India Securities Brokerage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Base Year Market Size (2025) | USD 6.18 Billion |

| Market Size (2026) | USD 6.98 Billion |

| Market Size (2031) | USD 13.09 Billion |

| Growth Rate (2025 - 2030) | 13.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Securities Brokerage Market Analysis by Mordor Intelligence

The India Securities Brokerage Market size is expected to grow from USD 6.18 billion in 2025 to USD 6.98 billion in 2026 and is forecast to reach USD 13.09 billion by 2031 at 13.33% CAGR over 2026-2031.

This measured growth trajectory reflects a market undergoing structural transformation as regulatory reforms reshape revenue models while technology adoption accelerates client acquisition. The sector's evolution from traditional full-service models to digital-first platforms has fundamentally altered competitive dynamics, with discount brokers capturing market share through zero-brokerage strategies that compress margins but expand addressable markets. SEBI's comprehensive derivatives trading reforms implemented throughout 2024-2025 have created a watershed moment for brokerage revenues, with F&O volumes declining 27% and broker profits dropping 37-60% across major players[1]Securities and Exchange Board of India, “SEBI Annual Report 2024-25,” SEBI.GOV.IN. This regulatory recalibration coincides with unprecedented demat account growth, surpassing 120 million accounts by August 2025, driven by streamlined KYC processes and UPI-enabled instant fund transfers that reduce friction in retail participation. The convergence of regulatory tightening and technological enablement has forced brokers to diversify revenue streams beyond transaction fees toward wealth management, lending, and advisory services.

Key Report Takeaways

- By type of security, stock trading led with 46% of the India securities brokerage market share in 2024, while derivatives are projected to grow at an 8.9% CAGR through 2030.

- By brokerage service, stock brokerage commanded 40.2% of the India securities brokerage market share in 2024, and forex services are advancing at a 7.4% CAGR.

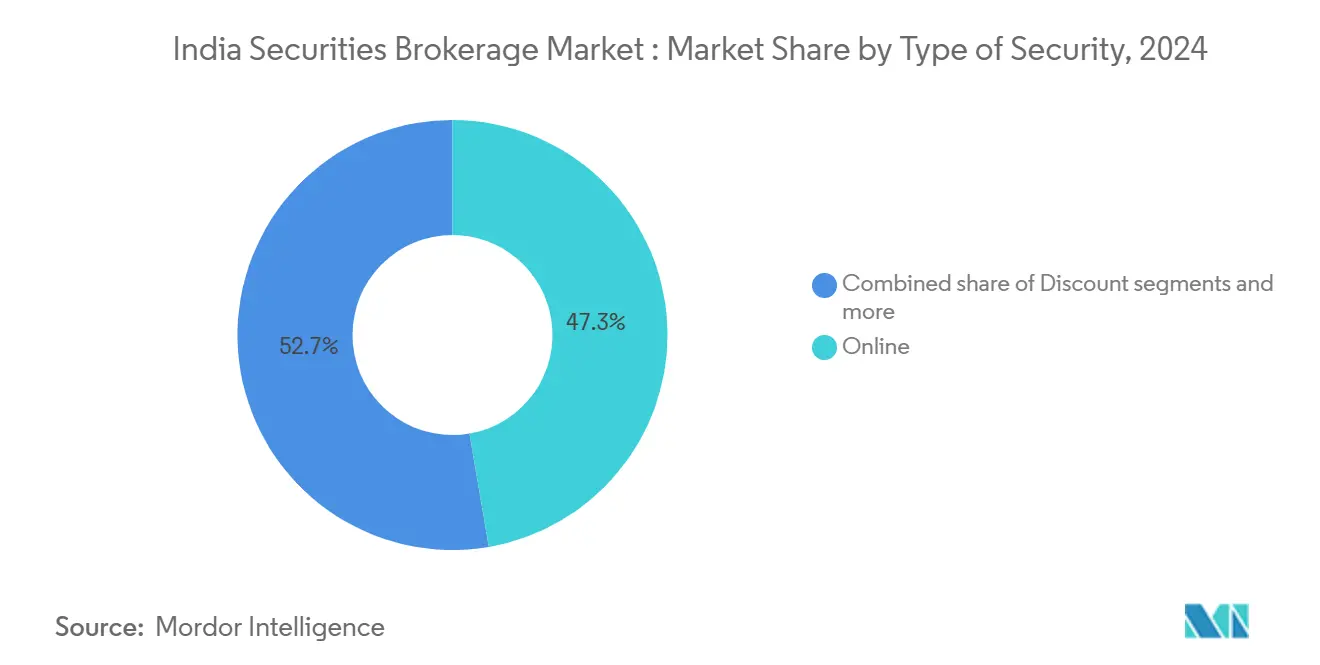

- By service type, online channels captured 51.3% of the India securities brokerage market share in 2024; robo-advisory platforms are set to expand at a 15.2% CAGR to 2030.

- By client type, retail investors accounted for 63.4% of the India securities brokerage market share in 2024, and the segment is progressing at a 9.1% CAGR over the forecast period.

- By geography, South India held 34.1% of the India securities brokerage market share in 2024, whereas West India records the fastest growth at a 6.5% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Securities Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demat account openings post-2020 | +3.5% | National, with concentration in South and West India | Medium term (2-4 years) |

| Growth of low-cost mobile trading platforms | +2.7% | National, strongest in tier-2/3 cities | Short term (≤ 2 years) |

| UPI-enabled instant fund transfer | +1.8% | National, highest adoption in urban centers | Short term (≤ 2 years) |

| Expanded exchange product suite | +1.3% | National, early adoption in metro cities | Medium term (2-4 years) |

| Tokenization of sovereign gold bonds | +0.9% | National, pilot phase in select cities | Long term (≥ 4 years) |

| Wealth-tech partnerships with neo-banks | +1.1% | Urban centers, expanding to tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demat Account Growth Transforms Market Access

Post-2020 demat account proliferation has fundamentally altered India's investment landscape, with accounts growing from 40 million to over 120 million by August 2025. SEBI's digital KYC rationalization and e-sign integration eliminated traditional paperwork barriers, enabling account opening within minutes rather than days [2]Securities and Exchange Board of India, “Demat Account Statistics 2025,” SEBI.GOV.IN. . This democratization effect extends beyond urban centers, with tier-2 and tier-3 cities contributing 45% of new account openings in 2024. The velocity of account creation has outpaced global benchmarks, positioning India as the world's fastest-growing retail investment market. However, account activation rates remain below 60%, indicating significant latent capacity for revenue conversion as financial literacy programs expand and product awareness increases.

Mobile-First Trading Platforms Reshape Client Acquisition

The migration to mobile-first trading platforms has created a structural shift in client acquisition costs and engagement patterns. Over 95% of new brokerage accounts originate from mobile applications, with average client acquisition costs dropping 40% compared to traditional branch-based models[3]National Payments Corporation of India, “UPI Product Statistics 2024,” NPCI.ORG.IN.. Zerodha's Kite platform processes over 6 million orders daily, while Angel One's SuperApp strategy integrates trading with mutual funds, insurance, and loans to increase client lifetime value. The mobile-centric approach has enabled brokers to reach previously underserved markets, with rural and semi-urban areas contributing 35% of new client additions. This technological leverage allows discount brokers to maintain profitability despite zero-brokerage models through scale economics and cross-selling opportunities.

UPI Integration Accelerates Trading Velocity

UPI AutoPay integration for securities trading has eliminated settlement delays that historically constrained intraday trading volumes. The Reserve Bank of India's payment infrastructure enables instant fund transfers up to INR 500,000 (USD 6,000) per transaction, facilitating same-day trade settlements and margin funding[4]Reserve Bank of India, “Financial Stability Report Dec 2024,” RBI.ORG.IN.. This technological advancement has increased average trading frequency by 25% among retail clients, as liquidity constraints no longer limit participation in volatile market conditions. The integration extends to IPO applications, mutual fund investments, and derivatives trading, creating a seamless financial ecosystem that reduces friction across investment products. NPCI data indicates securities-related UPI transactions grew 180% in 2024, demonstrating the infrastructure's transformative impact on capital markets participation.

Exchange Product Innovation Expands Revenue Opportunities

NSE and BSE's expanded product suite, including SME IPOs, InvITs, REITs, and weekly options, has diversified revenue streams for brokers beyond traditional equity trading. SME IPO listings increased 65% in 2024, generating higher brokerage fees due to retail allocation preferences and subscription multiples. InvIT and REIT markets have attracted institutional participation, creating opportunities for full-service brokers to leverage research capabilities and advisory services. Weekly options expiry introduction has increased derivatives trading frequency, though SEBI's subsequent restrictions on contract proliferation have moderated this growth. The product diversification strategy enables brokers to capture wallet share across asset classes while reducing dependence on equity market volatility for revenue generation.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-brokerage price wars | -2.2% | National, acute in metro markets | Short term (≤ 2 years) |

| Exchange infrastructure dependency | -1.3% | National | Medium term (2-4 years) |

| Inadequate cyber-resilience frameworks at mid-tier brokers | -1.7% | National, concentrated in emerging broker segments | Medium term (2–4 years) |

| Limited capital-market literacy outside Tier-1 cities | -1.4% | Regional, prominent in Tier-2 and Tier-3 markets | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Zero-Brokerage Competition

The race-to-zero brokerage pricing has fundamentally altered industry economics, with leading players eliminating equity delivery charges to attract price-sensitive retail clients. This strategic shift has compressed per-client revenue by 35-40% across the industry, forcing brokers to achieve profitability through scale and ancillary services. Zerodha's zero-brokerage model, generating revenue through interest on client funds and currency trading spreads, has become the industry template that competitors must match to remain competitive. The margin compression particularly impacts full-service brokers whose advisory and research capabilities command a limited premium in a commoditized trading environment. Regulatory frameworks under SEBI oversight ensure fair competition while preventing predatory pricing that could destabilize market structure.

Exchange Infrastructure Concentration Creates Systemic Risk

India's securities trading infrastructure remains highly concentrated around NSE and BSE systems, creating single points of failure that can disrupt nationwide trading activity. The February 2021 NSE technical outage, which halted trading for several hours, highlighted the systemic vulnerabilities inherent in a centralized market structure. While both exchanges have invested heavily in disaster recovery and backup systems, the fundamental architecture remains susceptible to cyber-attacks, technical failures, and capacity constraints during high-volume periods. This concentration risk extends to clearing and settlement systems, where NSCCL and ICCL handle the majority of trade processing, creating additional bottlenecks that could impact broker operations and client confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Security: Derivatives Gain Speed

Stock trading maintains its dominant position at 46% market share in 2024, reflecting India's equity-centric investment culture and retail preference for direct ownership over complex instruments. However, derivatives trading emerges as the fastest-growing segment at 8.9% CAGR through 2030, driven by sophisticated retail participation and institutional hedging requirements despite SEBI's regulatory tightening. The derivatives segment's resilience stems from its role in price discovery and risk management, with F&O turnover exceeding cash market volumes by 3:1 ratios during volatile periods at NSE. Bonds represent 6.5% market share but face structural headwinds from corporate credit concerns and interest rate volatility, while ETFs and mutual funds capture growing systematic investment plan flows.

Treasury notes and government securities trading remains constrained at 1.1% market share, primarily serving institutional participants and high-net-worth individuals seeking fixed-income exposure. The segment's limited retail penetration reflects complexity barriers and minimum investment thresholds that exclude smaller investors. SEBI's regulatory influence through margin requirements and position limits continues to shape derivatives participation, with new delta-based open interest calculations (FutEq) providing more accurate risk measurement frameworks that could enhance market stability while maintaining growth momentum.

By Type of Brokerage Service: Forex Gains Momentum Through GIFT City

Stock brokerage services dominate the market at a 40.2% share in 2024, encompassing equity delivery, intraday, and derivatives trading that form the core revenue base for most brokers. Forex trading emerges as the fastest-growing service category at 7.4% CAGR, propelled by NSE IFSC's dollar-rupee futures contracts and GIFT City's international trading infrastructure that enables 24-hour currency trading. This growth trajectory reflects India's increasing integration with global financial markets and NRI investment flows that require currency hedging capabilities.

Commodities trading maintains a 3.1% market share through the MCX and NCDEX platforms, serving agricultural producers and industrial consumers seeking price risk management tools. Insurance brokerage represents a 2.7% share but faces regulatory constraints from IRDAI guidelines that limit cross-selling opportunities between securities and insurance products. Real estate and mortgage brokerage services capture 5.2% combined share, benefiting from property market recovery and home loan demand in tier-2 cities. The regulatory framework under SEBI oversight ensures service quality standards while enabling innovation in product delivery and client engagement models.

By Type of Service: Robo-Advisory Platforms Capture Millennial Investment Flows

The technological transformation of service delivery models has created distinct growth patterns across traditional and digital channels. Full-service brokerage maintains 14.0% market share in 2024, serving high-net-worth clients who value research, advisory, and relationship management capabilities that justify premium pricing structures. These services particularly resonate with institutional clients and family offices requiring customized investment solutions and regulatory compliance support.

Robo-advisory platforms represent the fastest-growing service category at 15.2% CAGR through 2030, driven by millennial adoption of algorithm-based portfolio management and systematic investment strategies. The segment's growth reflects changing investor preferences toward low-cost, transparent, and goal-based investing that eliminates human bias and emotional decision-making. Online services command 51.3% market share, representing the industry's digital transformation as mobile applications become the primary client interface. Discount brokerage captures 31.6% share through zero-fee models that attract price-sensitive retail investors, while broker-dealers maintain 3.2% share serving institutional and corporate clients requiring specialized execution services.

By Client Type: Retail Dominance Drives Market Democratization

Retail clients constitute the market's largest segment at 63.4% share in 2024 and demonstrate the highest growth velocity at 9.1% CAGR through 2030, reflecting the democratization of capital markets participation across India's expanding middle class. This retail dominance represents a structural shift from institutional-led markets toward individual investor participation enabled by technology platforms and regulatory reforms that simplified account opening and trading processes. The retail segment's growth momentum stems from increasing disposable income, financial literacy initiatives, and digital payment infrastructure that reduces transaction friction.

High-net-worth individuals maintain a 25.3% market share, generating disproportionate revenue through higher transaction volumes and premium service utilization that includes portfolio management, tax planning, and estate services. Institutional clients represent a 15.7% share but contribute significantly to brokerage profitability through large-block trades and consistent trading volumes that provide revenue stability. Small and mid-sized enterprises capture 4.5% market share, primarily utilizing brokerage services for treasury management, employee stock option plans, and working capital optimization strategies that integrate securities trading with business operations.

Geography Analysis

South India commands the largest market share at 34.1% in 2024, leveraging established financial services ecosystems in Bangalore, Chennai, and Hyderabad that combine technology expertise with investment culture. The region's dominance stems from IT industry wealth creation, educational infrastructure that promotes financial literacy, and cultural affinity for equity investments that dates back to traditional trading communities. Karnataka and Tamil Nadu contribute disproportionately to demat account growth, with Bangalore alone accounting for 8% of national new account openings in 2024.

West India demonstrates the highest growth trajectory at 6.5% CAGR through 2030, driven by Mumbai's financial hub status and Gujarat's entrepreneurial ecosystem that generates consistent investment flows. The region benefits from proximity to corporate headquarters, mutual fund offices, and regulatory bodies that facilitate business development and client acquisition. North India captures 18.6% market share, reflecting Delhi NCR's government and corporate presence, while East India maintains 4.9% share despite Kolkata's historical trading heritage. Central and North-East India represent emerging opportunities with 2.8% and developing market shares, respectively, as digital infrastructure expansion enables brokerage services penetration into previously underserved regions.

Competitive Landscape

The Indian securities brokerage market is moderately fragmented, with the top five players collectively holding a significant portion of the market. This setup creates room for both large-scale players and niche specialists to operate profitably. The market follows a two-tier structure, where discount brokers like Zerodha and Angel One dominate client acquisition by offering zero-brokerage models. On the other hand, full-service firms such as ICICI Securities position themselves at the premium end through integrated banking offerings and tailored advisory services. This balance allows for diverse business models to coexist and succeed. The competitive landscape has intensified following SEBI's derivatives trading reforms, which slashed industry-wide revenues by 25–30% and triggered a strategic shift toward wealth management, lending, and cross-selling initiatives.

Technology has emerged as the key differentiator in the brokerage ecosystem. Market leaders are aggressively investing in AI-driven trading platforms, robo-advisory tools, and mobile-first experiences that reduce acquisition costs and enhance user engagement. Zerodha’s Kite Connect API ecosystem exemplifies this trend by enabling third-party developers to build on its platform, creating network effects and increasing customer retention. These innovations are expanding the scope of brokerage platforms beyond traditional services. By driving ecosystem stickiness, technology investments are helping firms build long-term competitive moats.

Simultaneously, the rise of embedded finance is reshaping distribution models within the industry. The SEBI approval for Jio BlackRock Broking in June 2025 reflects a growing preference for partnerships that leverage existing user bases instead of relying solely on organic growth. In this context, regulatory compliance has become a crucial source of competitive advantage. Mid-tier brokers, in particular, are differentiating through enhanced risk management and robust cybersecurity frameworks that align with SEBI mandates. Strong compliance not only builds trust among clients but also positions firms more favorably in a highly regulated market.

India Securities Brokerage Industry Leaders

Zerodha

Angel One

ICICI Securities

Upstox

Groww

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: SEBI opened algorithmic trading access to retail investors through registered intermediaries, democratizing sophisticated trading strategies previously available only to institutions.

- June 2025: Jio BlackRock Broking received SEBI approval to commence securities brokerage operations, marking Reliance Industries' entry into capital markets through its joint venture with BlackRock.

- June 2025: SEBI implemented comprehensive regulatory reforms covering IPOs, Alternative Investment Funds, REITs/InvITs, and delisting procedures to enhance market transparency and investor protection.

- March 2025: ICICI Securities completed its delisting and merger with ICICI Bank, creating India's largest integrated banking-broking entity with combined assets exceeding INR 20 trillion (USD 240 billion).

India Securities Brokerage Market Report Scope

| Bonds |

| Stocks |

| Treasury Notes |

| Derivatives |

| Others (ETFs, Mutual Funds) |

| Stock |

| Insurance |

| Mortgage |

| Real Estate |

| Forex |

| Leasing |

| Others (Commodities) |

| Full-Service |

| Discount |

| Online |

| Robo Advisor |

| Broker-Dealers |

| Retail |

| High Net Worth Individuals |

| Institutional |

| Small & Mid-Sized Enterprises |

| North India |

| West India |

| South India |

| East India |

| Central India |

| North-East India |

| By Type of Security | Bonds |

| Stocks | |

| Treasury Notes | |

| Derivatives | |

| Others (ETFs, Mutual Funds) | |

| By Type of Brokerage Service | Stock |

| Insurance | |

| Mortgage | |

| Real Estate | |

| Forex | |

| Leasing | |

| Others (Commodities) | |

| By Type of Service | Full-Service |

| Discount | |

| Online | |

| Robo Advisor | |

| Broker-Dealers | |

| By Client Type | Retail |

| High Net Worth Individuals | |

| Institutional | |

| Small & Mid-Sized Enterprises | |

| By Geography | North India |

| West India | |

| South India | |

| East India | |

| Central India | |

| North-East India |

Key Questions Answered in the Report

How large is the India securities brokerage market in 2025?

The India securities brokerage market size is USD 6.18 billion in 2025.

What is the expected CAGR for India brokerage services to 2031?

The market is projected to grow at a 13.3% CAGR between 2026 and 2031.

Which service type holds the largest share today?

Online brokerage commands 51.3% of 2024 value, reflecting digital adoption.

Which segment is growing fastest within the brokerage services?

Robo-advisory platforms are expanding at a 15.2% CAGR through 2030.

Which region shows the highest growth momentum?

West India is forecast to post a 6.5% CAGR through 2030.

Why are margins under pressure for brokers?

Zero-brokerage pricing and heightened competition reduce per-client revenue, prompting firms to diversify income streams.

Page last updated on: