India Bed And Bath Linen Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

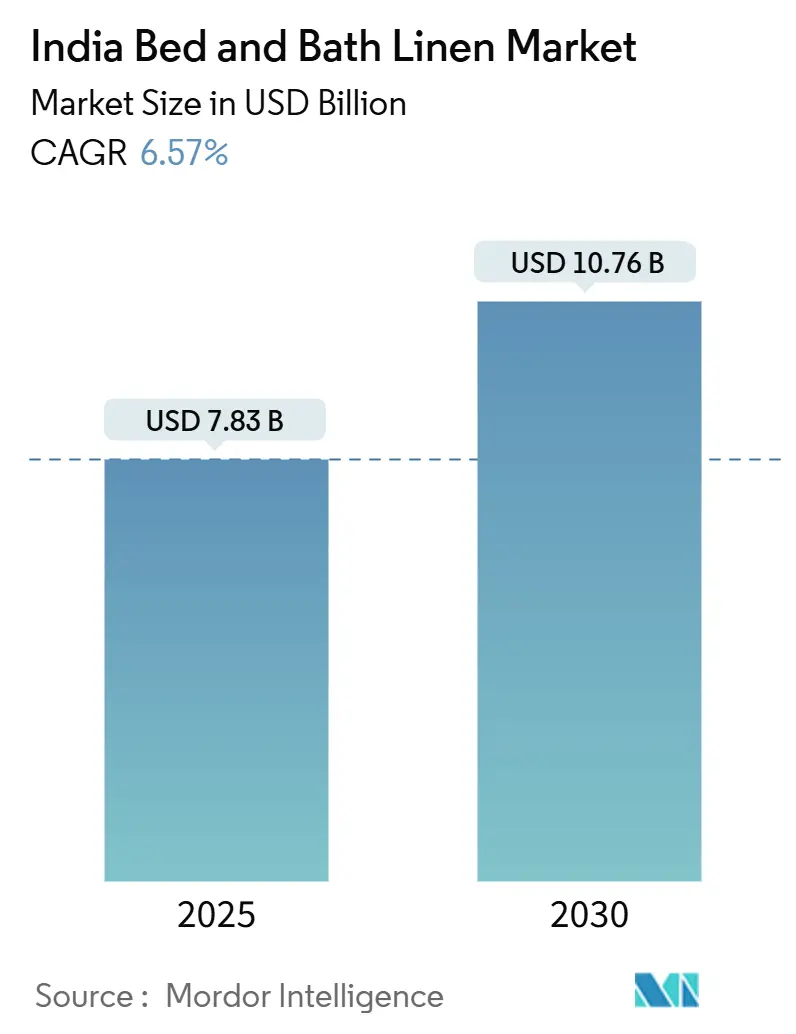

| Market Size (2025) | USD 7.83 Billion |

| Market Size (2030) | USD 10.76 Billion |

| Growth Rate (2025 - 2030) | 6.57% CAGR |

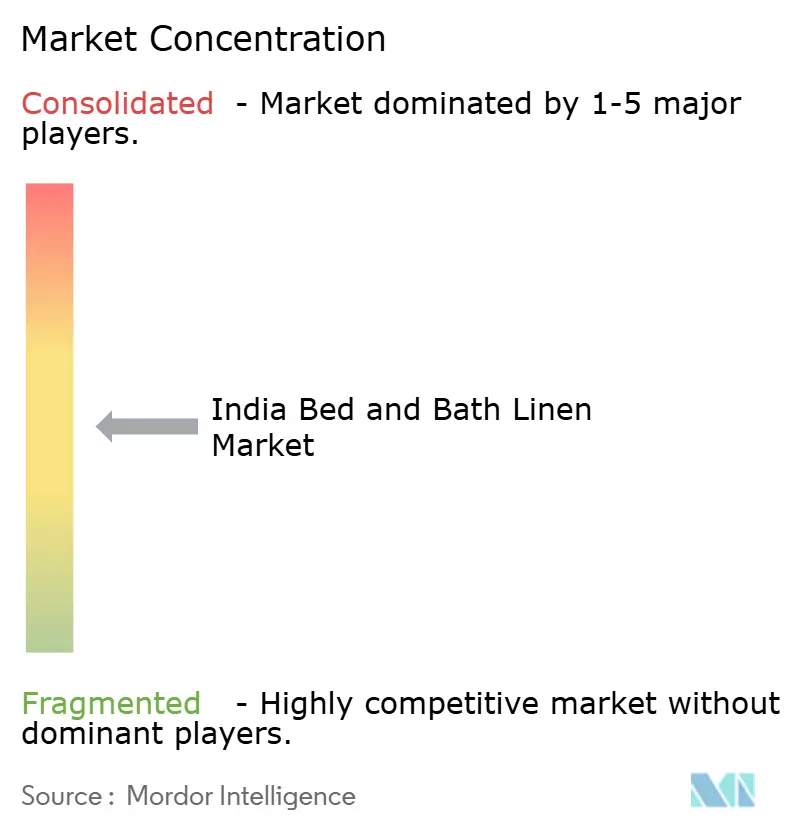

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Bed And Bath Linen Market Analysis by Mordor Intelligence

The India bed and bath linen market size stood at USD 7.83 billion in 2025 and is forecast to reach USD 10.76 billion by 2030, reflecting a 6.57% CAGR over the period. Growth for the India bed and bath market rides on post-G20 hospitality refurbishments, resilient cotton output, and premiumization that elevates thread-count expectations in urban homes. Established textile clusters in Tamil Nadu, Gujarat, and Maharashtra sustain cost efficiency while government incentives, such as the April 2024 duty-drawback hike for cotton linens, improve export margins. E-commerce is widening consumer access in Tier-2 and Tier-3 cities as smartphone adoption surpasses 750 million users, while sustainability trends are spurring interest in bamboo and modal fibers despite their price premium. Competitive intensity remains moderate, with Welspun, Trident, and Indo Count using vertical integration to offset cotton-price volatility and to serve emerging direct-to-consumer niches.

Key Report Takeaways

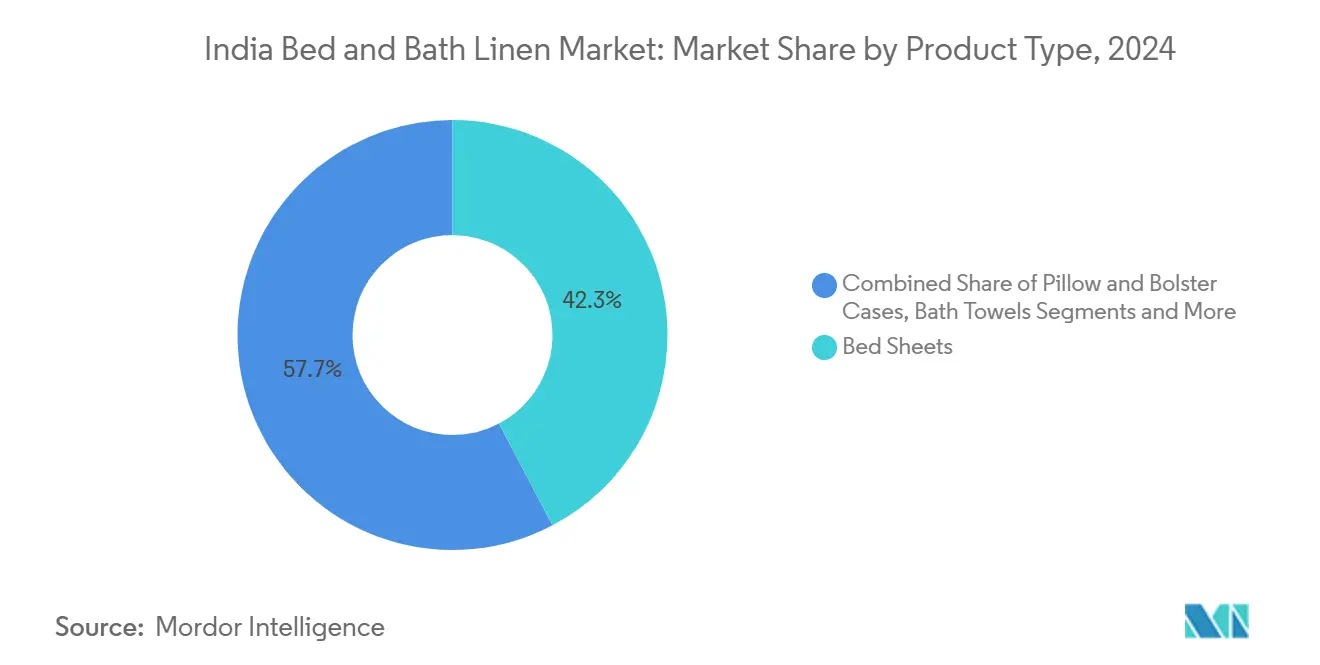

- By product type, bed sheets held 42.3% of India bed and bath market share in 2024, whereas duvet and quilt covers are projected to clock a 7.85% CAGR to 2030.

- By material, cotton dominated 62.5% of the India bed and bath market size in 2024, while bamboo and modal fibers are on track for an 8.12% CAGR through 2030.

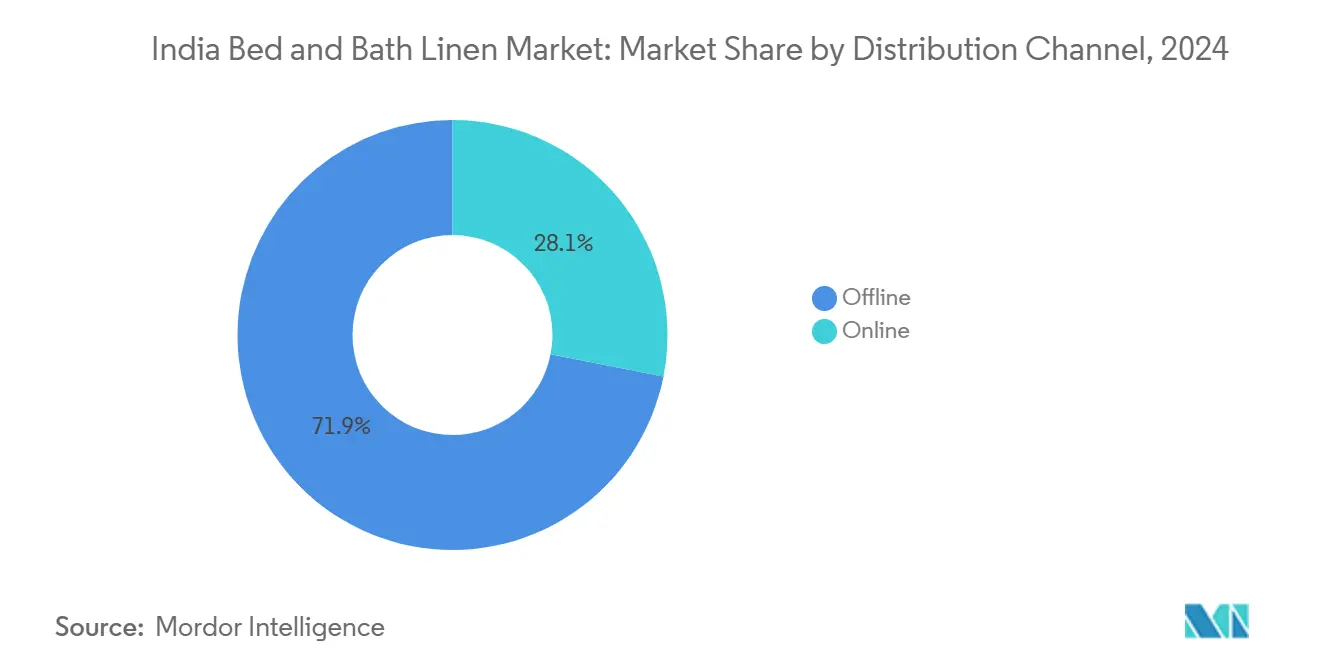

- By distribution channel, offline retail commanded 71.9% revenue share in 2024; online channels are advancing at an 8.83% CAGR on widening logistics coverage.

- By end user, residential accounted for 64.2% of India bed and bath market size in 2024, whereas hospitality is forecast to expand at 6.91% CAGR as tourism rebounds.

- By region, South India led with 30.2% revenue share in 2024, yet West India is poised for a 7.13% CAGR on the back of Gujarat’s 2024 textile-policy incentives.

India Bed And Bath Linen Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hospitality refurbishments post-G20 | 1.2% | National, concentrated in Delhi, Mumbai, Bengaluru | Medium term (2-4 years) |

| Growth of organized retail chains | 0.9% | Urban centers, expanding to Tier-2 cities | Long term (≥ 4 years) |

| E-commerce penetration in Tier-2 & Tier-3 cities | 1.1% | National, with early gains in UP, Bihar, Odisha | Short term (≤ 2 years) |

| Premium home-fashion influence from OTT interiors shows | 0.8% | Urban metros, spreading to Tier-1 cities | Medium term (2-4 years) |

| Expansion of cotton-poly rich blends for quick-dry bath towels | 0.7% | Manufacturing hubs in Gujarat, Tamil Nadu | Long term (≥ 4 years) |

| Green building certification pushing OEKO-TEX linen demand | 0.6% | Commercial centers, premium residential projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hospitality Refurbishments Post-G20

India’s G20 presidency heightened global visibility for local hotels, motivating chains to commit capex for full-scale linen upgrades that encompass sheets, towels, and bathrobes over the next 18–24 months [1]India Brand Equity Foundation, “Hospitality Sector Overview 2024,” ibef.org. Developers have 88,706 new keys in the pipeline, but just as critical is the refurbishment of the 180,403 existing rooms that must now meet higher thread-count and OEKO-TEX certification norms to retain franchise contracts with international operators. Procurement teams have begun moving from 210-TC basics to 300-TC cotton-poly blends that withstand 150 industrial washes, driving up per-room textile budgets by nearly 22% versus 2023. Bulk orders also cover institutional laundries and linen-rental firms, which in turn spur repeat demand because commercial laundering shortens product life cycles by 15–18%. Secondary business hubs such as Jaipur, Kochi, and Indore are adopting similar standards to attract MICE events, widening geographic demand beyond the traditional metro focus.

Growth of Organized Retail Chains

Although leading fashion retailers trimmed underperforming outlets in 2024, floor space in high-performing Tier-1 and Tier-2 malls actually rose, enabling larger “home zones” that dedicate up to 20% more shelf length to bed and bath SKUs[2]The Economic Times, “Retail Chains Rationalize Stores Amid Weak Demand,” economictimes.indiatimes.com. Chains now insist on exclusive colorways and seasonal drops, prompting mills to speed design-to-shelf cycles from 180 to 120 days through digital printing investments. Private-label collaborations give retailers margin lifts of 8-10 percentage points while locking in suppliers for three-year tenures, creating a predictable volume base for vertically integrated players. Experiential store concepts, complete with AR-enabled fabric visualizers and mock bedroom vignettes, elevate shopper dwell time and ticket size, especially for coordinated sheet-pillow sets. Retailers use loyalty apps to push targeted coupons, which data show lift conversion by 14% among repeat home-textile buyers.

E-commerce Penetration in Tier-2 & Tier-3 Cities

Improved logistics corridors and same-day delivery promises from carriers such as Delhivery have cut last-mile costs by 12% in the past year, making home-textile shipping to smaller towns viable at sub-INR 60 per parcel. Smartphone penetration exceeding 750 million users means rural consumers can now comparison-shop SKUs and prices once found only in metros, creating a fresh demand pool for bundled sheet-and-towel value packs. Cash-on-delivery still represents roughly 35% of bedding orders in Uttar Pradesh and Bihar, but digital payment uptake is climbing fast due to UPI-linked cashback schemes that boost average order value by 9%. High return rates, currently near 12% for linens, are being tamed through AI-driven size guides and 360-degree fabric zooms, cutting mismatched-color complaints by 3 percentage points quarter on quarter. Marketplace algorithms now spotlight OEKO-TEX badges, educating consumers and nudging them toward higher-value certified products

Premium Home-Fashion Influence from OTT Interiors Shows

Streaming platforms such as Netflix and Amazon Prime have turned décor series into taste-making engines, compressing trend cycles to less than six months and creating viral demand spikes for colors like sage green and terracotta. Influencer-led design drops often sell out within weeks, pushing manufacturers to earmark up to 15% of capacity for quick-turn production runs that rely on digital printing to slash sampling lead times. Social media amplification boosts duvet-cover sales, the most visual SKU. However, the hype also inflates inventory risk; brands counter by redirecting slow-moving designs to flash-sale platforms at steep discounts, a tactic that preserves cash flow but crimps margins by 5–7%. Retailers increasingly demand data on Pinterest and Instagram trend velocity before committing shelf space, formalizing a digital-first forecasting approach.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cotton prices | -1.4% | National, acute in cotton-producing states | Short term (≤ 2 years) |

| Slow adoption of bamboo fibre due to higher ASP | -0.8% | Urban premium markets, limited rural penetration | Medium term (2-4 years) |

| Water-intensive processing regulations are tightening | -0.7% | Manufacturing clusters in Gujarat, Tamil Nadu | Long term (≥ 4 years) |

| Fragmented, unorganized sector price under-cutting | -0.9% | National, concentrated in price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Cotton Prices

Spot cotton prices swung 15–20% in 2024, forcing mills to renegotiate yarn contracts almost monthly and dealers to re-label MRPs multiple times per season[3]India Brand Equity Foundation, “Cotton Procurement Under MSP 2024,” ibef.org. The Cotton Corporation of India cushioned growers by procuring 525 lakh quintals at MSP, yet mills still struggled with working-capital spikes that inflated interest costs by up to 150 basis points. SMEs lacked the financial muscle to hedge on commodity exchanges, leading some to cut loom shifts by 20% during peak volatility periods, which in turn delayed retailer replenishment cycles. Brands tried blending polyester to tame cost spikes, but consumer preference for 100% cotton in premium bed-sheet lines limited substitution scope. Frequent price tags on store shelves eroded shopper trust and nudged them toward promotional events, compressing retailer gross margins. Overall, cotton volatility is projected to shave roughly 1.4% off the market’s CAGR in the short term.

Slow Adoption of Bamboo Fibre Due to Higher ASP

Bamboo-derived rayon commands 20–30% premiums over cotton, limiting mass-market traction even though consumers appreciate its moisture-wicking and antibacterial properties. Domestic bamboo fiber capacity remains nascent; most yarn is imported from China and Vietnam, exposing mills to forex swings and four-week lead times that complicate demand planning. Retailers often allocate only one or two facings to bamboo SKUs because the higher ticket prices depress turnover rates compared with cotton counterparts. Brands must therefore spend heavily on point-of-sale education and influencer campaigns to communicate the fiber’s sustainability narrative, diluting already thin margins. Additionally, state-level regulations on bamboo cultivation vary widely, making backward integration risky for mills considering plantation investments.

Segment Analysis

By Product Type: Bed Sheets Lead Volume, Duvets Drive Innovation

Bed sheets contributed 42.3% to the India bed and bath market size in 2024. Mid-income households replace them every 2-3 years, bolstering continual baseline demand. Higher urban exposure to 500-thread-count narratives on OTT décor shows is nudging consumers toward sateen and percale upgrades. Organized brands leverage bundle pricing of sheet-pillowcase sets to lift ticket values. Simultaneously, India's bed and bath market growth in duvet and quilt covers is projected at 7.85% CAGR, aided by colder-climate AC usage in metros and aspirational layering aesthetics. Duvets also appeal to gift buyers during festive seasons, expanding peak-season volumes. Pillow and bolster cases grow in lockstep with sheet cycles, while mattress protectors benefit from rising mattress-replacement frequency linked to back-care awareness. Quick-dry bath towels adopt cotton-poly blends that cut tumble-dry minutes by 25%, answering sustainability calls and aligning with energy-starred washing machines.

The India bed and bath linen market landscape for bathrobes and bath mats remains niche yet offers margin headroom. Luxury hotel chains routinely order monogrammed robes as brand markers, while high-rise apartments demand slip-resistant bath mats for safety compliance. Product innovation around anti-microbial silver finishes commands 10% price premiums without major capex, encouraging mid-scale mills to diversify. Indo Count’s July 2025 Wamsutta relaunch underscores the premiumization pathway, pairing heritage branding with Egyptian-cotton SKUs. Small-batch design drops exploit the Instagram-centric discovery journey, though rapid obsolescence tests inventory discipline.

By Material: Cotton Dominance Faces Sustainable Challenge

Cotton held 62.5% of India bed and bath market share in 2024. Domestic output of 302.25 lakh bales underpins supply stability, but water-use scrutiny and farm-gate price volatility drive interest in blends. Polyester mixes lower shrinkage and speed drying, securing a role in entry-level towels and hospitality linens that face industrial laundering. Bamboo and modal fibers are on an 8.12% CAGR trajectory, spurred by wellness narratives around hypoallergenic benefits. Grasim’s record 810 KT cellulosic staple sales validate industrial momentum while OEKO-TEX guidelines nudge institutional buyers toward certified inputs.

Lyocell adoption is growing in premium sheets for its closed-loop processing and silk-like hand-feel, though cost barriers remain. Recycled PET yarns, as in GHCL’s “Rekoop,” strengthen circular-economy credentials and diversify raw-material exposure. Linen blends cater to boutique hotels targeting rustic aesthetics, yet limited flax cultivation keeps volumes low. The India bed and bath industry is witnessing more mills invest in dope-dyed yarn to cut water consumption by up to 90%, aligning material choices with ESG audits demanded by global buyers.

By Distribution Channel: Offline Resilience Meets Digital Acceleration

Offline formats generated 71.9% of India bed and bath market revenue in 2024. The tactile nature of sheet-buying keeps footfall robust in home centers where shoppers judge weave density by touch. Specialty chains curate visual merchandise pods that mimic bedroom settings, feeding impulse purchases. Mass merchandisers rely on value-pack promotions during festive periods, accounting for 40% of annual volume in some northern states. The India bed and bath market nevertheless records an 8.83% CAGR in online sales due to smartphone penetration exceeding 60% and one-day delivery badges expanding to 19,000 pin codes.

Click-and-mortar models flourish as brick-based retailers launch apps offering exclusive colorways not found in stores, driving omnichannel AOV uplift. Direct-to-consumer brands bypass wholesale margins, funneling savings into influencer partnerships that reach niche décor communities. Yet return logistics average 12% of GMV for bedding categories, pushing platforms to invest in AI sizing aids and 360-degree fabric zooms. Institutional procurement portals gain ground, linking hotels and hospitals to mills through reverse-auction modules that compress tender cycles from months to days.

By End User: Residential Stability, Hospitality Recovery

Residential demand accounted for 64.2% of India bed and bath market size in 2024, supported by rising household formation and gift-oriented festival spending. Urban nuclear families allocate higher discretionary outlays for bedroom aesthetics, evident in the proliferation of coordinated sheet-duvet sets. Replacement frequency remains sticky, but premium upgrade cycles shorten as disposable incomes rise. Hospitality segment demand is forecast to grow at a 6.91% CAGR through 2030, mirroring expansion in business travel corridors and luxury resort pipelines.

B2B buyers prioritize durability and chlorine-resistant colors, steering mills toward vat-dyed cotton that withstands 100 industrial wash cycles. Healthcare and institutional buyers value antimicrobial finishes compliant with NABH guidelines, sustaining volume for white towel and sheet SKUs. Educational hostels and defense barracks add baseline bulk orders, though margins trail consumer categories. Himatsingka Seide leverages Calvin Klein and Tommy Hilfiger licenses to capture aspirational domestic consumers while exporting hospitality-grade linens to North America, balancing cyclical exposure.

Geography Analysis

South India’s 30.2% revenue share in 2024 stems from decades-old clusters in Tamil Nadu, Karnataka, and Andhra Pradesh, where fiber-to-fabric integration compresses order-fulfillment cycles. State incentive schemes under the Comprehensive Integrated Textile Parks program increase water-recycling adoption, improving ESG scores sought by export clients. Port proximity in Chennai and Kochi grants mills a freight advantage of USD 75 per container over inland rivals, preserving margin headroom. Labor retention benefits from generational skill transfer, yet rising urban wages and migration to IT services could tighten loom-floor staffing in the long run.

West India’s 7.13% CAGR through 2030 underscores Gujarat’s textile-policy subsidies that grant 6% interest reimbursements on term loans for new looms. Surat’s synthetic yarn know-how opens hybrid-towel innovation, while Maharashtrian mills gain from Mumbai’s finance ecosystem, easing working-capital lines. The region’s dye-chemical proximity lowers input transit time, aiding faster shade-approval cycles for fashion-driven duvet covers. Government emphasis on technical-textile parks furthers capability diversification into moisture-management pillow protectors.

North India capitalizes on Delhi-NCR’s premium home décor consumption, with organized retail carpet area expanding by 1.3 million sq ft in 2025 alone. Growth also flows from religious-tourism hubs in UP that raise hotel linen orders. However, the distance from coastal ports inflates freight to EU buyers by USD 150 per TEU, partly offset by Dedicated Freight Corridor upgrades expected by 2027. East and North-East regions lag in volume but benefit from highway projects that cut transit to Kolkata port by 18% for Odisha-based weavers. Digital commerce fills physical-store gaps, letting Mizoram and Assam consumers access branded sheets within five-day delivery windows.

Competitive Landscape

The India bed and bath market is moderately concentrated. Welspun, Trident, and Indo Count wield cost advantages through vertically integrated spinning, weaving, and finishing capacities that lower per-meter costs by up to 12% versus standalone processors. Export orientation hedges currency risk, with Indo Count deriving 68% of FY25 revenue from North America. Domestic challenger brands leverage direct-to-consumer storefronts to bypass retail margins and create agile design drops tied to social-media trends.

Technology investment differentiates market leaders. Welspun’s patented Hygro-cotton uses hollow-core yarns that get softer after washing, enabling a 15% price premium. Trident deploys AI-enabled quality-inspection cameras that cut defect rates by 40%, translating into fewer chargebacks from large-format retailers. Sustainability credentials are turning into table stakes; GHCL’s Rekoop line uses recycled PET bottles, turning waste into soft bedding that satisfies corporate ESG audits.

Unorganized power-loom clusters, particularly in Erode and Bhiwandi, undercut pricing but face scaling limitations due to effluent rules and credit access. Regulatory tightening around zero-liquid-discharge plants may accelerate consolidation, giving capital-rich players room to expand their share. Strategic plays in 2025 include Indo Count’s Wamsutta premium relaunch and Raymond’s corporate demerger that unlocks focused capital for textile R&D. M&A interest from private equity circles around specialty bamboo-fiber mills signals incoming capacity alignment with sustainability trends.

India Bed And Bath Linen Industry Leaders

Welspun India Ltd

Trident Group

Indo Count Industries Ltd.

GHCL Home Textiles

Bombay Dyeing

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Indo Count Industries relaunched its Wamsutta brand to capture premium bedding demand in domestic and export markets.

- July 2025: D’Decor introduced FabriCare, aiming for INR 150 crore (USD 17.5 million) sales from easy-care upholstery and washable curtains backed by celebrity endorsements.

- May 2025: Raymond Limited completed the demerger of Raymond Realty, sharpening its strategic focus on core textiles and lifestyle verticals.

- April 2025: The Government of India raised duty-drawback rates on cotton bed and table linens from 2.6% to 3.0%, with the upper cap lifted to INR 68.9/kg, enhancing export competitiveness.

India Bed And Bath Linen Market Report Scope

| Bed Sheets |

| Pillow & Bolster Cases |

| Duvet/Quilt Covers |

| Mattress Protectors |

| Bath Towels |

| Hand & Face Towels |

| Bathrobes |

| Bath Mats |

| Cotton |

| Polyester |

| Bamboo/Modal |

| Linen Flax & Others |

| Offline | Mass Merchandisers (hypermarkets/supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Distribution Channels | |

| Online |

| Residential |

| Hospitality |

| Healthcare |

| Institutional/Others |

| North India |

| South India |

| West India |

| East & North-East India |

| By Product Type | Bed Sheets | |

| Pillow & Bolster Cases | ||

| Duvet/Quilt Covers | ||

| Mattress Protectors | ||

| Bath Towels | ||

| Hand & Face Towels | ||

| Bathrobes | ||

| Bath Mats | ||

| By Material | Cotton | |

| Polyester | ||

| Bamboo/Modal | ||

| Linen Flax & Others | ||

| By Distribution Channel | Offline | Mass Merchandisers (hypermarkets/supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Distribution Channels | ||

| Online | ||

| By End User | Residential | |

| Hospitality | ||

| Healthcare | ||

| Institutional/Others | ||

| By Region | North India | |

| South India | ||

| West India | ||

| East & North-East India | ||

Key Questions Answered in the Report

What is the current size of the India bed and bath market?

The India bed and bath market size reached USD 7.83 billion in 2025.

How fast will the sector expand by 2030?

It is projected to grow at a 6.57% CAGR, touching USD 10.76 billion by 2030.

Which product category is growing the fastest?

Duvet and quilt covers are forecast to record a 7.85% CAGR through 2030.

Why are bamboo and modal fibers gaining popularity?

They offer moisture-wicking and antimicrobial benefits that resonate with sustainability-minded consumers, supporting an 8.12% CAGR.

Which sales channel is accelerating the most?

Online retail is advancing at an 8.83% CAGR as e-commerce penetrates Tier-2 and Tier-3 cities.

Which region shows the highest growth momentum?

West India leads in growth potential with a 7.13% CAGR through 2030, driven by Gujarat’s 2024 textile-policy incentives.