Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The IoT Market Report is Segmented by Component (Hardware, Software, Services, and More), End-User Industry (Agriculture, Retail and E-Commerce, Energy and Utilities, and More), Application (Asset Tracking and Fleet Management, Predictive Maintenance, Smart Metering, and More), Deployment Model (Cloud, On-Premises, and More), and Geography

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

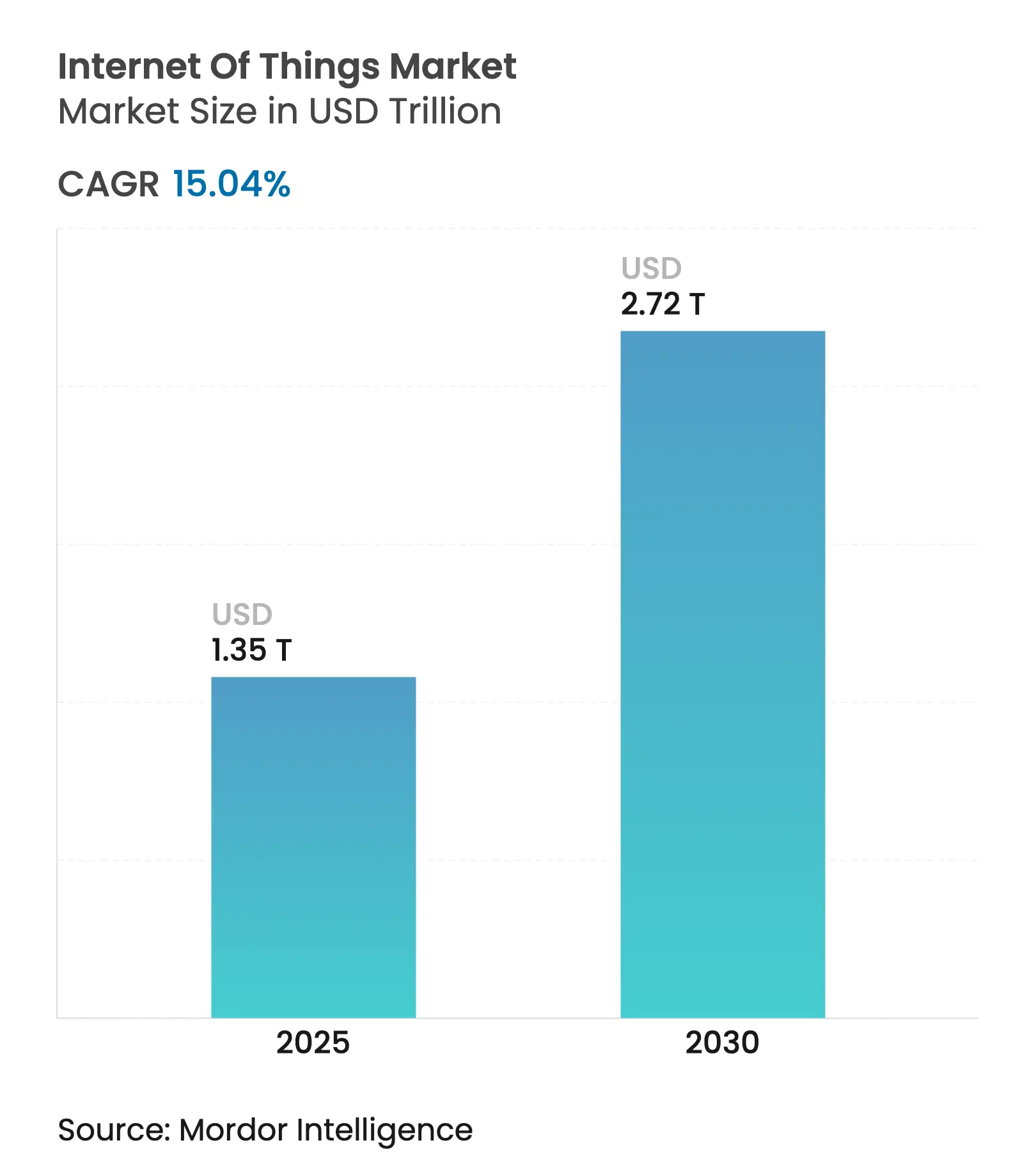

| Market Size (2025) | USD 1.35 Trillion |

| Market Size (2030) | USD 2.72 Trillion |

| Growth Rate (2025 - 2030) | 15.04 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Strong demand for real-time analytics, predictive maintenance, and autonomous decision systems is accelerating deployments across factories, farms, and logistics hubs. Rapid 5G roll-outs, growth of low-power wide-area networks, and falling sensor costs expand the addressable base of connected assets. Enterprises also value edge AI because it protects data sovereignty while guaranteeing millisecond response times. As a result, investment continues to shift from pilot projects to full-scale production across every major vertical. The Internet of Things market, therefore, continues to compound on a solid technology foundation supported by resilient capital spending and regulatory incentives aimed at efficiency and sustainability.[1]GSMA Intelligence, “IoT Market Update 2025,” gsma.com

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Connected-device proliferation and falling sensor costs Connected-device proliferation and falling sensor costs | +3.2% | Global | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:+3.2% | Geographic Relevance :Global | Impact Timeline :Medium term (2–4 years) |

5G and LPWAN roll-outs widen coverage 5G and LPWAN roll-outs widen coverage | +2.8% | North America and Asia-Pacific | Short term (≤ 2 years) | |||

Edge-AI analytics enable real-time value Edge-AI analytics enable real-time value | +2.5% | Global | Medium term (2–4 years) | |||

LEO-satellite IoT unlocks remote monitoring LEO-satellite IoT unlocks remote monitoring | +1.9% | Global rural and remote areas | Long term (≥ 4 years) | |||

ESG-linked supply-chain reporting mandates ESG-linked supply-chain reporting mandates | +1.6% | Europe and North America | Short term (≤ 2 years) | |||

Usage-based insurance powered by IoT telemetry Usage-based insurance powered by IoT telemetry | +1.4% | North America and Europe | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Connected-device proliferation and falling sensor costs

Unit prices for basic environmental sensors have declined from USD 20 to below USD 5, making dense instrumentation economically viable across factories and farms. Industrial-grade vibration sensors used in predictive maintenance now retail for USD 50-100 compared with USD 200-500 only five years ago.[2]Analog Devices, “Trends in Industrial Sensor Cost Reduction,” analog.com Lower hardware barriers attract new software integrators, broadening the Internet of Things market talent pool. BMW’s private 5G production network already links thousands of sensors to edge controllers that optimize throughput in real time. Temporary semiconductor shortages create cost pressure, yet design innovations that reduce component counts preserve downward price momentum. As firms connect ever-smaller assets, data volumes rise sharply, cementing analytics services as the fastest-growing revenue pool.

5G and LPWAN roll-outs widen coverage

Private 5G now underpins ultra-low-latency industrial control, demonstrated by John Deere’s Waterloo Works where flexible manufacturing lines rely on wire-free reconfiguration. LoRaWAN and NB-IoT networks complement 5G by linking remote fields, mines, and pipelines where cellular economics still lag. Kinéis and other nanosatellite operators bridge remaining gaps, enabling continuous visibility of livestock herds and maritime assets. Telecom operators coordinate spectrum and backhaul investments to match device density with viable returns. These converging access options keep the internet of things market on an inclusive path that spans both dense urban campuses and sparsely populated frontiers.

Edge-AI analytics enable real-time value

Inference engines embedded in gateways or microcontrollers turn raw sensor feeds into immediate actions. Predictive maintenance models detect bearing anomalies and trigger work orders within milliseconds. Vision-based inspection at the edge cuts manufacturing scrap rates without cloud round-trips. Yet AI workloads increase power draw; battery-operated nodes must balance model complexity against life-cycle targets. Academic studies show pruning and quantization can trim consumption by 40% without accuracy loss. Solar energy harvesting solutions extend autonomy, helping the market penetrate safety-critical zones where wiring is impractical.

LEO-satellite IoT unlocks remote monitoring

Low Earth Orbit constellations provide connectivity where terrestrial rollout is infeasible. Spacecom and AYECKA have packaged satellite IoT-as-a-Service for Sub-Saharan farms, delivering field data that guides irrigation plans. OneWeb’s agriculture program projects multi-billion-dollar global productivity gains through yield optimization. Power consumption remains a hurdle, but Very Low Earth Orbit designs at 300 km combine reduced path loss with simpler antennas, lowering energy per bit. Satellite service prices continue to decline, adding resiliency to the internet of things market backbone.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Escalating cybersecurity and privacy breaches Escalating cybersecurity and privacy breaches | −2.1% | Global | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:−2.1% | Geographic Relevance :Global | Impact Timeline :Short term (≤ 2 years) |

Protocol fragmentation and poor interoperability Protocol fragmentation and poor interoperability | −1.8% | Global multi-vendor sites | Medium term (2–4 years) | |||

Export controls squeezing chip / module supply Export controls squeezing chip / module supply | −1.5% | China-US technology flows | Short term (≤ 2 years) | |||

Edge-AI power draw strains device batteries Edge-AI power draw strains device batteries | −1.2% | Global battery-dependent nodes | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Escalating cybersecurity and privacy breaches

Connected assets expand the attack surface, with ransomware already halting factory lines and exposing proprietary recipes. The EU Cyber Resilience Act sets minimum encryption and patching obligations, forcing vendors to absorb higher compliance costs. Industrial buyers increasingly request secure-boot chipsets and zero-trust architectures, raising barriers for low-cost suppliers. Breach headlines could momentarily slow adoption, yet long-term security spending often translates into higher total contract values within the internet of things market.

Protocol fragmentation and poor interoperability

LoRaWAN, Zigbee, Thread, and Wi-Fi coexist inside the same building, demanding complicated gateways. The Matter standard promises unification but remains limited to consumer lighting and temperature controls. Enterprises therefore grapple with siloed data models that inflate integration timelines. Niche protocol expertise commands premium rates, limiting scalability for small and mid-sized users. Harmonized semantic models are progressing, yet broad adoption remains several release cycles away.

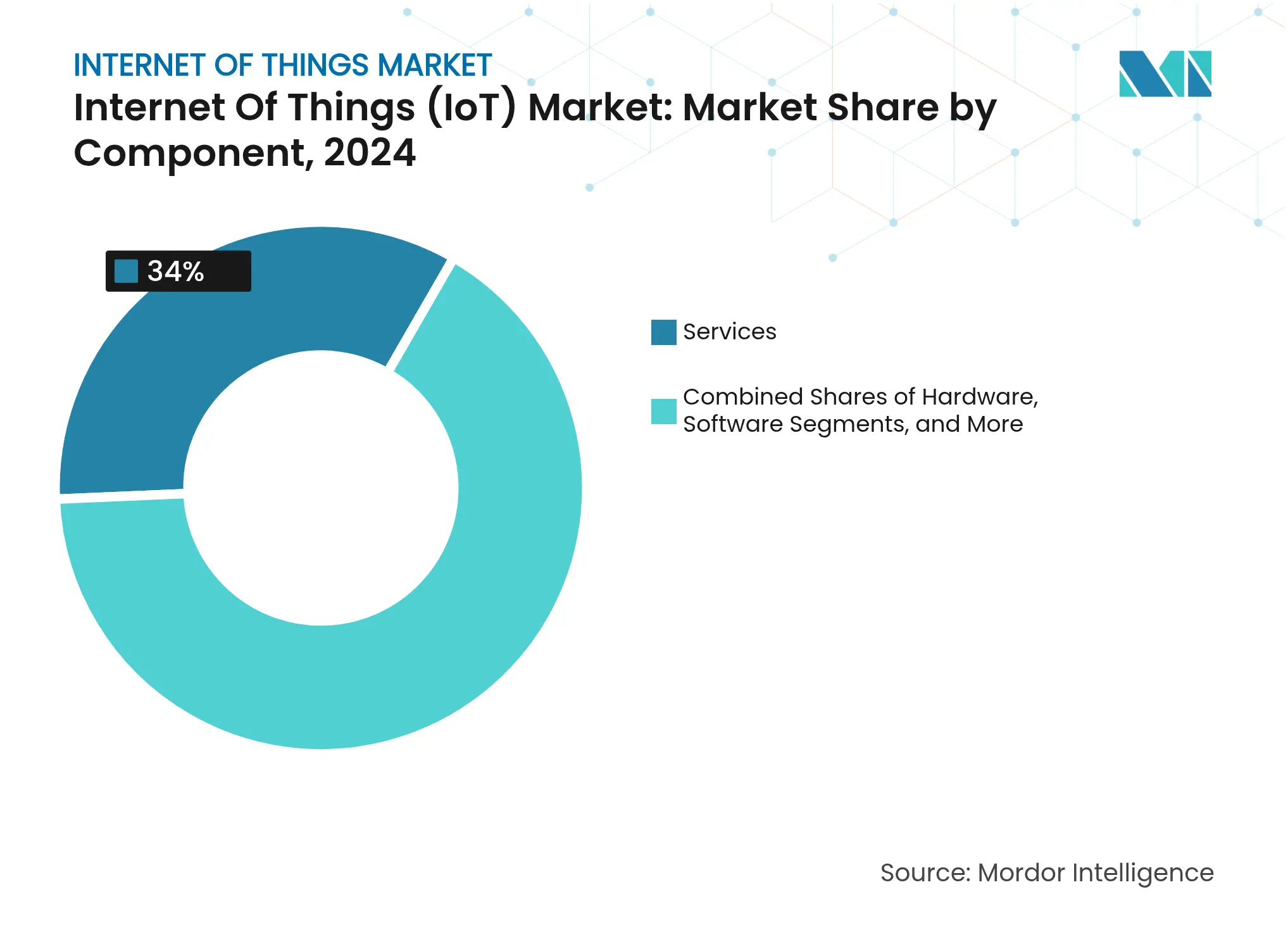

By Component: Service-led Transformation Shapes Integration Pathways

Services contributed 34% of 2024 revenue, underscoring the complexity of turning devices and data into measurable outcomes. Consulting teams map workflows, build secure architectures, and optimize dashboards that convert sensor streams into operational value. Hardware prices keep falling, yet integration demands elevate specialist labor rates, cementing services as the largest slice of the internet of things market. Edge platforms that blend container orchestration with OTA patching expand at 17.51% CAGR as buyers insist latency and data governance stay onsite. Connectivity modules absorb cost deflation, widening profit margins for solution assemblers who resell capacity across thousands of endpoints.

The push toward flexible infrastructure drives hybrid topologies where gateway agents decide what stays local and what travels to the cloud. Such orchestration intensifies demand for API harmonization between hyperscale clouds and factory floor controllers. Software vendors embed auto-ML engines that fine-tune models continuously, reinforcing subscriptions that lock customers into ecosystems. Meanwhile, satellite operators partner with terrestrial carriers to bundle fallback connectivity, broadening geographic applicability of the internet of things market. Vendors that package hardware, integration, and lifecycle management under outcome-based contracts are capturing share from component-centric rivals.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Manufacturing Retains Lead While Agriculture Accelerates

Manufacturing held 29.5% of 2024 spending as factories rely on predictive maintenance, robot coordination, and supply-chain transparency to safeguard uptime. Siemens reports record digital industries orders tied to brown-field retrofits that network legacy machines.[3]Siemens AG Investor Relations, “Q1 2025 Digital Industries Results,” press.siemens.com Automotive plants deploy thousands of torque and vibration sensors, feeding edge AI that quarantines anomalies before they trigger costly downtime. Environmental, health, and safety dashboards gain prominence as regulators tighten emission audits. Consequently, the Internet of Things market size for industrial plants is expected to expand steadily despite macro headwinds.

Agriculture, by contrast, grows fastest at a 19.2% CAGR. Soil probes, drone imagery, and satellite links allow farmers to adjust fertilizer and irrigation in near real time, lowering input costs per hectare. Start-ups bundle sensors, analytics, and credit services into subscription models affordable to mid-sized holdings. Livestock ranchers fit collars that monitor temperature, rumination, and location, trimming disease outbreaks and predation losses. As public agencies push food security, grant funding accelerates connected-farm adoption, broadening the Internet of Things industry customer base beyond early adopters.

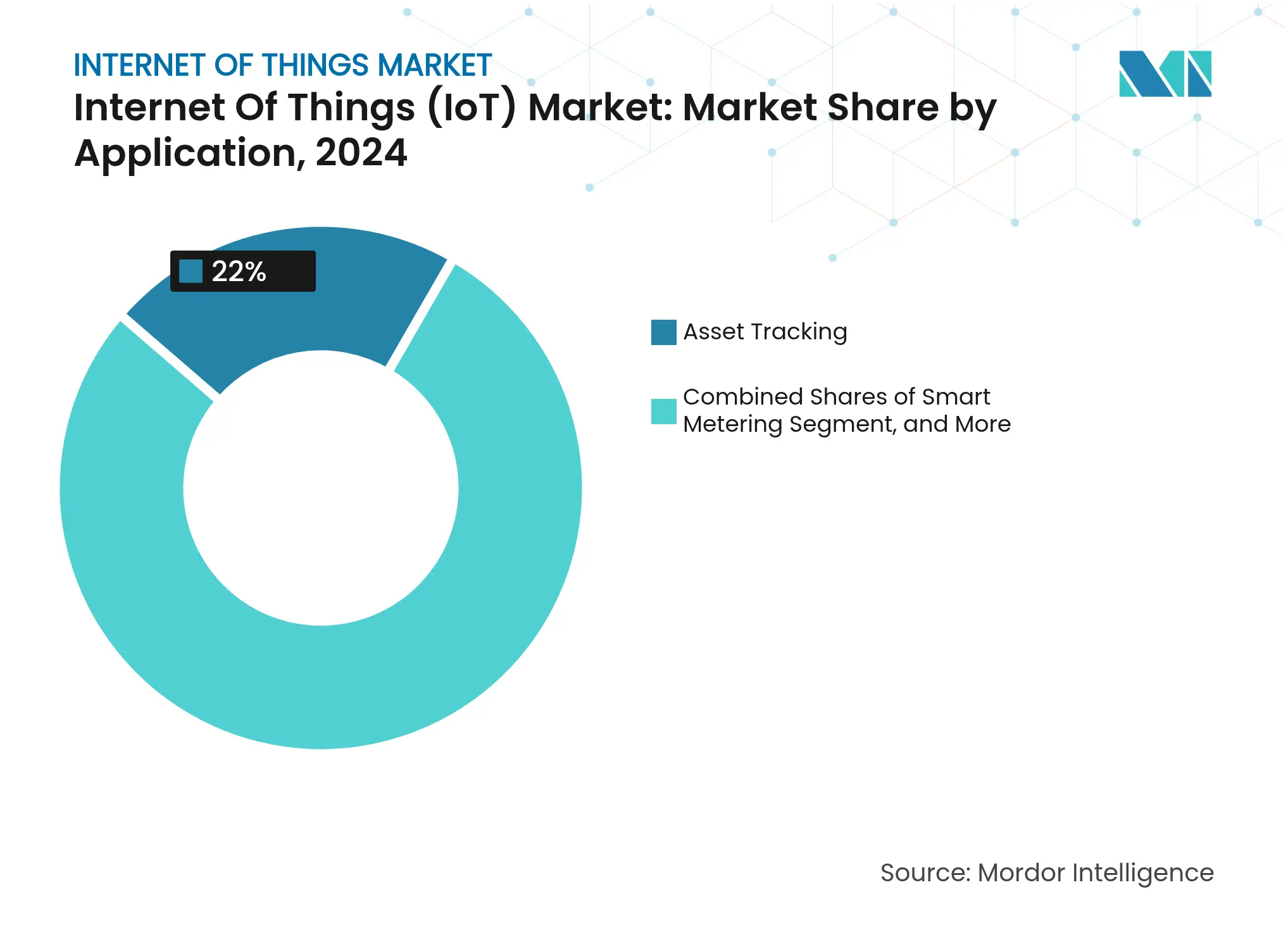

By Application: Asset Tracking Dominates While Environmental Monitoring Surges

Asset tracking captured 22% of the Internet of Things market in 2024, supported by falling GPS module prices and rising cargo theft risk. Logistics providers geofence trailers, pallets, and even individual cartons, reducing search times when shipments deviate. Cold-chain operators embed temperature sensors to satisfy pharmaceutical integrity mandates. Meanwhile, environmental monitoring posts the fastest 20.11% CAGR because air-quality, water-level, and methane-leak metrics are now mandatory in many jurisdictions. Edge AI filters noisy weather data, ensuring only anomalies traverse cellular links, trimming bandwidth cost.

Predictive maintenance, smart metering, and patient monitoring also expand, though at varied paces. Utilities replace legacy meters with bi-directional smart endpoints that detect tampering and relay outage alerts without truck rolls. Hospitals integrate wearables that transmit vitals straight into electronic health records, freeing nursing staff for higher-value care. Each new use case broadens the Internet of Things market addressable universe and raises expectations for service-level agreements spanning connectivity, cybersecurity, and analytics.

By Deployment Model: Cloud Leads Yet Edge Builds Momentum

Cloud retained 48% of 2024 deployments because elasticity and pay-as-you-grow economics appeal to companies with volatile workloads. Hyperscalers court OEMs with pre-built device registries, digital twin templates, and AI toolkits, making integration quick for pilot projects. Still, latency-sensitive processes push heavy workloads to the edge, where the segment grows at an 18% CAGR. Factory safety systems require microsecond responsiveness, prompting on-premises inference rather than round-trips to distant regions. Hence, the Internet of Things market is evolving into a distributed computing fabric that blends local processing with global orchestration.

Hybrid strategies prevail: raw sensor streams are summarized on-site and only exception data reaches central clouds for long-term learning. Such partitioning curbs backhaul cost and satisfies privacy statutes that prohibit cross-border movement of personally identifiable data. Orchestration stacks continuously synchronize containers and security policies between tiers, demanding sophisticated DevOps skills. Vendors that automate this choreography gain mindshare as enterprises scale proofs of concept into thousands of sites.

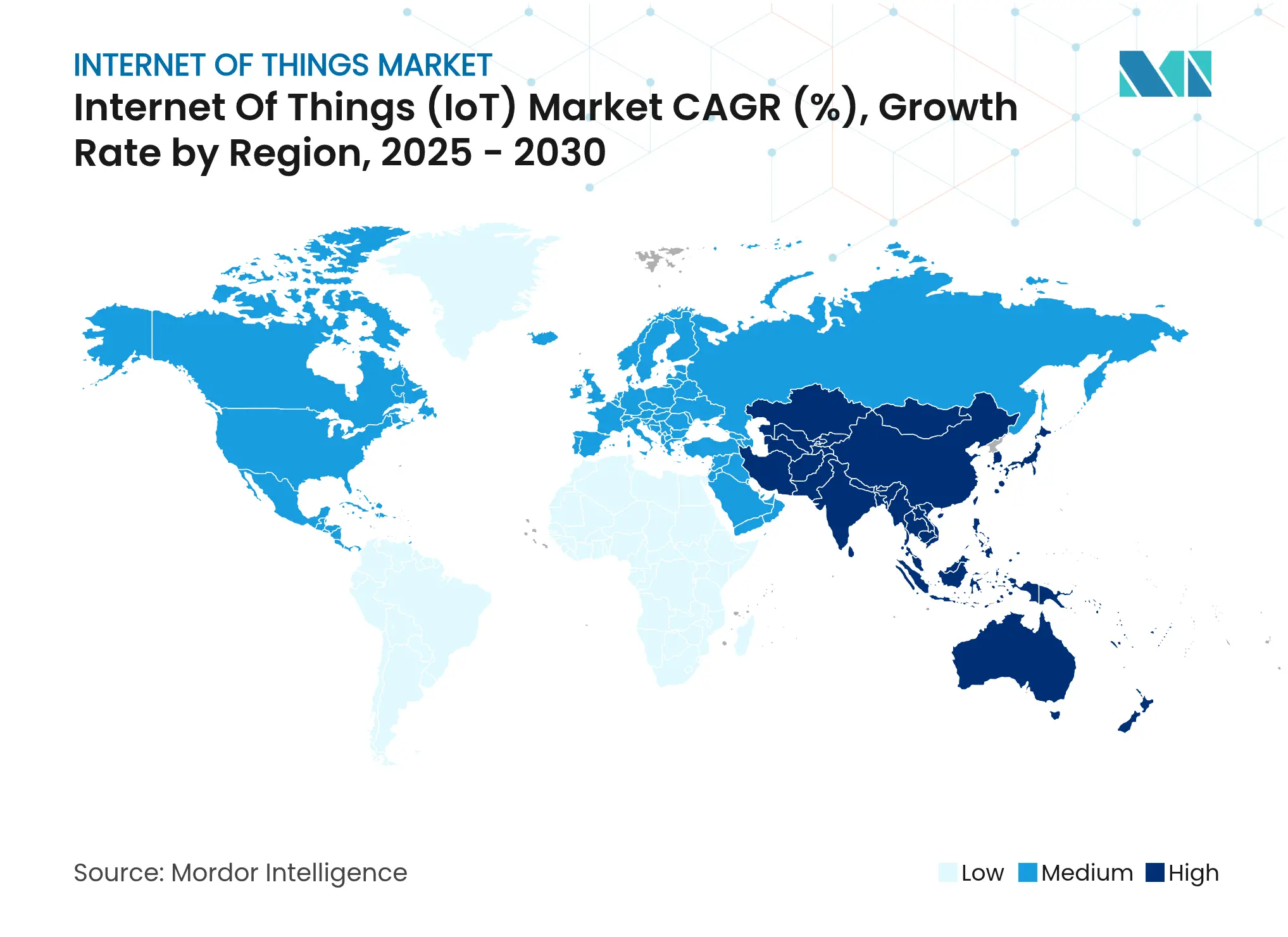

North America owned 32.3% of 2024 revenue, anchored by mature 5G roll-outs, wide adoption of private cellular licenses, and a robust digital-native workforce. Industrial facilities from automotive to food processing routinely pilot spectrum-sharing networks that stream high-fidelity data to edge AI controllers.[4]UScellular & Ericsson, “Private 5G for Industry Case Study,” uscellular.comPolicy frameworks prioritize innovation yet codify minimum security standards, promoting trust without stifling experimentation. Consequently, the IoT market continues to see steady capital allocations even when macro conditions fluctuate.

Asia-Pacific is projected to grow at 15.1% CAGR through 2030 as governments embed IoT into manufacturing subsidies and smart-city blueprints. Licensed cellular connections are set to reach 270 million by 2030 across India, China, and Southeast Asia. China accelerates domestic chip foundry investments to buffer export control uncertainties, while India leverages production-linked incentives to attract sensor assembly plants. Start-ups in Vietnam and Indonesia integrate LPWAN gateways with cloud dashboards, bringing mid-tier factories online at low cost. Together, these trends expand the Internet of Things market size across a demographically diverse region.

Europe emphasizes environmental compliance, making sensor-driven emissions tracking integral to corporate reporting. Edge deployments rise because privacy regulations encourage onsite processing. Public-private consortia finance smart port logistics and cross-border freight transparency systems. Middle East and Africa remain earlier in the adoption curve but leapfrog with satellite-enabled livestock monitoring and solar-powered water management. International development agencies fund pilot projects that demonstrate quick payback, nurturing localized expertise and widening the internet of things market footprint.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

The competitive arena is moderately fragmented: hyperscale cloud operators dominate platform spending, while sensor and module supply remains distributed among hundreds of vendors. Amazon Web Services, Microsoft, and Google bundle secure device onboarding, digital twins, and AI model libraries that shorten deployment timelines for integrators. Siemens and Honeywell layer industrial domain know-how atop cloud stacks, packaging turnkey offerings that target brown-field retrofits. Qualcomm broadened its portfolio by acquiring Sequans’ 4G IoT assets for USD 200 million, adding cost-efficient cellular modules to its roadmap.

Telecom operators monetize connectivity through tiered service agreements that include SIM management, data routing, and security certificates. Some, like UScellular, partner with Ericsson to deploy turnkey private networks for manufacturing clients. Edge AI start-ups such as Samsara differentiate on vertically tailored user interfaces, achieving 32% annual recurring revenue growth through focused fleet and industrial solutions. Patent filings intensify around low-power AI accelerators and target-wake-time scheduling, illustrated by Meta’s recent submissions that promise longer battery life in dense Wi-Fi environments. Customers gravitate toward vendors able to deliver integrated stacks that blend hardware, software, and services, thereby minimizing vendor management overhead and accelerating return on investment.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

IoT is a network of internet-connected objects. These objects collect and exchange data using sensors embedded within them. IoT has combined hardware and software with the internet to create a more technically driven environment. The scope of study on the IoT market is structured to track the spending on hardware, platforms, and services across end-user industries, such as manufacturing, transportation, retail, healthcare, energy, and utilities.

The Internet of Things (IoT) Market is segmented by component (hardware, software/platform, connectivity, and services), end-user industry (manufacturing, transportation, healthcare, retail, energy and utilities, residential, government, and insurance), and geography (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.