Market Trends of Europe Building & Construction Sheets Industry

This section covers the major market trends shaping the Europe Building & Construction Sheets Market according to our research experts:

Rise in Construction Equipment Sales

Construction was the most important end-user industry for sheets in 2021, accounting for almost 75% of the market. Sheets are utilised in flooring, walls & ceiling, windows, doors, roofing, building envelop, electrical, heating, ventilation, and air-conditioning (HVAC) and plumbing applications in the building sector because of their light weight, ease of installation, and energy-saving properties. Fences and walls are also used in both residential and commercial construction projects.

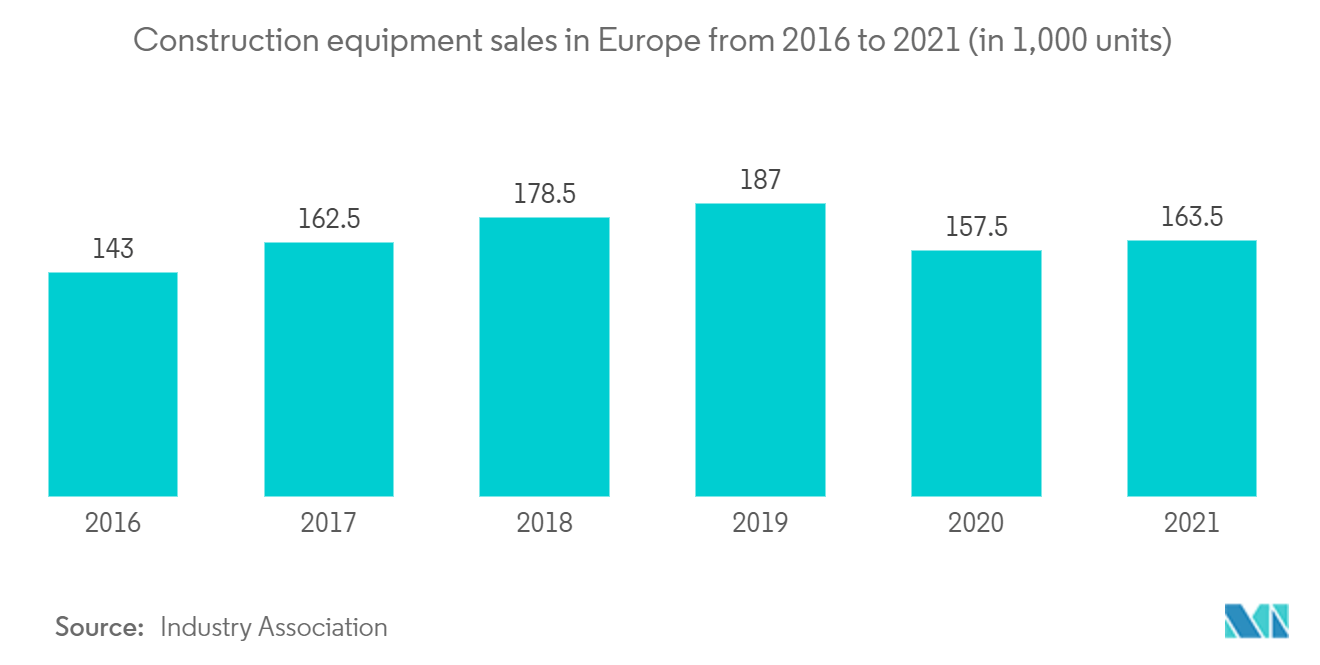

Construction equipment sales in Europe rose steadily until 2019, when they peaked. However, the business saw a significant fall in 2020 and 2021 after the COVID-19 pandemic. By 2025, it is expected that sales in this industry would not rebound to their pre-COVID-19 levels. 2021 saw consistent trends across the equipment sub-sectors with all product segments recording growth in sales of between 22% and 30%. Concrete machinery saw the strongest growth, slightly above the levels seen in the other sectors. The figures surely include a statistical 'base effect' of yearly comparison, with the enormous drop of the first pandemic lockdown in 2020. However, after weathering the Covid crisis, underlying demand within the industry has remained strong and is on track to close the gap with record sales levels of 2017.

From a regional perspective, the markets that were hit hardest in 2020 - particularly the UK and Spain - saw the best performances in 2021. Southern Europe and CEE markets saw above-average growth in sales, and even the mature markets in Northern Europe saw similar levels of recovery. None of the markets saw a fall in sales in 2021, and the only market that experienced single-digit growth was the high-volume German market. The fact that it has still not reached saturation levels can be considered a positive outcome. Turkey continued its recovery from the catastrophic levels of decline seen in 2018/19 and saw the highest levels of growth across the market regions.

Providing an outlook for European construction equipment market in 2022, according to European construction equipment association CECE, the business climate index for the industry recorded its highest ever value in the July 2021 survey and maintained extremely high levels throughout the rest of the year. In the first two months of 2022, there was another small improvement both for the current business situation and future sales expectations. European manufacturers hope that supply-side bottlenecks will create less concerns for the rest of the year. CECE says the demand-side clearly remains strong, as all equipment sub-sectors were expecting business to improve in the months leading up to the summer of 2022.

Increasing Demand for sheets in the Residential Construction Industry

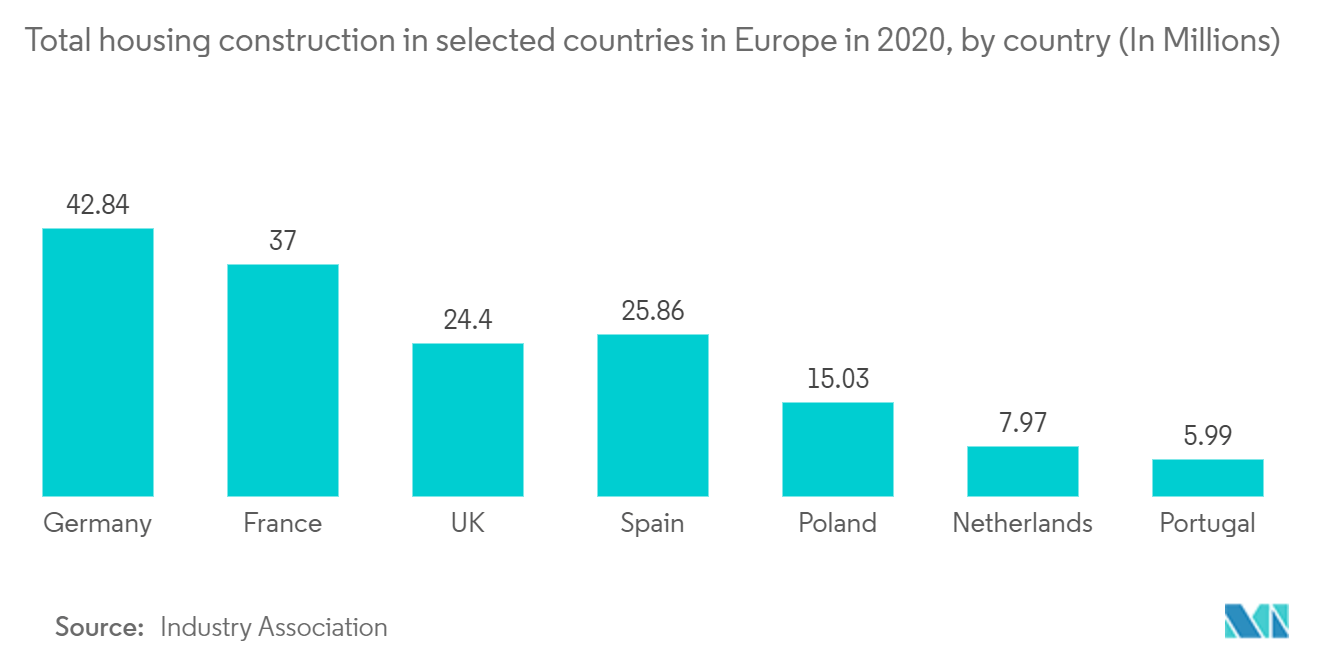

With a total of around 43 million dwelling units in 2020, Germany has the greatest housing stock among European countries. France, Spain, and the United Kingdom were also at the top of the list. This is unsurprising, given that the top four countries have some of Europe's largest populations. In different countries, the supply of new dwellings varies substantially. Poland and France had the most number of house completions in 2020, but Romania had the highest number of construction starts, leaving Poland and France in second and third place, respectively.

The residential sector has seen the biggest rise in investment volumes of any real estate asset class in Europe over the last investment cycle, accounting for 22% of investment activity in 2020, up from a mere 8% in 2009. Its defensive qualities led investors to increase spending in the sector during 2020, to some 18% above the five-year average. In terms of fresh capital, there is over EURO 60 billion in funds being raised with a focus on the sector - matching the amount invested in 2020 - as investors consider a range of asset types and routes to market, including the build-to-rent, build-to-sell, private rented, co-living, senior and student housing residential niches.

While the raft of new capital looking to invest in the residential sector points to greater diversity, this comes on the back of more consolidation of assets under management among the biggest residential landlords in Europe. Companies like Blackstone, AXA REIM, Union Investment, Greystar and Roundhill Capital have been busy building their portfolios. Swedish investor Heimstaden has been actively growing its presence across Europe over the last few years, and now sits firmly in second place at the top of the 'net investor' charts with a reported EURO 13.8 billion of assets under management. The recently proposed merger of Vonovia and Deutsche Wohnen will create a EURO 20 billion+ asset-rich investor that will be one of the most powerful players in Berlin's property market, Germany's biggest listed residential landlord and Europe's largest private residential landlord.