Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

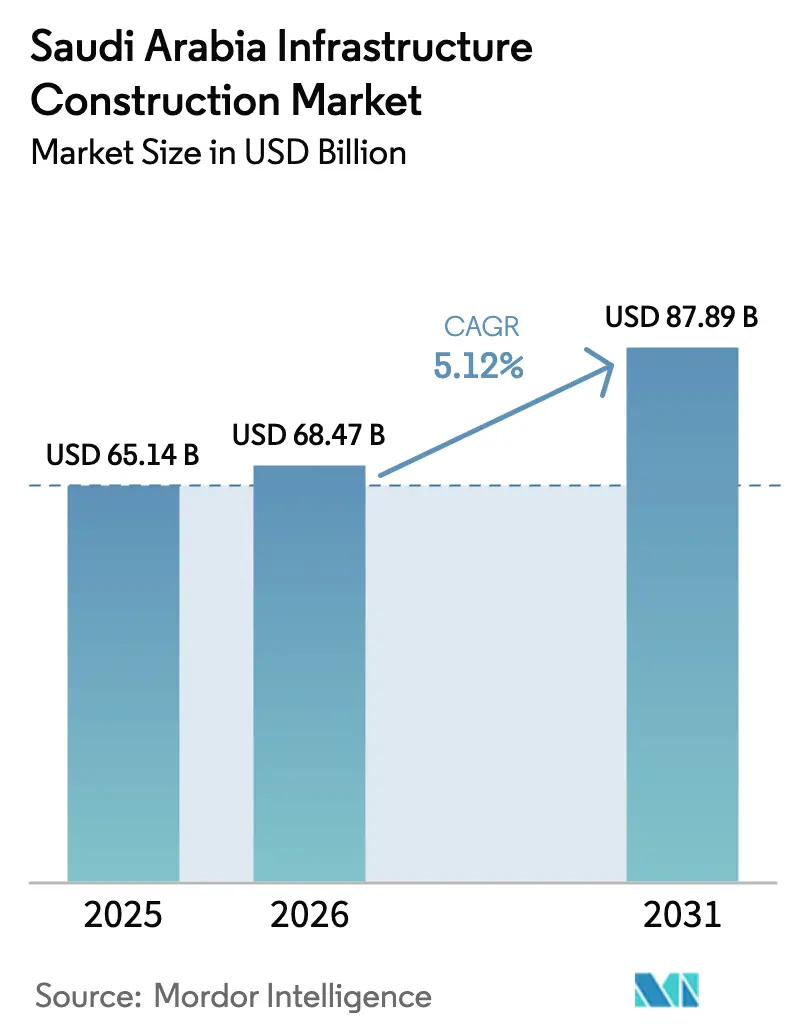

| Base Year Market Size (2025) | USD 65.14 Billion |

| Market Size (2026) | USD 68.47 Billion |

| Market Size (2031) | USD 87.89 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

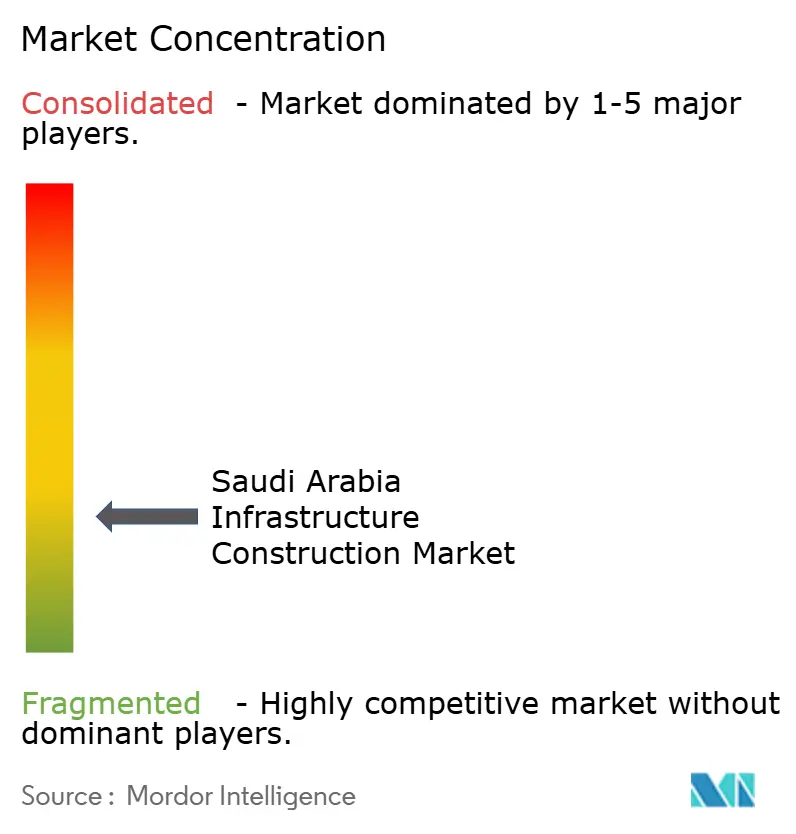

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Infrastructure Construction Market Analysis by Mordor Intelligence

The Saudi Arabia infrastructure construction market size was valued at USD 65.14 billion in 2025 and estimated to grow from USD 68.47 billion in 2026 to reach USD 87.89 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). The spending trajectory mirrors the Kingdom’s deliberate diversification away from crude exports toward logistics, renewable energy, and industrial capacity. Transportation programs, green-hydrogen complexes, and utility upgrades continue to underpin contract pipelines, yet growth has slowed from the double-digit surge recorded when giga-project announcements peaked in 2022-2023. Shifting Public Investment Fund (PIF) priorities now channel more capital into critical minerals, artificial-intelligence infrastructure, and tourism assets, recalibrating contractor order books toward extraction and data-center builds. At the same time, inflation in steel, cement, and labor is squeezing margins, making risk-sharing public-private partnership (PPP) models more attractive to domestic and international builders.

Key Report Takeaways

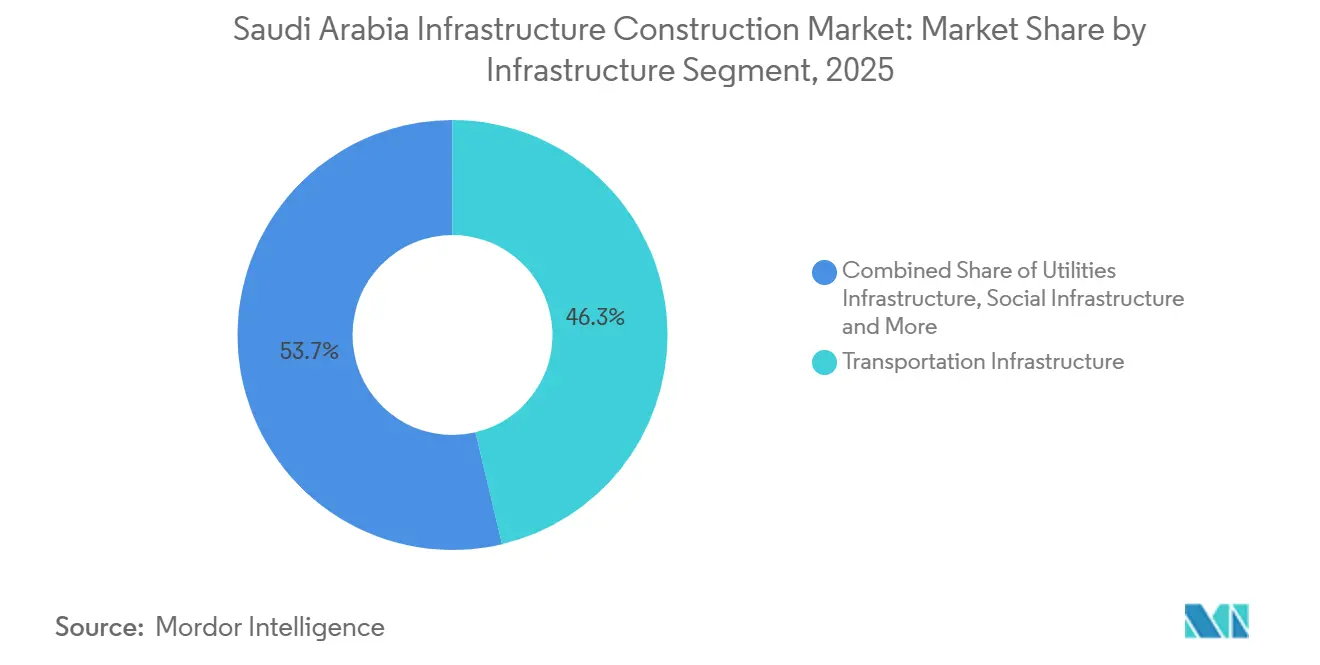

- By infrastructure segment, transportation captured 46.3% of the Saudi Arabia infrastructure construction market share in 2025, while social infrastructure is forecast to expand at a 6.11% CAGR through 2031.

- By construction type, new construction accounted for 76.7% of the Saudi Arabia infrastructure construction market in 2025, whereas renovation is advancing at a 6.44% CAGR through 2031.

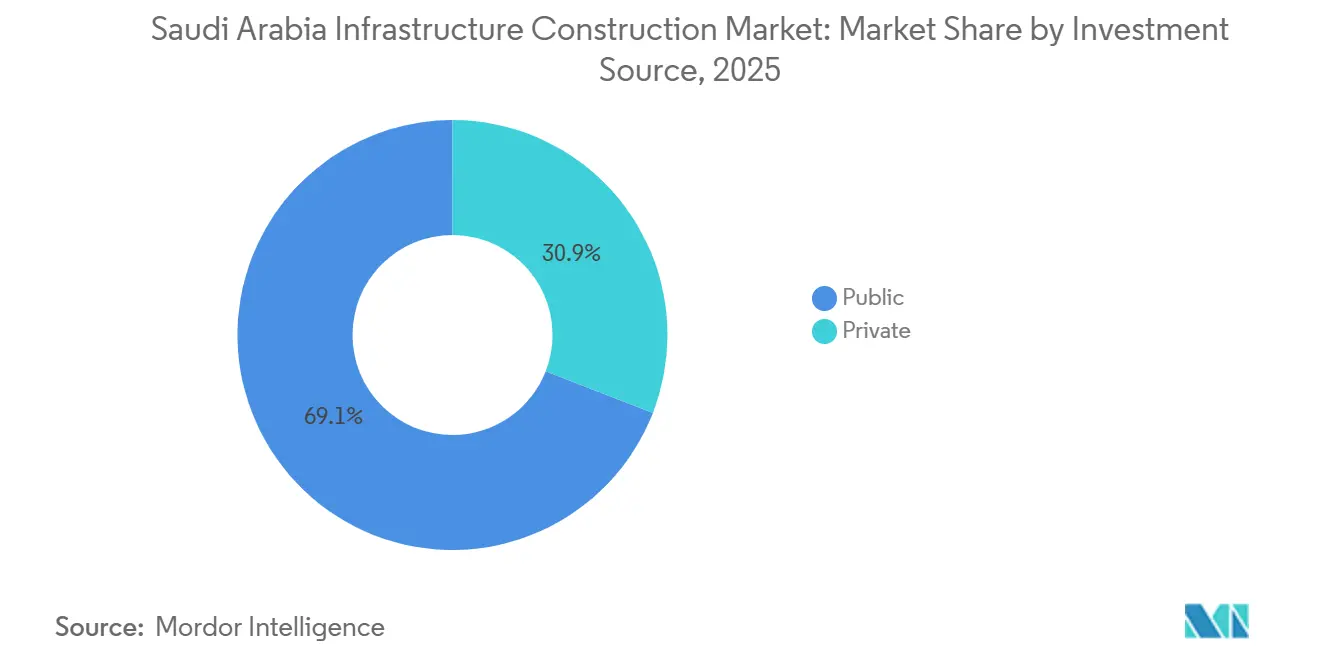

- By investment source, public funding held 69.1% of spending in 2025, but private capital routed through PPPs is projected to grow at a 6.81% CAGR between 2026 and 2031.

- By city, Riyadh led with a 2025 share of 33.4%, while the Dammam metropolitan area is set to post the fastest growth at a 7.09% CAGR thanks to petrochemical and carbon-capture projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga and mega programs sustain multi-year transport, utility, and social pipelines | +1.8% | Riyadh, NEOM, Jeddah, Dammam | Long term (≥ 4 years) |

| National logistics build-out across rail, ports, airports, and metros | +1.3% | Kingdom-wide hub corridors | Medium term (2-4 years) |

| Energy-transition capital spending on renewables, hydrogen, and carbon management | +1.1% | NEOM, Yanbu, Jubail, Northern Borders | Long term (≥ 4 years) |

| Water-security investments in desalination and reuse networks | +0.9% | Coastal population centers | Medium term (2-4 years) |

| PPP frameworks and sovereign co-funding crowd in private capital | +0.7% | Early adoption in Riyadh, Jeddah, and Eastern Province | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga Programs Sustain Multi-Year Pipelines

PIF-backed flagships such as King Salman International Airport and Diriyah Gate secure multi-billion-dollar packages that keep tier-one contractors mobilized for the long haul. Recent awards, including the USD 1.2 billion NEOM Phase 2 utilities backbone, signal a pivot from iconic real estate toward enabling industrial tenants. Local-content clauses that steered USD 157.6 billion into Saudi suppliers between 2020 and 2024 now underpin robust domestic fabrication, mechanical-electrical-plumbing (MEP), and precast ecosystems. As these long-dated contracts progress to the next phase, order books for tunneling, signaling, and rolling stock extend through 2030, anchoring labor demand despite PIF’s thematic shift[1]Public Investment Fund, “Annual Report 2024,” pif.gov.sa .

National logistics build-out across rail, ports, airports, and metros

The Landbridge rail corridor, King Abdullah Port’s 5 million TEU expansion, and metro extensions around Riyadh, Jeddah, and Dammam are central to the Kingdom’s goal of trimming Asia-Europe transit times. Container rail can move freight between the Red Sea and the Arabian Gulf in three days, compared with 14 days via the Suez Canal, enhancing Saudi Arabia's competitiveness in the infrastructure construction market. Air-side upgrades, such as Jeddah’s terminal expansion, designed to accommodate 80 million passengers by 2030, integrate with high-speed rail, easing pilgrim flows during Hajj. Together, these projects compress logistics costs for manufacturers by double-digit percentages, reinforcing the country’s non-oil export strategy.

Energy-Transition Capital Spending Drives Renewables and Hydrogen Infrastructure

The USD 8.4 billion NEOM Green Hydrogen complex—already 80% built—will start exporting 600 tons of hydrogen per day by 2027, while Yanbu’s 10 GW renewable-powered electrolyzer park targets 400,000 tons annually by 2030. ACWA Power’s 15 GW renewable energy pipeline and Saudi Electricity Company’s 8 GWh of battery storage create downstream demand for transmission lines, substations, and specialized HVAC systems, expanding the Saudi Arabia infrastructure construction market beyond hydrocarbons. Carbon-capture installations in Jubail alone command USD 2.3 billion in EPC packages, fostering new niches for contractors versed in process engineering and injection-well construction[2]ACWA Power, “15 GW Renewables Financial Close,” acwapower.com .

Water-Security Investments Support Urban and Industrial Growth

Reverse-osmosis desalination plants in Ras Mohaisen and Rabigh bring 900,000 m³-per-day capacity online before 2028, while Jeddah’s wastewater PPP adds 500,000 m³-per-day tertiary treatment for reuse in landscaping and industrial cooling. Solar-powered desalination at NEOM aims to eliminate fossil-fuel consumption, positioning the megacity as a sustainability showcase. Mandated ISO 14001 certification raises upfront compliance costs but improves environmental safeguards, extending permitting by up to nine months. These parallel investments reinforce potable-water resilience as the population edges toward 40 million by 2030.

Restraint Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Execution-capacity constraints and skilled-labor gaps | –1.2% | Riyadh, NEOM, Jeddah | Short term (≤ 2 years) |

| Cost inflation and higher financing costs | –0.9% | Kingdom-wide, acute for SMEs | Medium term (2-4 years) |

| Permitting and environmental-compliance complexity | –0.6% | Coastal desalination, extraction corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Execution-Capacity Constraints and Skilled-Labor Gaps

Simultaneous giga projects require project managers, structural engineers, and high-voltage electricians faster than the labor market can supply them. Expatriates still account for 85% of the 2.1 million construction workers, and wage inflation climbed 8-12% in 2025, compressing contractor margins by up to 300 basis points. New vocational centers launched in 2025 will graduate technicians, but their productivity ramp stretches 18-24 months, prolonging the bottleneck. Grade 1 classification rules, introduced to ring-fence projects above USD 267 million, further concentrate workloads among a small circle of firms, making skills shortages more acute for mid-tier players.

Cost Inflation and Higher Financing Costs

Steel prices rose 15% year-on-year in Q1 2025, and cement rose 8%, lifting the construction-cost index 11% in 2024. Fixed-price contracts awarded during the 2022 boom are now underwater unless escalation clauses apply. Meanwhile, SAIBOR’s average 5.8% rate in 2025 pushes up debt-service coverage ratios, squeezing speculative projects and renovation work with thinner margins. Banks prefer lending to Grade 1 firms, leaving smaller builders to turn to costlier non-bank channels, which drags on capital formation across the Saudi Arabian infrastructure construction market[3]Saudi Arabian Monetary Authority, “SAIBOR Rates 2025,” sama.gov.sa .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure Segment: Transportation Anchors, Social Accelerates

Transportation infrastructure dominated, with Saudi Arabia accounting for 46.3% of the infrastructure construction market share in 2025, reflecting heavy allocation to rail corridors, port expansions, and airport megaprojects. The Riyadh Metro Line 6 extension alone, worth USD 780 million, will connect industrial estates to the capital’s airport and cut logistics costs by 18%. Parallel builds at King Abdullah Port and King Abdulaziz International Airport lift container and passenger capacity to keep pace with maritime-air transshipment ambitions. Because design standards for these assets align with European and North American norms, tier-one global EPC firms remain deeply embedded, ensuring quality but increasing procurement complexity. Over the forecast, social infrastructure posts the fastest growth at a 6.11% CAGR, as new hospital clusters and 150 schools catch up with population gains and Vision 2030 quality-of-life metrics.

Increased allocation to oncology centers, cardiac units, and regional schools accelerates off-take for medical-grade HVAC, clean-room fit-outs, and modular classrooms, drawing mid-tier domestic firms into higher-value subcontracting. Public-private delivery cuts commissioning times by up to 18 months compared with traditional procurement, benefitting cash-flow-sensitive developers. Although utilities and extraction projects sit below transportation in the current market share, they are gaining share in the Saudi Arabia infrastructure construction market because battery storage, grid reinforcement, and hydrogen plants require specialized EPC inputs and command premium margins.

By Construction Type: New Builds Dominate, Renovation Gains Traction

New-build activity accounted for 76.7% of the 2025 value, consistent with the giga-project boom that defines the Saudi Arabia infrastructure construction market. King Salman International Airport, designed for 120 million passengers, illustrates the sheer scale: terminal shells, six runways, and inter-modal links spanning thousands of acres. Likewise, NEOM’s Green Hydrogen campus spans 300 square kilometers and integrates solar arrays, wind farms, and ammonia export jetties. Tangible spillovers include elevated demand for large-diameter pipe, high-strength concrete, and process-plant steel, locking in elevated volumes for domestic materials mills.

Renovation, however, advances fastest at a 6.44% CAGR because desalination retrofits, substation digitization, and wastewater upgrades help meet energy-efficiency targets without the complexity of greenfield projects. Reverse-osmosis conversions at legacy thermal desalination units cut power consumption by roughly one-third, freeing up natural-gas allocations for value-add petrochemical uses. Digital relays and SCADA overlays at 120 transmission substations reduce outage duration by 25%, curbing economic losses from blackouts. Because renovation work offers smaller ticket sizes and a quicker turnaround, it creates fertile ground for agile Saudi contractors who compete on speed and local regulatory fluency rather than scale.

By Investment Source: Public Leads, Private Accelerates Via PPPs

Public entities still fund 69.1% of 2025 output, anchored by ministry line items and PIF’s sizable balance sheet. Rail, airport, and grid megaprojects require sovereign guarantees to hit financial close at competitive borrowing rates. Nonetheless, private-sector capital routed through PPPs registers 6.81% CAGR through 2031, twice the pace of public disbursements, as concession-style mechanisms mature. The SAR 50 billion infrastructure fund, seeded by the National Development Fund, offers 30-year debt tenors indexed to inflation, enticing global pension funds hungry for predictable cash flows. Early successes, such as Riyadh’s 32-school bundle and Jeddah’s wastewater treatment concession, validate the model’s ability to accelerate delivery while transferring life-cycle risk off public ledgers.

Blended-finance structures also tap regional family offices for anchor equity in hospitality, hydrogen, and data-center builds, thereby diversifying ownership beyond legacy conglomerates. The Saudi Arabia infrastructure construction market size linked to PPP vehicles is therefore expected to surpass USD 25 billion by 2031, narrowing the public-private gap and fostering governance improvements through lender-driven oversight.

Geography Analysis

Riyadh’s 33.4% share in 2025 underscores its pull as the policy and finance center. The city houses flagship projects from airports to fintech campuses, with metro extensions knitting together industrial estates and the King Khalid International hub. Smart-city overlays increase fiber density and traffic-management sophistication, unlocking data for real-time optimization and lowering energy use per square foot. Social infrastructure advances through the 32-school PPP and tertiary-care expansions, aligning with municipal targets for health-care coverage and classroom ratios.

On the Red Sea coast, Jeddah leverages its maritime heritage and its status as a pilgrimage gateway. Terminal expansion to 80 million annual passengers dovetails with integrated high-speed rail to Mecca and Medina, relieving seasonal road congestion. Mixed-use regeneration of the historic downtown injects retail, cultural venues, and mid-scale hotels, diversifying the hospitality mix, which was previously skewed toward luxury resorts. Wastewater-to-reuse concessions lower potable-water demand by 15%, mitigating desalination strain in a city forecast to top 6 million residents by 2030.

Eastern Province’s Dammam and Jubail corridor surges on hydrocarbon-adjacent capex. Carbon-capture complexes, blue-hydrogen derivatives, and petrochemical expansions deepen vertical integration from feedstock to finished polymers. Precast and specialized-steel factories open in lockstep, shortening lead times for industrial modules and raising local content. Port investments add 5 million TEU of capacity at King Abdullah Port, positioning it as a viable Red Sea transshipment alternative and shaving voyage times to the Suez Canal chokepoint. Collectively, these drivers set Dammam on the fastest growth path in Saudi Arabia’s infrastructure construction market through 2031.

Competitive Landscape

Fragmentation is a defining feature of Saudi Arabia’s infrastructure construction market, with no small group of contractors exercising dominant control. Market concentration levels resemble those seen in mature European construction markets rather than the more consolidated structures typical of Gulf hydrocarbon economies. International EPC giants such as Bechtel, Parsons, Hyundai E&C, Samsung C&T, and China State Construction Engineering Corp secure packages above USD 1 billion by bundling design, finance, and operations expertise, de-risking delivery for sovereign owners. Saudi Grade 1 firms partner with these incumbents to gain know-how in building information modeling (BIM) and digital twin deployment, gradually narrowing capability gaps.

Technology adoption increasingly separates winners from laggards. Mandatory BIM on packages above USD 27 million slashes design clashes by 20% and trims rework budgets, while modular construction from El Seif’s new Dammam precast plant cuts on-site assembly schedules by the same margin. Only a dozen contractors possess the process-engineering capacity for CO₂ capture trains or hydrogen electrolyzers, leaving those pioneers to command above-average margins. Mid-tier Saudi builders thrive in the renovation niche: substation retrofits, ISO 14001 compliance upgrades, and reverse-osmosis conversions require agility and intimate regulatory familiarity more than balance-sheet heft.

Strategic moves in 2025-2026 further tilt the field. Nesma & Partners’ 40% acquisition of Al-Khodari & Sons brings mechanical-electrical-plumbing depth at a time when utility concessions are mushrooming. Saudi Binladin Group’s post-restructuring alliance with Bechtel on Qiddiya signals an appetite for risk-sharing joint ventures that blend local market access with global best practice. International newcomers eye data-center shells and battery-storage clusters as PIF shifts into AI and grid flexibility, tempting telecom-civil hybrids into what was once a petrochemical-dominated scene.

Saudi Arabia Infrastructure Construction Industry Leaders

Saudi Binladin Group

Nesma & Partners Contracting

El Seif Engineering Contracting

Al Ayuni Investment & Contracting

Al Fouzan Trading & General Construction

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Parsons won a USD 620 million smart-city backbone in Riyadh, installing fiber optics, IoT sensors, and digital-twin analytics across 150 km² to curtail congestion and reduce electricity consumption.

- February 2025: Bechtel secured the USD 1.2 billion NEOM utilities Phase 2 package, focusing on roads and backbone services for future industrial tenants.

- February 2025: Samsung C&T clinched a USD 950 million Red Sea resort project, financed in part by regional family offices.

- February 2025: Nesma & Partners bought 40% of MEP firm Al-Khodari & Sons for USD 85 million to expand integrated EPC coverage.

Saudi Arabia Infrastructure Construction Market Report Scope

The Saudi Arabia Infrastructure Construction Market encompasses the planning, development, maintenance, and modernization of essential infrastructure assets and systems across the Kingdom. This includes activities such as the construction and expansion of road and rail networks, development of power generation and transmission facilities, water desalination and distribution systems, wastewater treatment infrastructure, and social infrastructure required to support population growth and economic diversification.

The study provides a comprehensive assessment of the Saudi Arabian infrastructure construction market, examining prevailing market dynamics, key growth drivers and constraints, regulatory and policy frameworks, technological advancements, and an in-depth analysis of major market segments and the competitive landscape.

The Saudi Arabia Infrastructure Construction Market Report is Segmented by Infrastructure Segment (Transportation, Utilities, Social, Extraction), by Construction Type (New Construction, Renovation), by Investment Source (Public, Private), and by Geography (Riyadh, Jeddah, DMA, Rest of Saudi Arabia). The Market Forecasts are Provided in Terms of Value (USD).

By Infrastructure Segment

| Transportation Infrastructure |

| Utilities Infrastructure |

| Social Infrastructure |

| Extraction Infrastructure |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By City

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Infrastructure Segment | Transportation Infrastructure |

| Utilities Infrastructure | |

| Social Infrastructure | |

| Extraction Infrastructure | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By City | Riyadh |

| Jeddah | |

| DMA (Dammam Metropolitan Area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

What is the projected value of the Saudi Arabia infrastructure construction market in 2031?

It is forecast to reach USD 87.89 billion by 2031, expanding from USD 68.47 billion in 2026 at a 5.12% CAGR.

Which infrastructure segment leads by 2025 market share?

Transportation infrastructure leads with 46.3%, reflecting heavy investment in rail, ports, airports, and metros.

Which construction type is growing fastest to 2031?

Renovation work shows the highest growth, advancing at a 6.44% CAGR as legacy desalination plants, substations, and wastewater facilities undergo efficiency upgrades.

How important are PPPs to future project delivery?

PPP-structured projects funded by the National Development Fund and INFRA program are growing at a 6.81% CAGR, outpacing publicly funded builds and broadening access to global capital.

Which Saudi city will grow the fastest in infrastructure construction spending?

The Dammam metropolitan area is expected to post a 7.09% CAGR through 2031, buoyed by carbon-capture and petrochemical expansions.

What factors are restraining market growth?

Skilled-labor shortages, double-digit material inflation, and extended environmental-permitting timelines together shave an estimated 2.7 percentage points off potential CAGR.

Page last updated on: