South America Physical Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

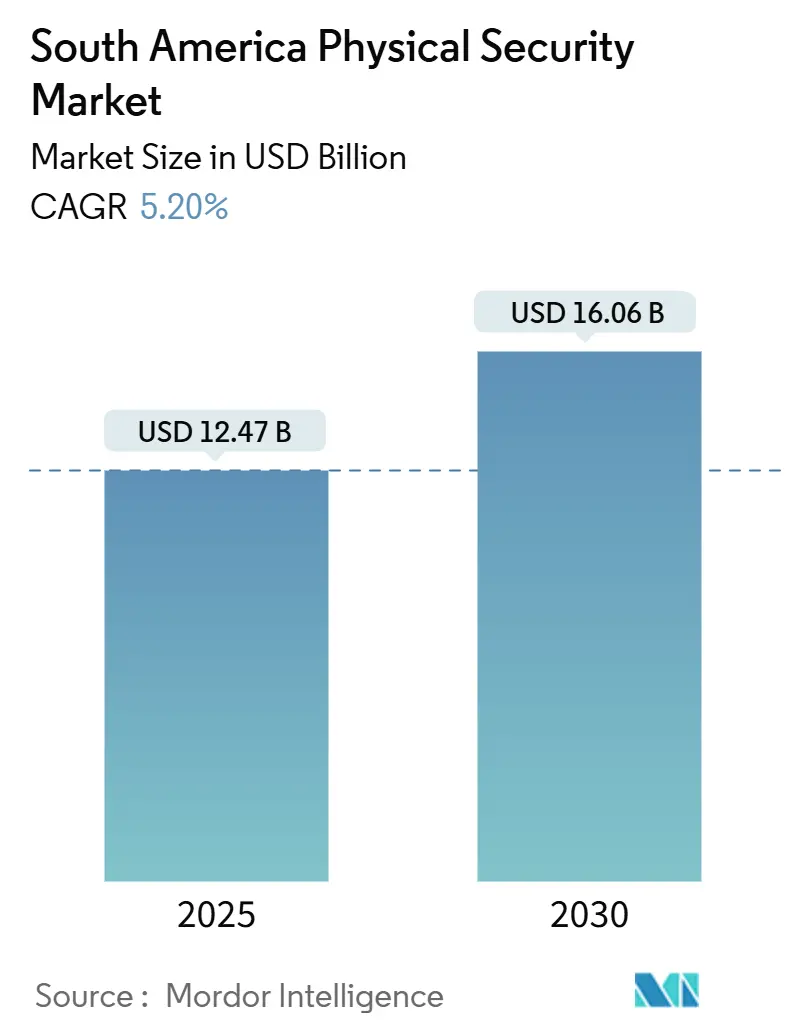

| Market Size (2025) | USD 12.47 Billion |

| Market Size (2030) | USD 16.06 Billion |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

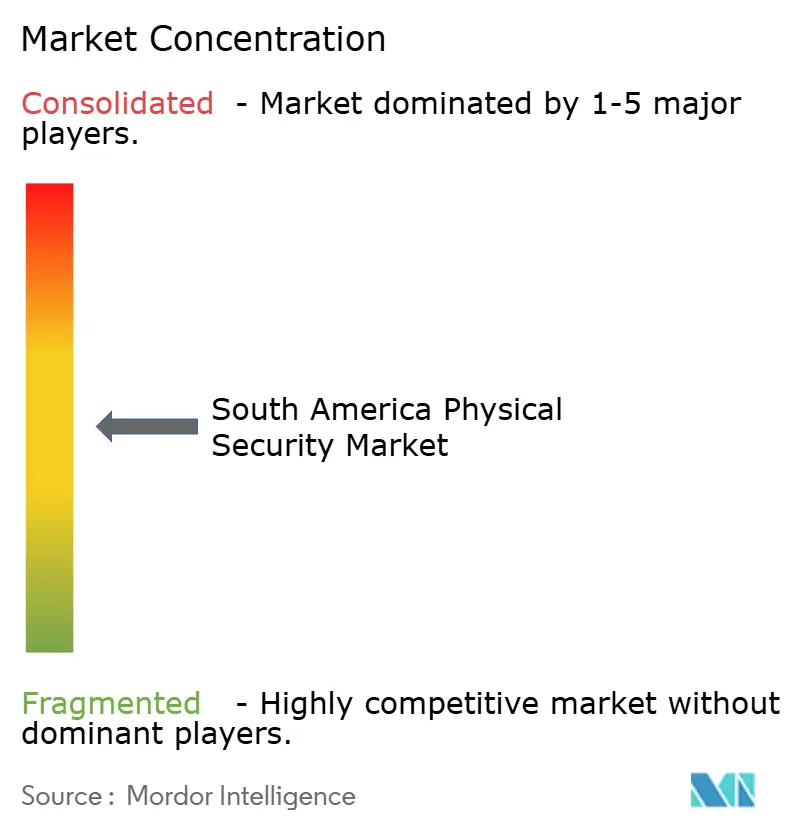

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Physical Security Market Analysis by Mordor Intelligence

The South America Physical Security market size stands at USD 12.47 billion in 2025 and is forecast to reach USD 16.06 billion by 2030, expanding at a 5.20% CAGR. The expansion is anchored in rapid urban growth, persistent crime in metropolitan areas and public-sector investments in smart-city infrastructure. Government programs mandating biometric verification, the falling price of IP-based cameras and the growing appetite for cloud deployment models are combining to widen the addressable customer base. Near-shoring is encouraging manufacturers to overhaul perimeter and access control systems to meet international compliance benchmarks, while AI-driven analytics help law-enforcement agencies respond faster in dense urban corridors. Import duties and local-content rules in Brazil and Argentina remain cost headwinds, yet the switch to subscription-based Video Surveillance as a Service (VSaaS) and Access Control as a Service (ACaaS) continues to entice budget-constrained customers toward scalable platforms.

Key Report Takeaways

- By system type, video surveillance led with 39.63% of South America physical security market share in 2024; biometric systems are advancing at a 5.88% CAGR through 2030.

- By service model, VSaaS commanded a 32.61% share of the South America physical security market size in 2024, while ACaaS recorded the highest projected 5.77% CAGR.

- By deployment model, cloud solutions accounted for 54.73% share of the South America physical security market size in 2024 and are expanding at a 6.22% CAGR.

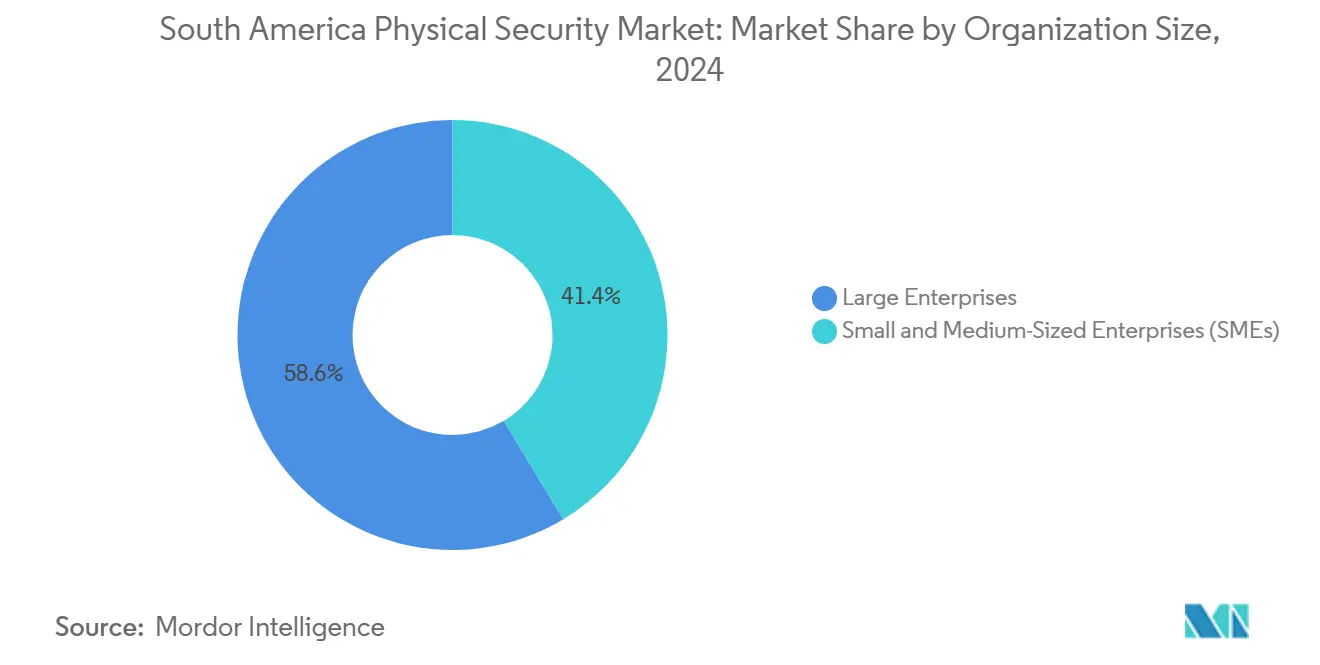

- By organization size, large enterprises held a 58.62% share in the South America physical security market in 2024; small and medium-sized enterprises are growing at a 6.31% CAGR.

- By end-user industry, government and public safety captured a 27.93% revenue share in 2024 in the South America physical security market; healthcare is forecast to rise at a 5.76% CAGR through 2030.

- By country, Brazil represented 29.98% of South America physical security market share in 2024 and is progressing at a 6.01% CAGR through 2030.

South America Physical Security Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government regulations mandate high-security protocols | +1.2% | Global, with early gains in Colombia, Brazil, Mexico | Medium term (2-4 years) |

| Rising smart-city and smart-building roll-outs | +0.9% | Brazil, Mexico, Colombia core, spill-over to Argentina | Long term (≥ 4 years) |

| Adoption of cloud-based VSaaS and ACaaS by SMEs | +0.8% | Global, particularly Brazil and Mexico | Short term (≤ 2 years) |

| Declining cost and higher ROI of IP-based hardware | +0.7% | Global | Medium term (2-4 years) |

| Near-shoring-driven factory security upgrades | +0.6% | Mexico, Brazil, Colombia | Medium term (2-4 years) |

| AI video-analytics to tackle urban crime hotspots | +0.5% | Brazil, Colombia, Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Regulations Mandate High-Security Protocols

Government mandates are compelling enterprises to adopt advanced security systems. Colombia’s National Digital Transformation Policy promotes nationwide facial-recognition roll-outs, while Brazil obliges biometric verification for social benefit disbursements. [1]Richard Santa, “Colombia's Progress Towards Smart Cities and the Challenges,” AVI Latinoamérica, avilatinoamerica.comMexico’s biometric CURP pilot in Veracruz signals a move toward unified identity management. These statutes prompt continuous upgrades as firms future-proof assets against tightening compliance. Spending is therefore decoupled from short-term economic swings, sustaining steady growth in the South America Physical Security market. Secondary effects include demand for cybersecurity-hardened edge devices that safely process sensitive biometrics.

Rising Smart-City and Smart-Building Roll-outs

Municipal authorities view integrated security as the backbone of digital transformation. Medellín offers free metro connectivity serving 80,000 daily users, while Mompox plans a USD 20 billion smart-city overhaul for its 45,000 residents. These projects specify CCTV, access control and IoT sensors that must interoperate with traffic, lighting and public Wi-Fi platforms. The resulting procurement pipeline favors vendors supplying end-to-end, cyber-secure solutions. Commercial developers mirror this trend by merging security with building-management systems to improve tenant safety and energy use. As deployments mature, demand shifts to analytics software that mines video data for urban-planning insights, reinforcing recurring revenue.

Adoption of Cloud-Based VSaaS and ACaaS by SMEs

SMEs increasingly select subscription models to obtain enterprise-grade surveillance without heavy capital outlays. Prosegur showcases hybrid packages that combine on-site guards, cloud cameras and centralized AI analysis through its Intelligent Security Operations Centers. Predictable monthly fees help smaller firms manage cash flow while scaling headcount. Brazil and Mexico, home to vibrant SME ecosystems, witness the fastest uptake. Providers benefit from sticky revenue as clients rely on continuously updated cloud firmware and analytics modules. The trend also fuels demand for resilient network infrastructure within industrial parks and mixed-use campuses.

Declining Cost and Higher ROI of IP-Based Hardware

Economies of scale in semiconductor fabs and stiffer supplier competition are lowering camera and access reader prices. Hanwha Vision forecasts edge-AI cameras with built-in generative analytics that cut bandwidth usage while producing richer metadata. Enhanced functionality improves return on investment by reducing false alarms and enabling remote diagnostics that shrink maintenance payrolls. Integrators can now justify projects with payback rooted in operational efficiencies rather than fear-based narratives. Affordable IP hardware also accelerates analog-to-digital migration, expanding the South America Physical Security industry into cost-sensitive mid-tier commercial properties.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial CAPEX for integrated solutions | -0.8% | Global, particularly affecting SMEs in Brazil, Mexico, Argentina | Short term (≤ 2 years) |

| Data-privacy and cyber-security concerns | -0.6% | Brazil, Argentina, Chile core, spill-over to Colombia | Medium term (2-4 years) |

| Rural connectivity and power-infrastructure gaps | -0.5% | Rest of South America, rural areas in Brazil, Colombia | Long term (≥ 4 years) |

| Import tariffs and local-content rules | -0.4% | Brazil, Argentina core, with moderate impact in Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX for Integrated Solutions

Fully featured surveillance, access control, and intrusion suites demand substantial hardware, licensing, and professional services. Even with cloud options, many entities prefer on-premises storage for sensitive evidence, which keeps upfront costs high. The integration of disparate subsystems often requires custom middleware and skilled installation, which can drive project costs beyond SME budgets. Financing constraints result in phased deployments that slow revenue conversion for vendors in the South America Physical Security industry. Although equipment prices are trending lower, installation labor and compliance documentation remain significant cost components.

Data-Privacy and Cyber-Security Concerns

Public opposition to indiscriminate surveillance gained momentum after studies criticized São Paulo’s Smart Sampa facial-recognition program for algorithmic bias. Organizations now demand end-to-end encryption and strict data retention policies, which prolong procurement cycles. Breaches affecting video streams or biometric vaults carry reputational and regulatory penalties, especially under Brazil’s LGPD framework. Vendors must invest in secure-by-design firmware and continuous penetration testing, which can inflate R&D budgets. These issues temper adoption, particularly among public entities wary of civil-society backlash.

Segment Analysis

By System Type: Video Surveillance Maintains Prime Position

Video surveillance delivered 39.63% of South America Physical Security market share in 2024 as organizations upgraded from analog to IP ecosystems that support AI analytics. The segment’s dominance reflects its adaptability across retail, transportation and city surveillance. IP cameras integrate seamlessly with existing IT networks, lowering incremental setup costs while unlocking cloud analytics that elevate situational awareness. Hybrid deployments help owners preserve sunk costs in coaxial infrastructure, driving adoption in budget-sensitive municipalities. Biometric and perimeter solutions complement cameras, expanding the South America Physical Security market size by simplifying identity verification at facility gateways and by protecting larger footprints such as industrial parks.

Growth in biometric systems is underpinned by regulatory mandates and improved sensor affordability. Fingerprint and facial-recognition algorithms now operate on low-power edge devices, minimizing latency while ensuring data residency compliance. Vendors bundle biometrics with access-control software to deliver unified dashboards that correlate entry logs with video evidence. This convergence simplifies audit trails, attracting critical-infrastructure operators that must document chain-of-custody. As hybrid platforms mature, buyers expect seamless scalability, a requirement that favors suppliers offering open SDKs and cloud-native microservices.

Note: Segment shares of all individual segments available upon report purchase

By Service Model: Cloud Services Accelerate Recurring Revenues

VSaaS captured 32.61% share of the South America Physical Security market size in 2024. Organizations outsource storage, firmware updates and analytics to specialized providers who guarantee service-level agreements. ACaaS, expanding at 5.77% CAGR, is similarly appealing as it eliminates on-site server maintenance and supports rapid credential provisioning for transient staff. Remote monitoring yields value for SMEs lacking security operations centers; third-party analysts triage alarms around the clock, forwarding verified incidents to local responders.

Hybrid service frameworks integrate human guards with AI analytics. Prosegur’s multi-country iSOCs fuse real-time feeds from cameras, IoT sensors and GPS trackers to dispatch mobile patrols when anomalies surface. For customers, the subscription model converts unpredictable capital expenses into fixed operational budgets. For vendors, multiyear contracts lock in cash flow while enabling upsell of advanced analytics modules as software updates.

By Deployment Model: Cloud Solutions Lead Digital Transformation

Cloud deployment models dominate with 54.73% market share in 2024 and maintain the highest growth rate at 6.22% CAGR through 2030, reflecting organizations' preference for scalable, cost-effective security solutions. On-Premises deployments continue to serve organizations with strict data sovereignty requirements or legacy system integration needs, particularly in government and financial services sectors. Edge/Hybrid deployments are gaining traction as organizations seek to balance cloud benefits with local processing capabilities for real-time applications.

Edge computing integration is becoming increasingly important as organizations seek to process video analytics locally while maintaining cloud connectivity for management and storage functions. Hanwha Vision's 2025 technology roadmap emphasizes edge AI cameras that reduce bandwidth requirements while providing real-time processing capabilities

By Organization Size: SMEs Drive Market Democratization

Large Enterprises maintain the largest market share at 58.62% in 2024, leveraging their substantial budgets to implement comprehensive security systems across multiple facilities. Small and Medium-Sized Enterprises represent the fastest-growing segment with a 6.31% CAGR through 2030, driven by declining technology costs and the availability of cloud-based service models that eliminate barriers to entry.

The democratization of advanced security technologies is enabling SMEs to access capabilities previously reserved for large organizations, including AI-powered video analytics and biometric access control systems. Cloud-based service models are particularly attractive to SMEs as they provide enterprise-grade functionality with predictable monthly costs rather than substantial capital investment.

By End-user Industry: Healthcare Leads Growth Amid Diversification

Government and Public Safety sectors maintain the largest end-user share at 27.93% in 2024, driven by substantial public investment in smart city infrastructure and law enforcement capabilities. Healthcare emerges as the fastest-growing vertical with a 5.76% CAGR through 2030, reflecting increased security awareness following pandemic-related vulnerabilities and the need to protect sensitive patient data and pharmaceutical assets. The Banking, Financial Services, and Insurance (BFSI) sector represents a significant market segment due to regulatory requirements and high-value asset protection needs. Information Technology and Telecommunications companies are implementing advanced security systems to protect critical infrastructure and comply with data protection regulations.

Transportation and Logistics sectors are experiencing increased security investment driven by nearshoring trends and the need to protect supply chain infrastructure. Retail organizations are adopting advanced video analytics to combat theft and optimize store operations by analyzing customer behavior. The residential security market is growing as urbanization increases and middle-class populations expand across the region.

Geography Analysis

Brazil anchors the regional landscape, holding 29.98% South America Physical Security market share in 2024. Mandatory biometric verification for welfare and the large-scale Smart Sampa project, with more than 31,000 cameras and USD 1.8 million monthly funding, fuel steady procurement. Local champion Intelbras provides domestically manufactured cameras and DVRs, reducing import costs and satisfying local-content quotas. Currency volatility is a persistent risk, prompting foreign suppliers to hedge through joint ventures with Brazilian integrators.

Mexico benefits from near-shoring inflows as electronics, automotive and aerospace firms relocate plants from Asia. Securing multi-hectare industrial parks demands perimeter RADAR, credentialed access turnstiles and redundant control rooms. The C5 integrated security command in Mexico City exemplifies federal commitment to surveillance modernization. Veracruz’s biometric CURP tests demonstrate grassroots penetration of identity solutions, setting a precedent for broader roll-out.

Argentina and Colombia are rising candidates for smart-city pilots. Buenos Aires leverages a USD 750 million defense package to modernize port and rail terminals, while Colombia’s USD 100 million surveillance allocation covers 20 mid-sized cities equipped with facial recognition. Uruguay’s USD 322 million security-equipment spend in 2023 underscores appetite across smaller economies. Vendors that localize interfaces and comply with data-sovereignty statutes gain competitive advantage as procurement shifts toward performance-based contracts.

Competitive Landscape

The South America Physical Security industry features moderate fragmentation. Chinese vendors Hikvision and Dahua combine cost efficiency with broad SKU catalogs, while diversified multinationals Honeywell, Bosch, and Johnson Controls leverage integrated platforms that tie video, intrusion, and HVAC controls into unified dashboards. Regional stalwart Intelbras ranks 11th globally with USD 434.44 million in revenue, showcasing the viability of manufacturing close to end markets.[2]William Pao, “Security 50: Optimism Prevails as Security Returns to Growth Trajectory,” asmag.com, asmag.com

The convergence of physical and cyber disciplines is reshaping competitive chessboards. Motorola Solutions layers Alta SOS into its Avigilon suite to forward geolocated alerts straight to emergency call centers.[3]Motorola Solutions Press Release, “Avigilon Hits $1.5 Billion Sales Run Rate Post Motorola Acquisition,” bctechnology.comAllied Universal executed five acquisitions in 2025, including Celar Security in Colombia, to enhance its cloud analytics and engineering capabilities. Service-centric players like Prosegur scale iSOCs that fuse manned guarding with AI surveillance, differentiating through responsiveness and multi-asset coverage.

Innovation clusters around edge AI, zero-trust architecture, and open APIs. Manufacturers releasing firmware development kits attract a partner ecosystem that tailors retail analytics or industrial-safety modules. Consolidation pressures mount on mid-tier distributors lacking R&D heft. Nevertheless, niches such as maritime perimeter protection and healthcare data integration offer room for specialized entrants.

South America Physical Security Industry Leaders

Bosch Security Systems GmbH

Dahua Technology Co., Ltd

Genetec Inc.

Hangzhou Hikvision Digital Technology Co., Ltd.

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Allied Universal purchased Celar Security and Soltes Technology in Colombia, adding USD 490 million annual revenue across South America.

- March 2025: Motorola Solutions enhanced Avigilon with Alta SOS, reaching a USD 1.5 billion annual sales run rate.

- February 2025: Prosegur reported a 32% rise in consolidated net income to EUR 17 million (USD 19.70 million) on 45.3% organic growth, fueled by technology-driven services.

- January 2025: ASSA ABLOY expanded its access-control portfolio by acquiring 3millID and Third Millennium Systems.

South America Physical Security Market Report Scope

Physical security refers to the prevention of unauthorized individuals from accessing controlled facilities. Physical security technologies have undergone significant development recently, offering advanced protection at competitive prices. Physical security devices utilize cloud technology and AI for even more sophisticated real-time data processing. Various automated physical security components can perform multiple functions in a physical security system.

The South American physical security market is segmented by system type (video surveillance system [IP surveillance, analog surveillance, and hybrid surveillance], physical access control system (PACS), biometric system, perimeter security, and intrusion detection), service type (Access Control-as-a-Service (ACaaS) and Video Surveillance-as-a-Service (VSaaS)), type of deployment (on-premises and cloud), organization size (SMEs and large enterprises), end-user industry (government services, banking and financial services, IT and telecommunications, transportation and logistics, retail, healthcare, residential, and other end-user industries), and country (Brazil, Mexico, Argentina, and the Rest of South America). The report offers the market sizes and forecasts for all the above segments in terms of value (USD).

| Video Surveillance | IP Surveillance |

| Analog Surveillance | |

| Hybrid Surveillance | |

| Physical Access-Control Systems (PACS) | |

| Biometric Systems | |

| Perimeter Security | |

| Intrusion Detection |

| Access Control as a Service (ACaaS) |

| Video Surveillance as a Service (VSaaS) |

| Remote Monitoring as a Service (RMaaS) |

| On-Premises |

| Cloud |

| Edge / Hybrid |

| Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises |

| Government and Public Safety |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecommunications |

| Transportation and Logistics |

| Retail |

| Healthcare |

| Residential |

| Energy and Utilities |

| Other End-user Industries |

| Brazil |

| Mexico |

| Argentina |

| Colombia |

| Rest of South America |

| By System Type | Video Surveillance | IP Surveillance |

| Analog Surveillance | ||

| Hybrid Surveillance | ||

| Physical Access-Control Systems (PACS) | ||

| Biometric Systems | ||

| Perimeter Security | ||

| Intrusion Detection | ||

| By Service Model | Access Control as a Service (ACaaS) | |

| Video Surveillance as a Service (VSaaS) | ||

| Remote Monitoring as a Service (RMaaS) | ||

| By Deployment Model | On-Premises | |

| Cloud | ||

| Edge / Hybrid | ||

| By Organization Size | Small and Medium-Sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-user Industry | Government and Public Safety | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Information Technology and Telecommunications | ||

| Transportation and Logistics | ||

| Retail | ||

| Healthcare | ||

| Residential | ||

| Energy and Utilities | ||

| Other End-user Industries | ||

| By Country | Brazil | |

| Mexico | ||

| Argentina | ||

| Colombia | ||

| Rest of South America |

Key Questions Answered in the Report

What is the 2025 valuation of the South America Physical Security market?

The market is valued at USD 12.47 billion in 2025.

How fast is the South America Physical Security market expected to grow?

It is projected to expand at a 5.20% CAGR through 2030.

Which country holds the largest share of spending?

Brazil accounts for 29.98% of regional revenue in 2024.

Which system type is leading adoption across segments?

Video surveillance leads with 39.63% share in 2024.

Why are SMEs embracing cloud security platforms?

Subscription models such as VSaaS and ACaaS reduce capital expenditure and offer scalable functionality.