’s Volt unit won a contract to run Southeast Asia’s largest public EV fast-charging hub.

- June 2025: Far East Organization completed its SAP S/4HANA migration with IBM Consulting, unlocking AI-powered facility workflows across 780 developments.

Singapore Facility Management Market Report Scope

Facility management includes various factors that impact organizational productivity and efficiency. FM includes management strategies and procedures for building management, infrastructure management for an organization, and general harmonization of an organization's work environment. This system standardizes services and streamlines operations for an organization.

The Singapore facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services], and soft services [office support and security, cleaning services, catering services, and other soft FM services ]), type (in-house facility management and outsourced facility management [single FM, bundled FM, and integrated FM]), and end-user industry (commercial, retail and restaurants, institutional, government, infrastructure, and public entities and industrial, and other end-user industries). The Market Sizes and Forecasts are Provided in Value (USD) for all the Above Segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-User Industry

| Commercial, Retail and Restaurants |

| Manufacturing and Industrial |

| Government, Infrastructure and Public Entities |

| Institutional |

| Other End-user Industries |

By Facility Type

| Commercial Buildings |

| Industrial Facilities |

| Public Infrastructure |

| Institutional Buildings |

| Other Facility Types |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-User Industry | Commercial, Retail and Restaurants | |

| Manufacturing and Industrial | ||

| Government, Infrastructure and Public Entities | ||

| Institutional | ||

| Other End-user Industries | ||

| By Facility Type | Commercial Buildings | |

| Industrial Facilities | ||

| Public Infrastructure | ||

| Institutional Buildings | ||

| Other Facility Types | ||

Key Questions Answered in the Report

What CAGR is forecast for the Singapore facility management market between 2026 and 2031?

The market is set to grow at 2.41% CAGR, moving from USD 3.78 billion in 2026 to USD 4.26 billion by 2031.

Which service category currently holds the largest share of facility spending in Singapore?

Hard services, covering mechanical, electrical and plumbing maintenance, account for 53.62% of 2025 spending.

Why are outsourced facility contracts so prevalent in Singapore?

Outsourcing dominates with 62.98% share because specialized vendors offer compliance expertise, technology investment and outcome-based guarantees that many owners prefer over in-house crews.

Which end-user vertical is expanding fastest through 2031?

Government, infrastructure and public entities are projected to rise at 3.31% CAGR, fueled by MRT expansions and smart-estate projects.

How does the Smart Nation program influence facility management?

The initiative embeds IoT sensors, predictive analytics and automated controls across buildings, making data-driven FM a baseline requirement for winning contracts.

What workforce challenges do Singapore FM companies face?

Tight foreign-worker quotas and rising wages spur automation investment while pressuring margins, especially in labor-intensive cleaning and security services.

Page last updated on: