Market Overview

| Study Period | 2019 - 2030 |

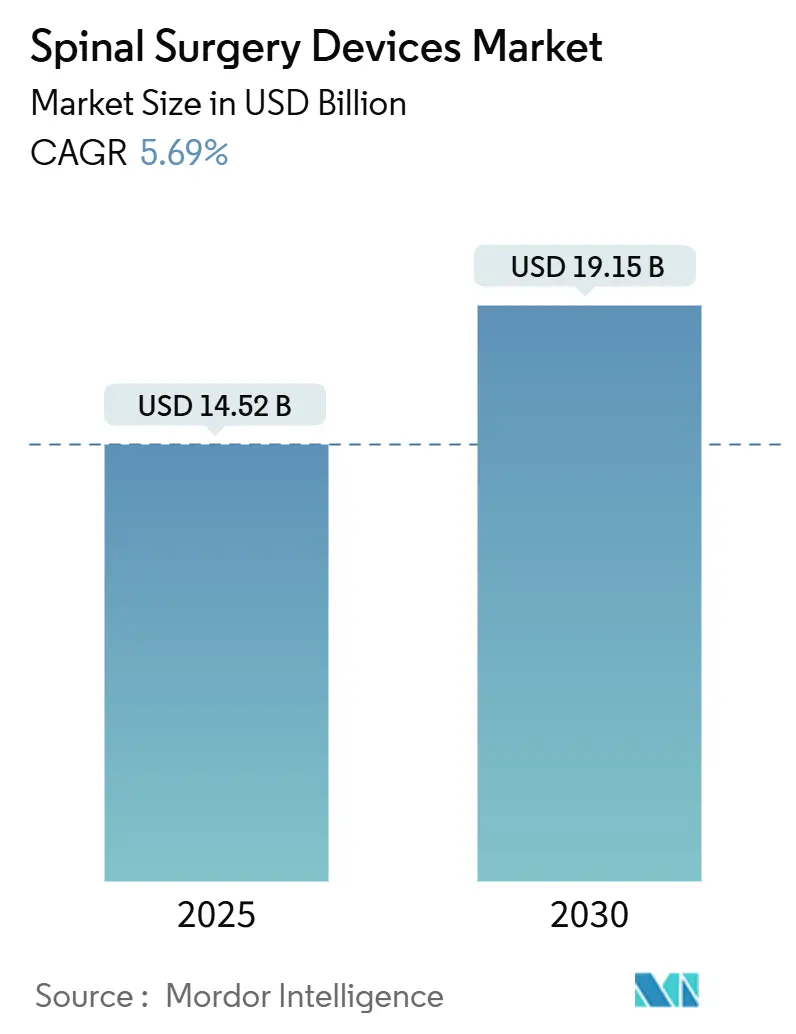

| Market Size (2025) | USD 14.52 Billion |

| Market Size (2030) | USD 19.15 Billion |

| Growth Rate (2025 - 2030) | 5.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spinal Surgery Devices Market Analysis by Mordor Intelligence

The spine surgery devices market size reached USD 14.52 billion in 2025 and is forecast to climb to USD 19.15 billion by 2030, advancing at a 5.69% CAGR. This expansion reflects rising surgical volumes tied to population aging, an increasing burden of degenerative spine conditions, and continuous device innovation. Robust demand persists for fusion instrumentation that remains the clinical mainstay for instability and deformity, yet surgeons are steadily adopting motion-preserving alternatives to mitigate adjacent‐segment disease. Precision technologies—robotic guidance, real-time navigation, and 3-D printing—are shortening operating times and improving construct accuracy, creating clear hospital ROI arguments. Outpatient migration strengthens as payors reward minimally invasive approaches that lower complication rates and accelerate recovery, driving facility-level competition to invest in advanced platforms.

Key Report Takeaways

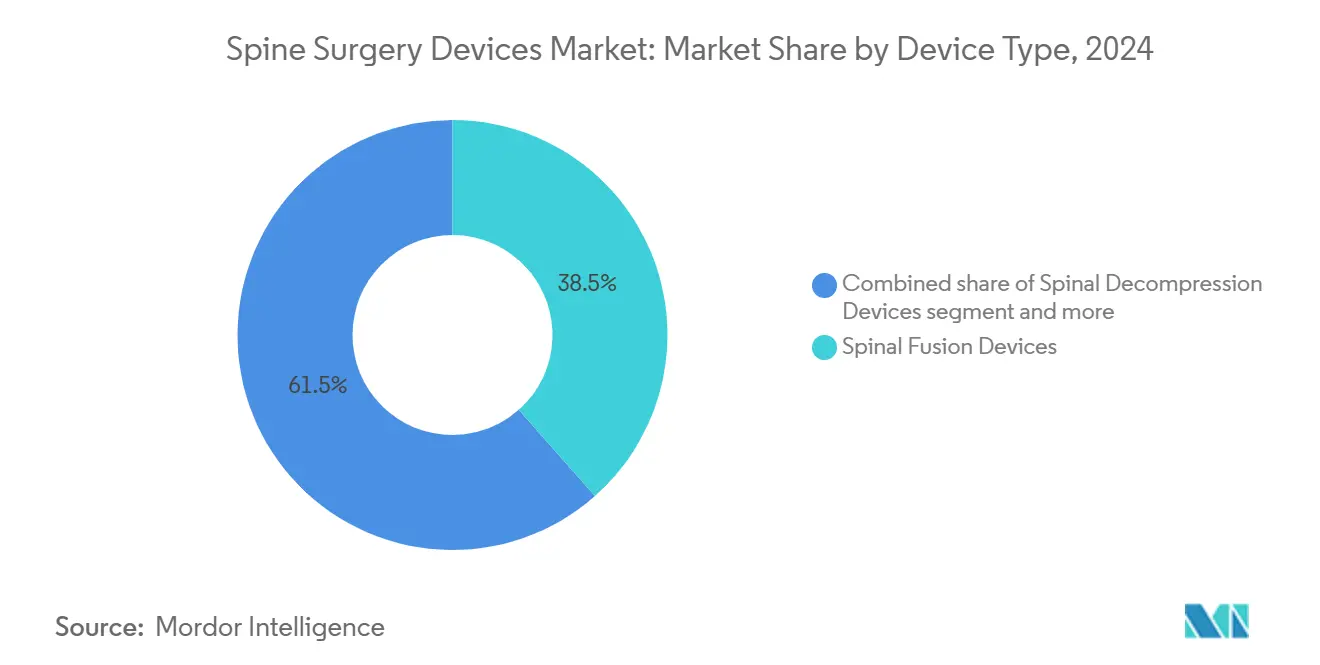

- By device type, Spinal Fusion Devices led with 38.46% of spine surgery devices market share in 2024, while Motion-Preservation/Non-fusion Devices are growing the fastest at a 6.75% CAGR through 2030.

- By procedure type, Open Spine Surgery held 56.58% of the spine surgery devices market size in 2024; Minimally-Invasive Spine Surgery is forecast to expand at a 5.91% CAGR to 2030.

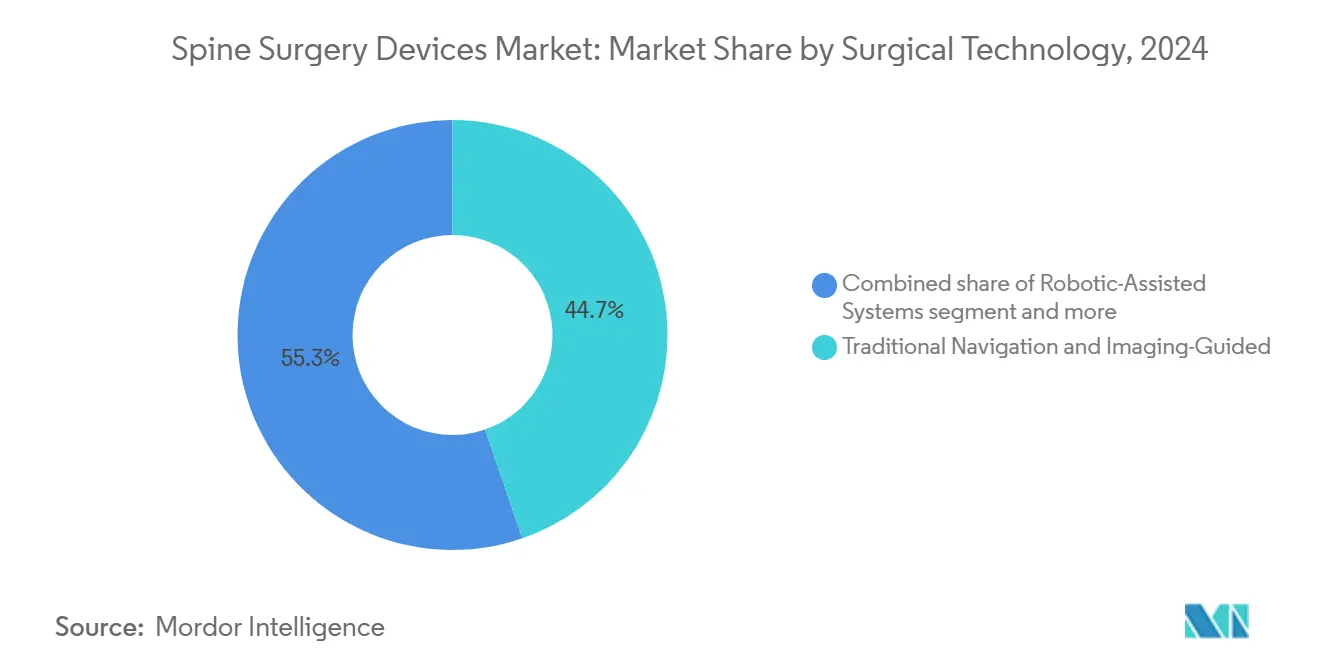

- By surgical technology, Traditional Navigation & Imaging-Guided approaches commanded 44.73% market revenue share in 2024; Robotic-Assisted Systems post the highest projected CAGR at 6.26% to 2030.

- By surgery setting, Hospitals accounted for 67.29% share of the spine surgery devices market size in 2024, whereas Ambulatory Surgery Centers are advancing at a 6.38% CAGR over the same outlook.

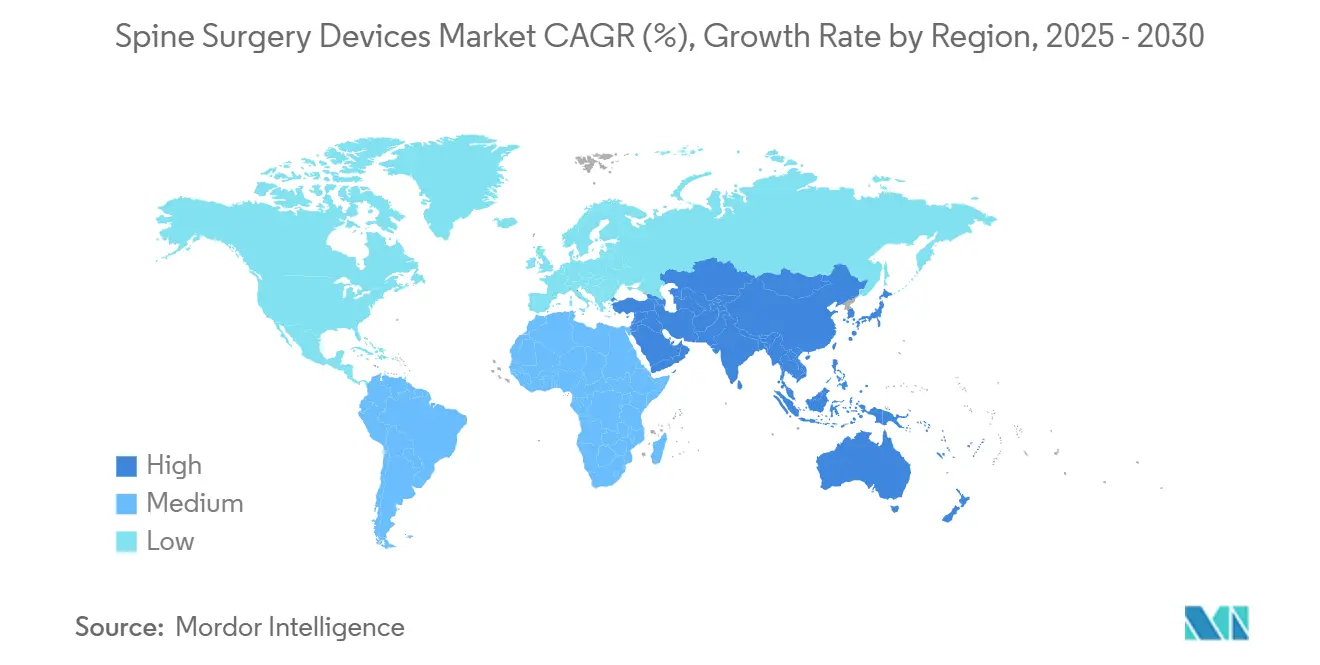

- By geography, North America captured 44.36% revenue share in 2024; Asia-Pacific is the fastest-growing regional segment with a 6.46% CAGR through 2030.

Global Spinal Surgery Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of degenerative spine disorders & obesity | +1.4% | Global, highest in aging regions | Short term (≤ 2 years) |

| Adoption of minimally invasive & robotic procedures | +1.2% | North America, Europe lead | Medium term (2-4 years) |

| Real-time AR/VR navigation & 3-D printed implants | +0.8% | North America, EU core, APAC spill-over | Long term (≥ 4 years) |

| Outpatient-friendly reimbursement at ASCs | +0.7% | North America, expanding to Europe | Medium term (2-4 years) |

| Next-generation implant materials | +0.6% | Global | Long term (≥ 4 years) |

| AI-driven predictive analytics | +0.5% | North America, EU, early APAC | Long term (≥ 4 years) |

Source: Mordor Intelligence

Growing prevalence of degenerative spine disorders & obesity

Low-back-pain DALYs climbed from 5.5 million in 1990 to 9.8 million in 2021 and are projected to exceed 11.6 million by 2050[1]Chuan Zhang, “Global, regional, and national burden and trends of Low back pain in middle-aged adults: analysis of GBD 1990–2021 with projections to 2050,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com, signaling sustained demand for surgical intervention. The ≥ 65-year cohort is set to reach 89 million by 2050, and roughly 27.5 million people already live with spinal deformities. High BMI accelerates adjacent-segment degeneration[2]Liu, Y., “How to prevent preoperative adjacent segment degeneration L5/S1 segment occuring postoperative adjacent segment disease? A retrospective study of risk factor analysis,” Journal of Orthopaedic Surgery and Research, josr-online.biomedcentral.com following fusion, fueling uptake of motion-preservation implants. Medicare volume forecasts through 2050 indicate steady growth in instrumented procedures, amplifying pressure on surgical capacity. Providers, therefore, embrace minimally invasive strategies capable of treating larger caseloads without compromising outcomes.

Rising adoption of minimally-invasive & robotic-assisted spine procedures

Robotic platforms achieve clinical acceptance rates approaching 97% among surgical trainees while trimming complex-case operating times by up to 62 minutes. Complete endoscopic cervical surgery delivers more than 85% patient satisfaction with fewer complications than open surgery. Hospitals report SGD 1,500 cost savings per patient when deploying robotics in multilevel cases. CMS continues to broaden ASC procedure lists, signaling policy momentum toward outpatient spine even though dedicated spine codes await approval. Health systems differentiate by coupling mini-access techniques with precision guidance to drive measurable value.

Breakthroughs in real-time AR/VR navigation & 3-D printed implants

Augmented-reality navigation now attains sub-millimeter pedicle screw accuracy, with the SPINAV randomized trial[3]Victor Gabriel El-Hajj, “Study protocol: the SPInal NAVigation (SPINAV) trial – comparison of augmented reality surgical navigation, conventional image-guided navigation, and free-hand technique for pedicle screw placement in spinal deformity surgery,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com providing the first high-level evidence for complex deformity care. Parallel advances in 3-D printed PEEK implants accelerate regulatory clearances; Curiteva’s trabecular PEEK system secured FDA 510(k) in under 60 days, underscoring a maturing pathway. Combining patient-specific cages with real-time guidance enables premium pricing justified by improved fusion rates and reduced revision risk.

Continuous advancements in implant materials

Titanium-coated PEEK cages match fusion rates of uncoated designs while providing radiolucent monitoring advantages. The FDA clearance of Mo50 Re alloy introduces rhenium-based constructs with zero observed breakage in early testing. Surface-modified devices such as Medtronic’s Titan nanoLOCK accelerate bone ingrowth, shortening healing timelines and reinforcing surgeon confidence.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure & implant cost; limited payor cover | -1.1% | APAC, Latin America, MEA | Short term (≤ 2 years) |

| Stringent multi-jurisdictional regulatory timelines | -0.9% | Global; EU MDR adds complexity | Medium term (2-4 years) |

| Supply-chain pressure on titanium & PEEK | -0.7% | Global, US & EU hubs affected | Short term (≤ 2 years) |

| Data-security liability for connected platforms | -0.4% | North America, EU, expanding APAC | Medium term (2-4 years) |

Source: Mordor Intelligence

High procedure & implant cost; limited payor coverage in emerging markets

France cut orthopedic implant reimbursement by 25%, targeting EUR 231 million savings and triggering device shortages. Cost-utility analysis places allograft cervical fusion at USD 2,492 per QALY versus USD 3,328 for PEEK cages, challenging premium strategies. Latin American access to minimally invasive platforms remains constrained by high capital outlays and fragmented insurance coverage. Vendors respond with value-engineered designs that retain core clinical benefits while trimming upfront spend.

Stringent multi-jurisdictional regulatory clearance timelines

EU MDR phases extend to 2028, imposing dual-track compliance that lengthens time-to-market and diverts R&D resources toward regulatory affairs. FDA 510(k) averages 90-180 days while PMA can exceed one year, skewing risk for smaller innovators. Delayed approvals suppress competitive dynamism and may slow diffusion of cutting-edge technologies capable of addressing unmet clinical needs.

Segment Analysis

By Device Type: Fusion leadership meets motion-preservation momentum

Spinal Fusion Devices held a 38.46% revenue share in 2024 within the spine surgery devices market. Interbody techniques such as ALIF and TLIF underpin this dominance, offering reproducible biomechanics and broad surgeon familiarity. Arthroplasty solutions, however, are climbing at a 6.75% CAGR, driven by evidence that motion preservation mitigates adjacent-segment degeneration. Lumbar disc replacement now delivers comparable pain reduction to fusion while preserving mobility[4]Pheasant, M.S., “The Future of Motion Preservation and Arthroplasty in the Degenerative Lumbar Spine,” Journal of Clinical Medicine, mdpi.com. The spine surgery devices market size for motion-preservation implants is projected to scale rapidly as long-term outcomes further validate their safety profile.

Clinical demand for biologically active surfaces fuels material innovation across both fusion and motion segments. Nano-textured titanium and porous PEEK aim to lower the 10% non-union rate observed in multi-level fusion. Vendors bundle these features with outcome-tracking software to create comprehensive value propositions that incentivize premium list pricing while addressing surgeon concerns over fusion reliability.

Note: Segment shares of all individual segments available upon report purchase

By Procedure Type: Open surgery resilience amid MISS acceleration

Open procedures still generated 56.58% of 2024 revenues, reflecting their necessity for deformity corrections and extensive reconstructions. Yet minimally invasive spine surgery advances at a 5.91% CAGR, propelled by patient demand for faster recovery and payer pressure to reduce inpatient stays. Medicare outpatient data revealed a 193% surge in spine cases from 2010-2021, underscoring procedural migration to settings that reward efficiency.

Endoscopic discectomy adoption illustrates this shift: its volume rose 8.58% between 2017-2021 while open microdiscectomy fell 27.78%. Hospitals invest in robotic and navigation platforms that extend MIS applicability to complex pathology, supporting the spine surgery devices market’s transition toward smaller incisions without sacrificing corrective potential.

By Surgical Technology: Robotics outpaces legacy navigation

Traditional image-guided systems retained 44.73% market share in 2024, yet robotic-assisted platforms post a 6.26% CAGR, capturing institutions seeking accuracy gains and operating-room efficiency. Meta-analysis confirms robotic screw placement accuracy surpasses 95% while lowering intraoperative revision rates. Vendors pivot to integrated ecosystems; Stryker’s Q Guidance with Copilot pairs innovative instruments and live feedback, while Globus Medical’s ExcelsiusHub unifies navigation, robotics, and data analytics.

AR-guided modalities represent the next horizon, blending headset visualization with navigation overlays. Early adopters report sub-millimeter accuracy, but widespread uptake depends on cost reduction and streamlined training. Hybrid suites housing multiple guidance tools may become the standard of care, further anchoring the spine surgery devices market to technology refresh cycles.

Note: Segment shares of all individual segments available upon report purchase

By Surgery Setting: ASC gains challenge hospital predominance

Hospitals delivered 67.29% of 2024 revenue, yet Ambulatory Surgery Centers are advancing at a 6.38% CAGR. ASC spine surgery exhibits safety profiles comparable to inpatient care while generating annual US savings of USD 140 million. CMS’s 2025 conversion factor of USD 54.895 for quality-compliant ASCs bolsters profitability for high-volume centers.

Outpatient candidacy now extends to select deformity and multi-level fusion cases when combined with mini-access approaches and rapid-recovery protocols. Providers that optimize anesthesia, navigation, and robotic workflows can transition higher-acuity cases safely to ASC environments, capturing payer incentives and patient preferences.

Geography Analysis

North America commanded 44.36% of global revenue in 2024, advancing at 4.86% CAGR to 2030. Supportive reimbursement, robust clinical research networks, and early adoption of precision technologies underpin regional leadership. FDA guidance offers predictable clearance pathways that encourage continuous device iteration. Market players intensify R&D around AI-enabled planning to preserve competitive moats.

Asia-Pacific marks the fastest trajectory at 6.46% CAGR, propelled by expanding surgical capacity and rising middle-class demand for advanced care. Urban centers in China and India invest in robotic suites, yet adoption disparities persist across rural regions. Local manufacturing partnerships help offset import tariffs and build price-appropriate portfolios, positioning vendors to capture incremental volumes as infrastructure matures.

Europe sustains a 5.38% CAGR despite regulatory headwinds from MDR. Countries tighten cost controls; France’s reimbursement cuts already reduce implant availability. Suppliers that validate superior outcomes can maintain premium pricing, but must navigate lengthened certification timelines. South America and MEA grow at 5.82% and 6.01% CAGRs, respectively, buoyed by public-health initiatives and private-sector investment. Limited payor coverage still constrains high-end system penetration, steering suppliers toward modular, lower-cost constructs that preserve essential functionality.

Competitive Landscape

Medtronic is a leading player in the market, supported by its AiBLE ecosystem that unites navigation, robotics, and AI planning. Johnson & Johnson is leveraging DePuy Synthes’ broad implant line and Monarch robotic platform. Globus Medical and Stryker are focusing on differentiated procedural systems—Globus with integrated neuromonitoring, Stryker with navigation-centric robotics.

M&A activity reshapes portfolios: Globus Medical acquired Nevro for USD 250 million to merge neuromodulation with structural implants, while Stryker divested its US spinal implant business to redeploy capital into guidance technologies. Emerging firms such as Neo Medical secure MDR certification for AI-driven systems that cut implant inventory and reduce rod breakage risk.

Competitive advantage is shifting from standalone devices to platform integration that locks surgeons into vendor ecosystems and simplifies data capture. Vendors that demonstrate measurable improvements in accuracy, operative time, and patient outcomes secure stronger buying-group contracts and long-term service revenue.

Spinal Surgery Devices Industry Leaders

-

Globus Medical

-

Johnson & Johnson Services, Inc.

-

Medtronic plc

-

Stryker Corporation

-

Zimmer Biomet Holdings

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Globus Medical completed its USD 250 million purchase of Nevro Corp., expanding its chronic-pain neuromodulation portfolio.

- February 2025: Medtronic launched the CD Horizon ModuLeX system, integrating with AiBLE for deformity corrections.

- December 2024: Neo Medical SA obtained MDR certification across its spine portfolio, enabling EU expansion.

- October 2024: Stryker finalized the acquisition of Vertos Medical to broaden its minimally invasive treatment options for lumbar stenosis.

Global Spinal Surgery Devices Market Report Scope

As per the scope of the report, spinal surgery devices are devices used to treat spinal injuries or deformities. They help restructure or realign the spine. The Spinal Surgery Devices Market is segmented by Device Type (Spinal Decompression, Spinal Fusion, Fracture Repair Devices, Arthroplasty Devices, Non-fusion Devices) and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD million) for the above segments.

| By Device Type | Spinal Decompression Devices | Corpectomy Systems | |

| Discectomy Systems | |||

| Facetectomy Systems | |||

| Foraminotomy Systems | |||

| Laminotomy Systems | |||

| Spinal Fusion Devices | Cervical Fusion | ||

| Interbody Fusion | |||

| Thoracolumbar Fusion | |||

| Others | |||

| Arthroplasty / Disc Replacement Devices | |||

| Fracture Repair & VCF Devices | |||

| Motion-Preservation / Non-fusion Devices | |||

| By Procedure Type | Open Spine Surgery | ||

| Minimally-Invasive Spine Surgery (MISS) | |||

| By Surgical Technology | Robotic-Assisted Systems | ||

| AR/VR-Navigated Systems | |||

| Traditional Navigation & Imaging-Guided | |||

| By Surgery Setting | Hospitals | ||

| Ambulatory Surgery Centers (ASCs) | |||

| Specialty Orthopedic & Spine Clinics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

By Device Type

| Spinal Decompression Devices | Corpectomy Systems |

| Discectomy Systems | |

| Facetectomy Systems | |

| Foraminotomy Systems | |

| Laminotomy Systems | |

| Spinal Fusion Devices | Cervical Fusion |

| Interbody Fusion | |

| Thoracolumbar Fusion | |

| Others | |

| Arthroplasty / Disc Replacement Devices | |

| Fracture Repair & VCF Devices | |

| Motion-Preservation / Non-fusion Devices |

By Procedure Type

| Open Spine Surgery |

| Minimally-Invasive Spine Surgery (MISS) |

By Surgical Technology

| Robotic-Assisted Systems |

| AR/VR-Navigated Systems |

| Traditional Navigation & Imaging-Guided |

By Surgery Setting

| Hospitals |

| Ambulatory Surgery Centers (ASCs) |

| Specialty Orthopedic & Spine Clinics |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What factors are prompting surgeons to adopt motion-preserving spine implants over traditional fusion devices?

Surgeons are turning to disc-replacement and other motion-preserving systems because they reduce adjacent-segment degeneration and maintain spinal mobility, which translates into lower revision risk and faster functional recovery.

How are robotic-assisted systems improving outcomes in spine surgery?

Robotic guidance delivers sub-millimeter screw accuracy and can trim operative times by close to an hour on complex cases, which lowers infection risk, shortens anesthesia exposure, and reduces overall hospital costs.

Why are ambulatory surgery centers gaining traction for spine procedures?

Outpatient facilities combine minimally invasive techniques with streamlined care pathways, enabling same-day discharge and cost savings that appeal to payors, surgeons, and patients alike.

What role do augmented reality and 3-D printed implants play in modern spine surgery?

AR navigation overlays real-time imaging onto the operative field for precise instrumentation, while 3-D printed, patient-specific cages optimize anatomical fit and promote more reliable fusion.

Which material innovations are enhancing spinal implant performance?

Titanium-coated and nano-textured PEEK surfaces improve osseointegration and radiolucency, and new rhenium-containing alloys show greater fatigue strength, helping cut down on hardware failure.

How is the EU Medical Device Regulation influencing product development timelines for spine device manufacturers?

MDR’s stricter evidence and surveillance requirements lengthen approval cycles and increase compliance costs, pushing companies to allocate more resources to regulatory strategy before launching new technologies.

Page last updated on: June 23, 2025