Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 28.83 Billion |

| Market Size (2030) | USD 38.67 Billion |

| Growth Rate (2025 - 2030) | 6.05% CAGR |

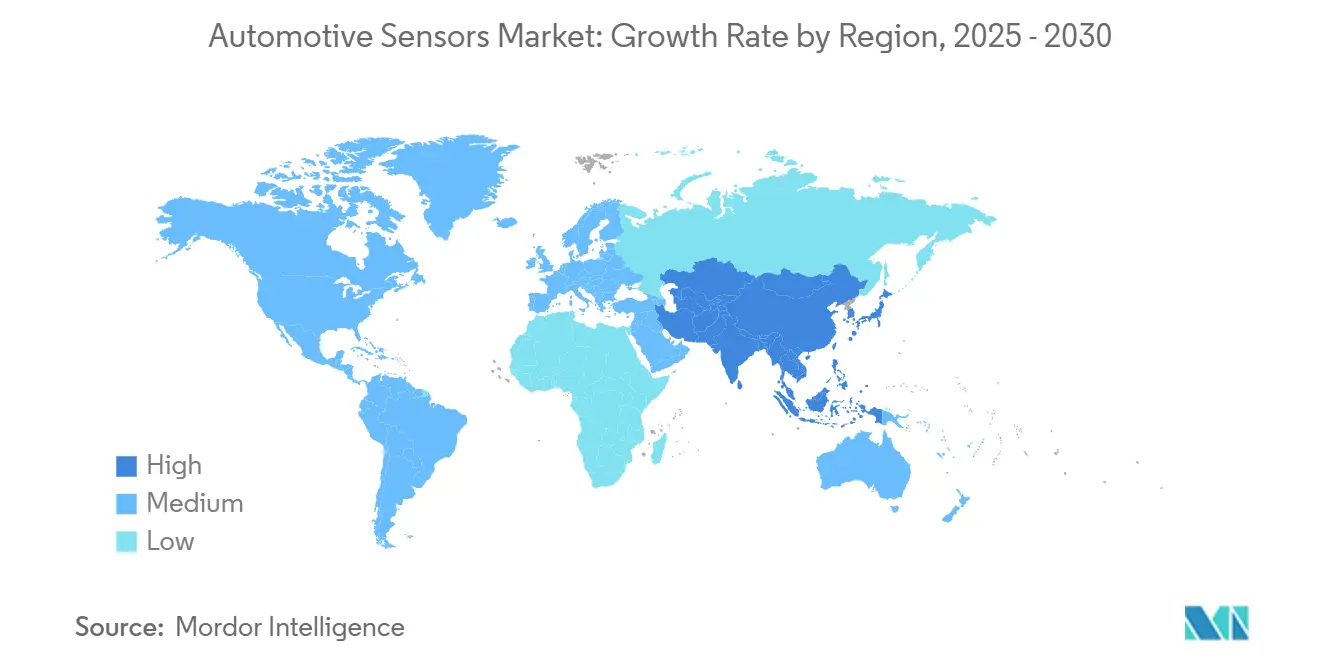

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

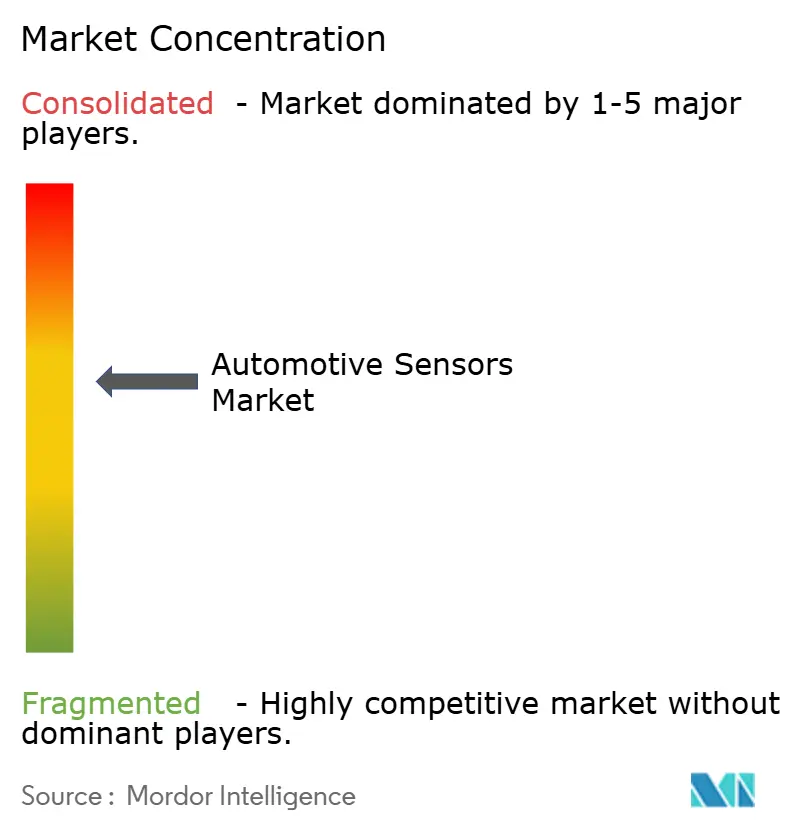

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Sensors Market Analysis by Mordor Intelligence

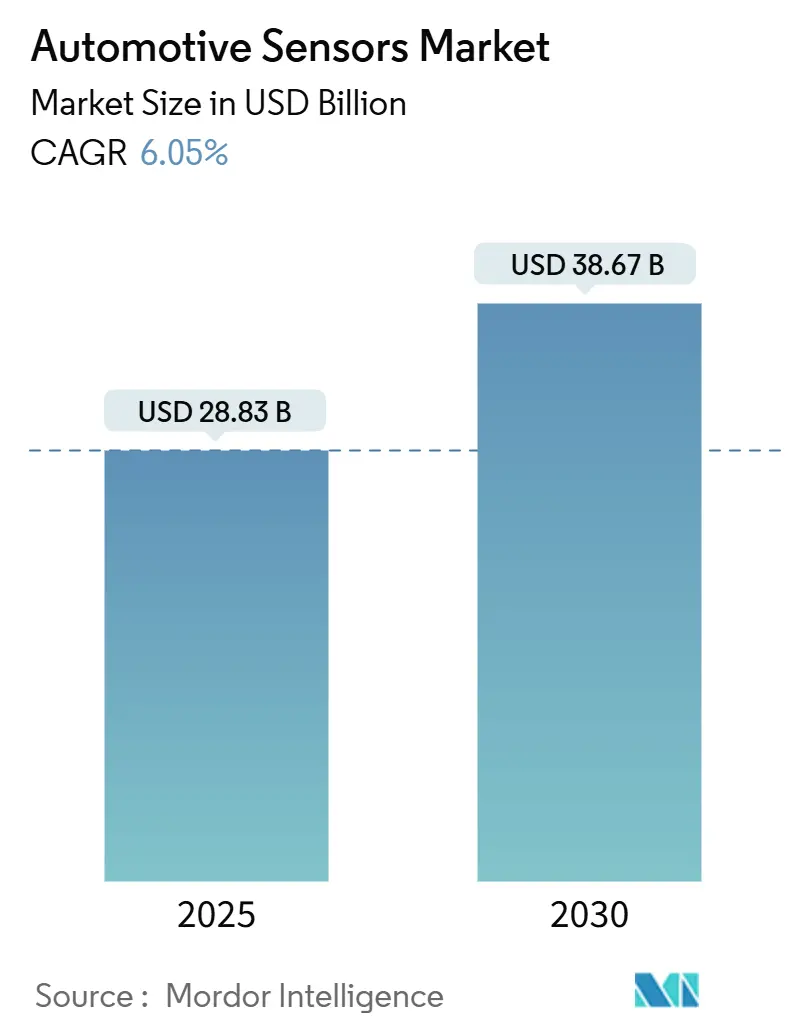

The automotive sensors market reached USD 28.83 billion in 2025 and is forecast to climb to USD 38.67 billion by 2030 on a 6.05% CAGR. The market’s growth is anchored in accelerating deployments of advanced driver-assistance systems (ADAS), electrification mandates that add new sensing points, and the semiconductor industry’s ability to deliver cost-effective micro-electromechanical systems (MEMS) at scale. Momentum also reflects the shift from mechanical to electronic sensing, particularly in propulsion systems, where premium-priced perception technologies replace legacy components. Regulatory pressure for emissions reduction and crash-avoidance performance keeps demand steady, while falling average selling prices (ASPs) for MEMS lower adoption barriers across vehicle segments. The automotive sensors market, therefore, evolves from basic measurement functions toward intelligent, connected edge devices able to process data locally.

Key Report Takeaways

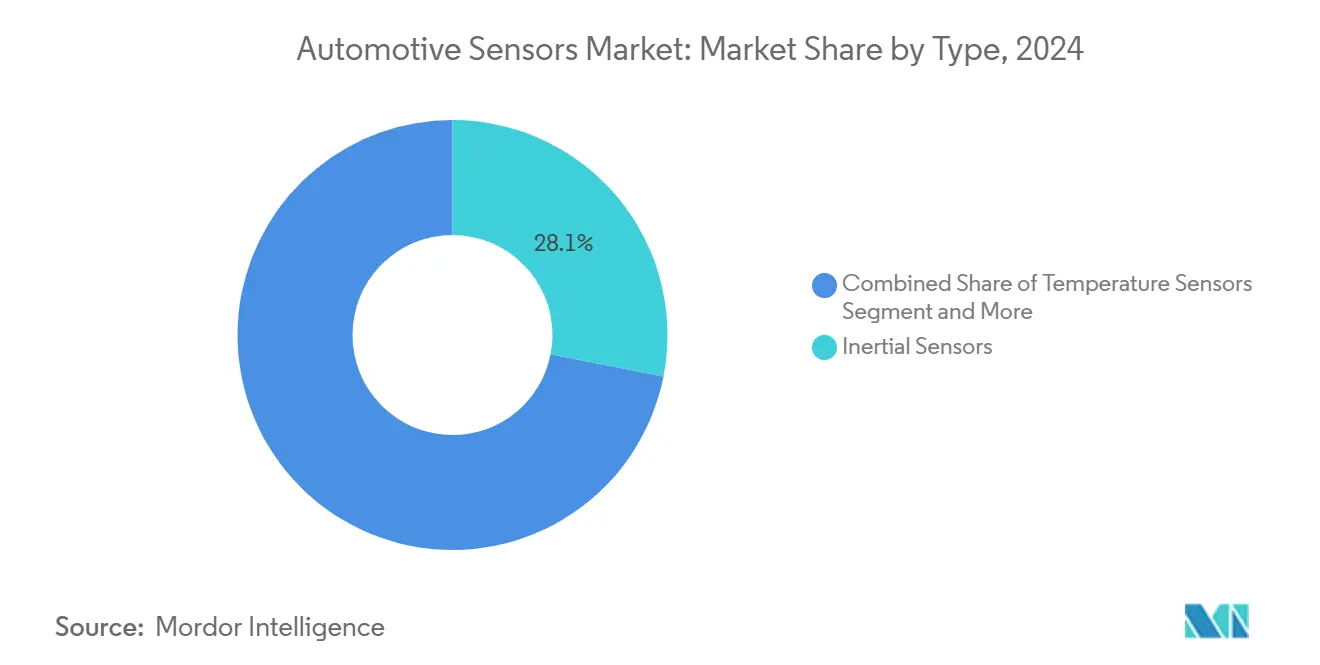

- By type, inertial sensors led the automotive sensors market with 28.13% of the share in 2024 and are growing at a 6.47% CAGR to 2030.

- By application, the powertrain segment held 40.55% of the automotive sensors market size in 2024, while telematics recorded the fastest 8.86% CAGR through 2030.

- By vehicle type, passenger cars commanded 71.18% revenue share in 2024; commercial vehicles are expanding at a 7.15% CAGR to 2030.

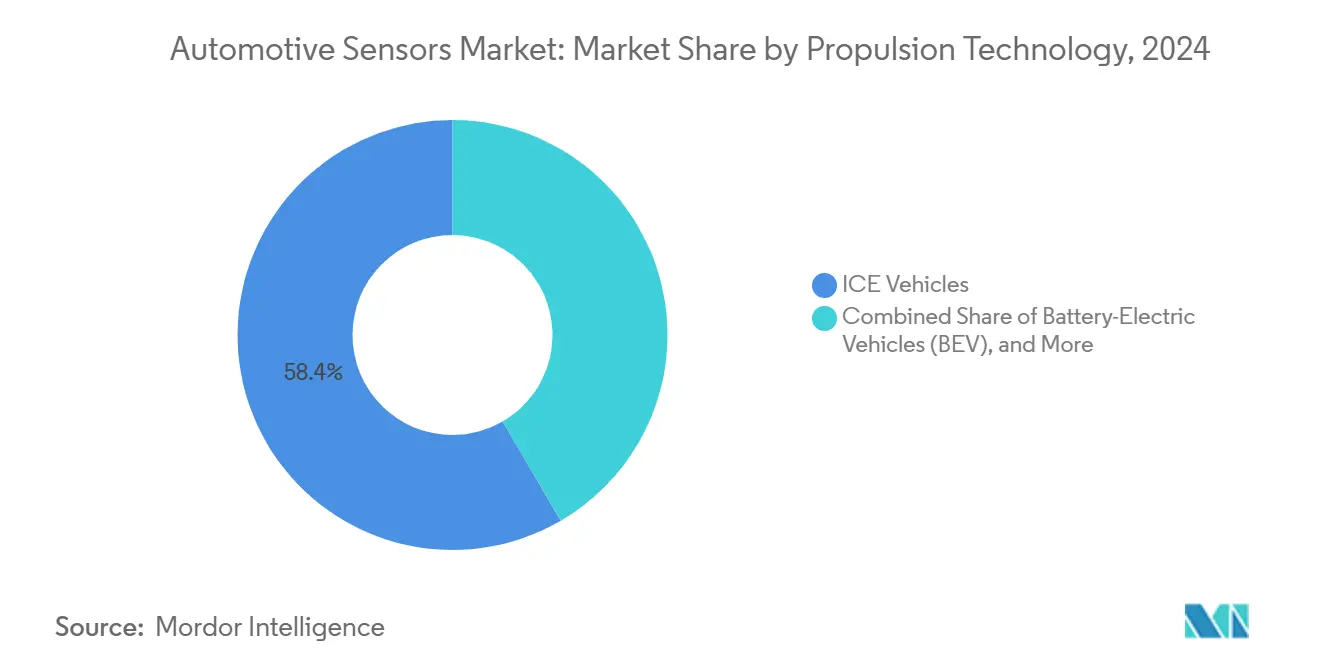

- By propulsion technology, internal combustion engine vehicles held 58.40% of the automotive sensors market size in 2024; fuel-cell electric vehicles are projected to grow at a 24.50% CAGR to 2030.

- By sales channel, OEM-fitted sensors dominated with 88.20% share in 2024; the aftermarket segment is advancing at a 12.40% CAGR through 2030.

- By geography, Asia-Pacific captured 42.30% revenue share in 2024 and is advancing at a 9.10% CAGR to 2030.

Global Automotive Sensors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS and Autonomous-Driving Sensor Proliferation | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Emission and Safety Mandates Driving Pressure/Gas Sensors | +1.2% | Global, strongest in EU and China | Short term (≤ 2 years) |

| EV Thermal-Battery Sensing Boom | +1.5% | APAC core, expanding to North America | Medium term (2-4 years) |

| Falling MEMS ASP Enabling Mass Adoption | +0.9% | Global, cost-sensitive markets first | Long term (≥ 4 years) |

| OTA-Ready Self-Diagnostic Smart Sensors | +0.6% | Premium markets, gradual mainstream | Long term (≥ 4 years) |

| Usage-Based-Insurance Telematics Demand | +0.4% | North America and Europe primarily | Medium term (2-4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

ADAS and autonomous-driving sensor proliferation

Automatic emergency braking, lane-keeping assist, and pedestrian detection in upcoming safety ratings drive higher sensor counts per vehicle[1]National Highway Traffic Safety Administration, “New Car Assessment Program Final Decision Notice – ADAS Roadmap,” nhtsa.gov. Semiconductor roadmaps anticipate that ADAS will capture nearly one-third of automotive chip demand by 2027 as Level 2+ functions become standard. Chinese brands intensify price competition by bundling full ADAS suites at minimal cost, compelling global suppliers to slash system prices without eroding performance. Radar, LiDAR, and camera fusion are about to reach 99.97% detection accuracy, yet create terabyte-scale data loads that are increasingly processed at the sensor edge to cut latency. Edge AI capability, therefore, becomes the next differentiation lever in the automotive sensors market.

Emission and safety mandates driving pressure / gas sensors

The U.S. Environmental Protection Agency’s 2027–2032 rules require a 50% cut in greenhouse-gas output, forcing real-time sensing of exhaust after-treatment efficiency[2]Environmental Protection Agency, “Multi-Pollutant Emissions Standards for Model Years 2027–2032,” epa.gov. Parallel hydrogen-vehicle regulations (FMVSS 307/308) add pressure and leak-detection requirements for new fuel systems. Euro 7 extends particulate and NOx limits, spurring precision gas-sensor demand, while the U.K. Progressive Safe System introduces blind-spot sensing on heavy trucks to protect vulnerable road users. The overlapping mandates tighten design windows and secure multi-year demand for high-accuracy pressure and gas sensors.

EV thermal-battery sensing boom

UNECE Global Technical Regulation 20 obligates embedded sensors in every battery pack to detect thermal runaway events. Suppliers such as Infineon now market dedicated pressure devices certified to ISO 26262 for autonomous safety shutdowns. Research highlights Fiber Bragg Grating and infrared optical sensors for non-intrusive cell monitoring, widening the technology palette. With semiconductor value per electric vehicle already six times higher than in internal-combustion cars, battery-safety sensing has become a mandatory, margin-rich category.

Falling MEMS ASP enabling mass adoption

Global MEMS output hit 34 billion units in 2024 as 300 mm foundries expand, pushing sensor ASPs lower and allowing even entry-level vehicles to add multiple sensing nodes. Bosch recently unveiled the world’s smallest automotive accelerometer, demonstrating miniaturization that lowers material cost yet boosts performance density. Standardized substrates under SEMI MS12 shorten development cycles and encourage multi-source supply, underpinning long-run cost declines in the automotive sensors industry.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor Cost Pressure on Mass-Market Vehicles | -1.1% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Semiconductor Wafer-Supply Volatility | -0.8% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| ADAS Liability Delaying New Sensor Specs | -0.5% | North America and Europe primarily | Medium term (2-4 years) |

| Privacy Limits to Sensor-Data Monetization | -0.3% | Europe and select jurisdictions | Long term (≥ 4 years) |

Source: Mordor Intelligence

Sensor cost pressure on mass-market vehicles

Between 2023 and 2029, vehicles are set to see a swift uptick in their average semiconductor content, compressing OEM margins in price-sensitive segments. Low-cost Chinese EV brands already offer full ADAS suites at no extra charge, escalating pricing pressure on established suppliers. Tier-one sensor makers must, therefore, integrate functions, shrink packages, and adopt system-on-chip designs to deliver value without eroding profitability.

Semiconductor wafer-supply volatility

Lead times for automotive-grade chips have stretched past one year, compelling vehicle makers to carry high inventory buffers bis.gov. Although the U.S. CHIPS Act allocates USD 39 billion to new fabs, material shortages and equipment bottlenecks delay capacity additions. Because 66% of automotive products still rely on Chinese foundries, geopolitical risk remains a live concern, prompting dual-sourcing and long-term supply agreements.

Segment Analysis

By Type: Inertial Sensors Lead Multi-Sensor Integration

Inertial sensors generated 28.13% of 2024 revenue because accelerometers and gyroscopes anchor electronic stability control, navigation, and ADAS stacks. Higher-resolution inertial measurement units (IMUs) are now embedded inside zonal architectures, and suppliers integrate self-diagnostics that meet AEC-Q100 grade 1 to cut cabling and lower overall system weight. Magnetic sensors gain traction in EV traction-motor control, while gas sensors rebound on emissions and cabin-air mandates. Pressure and temperature sensors expand beyond combustion engines into battery thermal-runaway detection.

System-level integration is accelerating: combo packages merge accelerometer, gyroscope, and magnetometer functions, reducing OEM SKU counts and simplifying qualification cycles. Falling MEMS ASPs keep inertial devices economically feasible for mass-market cars, and edge AI blocks are starting to appear on-die to pre-filter motion data locally. The net result is a sustainable 6.47% CAGR through 2030 for this cornerstone category, as every additional autonomy layer requires finer motion awareness.

Note: Segment shares of all individual segments available upon report purchase

By Application: Powertrain Dominance Faces Telematics Disruption

Powertrain sensing delivered 40.55% of 2024 revenue, through indispensable roles in fuel metering, ignition, turbo boost, and after-treatment control. Yet battery-electric architectures omit several legacy measurements, softening long-range growth. In contrast, telematics sensors post the quickest 8.86% CAGR as usage-based insurance and fleet optimization adopt GPS, accelerometer, and OBD data streams to lower crash frequency by up to 43%.

Body electronics maintain mid-single-digit expansion as comfort functions proliferate, and vehicle security evolves from alarms to integrated intrusion-detection radar. Software-defined vehicles shift value from mechanical actuation to data, and OEMs increasingly monetize sensor payloads via predictive-maintenance subscriptions. This realignment cushions the tapering of pure powertrain demand and diversifies revenue toward connected services.

By Vehicle Type: Commercial Vehicles Accelerate Sensor Adoption

Passenger cars commanded 71.18% of 2024 revenue, yet commercial vehicles log the faster 7.15% CAGR because fleet operators bankroll safety compliance and operational efficiency. Europe’s Progressive Safe System and similar urban-safety rules impose blind-spot detection and driver-visibility aids on heavy trucks, directly lifting the automotive sensors market share for radar, ultrasonic, and camera modules.

Fleet buyers calculate quick payback from fewer collisions, fuel savings, and insurance credits, prompting retrofit campaigns on existing assets. ZF and Bendix now market ADAS packages ruggedized for vibration and duty-cycle extremes, while over-the-air calibration tools minimize downtime. This willingness to invest turns commercial vehicles into proving grounds for next-generation sensors that later cascade into passenger models.

By Propulsion Technology: FCEVs Drive Sensor Innovation

Internal-combustion vehicles still held 58.40% of 2024 revenue, but fuel-cell electric vehicles (FCEVs) are the breakout, posting a 24.50% CAGR as hydrogen infrastructure scales. New FMVSS 307/308 regulations obligate pressure, leak, and temperature sensors on compressed-hydrogen tanks, spawning a premium niche with stringent reliability demands.

Battery-electric models need dense thermal-runaway monitoring, while plug-in hybrids combine both combustion and EV requirements, lifting sensor counts but complicating integration. Suppliers with hydrogen-competent portfolios command elevated gross margins thanks to limited competition and certification barriers. Collectively, propulsion diversification cushions cyclical risk and expands the total addressable automotive sensors market.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Aftermarket Gains Retrofit Momentum

OEM-fitted systems dominated 88.20% of 2024 shipments, but the aftermarket is scaling at a 12.40% CAGR as owners retrofit ADAS or telematics on vehicles already in service. SEMA calculates the U.S. ADAS aftermarket near USD 1 billion and growing 9–10% annually on cost-effective alternatives to trading in a vehicle.

Calibration complexity births a parallel services market: repair shops invest in alignment rigs and software subscriptions to ensure sensor accuracy after windshield or bumper replacements. Fleet managers appreciate the pay-as-you-go upgrade path, which avoids capital outlay on new trucks yet satisfies insurer and regulator requirements. Continued sensor miniaturization and standardized interfaces lower installation friction, validating the aftermarket as a durable growth corridor within the automotive sensors market.

Geography Analysis

Asia-Pacific led with 42.30% revenue share in 2024 and is expected to post the quickest 9.10% CAGR to 2030. China already manufactures around 62% of global EVs and 77% of batteries, providing a vast indigenous market for sensors and guaranteeing scale advantages. Vertically integrated champions such as BYD build up to 70% of semiconductor content in-house, including camera and electromagnetic devices, tightening local supply loops. Japan leverages decades of sensor know-how while attracting new wafer capacity via government incentives, and Taiwan’s foundries remain pivotal to leading-edge MEMS production. Government subsidies and aggressive electrification targets reinforce the region’s expansion.

North America maintains a premium ADAS focus, aided by robust safety regulations and funding to localize chip fabrication. The CHIPS Act’s capital grants plus tax incentives reduce reliance on overseas foundries, supporting a resilient supply base. NHTSA’s added ADAS metrics under the New Car Assessment Program guarantee baseline installation of critical sensors from model-year 2026 onwards, underpinning steady demand across vehicle classes.

Europe emphasizes emissions compliance and urban-safety mandates that raise sensor density in both passenger cars and heavy trucks. Euro 7 rules and Progressive Safe System requirements trigger new opportunities for gas detectors and blind-spot solutions. At the same time, cost competition from imported Chinese EVs forces European suppliers to accelerate cost-down initiatives without sacrificing precision, creating a challenging but innovation-rich environment for the automotive sensors market.

Competitive Landscape

The key market players, including Robert Bosch, DENSO, and Continental capture growing value by embedding signal processing and connectivity features directly inside sensor packages. Traditional tier-one suppliers respond with vertical integration, proprietary software stacks, and joint design centers with OEMs. Emerging Chinese players bundle complete sensor-software suites at aggressive pricing, intensifying competition on cost.

Strategic moves reflect consolidation and partnership trends. Infineon’s USD 2.5 billion purchase of Marvell’s automotive Ethernet business in April 2025 integrates microcontrollers with high-bandwidth networking for software-defined vehicles. Indie Semiconductor’s collaboration with GlobalFoundries delivers 77 GHz and 120 GHz radar SoCs optimized for power-efficient ADAS.

Meanwhile, a cross-industry Autonomous Vehicle Computing Consortium pools resources from automakers and chip vendors to standardize in-vehicle compute architectures. White-space prospects include hydrogen leak detection, battery thermal-runaway sensing, and embedded edge AI that turns sensors into local analytics nodes—areas where niche suppliers can secure premium share.

Automotive Sensors Industry Leaders

-

Continental AG

-

NXP Semiconductors NV

-

Robert Bosch GmbH

-

Infineon Technologies AG

-

DENSO Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Infineon Technologies acquired Marvell’s Automotive Ethernet unit for USD 2.5 billion to integrate networking with microcontroller portfolios.

- March 2025: Indie Semiconductor and GlobalFoundries partnered to develop 77 GHz / 120 GHz radar SoCs targeting forward-collision and emergency braking systems

- November 2024: Murata introduced the SCH1633-D01 six-DoF MEMS sensor, a single-package solution for ADAS with AEC-Q100 grade 1 rating

- April 2024: NOVOSENSE launched the NSHT30-Q1 CMOS-MEMS temperature-humidity sensor for HVAC and battery applications

Global Automotive Sensors Market Report Scope

Automotive sensors are used to gather information about the vehicle's surroundings, such as its speed, location, and environment, and then send this information to the vehicle's onboard computer system to make decisions.

The Automotive Sensors Market is Segmented by Type (Temperature Sensors, Pressure Sensors, Speed Sensors, Level/Position Sensors, Magnetic Sensors, Gas Sensors, and Inertial Sensors), Application (Powertrain, Body Electronics, Vehicle Security Systems, and Telematics), Vehicle Type (Passenger Cars and Commercial Vehicles), and By Geography (North America, Europe, Asia-Pacific, and Rest of World). The report covers the market size in value (USD billion) for all the above segments.

| By Type | Temperature Sensors | ||

| Pressure Sensors | |||

| Speed Sensors | |||

| Level / Position Sensors | |||

| Magnetic Sensors | |||

| Gas Sensors | |||

| Inertial Sensors | |||

| By Application | Powertrain | ||

| Body Electronics | |||

| Vehicle Security Systems | |||

| Telematics | |||

| By Vehicle Type | Passenger Cars | ||

| Commercial Vehicles | |||

| By Propulsion Technology | ICE Vehicles | ||

| Battery-Electric Vehicles (BEV) | |||

| Plug-in Hybrid Vehicles (PHEV) | |||

| Fuel-cell Electric Vehicles (FCEV) | |||

| By Sales Channel | OEM-fitted Sensors | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Turkey | ||

| GCC | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

By Type

| Temperature Sensors |

| Pressure Sensors |

| Speed Sensors |

| Level / Position Sensors |

| Magnetic Sensors |

| Gas Sensors |

| Inertial Sensors |

By Application

| Powertrain |

| Body Electronics |

| Vehicle Security Systems |

| Telematics |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By Propulsion Technology

| ICE Vehicles |

| Battery-Electric Vehicles (BEV) |

| Plug-in Hybrid Vehicles (PHEV) |

| Fuel-cell Electric Vehicles (FCEV) |

By Sales Channel

| OEM-fitted Sensors |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Turkey |

| GCC | |

| South Africa | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the automotive sensors market?

The market generated USD 28.83 billion in 2025 and is projected to reach USD 38.67 billion by 2030 on a 6.05% CAGR.

Which sensor type holds the largest share today?

Inertial sensors lead with 28.13% of 2024 revenue because stability control, navigation, and ADAS functions all rely on high-resolution motion data.

Why is Asia-Pacific growing fastest?

China’s dominance in electric-vehicle and battery manufacturing, coupled with Japanese sensor expertise, drives a 9.10% CAGR for the region through 2030.

How are emissions regulations affecting sensor demand?

Stricter EPA, Euro 7, and hydrogen safety rules compel real-time gas and pressure monitoring, boosting demand for high-precision sensing across powertrain and EV systems.

What is driving the aftermarket opportunity?

Fleet operators and consumers retrofit older vehicles with ADAS and telematics packages, pushing the aftermarket channel to a 12.40% CAGR through 2030.

Which propulsion technology offers the fastest sensor growth?

Fuel-cell electric vehicles are projected to expand at a 24.50% CAGR, requiring specialized hydrogen-storage and fuel-cell monitoring sensors not needed in other drivetrains.

Page last updated on: June 23, 2025