Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

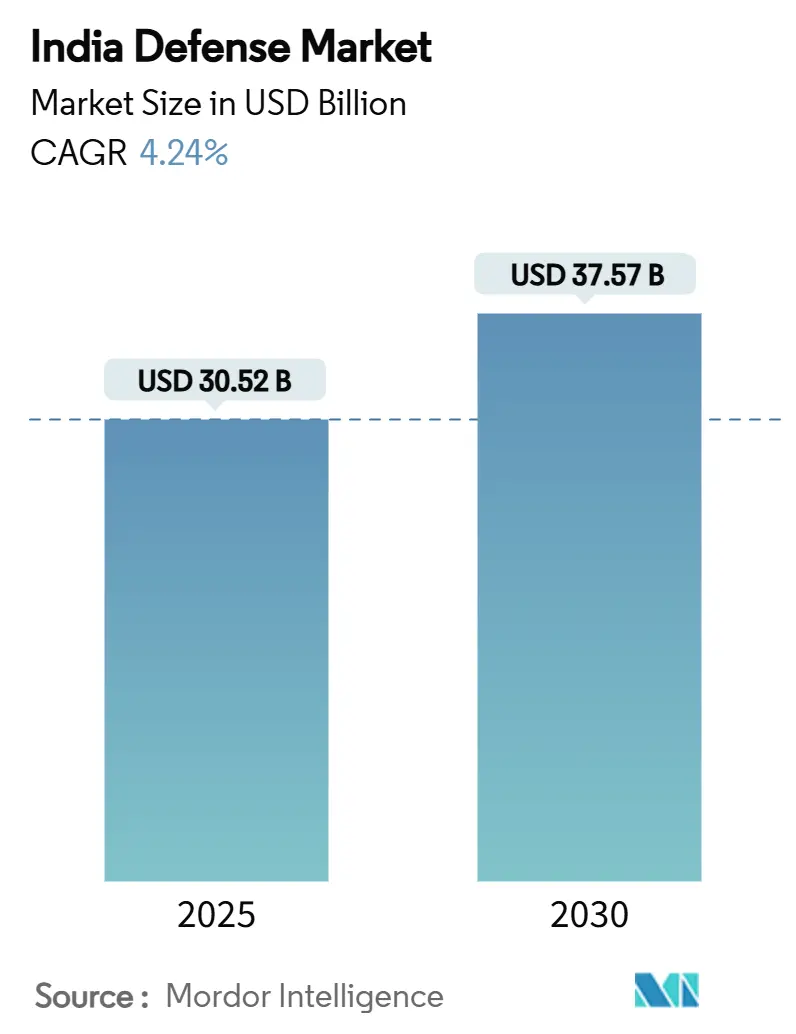

| Market Size (2025) | USD 30.52 Billion |

| Market Size (2030) | USD 37.57 Billion |

| Growth Rate (2025 - 2030) | 4.24% CAGR |

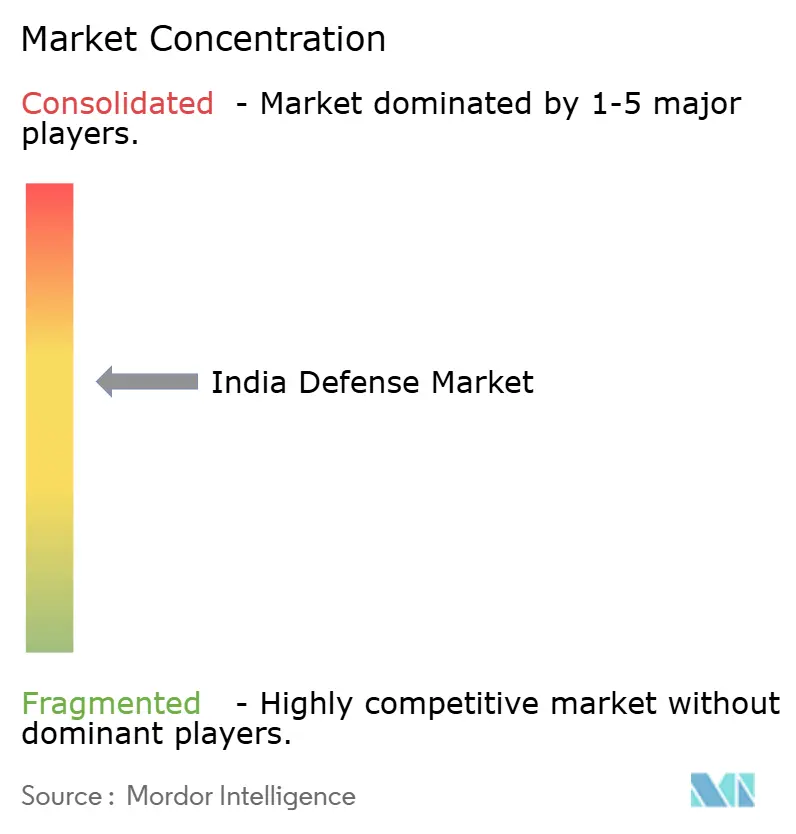

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Defense Market Analysis by Mordor Intelligence

The India defense market is valued at USD 30.52 billion in 2025 and is forecasted to reach a market size of USD 37.57 billion by 2030, expanding at a 4.24% CAGR. Robust funding, a 75% domestic-procurement mandate, and steady private-sector entry fuel the market’s measured growth. Rising border tensions with China and Pakistan are accelerating near-term acquisitions, while the 2025 “Year of Reforms” program prioritizes integrated modernization across land, sea, air, cyber, and space domains. Record-high domestic production in FY 2024 underscores how localization policies reshape supply chains. At the same time, export successes such as BrahMos missile deals highlight India’s emergence as a technology provider in the wider Indo-Pacific region.

Key Report Takeaways

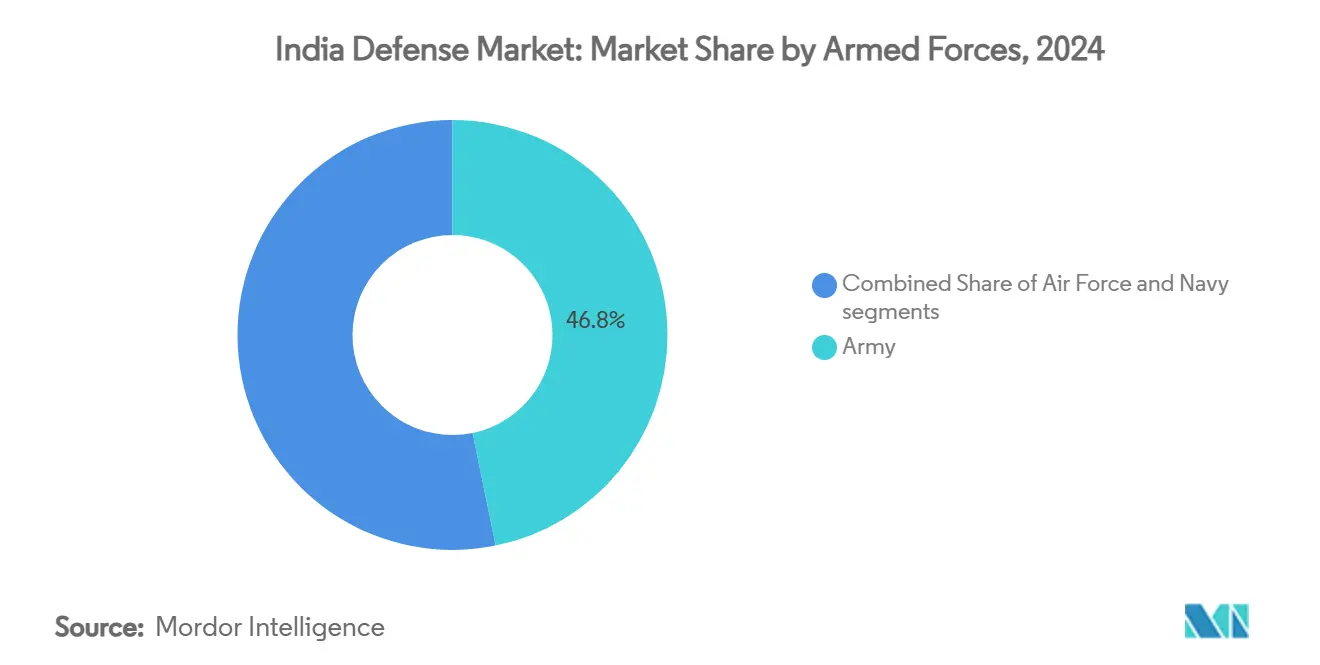

- By armed forces, the Army held 46.78% of the India defense market share in 2024, whereas the Navy is projected to post the fastest 5.26% CAGR to 2030.

- By type, vehicles led with 28.76% revenue share in 2024; unmanned systems are expected to expand at a 7.35% CAGR through 2030.

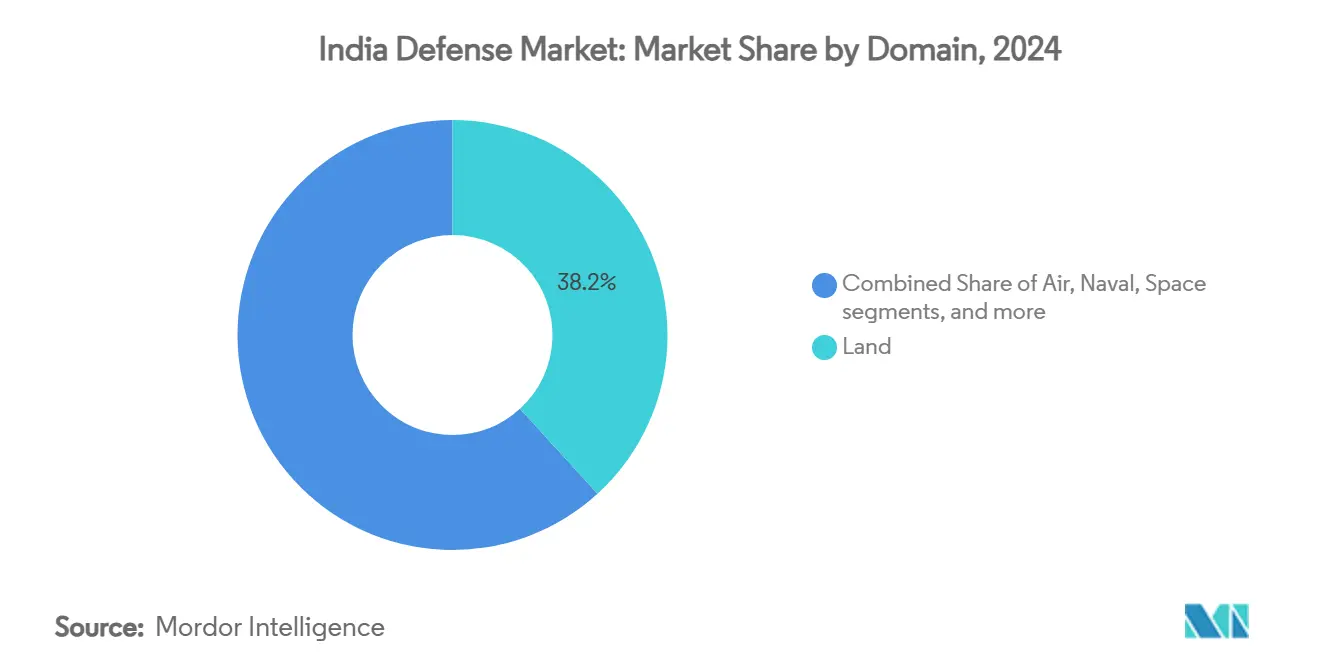

- By domain, land operations accounted for 38.22% of the India defense market size in 2024, while cyber and electromagnetic spectrum operations are advancing at a 6.76% CAGR to 2030.

- By procurement nature, indigenous production commanded 61.10% of the India defense market size in 2024 and is forecasted to grow at a 5.10% CAGR to 2030.

- HAL, BEL, and MDL are together ranked among the top 100 global arms firms, yet they capture only 1% of global arms sales, signalling ample headroom for scale-up.

India Defense Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding defense budget and localization drive | +1.2% | National; defense corridors | Medium term (2-4 years) |

| Accelerated investment in AI-enabled combat and autonomous swarm technologies | +0.8% | Bengaluru, Hyderabad, Pune R&D hubs | Long term (≥ 4 years) |

| Escalating geopolitical tensions along the borders | +1.1% | LAC and LoC regions | Short term (≤ 2 years) |

| Emergence of dual-use space assets driving C4ISR capability demand | +0.6% | National; space command integration | Long term (≥ 4 years) |

| Increased private sector participation enabled by liberalized FDI policies | +0.7% | UP and Tamil Nadu defense corridors | Medium term (2-4 years) |

| Structural modernization of the Army, Navy, and Air Force | +0.9% | National; integrated theatre planning | Medium term (2-4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Expanding Defense Budget and Localization Drive

The FY 2025-26 Union Budget allocates INR 6.81 trillion (USD 78.7 billion) to defense, a 9.5% rise over the previous year. Three-quarters of the modernization outlay is ring-fenced for domestic sourcing, pressing global OEMs to partner locally or cede market access. DRDO’s INR 26,816.82 crore (USD 3.13 billion) research budget backs 100 priority projects, while 509 import-prohibited items anchor captive demand for Indian suppliers. Although capital spending hit INR 1.8 trillion (USD 21 billion), defense still absorbs only 1.9% of GDP, prompting innovative financing such as a proposed non-lapsable modernization fund. Together, these measures widen the addressable Indian defense market for homegrown firms and nudge foreign players toward deeper technology transfer.

Accelerated Investment in AI-Enabled Combat and Autonomous Swarm Technologies

The Defence Artificial Intelligence Project Agency receives USD 12 million annually to prototype cognitive radar and autonomous swarms.[1]Defence Research & Development Organisation, “Budget Highlights 2025-26,” drdo.gov.in Exercises such as Dakshin Shakti showcased human-in-the-loop swarms that align with India’s doctrinal emphasis on operator oversight. Startup engagement via the iDEX program has onboarded 194 firms, shortening innovation cycles and easing entry barriers. However, limited access to high-end semiconductors—constrained by US export controls—creates a technology gap that India’s USD 10 billion Semiconductor Mission seeks to close. The ability to indigenize chips will ultimately determine whether AI capabilities migrate from demonstrations to line units, shaping the long-run trajectory of the Indian defense market.

Escalating Geopolitical Tensions Along the Borders

The October 2024 India-China standoff resolution did not curb modernization; both sides acknowledged deterrence deficiencies. Operation Sindoor in May 2025 neutralized 600 hostile drones, validating indigenous S-400 and Akash systems under live combat conditions.[2]Press Information Bureau, “Operation Sindoor Factsheet,” pib.gov.in Border-roads spending rose 9.74% to INR 7,146.50 crore (USD 835.9 million), linking forward posts to civilian infrastructure. INS Vikrant’s deployment during Pakistan tensions signalled a maritime deterrent posture, and the S-400 Sudarshan Chakra battery deterred Pakistani F-16 repositioning. Such episodes accelerate short-cycle procurements, particularly for air-defense, drone-countermeasure, and high-altitude platforms, lifting near-term demand across the Indian defense market.

Emergence of Dual-Use Space Assets Driving C4ISR Capability Demand

The Defence Space Agency plans a 52-satellite constellation, awarding 31 satellites to private firms. SPADEX’s successful on-orbit rendezvous demonstrated capabilities critical for future anti-satellite operations. An INR 25,000 crore (USD 2.92 billion) allocation through 2030 underwrites satellite communications, early-warning payloads, and secure data links. Tamil Nadu’s planned 2,000-acre space park exemplifies the civil-military industrial nexus. Yet China’s advanced antisatellite tools amplify urgency; closing this gap will require sustained funding and reforms that keep C4ISR programs on schedule.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vulnerabilities in critical alloy and semiconductor supply chains | -0.9% | National; high-tech systems | Short term (≤ 2 years) |

| Inefficient and bureaucratic defense procurement framework | -1.1% | National; all procurement categories | Medium term (2-4 years) |

| Cybersecurity breaches and IP theft are hindering indigenous R&D progress | -0.7% | National, with concentration in R&D hubs and defense corridors | Medium term (2-4 years) |

| High pension and salary expenditures limiting capital investment | -0.8% | National, affecting all three services uniformly | Long term (≥ 4 years) |

Source: Mordor Intelligence

Vulnerabilities in Critical Alloy and Semiconductor Supply Chains

India imports 82% of lithium and 76% of silicon from China, risking production delays for precision weapons and avionics. Semiconductor shortages postponed Tejas Mk-1A deliveries by eight months, exposing cascading effects on downstream programs. The National Critical Mineral Mission earmarks INR 16,000 crore (USD 1.87 billion) to secure 50 overseas mines, yet geopolitical frictions could restrict access. Tata Electronics’ fab, expected online in 2026, will narrow but not eliminate short-term supply gaps. Dual-sourcing and the India-US TRUST initiative offer mitigation, but ITAR curbs limit technology depth, tempering growth across the Indian defense market.

Inefficient and Bureaucratic Defense Procurement Framework

Complex acquisition procedures add 3-5 years to average procurement cycles, as illustrated by Apache helicopter delays that left Army squadrons non-operational for 15 months. The “Bofors syndrome” sustains risk-averse behavior that prizes paperwork over readiness. Despite successful indigenous trials, only 8% of the planned 2,800 artillery guns have been inducted. Repeated rifle tender cancellations underscore systemic issues undermining Make-in-India goals. 2025’s “Year of Reforms” intends to streamline the Defense Acquisition Procedure, but entrenched processes remain the stiffest drag on the Indian defense market.

Segment Analysis

By Armed Forces: Army Dominance Amid Naval Acceleration

The Army commanded 46.78% of the Indian defense market in 2024, a position earned through extensive modernization needs across 6,811 km of disputed borders. Yet the Navy’s 5.26% forecast CAGR signals growing maritime focus as India asserts Indo-Pacific influence. INS Vikrant, INS Surat, and INS Vaghsheer entered service in 2025 with 75% indigenous content, underlining local shipbuilding maturity. Project 75I’s INR 43,000 crore (USD 5.02 billion) AIP-enabled submarine program further elevates naval technological complexity.[3]Indian Navy, “Project 75I Overview,” navy.gov.in

The Air Force, hampered by a 31-squadron fleet versus an authorized 42, sees slower budget traction despite urgent requirements. HAL’s AMCA program—a joint venture with four private firms—marks a pivot toward collaborative high-technology development. Concurrently, the Navy’s Sprint initiative aims to field 75 new Indigenous technologies each year, outpacing peer services in R&D intensity. Upcoming Integrated Theatre Commands could realign resource flows, but the Army’s land-centric imperatives will remain the anchor of the Indian defense market.

Note: Segment shares of all individual segments available upon report purchase

By Type: Vehicle Supremacy Challenged by Unmanned Revolution

Vehicles held 28.76% of 2024 revenue as the Indian defense market size favored platforms such as main battle tanks, artillery carriers, and transport aircraft. High-altitude demands prompted the Zorawar light tank program tailored for Ladakh terrains. However, unmanned systems are set to outpace all other categories at a 7.35% CAGR. Recent military operations show that AI-enabled swarm drones proved cost-effective force multiplication, and the domestic drone market could reach USD 11 billion by 2030.

Training and protection systems are scaling alongside the Agnipath tour-of-duty model, which demands accelerated skill pipelines. C4ISR and electronic warfare (EW) suites gain prominence as multi-domain operations require unified situational awareness. Smart munitions and domestically produced ammunition address supply security as imports taper. Backed by dedicated doctrine, emerging space and cyber procurements compel legacy contractors to diversify portfolios or risk obsolescence in the evolving Indian defense market.

By Domain: Land Dominance Amid Cyber Emergence

Land operations represent 38.22% of the 2024 India defense market size, reflecting persistent continental threats. Yet cyber and electromagnetic spectrum operations are the fastest-growing, tracking a 6.76% CAGR. Establishment of Command Cyber Operations Wings and a Joint Doctrine signals institutional prioritization of offensive cyber capabilities.

Air modernization focuses on multi-role fighters integrating indigenous missiles such as Astra, while naval expansion hinges on blue-water platforms like Vikrant to secure sea lanes. Space militarization accelerates through the 52-satellite constellation, integrating private industry into defense orbit. AI’s diffusion across every domain blurs traditional boundaries, pointing toward a future when the idea of separate domains diminishes within the Indian defense market.

Note: Segment shares of all individual segments available upon report purchase

By Procurement Nature: Indigenous Ascendancy

Indigenous production captured 61.10% of the Indian defense market in 2024 and is forecast to climb at a 5.10% CAGR. The 75% domestic-sourcing mandate locks in volumes for local firms and exposes capability gaps in semiconductors and special alloys. Foreign procurement’s relative decline masks its criticality for fifth-generation fighters and advanced sensors, where local skills remain nascent.

Russia’s offer of Su-57E source-code access contrasts with France’s guarded Rafale codes, illustrating how geopolitical dynamics drive technology transfer depth. BrahMos’ journey from joint venture to 83% indigenous content shows a viable pathway to sovereignty. Defense corridors in Uttar Pradesh and Tamil Nadu cluster suppliers, cutting logistics costs and fostering economies of scale that strengthen the Indian defense market.

Geography Analysis

Regional threat vectors and industrial ecosystems shape defense spending patterns across India. Northern and eastern frontier states command outsized allocations for high-altitude warfare gear, from lightweight howitzers to specialized snowmobility vehicles. The deployment of Zorawar light tanks in Ladakh typifies border-driven procurement requirements. Concurrently, INR 6,500 crore (USD 760.3 million) in border-roads upgrades bolster logistics and civilian access, underscoring defense’s dual-use dividends.

Coastal regions are experiencing intensified naval asset activity. INS Vikrant’s Arabian Sea patrols during Pakistan tensions highlight western seaboard relevance, while the Bay of Bengal hosts anti-submarine exercises that integrate P-8I and MH-60R platforms. Shipyards such as Mazagon Dock and Goa Shipyard anchor localized supply chains, ensuring timely refit cycles and spares availability.

Defense Industrial Corridors concentrate manufacturing prowess. Uttar Pradesh has secured INR 28,475 crore (USD 3.33 billion) of commitments from 169 firms, turning the Lucknow-Kanpur belt into a missile-production hub. Tamil Nadu leverages its aerospace heritage, attracting electronics majors that feed civil and defense avionics. Telangana’s incentive programs have lured Vem Technologies and other mid-tier suppliers, diversifying geographic risk. This distributed industrial footprint enhances resilience in the Indian defense market and shortens delivery timelines for frontline units.

Competitive Landscape

Competition is evolving from PSU-centric to ecosystem-centric models. Hindustan Aeronautics Limited (HAL), Bharat Electronics Ltd., and Mazagon Dock Shipbuilders Limited (MDL) remain dominant, yet their combined global arms-sales share is only 1%, offering ample runway for growth. HAL’s invitation to four private partners in the AMCA jet exemplifies a partnership template breaking the monopoly mold. Tata Advanced Systems, Adani Defence, and L&T Defense leverage scale, balance-sheet depth, and global tie-ups to outbid PSUs on agility and cost.

Technology transfer has become the prime differentiator; Russia’s willingness to share Su-57E source code signals strategic alignment, whereas France’s limited Rafale access underscores commercial caution. Niche firms such as Data Patterns and Paras Defence exploit gaps in counter-drone and electronic-warfare niches, aligning with the market’s shift toward specialized, high-velocity solutions. Export momentum—USD 1.5 billion in BrahMos sales across Southeast Asia—confirms India’s graduation from captive domestic supplier to credible global competitor, fortifying its stature in the Indian defense market.

India Defense Industry Leaders

-

Hindustan Aeronautics Limited (HAL)

-

Bharat Electronics Ltd.

-

Defence Research & Development Organisation (DRDO)

-

Tata Advanced Systems Limited (Tata Group)

-

Larsen & Toubro Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: The Indian Ministry of Defence signed two contracts with Hindustan Aeronautics Limited (HAL) to procure 156 Light Combat Helicopters (LCH), Prachand, including training and associated equipment. The contracts comprise 66 LCHs for the Indian Air Force (IAF) and 90 LCHs for the Indian Army.

- March 2025: The Indian Ministry of Defence signed two contracts valued at INR 6,900 crore (USD 807.09 million) with Bharat Forge Limited and Tata Advanced Systems Limited for the procurement of 155mm/52 calibre Advanced Towed Artillery Gun Systems (ATAGS) and High Mobility 6x6 Gun Towing Vehicles.

- March 2025: The Union Ministry of Defence (MoD) signed contracts valued at INR 2,500 crore (USD 292.4 million) to procure the tracked version of the Nag Anti-Tank Missile System (NAMIS) for the Indian Army's mechanized formations. The ministry also finalized a contract with Force Motors Limited and Mahindra & Mahindra Limited to supply approximately 5,000 light vehicles for the Armed Forces.

India Defense Market Report Scope

The Indian defense market covers all aspects of the military vehicle, armament, other equipment procurements, and upgrade and modernization plans. The report also provides insights into the budget allocation and spending of the country in the past, present, and forecast periods.

The Indian defense market is segmented by armed forces and type. Armed forces segment the market into the army, navy, and air force. By type, the market is classified into fixed-wing aircraft, rotorcraft, ground vehicles, naval vessels, C4ISR, weapons and ammunition, protection and training equipment, and unmanned systems. The report also covers the market sizes and forecasts for the Indian defense market. The market size is provided for each segment in terms of value (USD).

| By Armed Forces | Air Force |

| Army | |

| Navy | |

| By Type | Personnel Training and Protection |

| C4ISR and Electronic Warfare | |

| Vehicles | |

| Weapons and Ammunition | |

| Unmanned Systems | |

| Space and Cyber Systems | |

| By Domain | Land |

| Air | |

| Naval | |

| Space | |

| Cyber and Electromagnetic Spectrum | |

| By Procurement Nature | Indigenous Production |

| Foreign Procurement |

By Armed Forces

| Air Force |

| Army |

| Navy |

By Type

| Personnel Training and Protection |

| C4ISR and Electronic Warfare |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

By Domain

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

By Procurement Nature

| Indigenous Production |

| Foreign Procurement |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the India defense market?

The India defense market stands at USD 30.52 billion in 2025 and is projected to reach USD 37.57 billion by 2030, expanding at a 4.24% CAGR.

Which armed service is growing the fastest?

The Navy is the fastest-expanding service, expected to post a 5.26% CAGR through 2030 on the back of blue-water capability investments.

How much of India’s defense procurement is sourced domestically?

Indigenous production accounts for 61.10% of total procurement value and is backed by a 75% domestic-sourcing mandate for modernization funds.

Why are unmanned systems important to India’s defense modernization?

AI-enabled drones proved their effectiveness during various military operations and are forecast to grow at a 7.35% CAGR, offering cost-efficient force multiplication.

What are the main supply-chain risks facing Indian defense manufacturers?

Heavy dependence on Chinese lithium and silicon, coupled with semiconductor shortages, poses critical vulnerabilities that the National Critical Mineral Mission aims to offset.

How is India leveraging space assets for defense?

A 52-satellite constellation managed by the Defence Space Agency will strengthen C4ISR capabilities, with 31 satellites being built by private partners under a INR 25,000 (USD 2.92 billion) crore program

Page last updated on: July 3, 2025