Offshore AUV And ROV Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

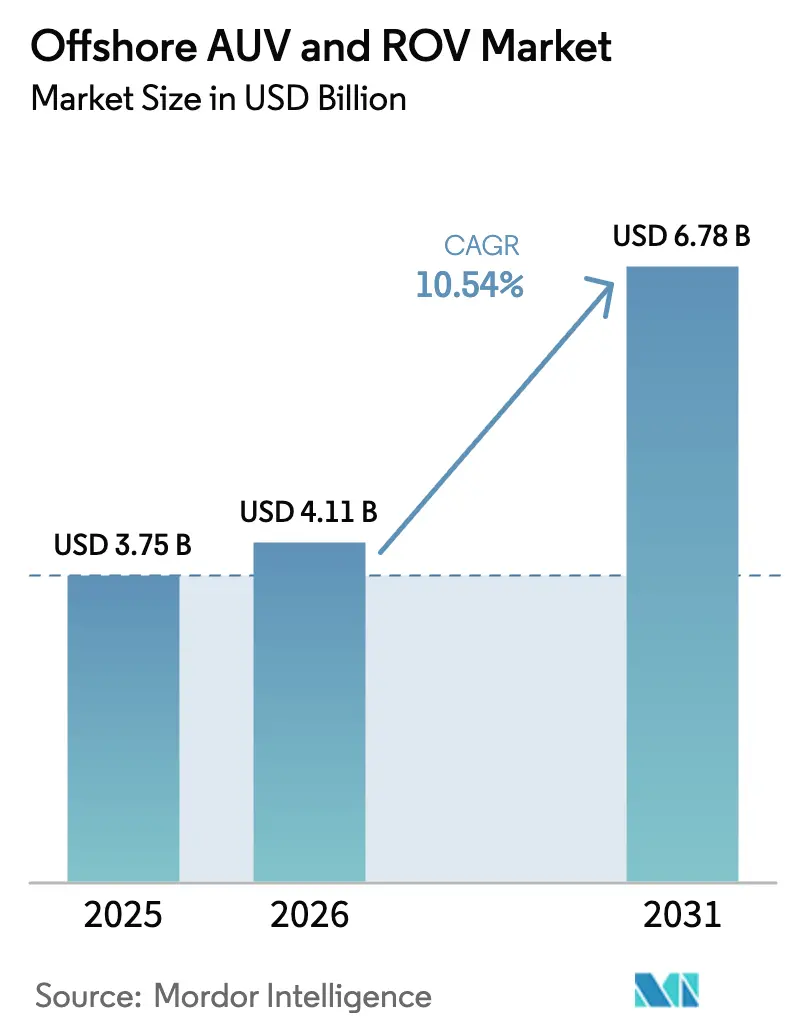

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 6.78 Billion |

| Growth Rate (2026 - 2031) | 10.54% CAGR |

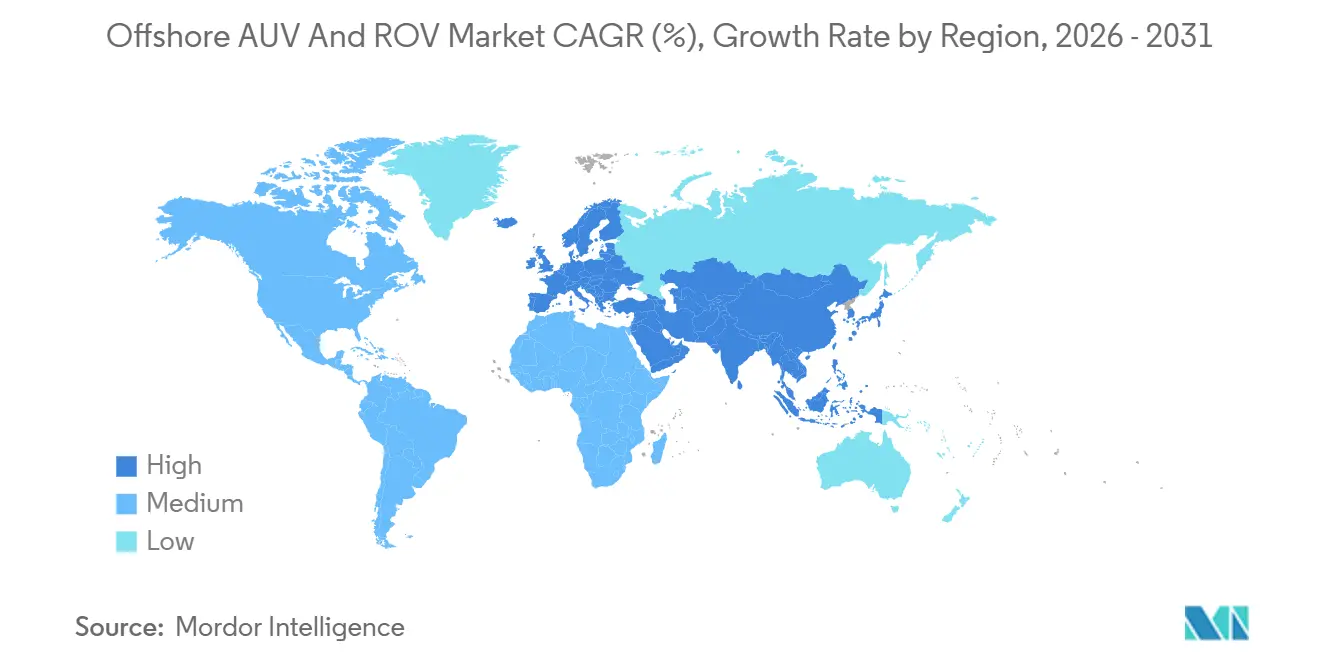

| Fastest Growing Market | Europe |

| Largest Market | Middle East and Africa |

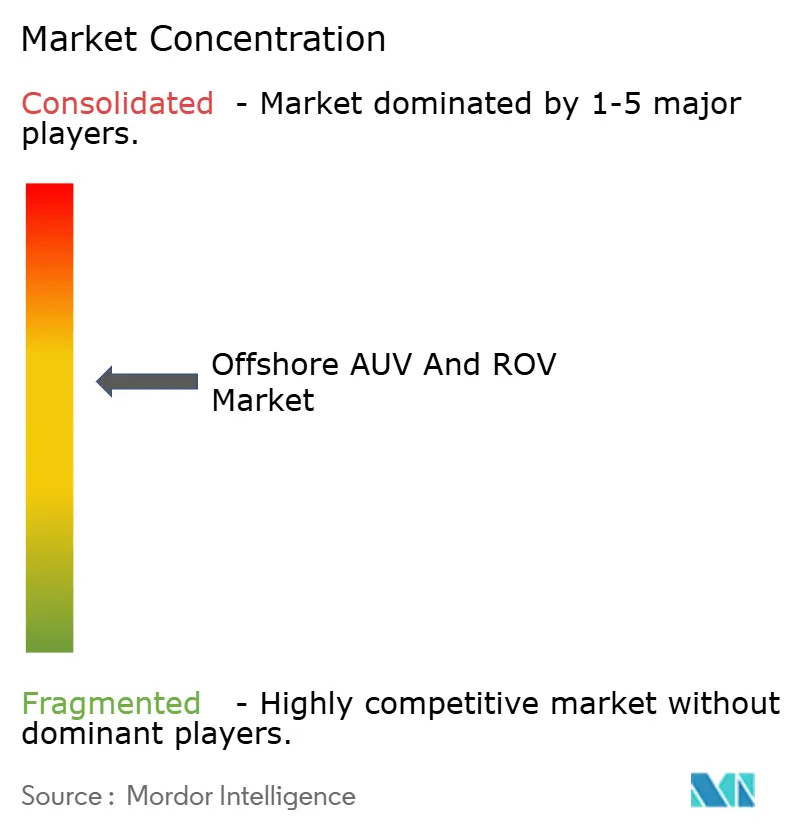

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore AUV And ROV Market Analysis by Mordor Intelligence

The offshore AUV and ROV market size is valued at USD 4.11 billion in 2026 and is projected to reach USD 6.78 billion by 2031, registering a 10.54% CAGR over the forecast period, underscoring the sector’s rapid monetization curve and resilient demand drivers. Oil-and-gas operators are reinvesting in deep-water assets, offshore wind developers are scaling inspection fleets, and defense ministries are fortifying seabed infrastructure, collectively shortening payback periods for subsea robotics at depths beyond diver limits. Remotely operated vehicles currently dominate deployments, yet autonomous underwater vehicles are accelerating fastest as large-area survey and predictive maintenance missions displace towed arrays. Electric propulsion continues to lead thanks to lower topside weight and minimal leakage risk, while hybrid powertrains are gaining traction where torque-intensive tooling and extended endurance converge. The convergence of hydrocarbon extraction, renewable-energy servicing, and maritime security is insulating the offshore AUV and ROV market from oil-price swings and creating multiyear visibility for equipment suppliers.

Key Report Takeaways

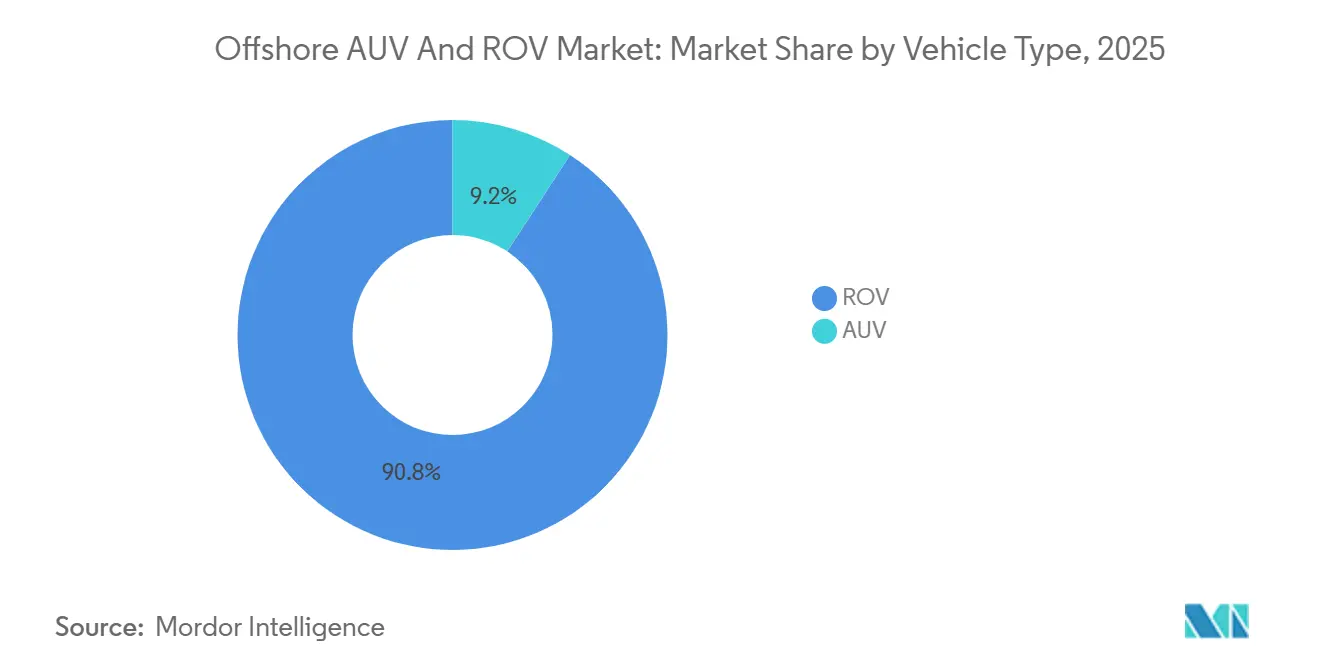

- By vehicle type, remotely operated vehicles held 90.8% of the offshore AUV and ROV market share in 2025, while autonomous underwater vehicles are forecast to expand at a 13.5% CAGR through 2031.

- By vehicle class, work-class platforms commanded a 74.2% share of the offshore AUV and ROV market size in 2025 and are expected to grow at a 12.1% CAGR to 2031.

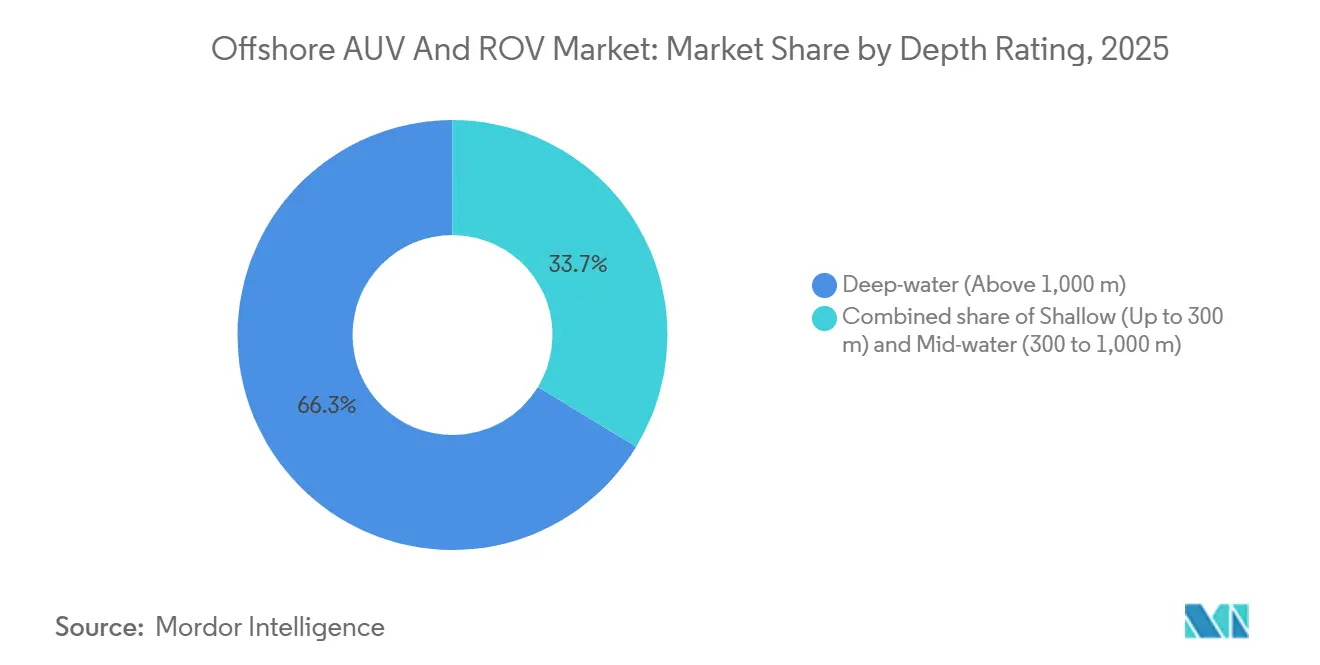

- By depth rating, operations deeper than 1,000 meters captured 66.3% of offshore AUV and ROV market share in 2025, yet shallow-water missions are projected to progress at a 14.4% CAGR through 2031.

- By propulsion system, electric architectures dominated 80.5% of the offshore AUV and ROV market size in 2025, whereas hybrid designs are poised for a 15.3% CAGR to 2031.

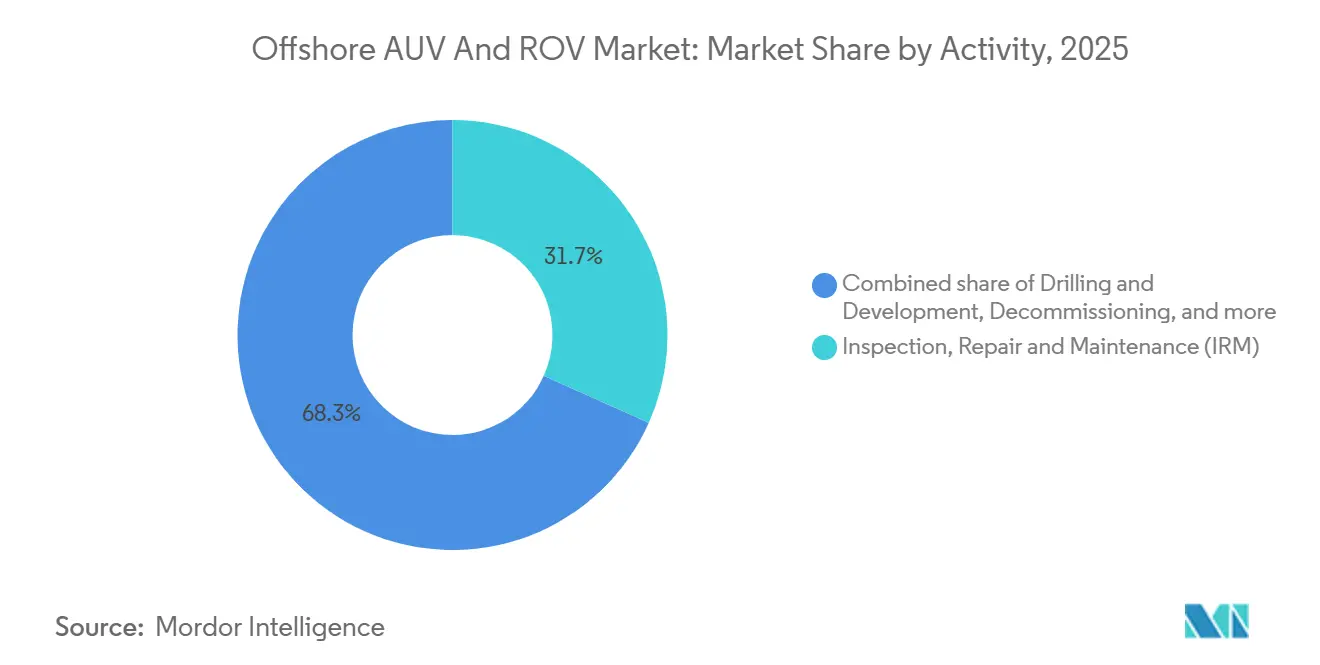

- By activity, inspection, repair, and maintenance accounted for 31.7% of revenue in 2025 and is advancing at a 12.0% CAGR through 2031.

- By end-user, oil and gas represented 83.6% of revenue in 2025; offshore wind is on track for a 20.8% CAGR through 2031, outpacing every other segment.

- By geography, the Middle East and Africa held a dominant 36.1% share of the offshore AUV and ROV market. Meanwhile, Europe is projected to experience robust growth, with an anticipated CAGR of 18.7% extending to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Offshore AUV And ROV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upsurge in deep-water E&P spending post-2024 oil-price recovery | 3.2% | Global, with early gains in MEA, Brazil | Medium term (2-4 years) |

| Accelerating offshore wind capacity build-outs in Europe, APAC & U.S. | 2.7% | Europe, APAC, U.S. East Coast | Long term (≥ 4 years) |

| Remote-operations cost savings >40% via ROC/USV-AUV workflows | 1.6% | North Sea, Gulf of Mexico, APAC | Short term (≤ 2 years) |

| Resident subsea robotics hubs at ≥1 km depth (Equinor, Petrobras pilots) | 1.1% | Norway, Brazil, GoM | Medium term (2-4 years) |

| AI-enabled multi-modal inspection vehicles reducing IRM downtime | 1.0% | Global, concentrated in mature O&G basins | Short term (≤ 2 years) |

| Growing defense budgets for seabed-infrastructure protection (AUKUS, NATO) | 0.6% | U.S., UK, Australia, NATO member states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Upsurge In Deep-Water E&P Spending Post-2024 Oil-Price Recovery

Brent crude stabilized above USD 80 per barrel through 2025, reinstating final investment decisions on ultra-deep projects that had stalled during the pandemic downturn. Petrobras allocated USD 102 billion for 2024-2028 capital spending, with 80% directed to pre-salt fields exceeding 2,000 meters, each requiring heavy-duty work-class ROVs for riser installation and tree intervention. Chevron raised upstream capex by 10% for 2026, prioritizing Gulf of Mexico tie-backs and West African prospects that demand resident inspection drones to minimize rig time. Global offshore capital expenditure is projected to climb to USD 180 billion by 2027, a 22% rise over 2023, with deep-water projects accounting for 60% of incremental spending.[1]International Energy Forum, “Global Upstream Outlook 2025,” ief.org Extended field life for aging North Sea platforms, owing to delayed decommissioning, is sustaining demand for inspection ROVs capable of evaluating fatigue and plugging suspended wells.

Accelerating Offshore Wind Capacity Build-Outs In Europe, APAC & U.S.

The Global Wind Energy Council recorded 35 GW of new offshore wind commissioned in 2024, with Europe and China delivering 28 GW.[2]Global Wind Energy Council, “Global Offshore Wind 2024,” gwec.net The International Energy Agency projects annual additions above 40 GW by 2027 as fixed-bottom and floating arrays reach commercial operation. The United Kingdom’s Dogger Bank, at 3.6 GW, requires year-round cable-burial verification via electric-propulsion AUVs outfitted with multibeam sonar and sub-bottom profilers. Denmark’s Energy Island initiative aims for 10 GW by 2030, mandating real-time inspections of inter-array cables to preserve grid reliability under Energinet standards. Japan designated 11 promotion zones in 2025, prompting Mitsubishi Heavy Industries to trial ROVs for floating-platform mooring checks in typhoon-exposed waters. Taiwan’s 5.6 GW target by 2026 has driven Ørsted and JERA to contract dedicated subsea fleets for scour monitoring in high-current environments.

Remote-Operations Cost Savings above 40% Via ROC/USV-AUV Workflows

Equinor’s Hydrone-R deployment at the Njord field in 2024 cut intervention vessel days by 35% through shore-based piloting.[3]Equinor, “Hydrone-R Deployment Success,” equinor.com Saipem’s Hydrone-W, stationed at 1,200 meters on TotalEnergies’ Ikike field, eliminated a dedicated support vessel, trimming mobilization costs by 40%. ISO 19901-10 formalized guidance for unmanned offshore installations in 2025, while IMCA published best practices for pairing USVs with tethered or autonomous subsea assets. Satellite connectivity, such as Inmarsat Fleet Xpress, enables real-time video streaming to onshore control rooms, allowing 24/7 operations without crew-change cycles. Harsh-weather basins like the Barents Sea particularly benefit as limited weather windows restrict conventional vessel use.

AI-Enabled Multi-Modal Inspection Vehicles Reducing IRM Downtime

Nauticus Robotics introduced the Aquanaut 2 in 2025, embedding computer-vision models trained on 500,000 subsea images that detect corrosion and marine growth with 95% accuracy, cutting data-processing time from weeks to hours. TechnipFMC’s iEPCI digital twin predicts valve-actuator failures via acoustic-signature analysis, enabling scheduled maintenance that preempts unplanned shutdowns. API’s Recommended Practice 2MIM endorses AI-assisted inspection, and ISO 16708 amendments are underway to incorporate autonomous defect classification. Fugro’s cloud analytics reduced inspection cycles for Shell’s Prelude FLNG by 28% in 2025, confirming the commercial case for predictive workflows. Operators are bundling digital twins with long-term service agreements, effectively locking in recurring revenue for analytics vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shallow-water O&G licence bans in California, New Zealand, parts of EU | -1.7% | California, New Zealand, North Sea, select EU | Medium term (2-4 years) |

| Tight global supply of deep-rated Li-ion batteries (sub-sea qualified) | -1.4% | Global, acute in APAC and EU | Short term (≤ 2 years) |

| Tariff-driven surge in specialty-alloy & servo-motor import costs (US-2025) | -0.9% | U.S., with spill-over to North America supply | Short term (≤ 2 years) |

| Acoustic spectrum crowding hindering reliable subsea comms in brownfields | -0.6% | Mature O&G basins (North Sea, Gulf of Mexico) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shallow-Water O&G Licence Bans In California, New Zealand, Parts Of EU

California extended its offshore drilling moratorium to 2030 via Executive Order N-82-20, freezing new leases within state waters and curtailing shallow-water ROV demand in the Santa Barbara Channel.[4]California State Lands Commission, “Drilling Moratorium Extension,” slcc.ca.gov New Zealand’s Crown Minerals Act amendment imposed a permanent ban on new offshore exploration in 2024, re-directing subsea robotics toward decommissioning of legacy Taranaki basin assets. Denmark halted new North Sea licensing rounds in 2024 under its Climate Agreement, accelerating platform removal timelines. Although exploration declines, regulatory directives such as EU Directive 2013/30/EU obligate well plugging and structure removal, sustaining ROV utilization for abandonment campaigns.

Tight Global Supply Of Deep-Rated Li-Ion Batteries (Subsea Qualified)

Pressure-compensated lithium-ion modules remain capacity-constrained as automotive and grid storage absorb worldwide cell production. Blue Logic’s subsea battery, integral to resident drones, relies on specialized electrolyte chemistries manufactured by a limited supplier base, including Saft and EnerSys, stretching lead times to 18 months in 2025. The U.S. Department of Energy classified battery-grade lithium and cobalt as supply-chain vulnerabilities, citing 70% of cell output concentrated in East Asia. Delivery delays have forced North Sea offshore wind operators to specify hybrid propulsion that combines smaller battery packs with hydraulic systems, slightly raising vessel dependence. IEC 62619 lacks subsea-specific testing protocols, compelling OEMs to shoulder proprietary qualification costs that inhibit economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: ROVs Maintain Dominance While AUVs Accelerate

ROVs captured 90.8% of the offshore AUV and ROV market share in 2025, a testament to their indispensability for real-time manipulation tasks such as valve actuation and hot-stab operations. The offshore AUV and ROV market size for autonomous platforms, however, is projected to expand at a 13.5% CAGR as operators deploy AUVs for wide-area pipeline surveys and environmental monitoring. Petrobras deployed 12 AUVs in 2025 to map pre-salt prospects, lowering survey costs by 50% compared to towed arrays. Regulatory clarity is emerging: pending IMO SOLAS amendments would classify autonomous subsea vehicles as unmanned systems, potentially easing insurance hurdles and accelerating uptake.

The offshore AUV and ROV industry is witnessing a bifurcation: tethered work-class ROVs evolve into mobile manipulators with force-feedback control, while autonomous vehicles serve as sensor-fusion hubs integrating synthetic-aperture sonar and magnetometers. Hybrid models like Saab’s Sabertooth can toggle between tethered and untethered modes; the U.S. Navy ordered USD 25 million worth of such units for mine neutralization in 2025. Defense specifications are expected to cascade into commercial standards, reinforcing demand for dual-mode versatility.

By Vehicle Class: Work-Class Systems Anchor Intervention Spectrum

Work-class ROVs held 74.2% of the offshore AUV and ROV market size in 2025 and will retain leadership with a projected 12.1% CAGR to 2031. Light work-class units dominate cable inspections and valve manipulations in shallow-water wind farms, while heavy work-class vehicles manage riser connections at 4,000-meter depths in Brazil and West Africa. Electric work-class variants such as Soil Machine Dynamics’ eWROV reduce deck weight by 40%, enabling deployment from smaller DP-1 vessels and lowering daily charter rates.

Observatory-class vehicles trail as operators favor multi-role work-class platforms that can shift between laser metrology and cutting tasks without re-mobilization. Fugro’s Blue Essence exemplifies modular work-class architecture capable of carrying a grinder or laser scanner interchangeably, trimming campaign costs. Environmental discharge regulations under OSPAR are accelerating the transition to electric actuation, further reinforcing work-class demand.

By Depth Rating: Deep-Water Primacy Meets Shallow-Water Surge

Deep-water missions above 1,000 meters accounted for 66.3% of revenue in 2025, driven by ultra-deep hydrocarbon projects that rely on pressure-compensated electronics and advanced navigation. Shallow-water activity, however, is forecast to grow at a 14.4% CAGR as nearshore wind farms proliferate across the North Sea, Baltic, and East China Sea. Reach Subsea’s containerized Surveyor Interceptor enables rapid mobilization from crew-transfer vessels, aligning with developers’ desire for small-footprint assets.

Mid-water applications address continental shelf wind farms and mid-life oil platforms, requiring vehicles that combine high-definition video with moderate tooling. Deep-water systems are now integrating Sonardyne SPRINT-Nav inertial units delivering sub-meter accuracy without LBL arrays, enhancing efficiency where seafloor morphology obstructs transponders. Maintenance intervals are being depth-standardized under IOGP Guideline 373, requiring tighter service cycles for biofouling-prone shallow-water platforms.

By Propulsion System: Electric Supremacy, Hybrid Momentum

Electric propulsion commanded 80.5% of the offshore AUV and ROV market share in 2025 due to reduced topside weight and elimination of hydraulic fluid discharge. Hybrid propulsion, merging electric thrusters with on-demand hydraulic pumps, is slated for a 15.3% CAGR through 2031. Kongsberg’s Hugin AUV achieved a 72-hour mission in 2025 on pure electric power, underscoring endurance improvements.

TechnipFMC’s Schilling Robotics fleet demonstrates hybrid energy savings of 30%, using electric mode for transit and hydraulic surge only during torque operations. The U.S. Navy’s 2025 Unmanned Undersea Vehicle Master Plan specifies hybrid propulsion to balance stealth and manipulation capability. EU Marine Strategy Framework pressures operators to minimize underwater noise, favoring electric drives within marine-protected zones.

By Activity: IRM’s Dual Leadership In Share And Growth

Inspection, repair, and maintenance generated 31.7% of revenue in 2025 and is expected to continue leading with a 12.0% CAGR as more than 10,000 kilometers of pipelines installed before 2010 require integrity verification. Drilling and development remain strong, backed by FIDs in Brazil, Guyana, and Mozambique. Subsea 7’s USD 2.8 billion SURF backlog illustrates construction demand.

Decommissioning is gathering momentum in the North Sea as 2,000 wells must be plugged and abandoned by 2030 under UK-OGA estimates. Environmental monitoring, though the smallest, is expanding under EU spatial planning directives mandating real-time sediment monitoring during cable burial; ICES issued 2025 guidelines for AUV-based impact surveys. Operators increasingly bundle IRM with environmental monitoring to amortize mobilization costs.

By End-User Application: Hydrocarbon Anchor, Offshore Wind Upswing

Oil and gas accounted for 83.6% of revenue in 2025, driven by new production in Suriname, Namibia, and pre-salt Brazil. Offshore wind is poised to grow at a 20.8% CAGR, catalyzed by multi-gigawatt build-outs in Europe, China, and the United States. Defense applications are strengthening as AUKUS nations invest in seabed infrastructure protection and mine countermeasures, employing AI-enabled AUVs to patrol fiber-optic cables and gas pipelines.

Research institutions such as WHOI deploy AUVs for climate studies, while aquaculture operators in Norway leverage ROVs for net-pen inspections to limit fish mortality. Ørsted and Equinor have locked in multiyear ROV capacity via framework agreements, tightening supply and elevating day rates for inspection-class vehicles.

Geography Analysis

Middle East and Africa led with 36.1% of revenue in 2025 as Saudi Aramco’s Marjan expansion and Qatar Energy’s North Field East project required more than 80 work-class ROVs for subsea-tree installation and flowline monitoring. ADNOC’s USD 1.65 billion EPC contract awarded to Subsea 7 in 2025 underscores the region’s commitment to resident inspection drones for 200 kilometers of infrastructure. Nigeria’s Bonga Southwest field and South Africa’s Brulpadda prospect add further pull for deep-water ROVs, while Egypt’s Zohr gas continues to generate multiyear IRM demand. Political risk and energy-transition policies temper long-term upside, but near-term hydrocarbon spend remains strong.

Europe is forecast to post the fastest CAGR at 18.7% through 2031, driven by offshore wind expansion and North Sea decommissioning mandates. Dogger Bank’s final phase necessitates continuous cable integrity checks via scanning AUVs. Norway’s Hydrone-R resident drone reduces vessel days by 40 per year in harsh conditions. Denmark’s Kriegers Flak and Germany’s 7 GW Baltic auctions intensify demand for shallow-rated vehicles, while France’s floating-wind pilots require AUV-mediated mooring surveillance. OSPAR Commission rules stipulate structure removal within three years of production cessation, pushing rapid ROV mobilization for dismantling.

Asia-Pacific, South America, and North America share the remainder of the offshore AUV and ROV market. China installed 6.3 GW of offshore wind in 2025, deploying ROVs for dynamic cable burial in high-current zones. Japan’s floating-wind pilots off Goto rely on AUVs for typhoon-resilient mooring inspection. Brazil produced 2.9 million barrels per day from pre-salt assets, necessitating deep-water ROV support at depths beyond 2,000 meters. The U.S. Gulf of Mexico sustains ROV demand for mature assets, and the East Coast wind pipeline is triggering new inspection requirements. Canada initiated exploratory leasing in Atlantic provinces in 2025, laying the groundwork for future ROV deployments.

Competitive Landscape

The top five companies, Oceaneering International, TechnipFMC, Fugro, Subsea 7, and Saipem, command 55% of global revenue, reflecting moderate concentration. Integrated service models allow incumbents to bundle subsea construction, inspection, and decommissioning, capturing framework agreements that provide multiyear backlog visibility. TechnipFMC’s outcome-based contracts tie remuneration to uptime, aligning incentives with operators’ production goals.

Nauticus Robotics and Ocean Infinity exemplify disruptive entrants leveraging AI-enabled autonomy to reduce offshore personnel; Ocean Infinity’s USD 150 million Series C in 2024 highlights venture appetite. Strategic partnerships, such as Equinor and Saipem’s Hydrone-R co-development, share technology risk and accelerate commercialization. Kongsberg’s 2025 acquisition of Reach Subsea’s ROV division for USD 85 million consolidates Norway’s supply chain and broadens Kongsberg’s autonomous-system offering.

Regulatory compliance under IMCA R-014 (personnel competence) and R-004 (maintenance) remains a gatekeeper for contract awards, limiting new entrants without certification infrastructure. Technology differentiation centers on electric propulsion, AI-driven anomaly detection, and satellite connectivity for remote operations. Players reliant on hydraulic legacy systems face margin compression as environmental regulations penalize fluid leaks.

Offshore AUV And ROV Industry Leaders

Oceaneering International, Inc.

Fugro N.V

Subsea 7 SA

TechnipFMC PLC

DOF Subsea

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Helsing, a German defense technology firm, is in the process of acquiring Blue Ocean, an Australian company specializing in the design, development, and operation of autonomous underwater vehicles (AUVs).

- September 2025: Forssea Robotics, a French firm specializing in underwater robotics, has partnered with Deep Ocean Search (DOS), based in Mauritius, and its French counterpart, The Deep Company (TDC), to globally deploy survey-augmented remotely operated vehicle (ROV) services.

- August 2025: In a competitive tender, Oceaneering International, Inc.'s Brazilian arm, Marine Production Systems do Brasil LTDA (MPS), clinched multiple Subsea Robotics contracts from Petróleo Brasileiro S.A. (Petrobras) in Q2 2025.

- April 2025: RS Aqua has secured the role of the official distributor for the cutting-edge SRS Fusion hybrid ROV/AUV in the UK and Ireland. SRS (Strategic Robotic Systems), like RS Aqua, operates under the umbrella of General Ocean’s group.

Global Offshore AUV And ROV Market Report Scope

An autonomous underwater vehicle (AUV) is an unmanned underwater robot that can operate independently. Moreover, an AUV is programmed to perform tasks such as sample collation, survey, inspection, repair and maintenance, mapping, construction, decommissioning, marine research, and deep-sea mining.

A remotely operated vehicle (ROV) is an unoccupied robot, a highly maneuverable underwater machine attached to a series of cables that can explore ocean depths. These cables convey command and control signals between the operator and the ROV, allowing remote vehicle navigation.

The offshore AUV & ROV market is segmented by vehicle type, vehicle class, depth rating, propulsion, activity, end-user, and geography. By vehicle type, the market is segmented into remotely operated vehicles (ROVs) and autonomous underwater vehicles (AUVs). By vehicle class, the market is segmented into work-class and observatory-class vehicles. By depth rating, the market is segmented into shallow-water, mid-water, and deep-water vehicles. By propulsion, the market is segmented into electric, hydraulic, and hybrid systems. By activity, the market is segmented into drilling, construction, inspection, repair and maintenance (IRM), decommissioning, and monitoring. By end-user, the market is segmented into oil & gas, offshore wind, defense, research, and aquaculture. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report also covers the market sizes and forecasts for the offshore AUV & ROV market across major countries within each region. For all segments, market sizing and forecasts are provided on the basis of value (USD).

| ROV |

| AUV |

| Work-class | Light Work-class |

| Medium Work-class | |

| Heavy Work-class | |

| Observatory-class |

| Shallow (Up to 300 m) |

| Mid-water (300 to 1,000 m) |

| Deep-water (Above 1,000 m) |

| Electric |

| Hydraulic |

| Hybrid |

| Drilling and Development |

| Construction and Installation |

| Inspection, Repair and Maintenance (IRM) |

| Decommissioning |

| Environmental Monitoring |

| Oil and Gas |

| Offshore Wind |

| Defense and Security |

| Research and Academia |

| Aquaculture and Marine Infrastructure |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Norway | |

| Denmark | |

| Germany | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Vehicle Type | ROV | |

| AUV | ||

| By Vehicle Class | Work-class | Light Work-class |

| Medium Work-class | ||

| Heavy Work-class | ||

| Observatory-class | ||

| By Depth Rating | Shallow (Up to 300 m) | |

| Mid-water (300 to 1,000 m) | ||

| Deep-water (Above 1,000 m) | ||

| By Propulsion System | Electric | |

| Hydraulic | ||

| Hybrid | ||

| By Activity | Drilling and Development | |

| Construction and Installation | ||

| Inspection, Repair and Maintenance (IRM) | ||

| Decommissioning | ||

| Environmental Monitoring | ||

| By End-user Application | Oil and Gas | |

| Offshore Wind | ||

| Defense and Security | ||

| Research and Academia | ||

| Aquaculture and Marine Infrastructure | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Norway | ||

| Denmark | ||

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value for the offshore AUV and ROV market in 2031?

The market is expected to reach USD 6.78 billion by 2031.

Which vehicle type is growing fastest?

Autonomous underwater vehicles are forecast to expand at a 13.5% CAGR through 2031.

Why are hybrid propulsion systems gaining traction?

Hybrids blend electric efficiency with hydraulic torque, enabling longer missions while supporting high-power tooling.

Which region will post the highest growth?

Europe is projected to grow at an 18.7% CAGR, led by offshore wind build-outs and decommissioning mandates.

How are resident drones reducing costs?

Stationing ROVs and AUVs subsea eliminates dedicated support vessels, trimming intervention expenses by up to 40%.

Page last updated on: