Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

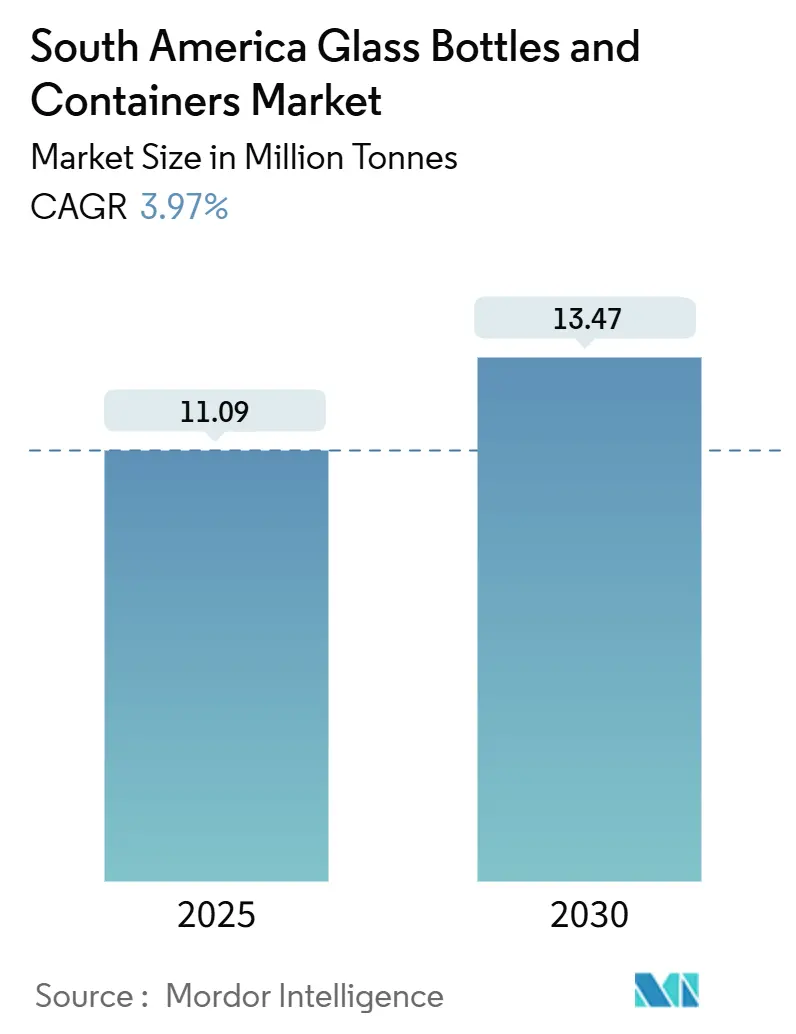

| Market Volume (2025) | 11.09 Million tonnes |

| Market Volume (2030) | 13.47 Million tonnes |

| Growth Rate (2025 - 2030) | 3.97% CAGR |

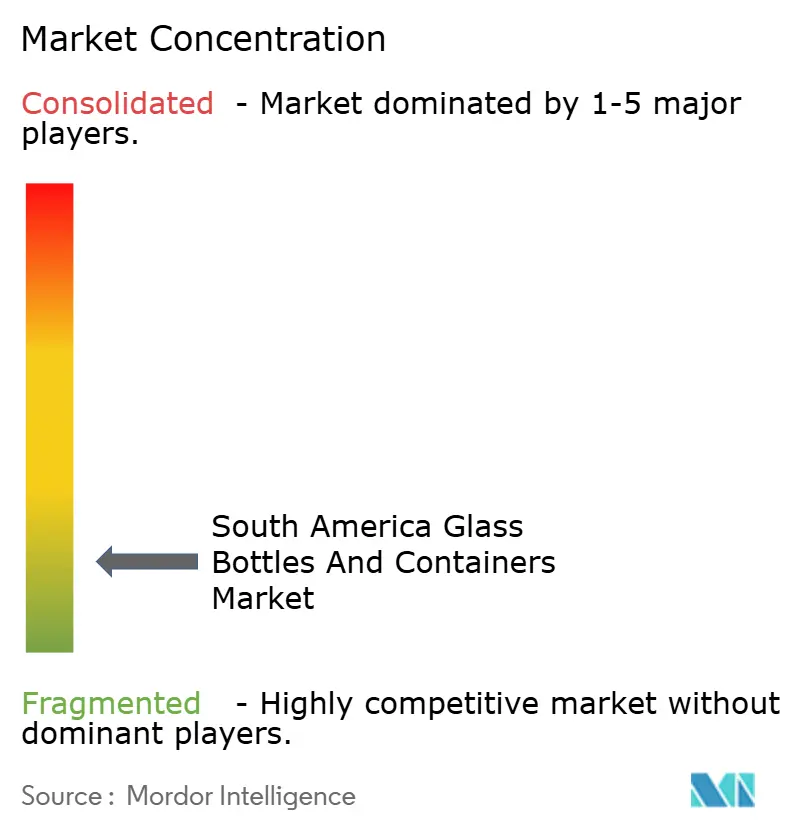

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Glass Bottles And Containers Market Analysis by Mordor Intelligence

The South America Glass Bottles and Containers Market size is estimated at 11.09 million tonnes in 2025, and is expected to reach 13.47 million tonnes by 2030, at a CAGR of 3.97% during the forecast period (2025-2030). A decisive policy push toward circular-economy goals, consumer migration to premium packaging, and the region’s rising middle-income cohort collectively propel demand, while elevated furnace energy bills and logistics costs moderate the growth curve. Sustainability mandates are tightening Extended Producer Responsibility (EPR) rules, prompting beverage, food, and beauty brands to specify infinitely recyclable glass to future-proof compliance strategies.[1]Deutsche Gesellschaft für Internationale Zusammenarbeit, “Economía Circular en Colombia,” giz.de Accelerated beverage launches in wine, spirits, craft beer, and functional drinks keep glass at the center of premium product narratives, even as producers pursue lightweighting to soften shipping costs. Downstream, cosmetics players utilize glass for its shelf appeal and formula stability, while amber formats gain market share in response to pharmaceutical needs for ultraviolet barrier protection. Parallel capacity additions in Brazil and Colombia signal that leading converters are re-engineering furnace fleets for energy efficiency, alternative fuels, and hybrid melting to defend operating margins amid volatile gas tariffs.

Key Report Takeaways

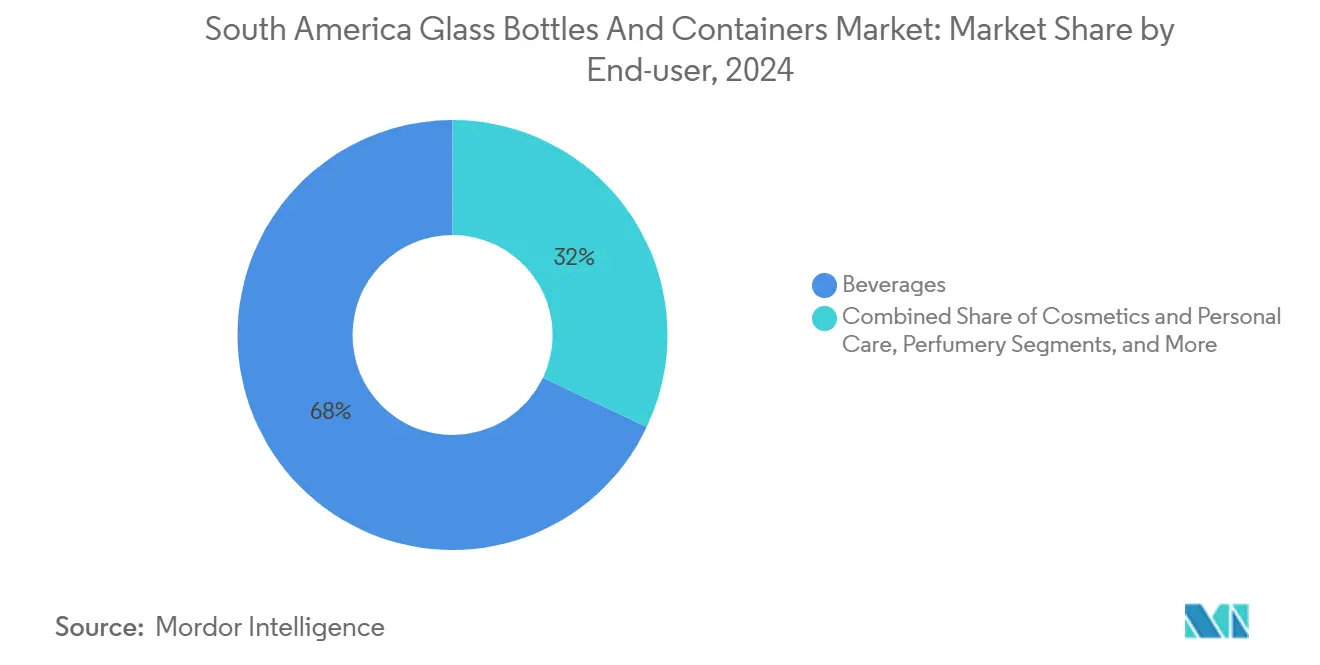

- By end-user, beverages captured 67.97% of the South America glass bottles and containers market share in 2024. Cosmetics and personal care products registered the highest trajectory, with a 5.27% CAGR through 2030.

- By color, Flint glass captured 60.37% of the South America glass bottles and containers market, while amber glass is projected to grow at a 4.89% CAGR between 2025 and 2030.

- By country, the South America glass bottles and containers market for Argentina is projected to grow at a 5.34% CAGR between 2025-2030.

South America Glass Bottles And Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable Packaging Solutions in Beverage and Food Industries | +1.2% | Brazil, Argentina core markets with Colombia emerging | Medium term (2-4 years) |

| Growing Alcohol Consumption Driving Premium Glass Bottle Usage | +0.8% | Regional, with concentration in Brazil, Colombia urban centers | Short term (≤ 2 years) |

| Expansion of Pharmaceutical and Cosmetic Sectors Boosting Glass Container Adoption | +0.7% | Urban centers across Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Government Regulations Favoring Recyclable and Non-Toxic Packaging Materials | +0.6% | MERCOSUR countries, national EPR frameworks | Medium term (2-4 years) |

| Increasing Investments in Local Glass Manufacturing Facilities | +0.4% | Colombia manufacturing corridors, Brazil industrial zones | Long term (≥ 4 years) |

| Consumer Preference for Premium Packaging in Urban Markets | +0.3% | Metropolitan areas in Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Packaging Solutions

Regulators across MERCOSUR have embedded recyclability thresholds in new EPR decrees, causing a structural pivot toward glass that accelerates baseline demand and tilts brand strategies toward closed-loop models. Brazil’s Nova Indústria Brasil program has earmarked USD 60 billion in concessional lines to retrofit packaging lines and fund reverse logistics networks, creating a policy flywheel that raises the cost of non-compliant plastic alternatives. National waste-collection gaps amplify the advantage because glass enjoys entrenched buy-back channels, enabling converters to secure higher cullet ratios that improve furnace energy efficiency. Beverage multinationals are now committed to achieving 50–70% recycled content in their regional portfolios by 2030, which translates into firm order books that anchor furnace debottlenecking projects. As a result, sustainability clauses have shifted from marketing talking points to hard-tender requirements that favor suppliers with high recovery rates and low life-cycle emissions.

Growing Alcohol Consumption Driving Premium Glass Bottle Usage

Urban millennials and Gen-Z consumers are trading up to craft spirits, premium beers, and estate wines, which are packaged exclusively in glass, thereby energizing volume growth above baseline population trends. Spirits distillers in Brazil posted low-double-digit shipment gains in 2024, with premium SKUs outpacing mainstream offerings by a 3:1 ratio, reinforcing the value of glass as a badge of authenticity. Vitro’s USD 70 million furnace rebuild in Toluca increased daily nameplate capacity to 230 tons, serving prestige spirits, fragrance flacons, and limited-edition beverage runs, underscoring converter confidence in premiumization tailwinds. Regional vintners exporting to North America and Europe further specify heavy-weight bottles to underscore terroir credentials, expanding the South America glass bottles and containers market’s footprint in value terms, even where unit volumes advance modestly.

Expansion of Pharmaceutical and Cosmetic Sectors Boosting Adoption

South America’s middle-class cohort is forecast to add 25 million consumers by 2030, channeling disposable income toward skincare, fragrance, and nutraceutical products that rely on barrier-grade amber or flint vials. Cosmetics lines proliferated by nearly 18% YOY in Brazilian drugstores during 2024, and local fillers increasingly select glass droppers and jars that convey purity and recyclability. Pharmaceutical growth, especially in over-the-counter syrups and pediatric formulations, intensifies demand for type III and borosilicate bottles that meet stringent extractables/leachables thresholds. Colombia’s INVIMA green-lights returnable glass systems for certain drug categories, enabling up to 12 reuse cycles and reducing the cost of ownership for hospital buyers. These trends solidify a multiyear pull for specialty glass, particularly amber formats that shield photosensitive molecules.

Government Regulations Favoring Recyclable and Non-Toxic Materials

New food-contact directives within MERCOSUR ban packaging materials that fail to meet prescribed recovery quotas, prioritizing glass over polymers that carry a higher risk of contamination or micro-migration. Argentina’s Régimen de Incentivo para Grandes Inversiones confers accelerated depreciation and duty-free imports on machinery that lowers carbon intensity, making it financially attractive to commission next-generation oxy-fuel furnaces with 30% lower CO₂ profiles. Chile’s Packaging Producer Registry enforces escalating take-back targets, driving brand owners to contract with glass suppliers offering cullet-feed assurances and data-rich traceability. Such policy arcs compress payback periods for plant upgrades and push beverage bottlers toward glass, fostering structural volume resilience for the South America glass bottles and containers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Costs Associated with Glass Production | -0.9% | Regional, particularly energy-intensive manufacturing zones | Short term (≤ 2 years) |

| Competition from Lightweight and Cost-Effective Plastic Alternatives | -0.7% | Price-sensitive consumer segments across region | Medium term (2-4 years) |

| Logistical Challenges in Transporting Fragile Glass Containers Across Regions | -0.5% | Cross-border trade corridors, remote distribution areas | Long term (≥ 4 years) |

| Limited Recycling Infrastructure in Certain South American Countries | -0.3% | Rural areas, smaller municipalities with limited waste management | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Energy Costs Associated with Glass Production

Melting furnaces operate at temperatures near 1,500 °C and consume natural gas and electricity, which together can account for up to 20% of the cost of goods sold, exposing producers to tariff fluctuations and currency volatility. O-I Glass shuttered select lines in July 2025 to rein in overhead when spot gas prices spiked 42% YOY, highlighting the sensitivity of kiln economics to commodity prices. While cullet feed reduces energy per ton by up to 30%, inadequate collection in rural catchments limits achievable recycled-content ratios, particularly outside Brazil and Colombia. These cost headwinds squeeze margins and may delay scheduled rebuilds, tempering throughput additions for the South America glass bottles and containers market.

Competition from Lightweight and Cost-Effective Plastic Alternatives

PET containers weigh as little as 10% of a comparable glass bottle, translating into freight savings that can reach 30 USD per pallet on long‐haul routes across the Andes. Arca Continental committed MXN 3 billion to PET collection and closed-loop flake capacity through 2027, signaling that beverage incumbents will continue to keep plastics in their multi-format portfolios for value-conscious shoppers. Retailers in lower-income neighborhoods frequently price beverages below psychological thresholds rooted in packaging costs, restricting glass volumes where elasticity is high. Consequently, glass converters must focus on functional niches such as ultraviolet barrier, chemical inertness, or premium aesthetics to fend off substitution threats in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Volume, Cosmetics Lead Growth

Beverages accounted for 67.97% of the South America glass bottles and containers market in 2024 as brand owners rely on glass to protect taste profiles and elevate perceived quality. Segment resilience stems from wine and spirits labels that position glass as integral to heritage narratives, while non-alcoholic functional drinks increasingly tap embossed flint bottles to signal purity. The South America glass bottles and containers market size attributed to beverages is projected to grow at roughly the headline pace, supported by incremental craft-brew launches and regulatory plastic bans in municipal zones.

Cosmetics and personal care register the highest trajectory at a 5.27% CAGR through 2030, reflecting aspirational consumption trends in urban centers such as São Paulo, Bogotá, and Buenos Aires. Luxury skincare refill lines utilize thick-walled jars that encourage reuse, aligning with zero-waste commitments and increasing the average unit value. The segment’s progress also benefits the South America glass bottles and containers industry through the cross-pollination of decoration techniques, including lacquering, acid etching, and digital printing, which were first perfected for fragrance flacons.

By Color: Flint Dominates, Amber Accelerates

Flint glass captured 60.37% of the South America glass bottles and containers market in 2024, driven by its clarity and branding versatility. It remains the default choice for transparent beverage and condiment applications, where product visibility serves as a quality indicator. Batch houses favor flint due to stable raw material supply and high cullet availability, allowing converters to maximize furnace uptime. The South America glass bottles and containers market size for flint applications is expected to expand steadily as premium beverage and clear-packaged food demand rises.

Amber glass, however, is the fastest-growing material with a 4.89% CAGR outlook through 2030, as pharmaceutical labs and craft brewers adopt UV-shield formats that extend shelf life. Regulatory pharmacopoeias mandate light-barrier packaging for certain antibiotics and vitamin solutions, locking in a baseline stream of amber orders. Specialty-tea and cold-brew coffee startups also shift to amber 330 ml bottles to merge artisanal cues with functional protection, adding incremental tonnage. Combined, these dynamics diversify furnace color campaigns and enlarge the value pool for the South America glass bottles and containers market.

Geography Analysis

Brazil accounts for more than half of regional output, leveraging its long-established furnace clusters near São Paulo and Rio de Janeiro that serve dense consumer catchments. Nova Indústria Brasil’s USD 60 billion modernization fund offers subsidized credit for low-carbon furnaces, enabling market leaders to schedule cold repairs without liquidity strain. Ardagh, Wheaton, and O-I colocate cullet processing plants with furnaces, lifting recycled content and trimming energy draw. These integrated loops reinforce Brazil’s status as the demand and supply gravity center for the South America glass bottles and containers market.

Colombia is the breakout growth pocket, buoyed by a USD 120 million expansion at O-I’s Zipaquirá complex that adds two forehearths and a high-speed cosmetic-jar line.[2]O-I Glass, “10-K Annual Report 2024,” o-i.com Trade-zone incentives eliminate VAT on imported refractories and combustion equipment, compressing capex per ton and attracting second-tier players exploring joint ventures. INVIMA’s endorsement of returnable drug containers decreases total system cost, nudging hospital groups to specify glass over disposable plastics, which in turn pushes up amber pull.

Argentina offers latent upside as the Régimen de Incentivo para Grandes Inversiones grants decade-long tax holidays for projects exceeding USD 200 million, enticing investors who are weighing furnace builds versus upgrades elsewhere. Domestic wine bottlers in Mendoza are seeking supply security to match their vineyard expansion plans, lobbying for on-site furnace capacity due to high freight costs from Brazilian plants. Beyond the Big Three, Chile, Peru, and Ecuador collectively account for a single-digit share, yet exhibit above-average CAGR as premium beverage and cosmetic consumption rises in metropolitan corridors, supplying the long-tail expansion of the South America glass bottles and containers market.

Competitive Landscape

The regional arena tilts toward a handful of global juggernauts, yet fresh consolidation efforts signal a potential reshuffle. O-I Glass delivered USD 141 million operating profit in its Americas arm during Q1 2025, even while curbing capacity to mitigate energy cost shocks. Its network across Brazil, Colombia, Peru, and Ecuador affords customer proximity and economies of scope, positioning the company for swift color or mold changeovers.

Brazil’s Moreira Salles family executed a landmark takeover of France-based Verallia in March 2025, foreshadowing deeper South American influence over European glass flows and possibly channeling incremental capital toward Brazilian furnace upgrades.[3]Alessandro Parodi, “Brazil’s Moreira Salles family launches takeover bid for French bottler Verallia,” reuters.com The move consolidates global rival counts and could shift procurement leverage toward local beverage majors, who favor regional sourcing to hedge against currency swings.

Technological differentiation centers on hybrid furnaces that blend renewable electricity with oxy-fuel burners to reduce CO₂ emissions by up to 40% and lower NOₓ levels below EU limits. Saverglass, for instance, implemented a pilot system that reduced electricity draw by 30% while maintaining pull rates, demonstrating that sustainability gains can be achieved while maintaining throughput efficiency. Lightweighting, holographic embossing, and digital direct-to-glass printing expand customization options, allowing brands to enhance shelf presence without the environmental impact of plastic sleeves. These innovations reinforce glass’s premium aura and shelter margin structure for incumbents in the South America glass bottles and containers market.

South America Glass Bottles And Containers Industry Leaders

Verallia SA

Ardagh Group S.A.

Gerresheimer Querétaro S.A. de C.V.

Vidrala SA

Owens-Illinois Perú S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: O-I Glass implemented furnace closures at select South American sites to align production with near-term demand shifts and rising gas prices.

- May 2025: O-I Glass reported USD 141 million operating profit for Q1 2025, citing resilience in premium beverage channels despite energy headwinds.

- March 2025: Brazil’s Moreira Salles family secured control of Verallia, signaling a consolidation wave that could pivot capital expenditure toward South America.

- February 2025: Further clarification from the Moreira Salles group confirmed regulatory filings for the Verallia acquisition, which aims to deepen local manufacturing.

South America Glass Bottles And Containers Market Report Scope

The South America Glass Bottles and Containers Market Report segments the market by End-User. These include Beverages, which are further divided into Alcoholic (covering Beer, Wine, Spirits, and other drinks like Cider and Fermented Beverages) and Non-Alcoholic (encompassing Juices, Carbonated Drinks, Dairy-Based Drinks, and other beverages). The Food segment includes items like Jam, Jelly, Marmalades, Honey, Sausages, Condiments, Oil, and Pickles. Other segments include Cosmetics and Personal Care, Pharmaceuticals (excluding Vials and Ampoules), and Perfumery. The market is also categorized by Color, featuring Flint, Green, Amber, and other shades, and by Country, highlighting Brazil, Argentina, Colombia, and the Rest of South America. Forecasts are presented in terms of volume (tonnes).

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

By Country

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

| By Country | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected volume of the South America glass bottles and containers market by 2030?

The market is forecast to reach 13.47 million Tonnes by 2030, expanding at a 3.97% CAGR.

Which end-user category leads demand in South America?

Beverages command 67.97% of 2024 volume thanks to strong wine, spirits, and premium soft-drink uptake.

Why is amber glass growing faster than other colors?

Pharmaceutical and craft-beverage producers need ultraviolet protection, driving amber’s 4.89% CAGR outlook.

How are energy costs influencing regional capacity decisions?

High gas prices forced furnace closures and staggered rebuilds, prompting firms to adopt hybrid melting for efficiency.

Which country is the main production hub for glass bottles in South America?

Brazil houses the largest furnace cluster and benefits from subsidized modernization funds and extensive cullet infrastructure.

What recent consolidation could reshape supply dynamics?

The Moreira Salles family’s acquisition of Verallia may redirect investment toward South American plants and enhance regional bargaining power.

Page last updated on: