Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 5.20 Billion |

| Market Size (2030) | USD 6.5 Billion |

| Growth Rate (2025 - 2030) | 4.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Life And Non-Life Insurance Market Analysis by Mordor Intelligence

The Czech Republic Life and Non-Life Insurance Market size is USD 5.20 billion in 2025 and is projected to reach USD 6.5 billion by 2030, reflecting a 4.6% CAGR over the period. Premium expansion in non-life lines, rapid digitization of distribution, and climate-driven repricing of property risks are reshaping industry economics. Mandatory motor third-party liability (TPL) coverage continues to anchor written premiums even as telematics and usage-based models tilt competition toward risk-based pricing. Construction-cost inflation is driving quarterly indexation of property sums insured, while green-transition liability and cyber coverages gain traction as small and medium enterprises respond to new EU regulations. Profitability, however, remains squeezed by intense price competition in the motor business and a prolonged low-rate environment that narrows guaranteed-rate spreads in life portfolios. Carriers are therefore doubling down on AI-driven underwriting, bancassurance APIs, and parametric products to protect margins and close protection gaps.

Key Report Takeaways

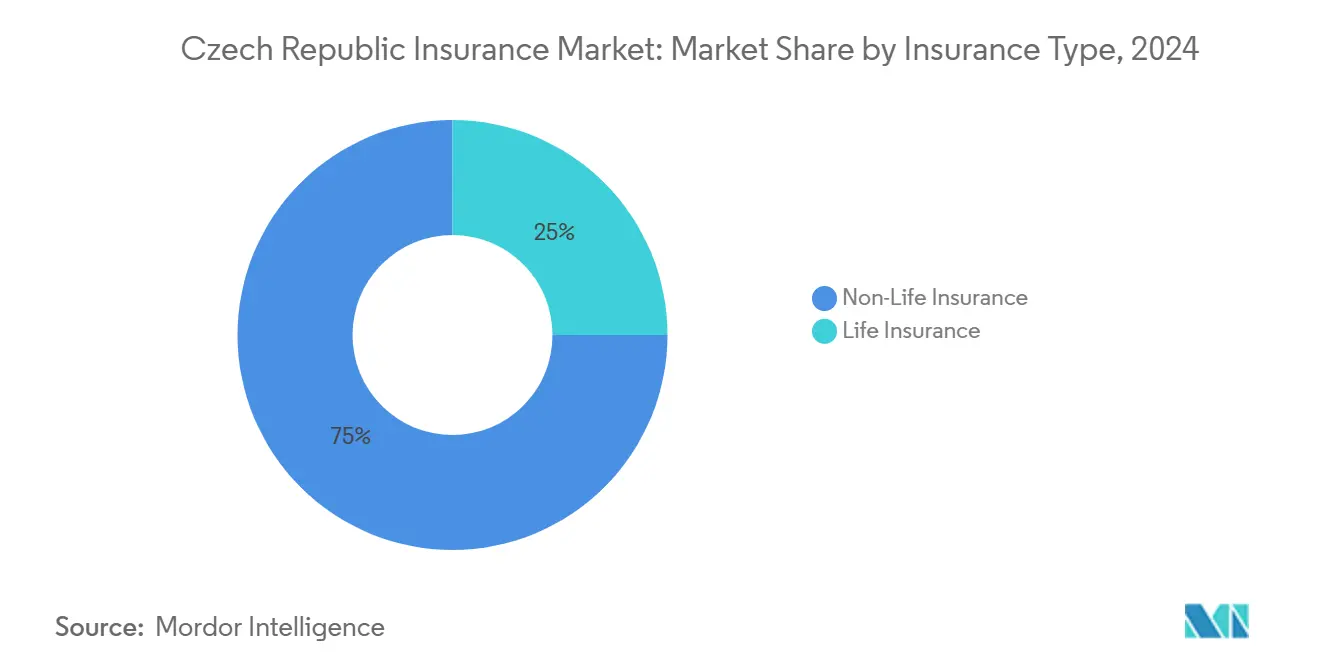

- By insurance type, non-life led with a 75% revenue share in 2024 and is projected to advance at a 5.5% CAGR through 2030.

- By distribution channel, agency networks held a 42% share in 2024, while online and digital-direct methods are forecast to post a 7.34% CAGR through 2030.

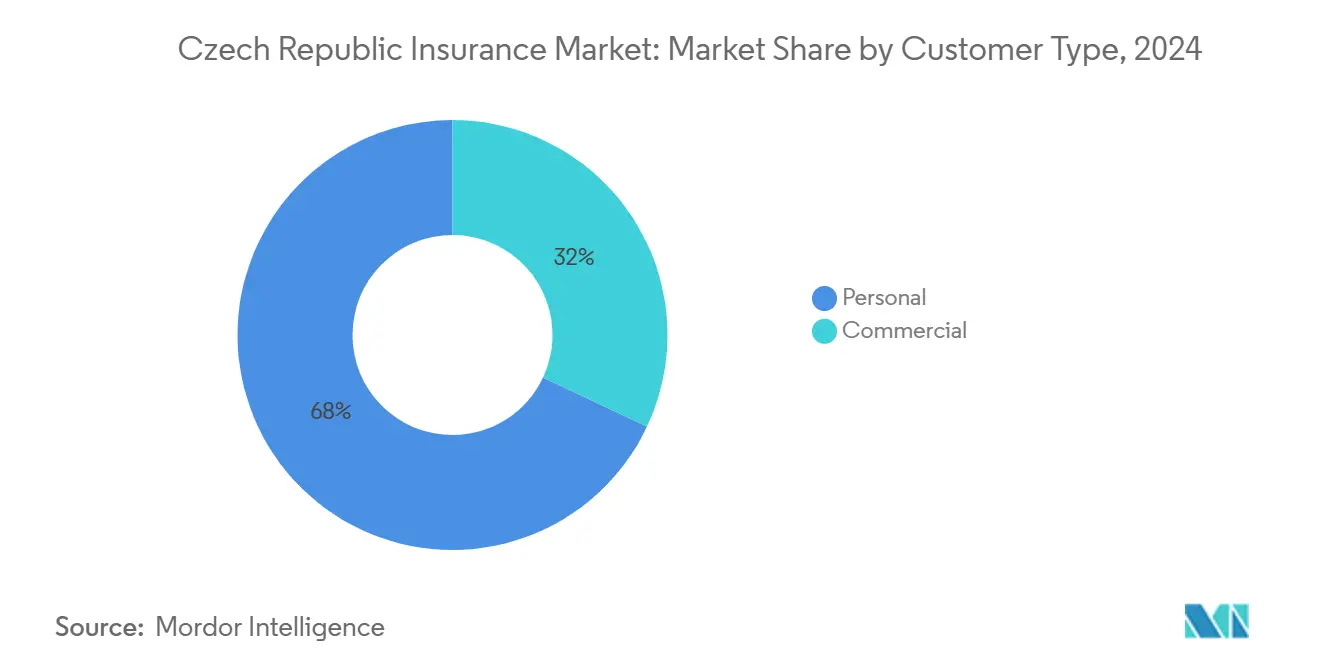

- By customer type, personal lines accounted for 68% of 2024 premiums, whereas commercial coverages are expected to grow at a 6.2% CAGR to 2030.

Czech Republic Life And Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory motor TPL coverage and rising vehicle registrations | +0.80% | Prague, Brno, Ostrava corridors | Short term (≤ 2 years) |

| Indexation of property sums insured amid construction-cost inflation | +1.20% | Nationwide, highest in Prague and South Moravia | Medium term (2-4 years) |

| Aging population boosting demand for life and pension savings | +0.90% | Rural districts with median age > 45 years | Long term (≥ 4 years) |

| Digital bancassurance APIs unlocking under-insured retail segments | +0.70% | Smartphone-dense urban areas | Medium term (2-4 years) |

| EU sustainable-finance rules spurring green product launches | +0.50% | National, aligned with EU timelines | Long term (≥ 4 years) |

| AI-driven micro segmentation enabling motor usage-based pricing | +0.60% | Competitive urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Motor TPL Coverage and Rising Vehicle Registrations

Act No. 30/2024 removed the paper green card yet imposed a 15-day claims-settlement deadline, compelling insurers to upgrade automation and analytics [1]Czech National Bank, “Financial Stability Report Autumn 2024,” cnb.cz. Passenger-vehicle registrations rose 3.2% year-on-year in Q3 2024 on the back of EV incentives worth EUR 200 million. Generali Česká pojišťovna’s computer-vision app now settles 70% of minor collision claims without a human adjuster, cutting cycle time to four days. Škoda Auto’s embedded telematics funnels real-time data to partner insurers, unlocking 15-20% premium discounts for low-mileage drivers. Fraud risk is edging up, with detected cases valued at CZK 1.754 billion in 2024, a 12% rise from 2023.

Indexation of Property Sums Insured Amid Construction-Cost Inflation

Steel and cement input costs jumped 18.6% year-on-year in Q1 2025 as EU CBAM tariffs hit imports, forcing quarterly indexation of building values. Storm Boris in September 2024 caused CZK 17 billion in insured losses and widened the national protection gap to 66%. Reinsurers responded by lifting catastrophe treaty rates 25-30% at 2025 renewals [2]Guy Carpenter, “Storm Boris Post-Event Analysis,” guycarp.com. Kooperativa’s parametric flood cover pays within 48 hours when river gauges breach set thresholds, bypassing adjuster disputes. The CNB now tags underinsurance in property lines as a systemic risk because only 42% of homes carry full building insurance.

Aging Population Boosting Demand for Life and Pension Savings Vehicles

Median age reached 43.9 years in 2024, and the 65+ cohort will climb to 24.3% of the population by 2030. Life GWP rose 6.6% to CZK 57.7 billion in 2024, yet falling policy rates squeezed spreads to 130-230 basis points. The CNB will cap unit-linked commissions at 2.5% of annual premium for the first five years from 2025, disrupting bancassurance economics. NN and MetLife are piloting hybrid products combining a 0.5-1.0% guarantee with equity upside. Higher tax-deductible ceilings will unlock a CZK 6 billion addressable pool for pension savings by 2027.

Digital Bancassurance APIs Unlocking Under-Insured Retail Segments

ČSOB Pojišťovna’s Guidewire deployment slashed onboarding to 15 minutes inside Komerční banka’s app. Kooperativa’s George ecosystem posts a 34% attach rate for micro policies among 25-40-year-olds. Acquisition costs drop 40-50% when API distribution replaces agency commissions. EIOPA, meanwhile, flags 30-70% commissions on mortgage credit protection as a consumer risk, prompting the upcoming cap. Generali responded by launching a no-commission direct platform for tech-savvy millennials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense price competition compressing average premium rates | -0.90% | Motor TPL and household lines | Short term (≤ 2 years) |

| Persistently low guaranteed-rate spreads eroding life profitability | -0.70% | All life carriers | Medium term (2-4 years) |

| Severe weather events driving claims volatility and reinsurance costs | -1.10% | Flood-prone Moravia and Bohemia | Short term (≤ 2 years) |

| 2025 cap on unit-linked commissions curbing distributor incentives | -0.50% | Bancassurance and agent channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition Compressing Average Premium Rates

Average motor TPL premiums fell 3-4% in 2024 even as claims frequency inched higher, pushing the line’s combined ratio to 98.2%. Online aggregators cut switching friction to under 10 minutes, eroding loyalty and lifting acquisition costs above CZK 1,500 per motor policy. Generali saw a 2.8% average-premium decline in 2024 and tightened underwriting filters for high-risk postcodes. VIG trimmed combined ratios two points through telematics-driven selection but warns competition will stay fierce through 2026. The CNB cautions that persistent discounting could threaten solvency if another catastrophe mirrors Storm Boris within 24 months.

Persistently Low Guaranteed-Rate Spreads Eroding Life Profitability

Repo cuts from 7.00% to 4.00% during 2024 narrowed the spread between 10-year bonds and policy guarantees to barely 130-230 basis points. Life sector pre-tax profit slipped 6.9% despite premium growth, as investment yields lagged. Carriers trimmed new guarantees to 0.5-1.0% and shifted toward unit-linked structures, but the 2025 commission cap will slice new-business margins by 200-300 basis points [3]European Insurance and Occupational Pensions Authority, “Supervisory Convergence Report 2024,” eiopa.europa.eu. ECB guidance implies muted bond yields through 2027, limiting reinvestment upside [4]European Central Bank, “Monetary Policy Outlook 2025-2027,” ecb.europa.eu. Alternative assets offer yield pickup, yet Solvency rules restrict non-investment-grade holdings to 10% of technical provisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Non-Life Momentum Underpinned by Motor and Property

Non-life business generated 75% of 2024 premiums, and that dominance is poised to continue thanks to mandatory TPL, quarterly property-value indexation, and growing catastrophe awareness. Motor products provide close to half of non-life revenue, and the Czech Republic insurance market share for telematics-enabled policies has already passed 15% in Prague and Brno. Property lines, roughly 28% of non-life, track the construction-price index and are seeing sums insured raised each quarter to avoid undercoverage. Liability, accident, and health account for the remaining share, with cyber riding a regulatory tailwind from DORA.

Life insurance, at 25% of total written premiums, is expanding more slowly as guaranteed-rate business recedes. Unit-linked demand is rising despite the upcoming commission cap. Carriers are also nurturing longevity-indexed annuities that shift mortality risk to the capital markets. As spreads stay narrow, the Czech Republic insurance market size for life products is increasingly driven by asset-management components rather than pure risk covers.

By Distribution Channel: Digital Direct Gains Scale

Agency networks still place 42% of total GWP, especially in rural regions where smartphone penetration is lower. Yet the Czech Republic insurance market is tilting toward mobile and API-based distribution. Digital-direct premiums are poised for a 7.34% CAGR through 2030 as carriers embed policy journeys in banking apps and e-commerce checkouts. Direct pojišťovna’s pay-per-kilometer model and Kooperativa’s George ecosystem show how acquisition costs can fall by roughly half when intermediaries are bypassed.

Bancassurance commands 28% of written premiums, with high exposure to life and credit-related covers. The forthcoming commission ceiling will likely temper that channel’s growth. Brokers maintain about a 30% share, specializing in commercial and specialty risks where advisory content is valued. Hybrid models blending robo-advice, human chats, and pay-as-you-go commissions are emerging in response to regulatory pressure.

By Customer Type: Commercial Demand Accelerates Under ESG and Cyber Mandates

Personal lines contribute 68% of total premiums, powered by motor, home, and traditional life protection. Nevertheless, commercial lines are picking up speed, forecast at 6.2% CAGR through 2030 as companies insure against green-transition liabilities and digital-operations outages. The Czech Republic insurance market size for cyber cover is still modest, but it is growing at double-digit rates as DORA testing rules go live in 2025. Parametric business-interruption products and directors’ and officers’ liability are also expanding as SMEs professionalize risk management. Trade-credit insurance remains underpenetrated but may gain as exporters diversify beyond the EU.

Geography Analysis

Prague and Central Bohemia generated 38% of premiums in 2024 on the back of higher vehicle and property values. Storm Boris, however, demonstrated that Moravian-Silesian and Olomouc regions bear outsized catastrophe exposure, accounting for half of the national insured losses. South Moravia contributes 14% of commercial premiums thanks to the Brno manufacturing cluster. Digital uptake is sharply regional: smartphone penetration exceeds 78% in Prague and Brno, allowing digital-direct to scale quickly, while rural Vysočina and Karlovy Vary rely on agency sales. Property insurance penetration trails urban centers by 18 percentage points in these districts, creating a protection gap.

Cross-border mobility is rising now that paper green cards are gone. The Czech Republic insurance market processes cross-border motor claims 30% faster, an efficiency gain that supports traveler confidence. Still, AI underwriting rules require bias testing to ensure driver scoring does not discriminate in border regions. Generali reports cross-border claims rose to 6.2% of motor totals in 2024, reflecting revived tourism and simplified EU procedures.

Competitive Landscape

The Czech Republic insurance market features a moderate concentration: VIG subsidiaries Kooperativa and ČPP, together with Generali and Allianz, hold roughly a 73% share. VIG’s Czech operations deliver 22% of group profit, signaling deep parent commitment to telematics and bancassurance investment. Generali’s 23.2% share benefits from life leadership, yet motor margins are thinning under price pressure. Allianz, UNIQA, ČSOB Pojišťovna, and digital-native Direct pojišťovna compete on user experience, UBI pricing, and niche innovation. Smaller disrupters like Pillow pojišťovna focus on short-term-rental property, while Maxima covers agriculture and forestry.

Green-transition liability, cyber, and parametric weather products represent the clearest white spaces. Guidewire-enabled real-time issuance positions ČSOB Pojišťovna to go after gig-economy and microbusiness segments. Regulatory requirements for algorithm documentation create a moat that favors carriers with robust data-science teams. Those lacking actuarial depth may face higher compliance expenses or fall behind in advanced pricing.

Czech Republic Life And Non-Life Insurance Industry Leaders

Kooperativa pojišťovna (VIG Group)

Česká podnikatelská pojišťovna (ČPP, VIG)

Generali Česká pojišťovna

Allianz pojišťovna

UNIQA pojišťovna

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Generali Česká pojišťovna merged ČP INVEST asset management, bringing EUR 4.2 billion under one roof for cross-selling of unit-linked life products.

- November 2024: Zuzana Silberová of CNB elected EIOPA Vice-Chair for a five-year term, boosting Czech influence over EU prudential rules.

- September 2024: Storm Boris caused CZK 17 billion in insured losses, raising 2025 catastrophe reinsurance pricing by 25-30%.

- June 2024: ČSOB Pojišťovna adopted Guidewire InsuranceSuite, cutting policy-issuance time to 15 minutes.

Czech Republic Life And Non-Life Insurance Market Report Scope

By Insurance Type

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Property Insurance | |

| Liability Insurance | |

| Health Insurance | |

| Travel Insurance |

By Distribution Channel

| Individual Agency |

| Bancassurance |

| Online / Digital Direct |

| Brokers & Affinity |

By Customer Type

| Personal |

| Commercial |

| By Insurance Type | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Property Insurance | ||

| Liability Insurance | ||

| Health Insurance | ||

| Travel Insurance | ||

| By Distribution Channel | Individual Agency | |

| Bancassurance | ||

| Online / Digital Direct | ||

| Brokers & Affinity | ||

| By Customer Type | Personal | |

| Commercial | ||

Key Questions Answered in the Report

What is the projected value of the Czech Republic insurance market in 2030?

It is forecast to reach USD 6.5 billion by 2030, growing at a 4.6% CAGR.

Which segment leads premium generation?

Non-life lines, driven by motor and property, hold 75% of written premiums.

How fast are digital-direct channels expanding?

Online and digital-direct distribution is projected to post a 7.34% CAGR through 2030.

What impact did Storm Boris have on reinsurance costs?

The event lifted catastrophe treaty pricing for 2025 renewals by 25-30%.

How will the 2025 commission cap affect bancassurance?

It limits unit-linked commissions to 2.5% of annual premium, reducing distributor incentives and pushing carriers toward fee-based or digital channels.

Which emerging product areas offer growth potential?

Cyber insurance, parametric flood cover, and green-building policies hold the strongest upside under new EU regulations.

Page last updated on: