Market Size of Grapes Value Chain Analysis

| Study Period | 2019 - 2029 |

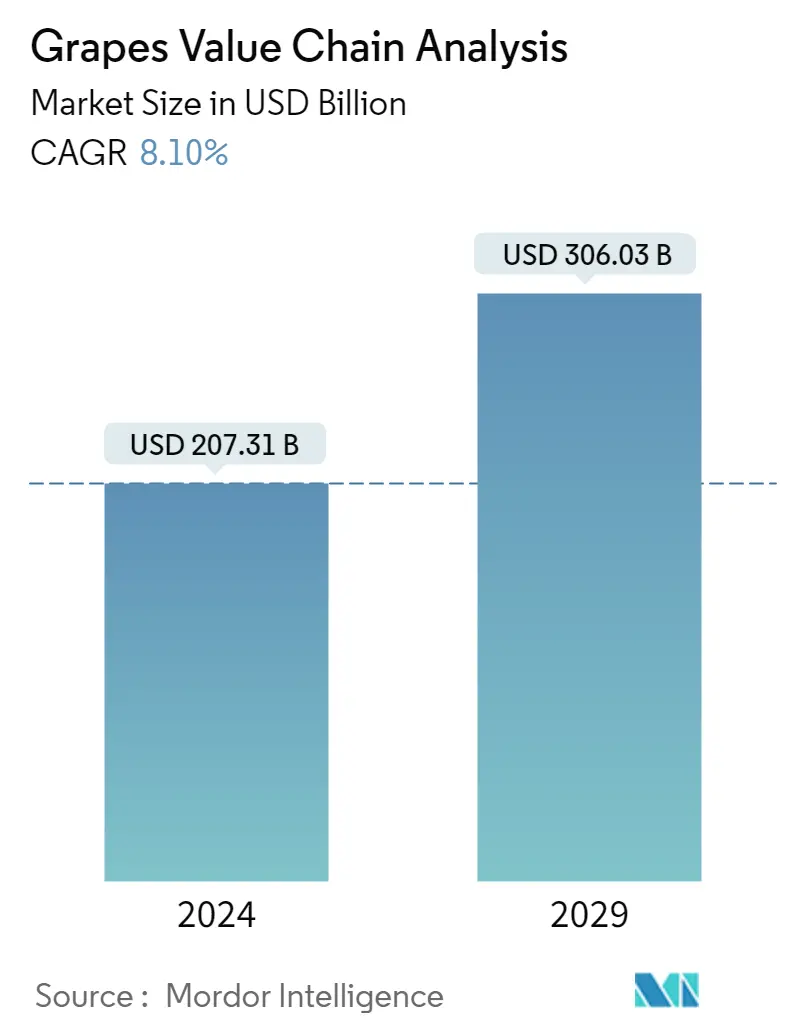

| Market Size (2024) | USD 207.31 Billion |

| Market Size (2029) | USD 306.03 Billion |

| CAGR (2024 - 2029) | 8.10 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Grapes Value Chain Analysis Market Analysis

The Grapes Market size is estimated at USD 207.31 billion in 2024, and is expected to reach USD 306.03 billion by 2029, growing at a CAGR of 8.10% during the forecast period (2024-2029).

- Grapes are one of the largest fruit crops, with approximately 6,729,198 hectares of area harvested worldwide in 2021. According to a United States Department of Agriculture report, global table grape production in 2021 reached about 25.5 million metric tons (MMT). Table grapes and wine grapes are the two major types of grapes grown worldwide, out of which table grapes are freshly consumable.

- The Farmers are the primary stakeholder in the grape value chain, and they involve in the process of production of grapes. Farmers incur various costs, including seed, labor, tractor, and transportation. Aggregators/farmer co-operatives are the stakeholders in the grape value chain next to farmers.

- After aggregators/farmer co-operatives exporters come into the role, the major exporters of grapes are the United States, Peru, Chile, and the Netherlands. The costs incurred by exporters include labor, transportation, overheads, bulk packaging, fertilizer, crop protection, and insurance charges. Exporters also pay insurance for the value of the commodity and vehicle they are exporting to safeguard the capital invested, despite the adverse situations during transport from one port to another.

- Moving forward in the chain, importers, and wholesalers come next to exporters. And the final stakeholders in the grape value chain are retailers. Costs incurred by the retailers include transportation, overheads, and packaging costs.

- Developing new varieties of fresh grapes requires significant investment and experimentation. The R&D activities and launching of. It produces grapes varieties tiesfreshmanainly being carried out around the globe by public and private firms for future development in the grape market. For instance, recently, Embrapa, the Brazilian Agricultural Research Corporation, Semiárido unveiled the first table grape variety BRS Tainá to be bred exclusively for production in the northeast of Brazil. BRS Tainá is a white seedless variety with a 'neutral and pleasant flavor,' developed to suit the growing conditions in the Sào Francisco Valley. It is also a fast-growing, vigorous variety with an average yield of 25 tonnes per hectare per production cycle,' medium-sized bunches weighing around 270g and measuring 15cm x 10cm.