Carbon Fiber Reinforced Plastic (CFRP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

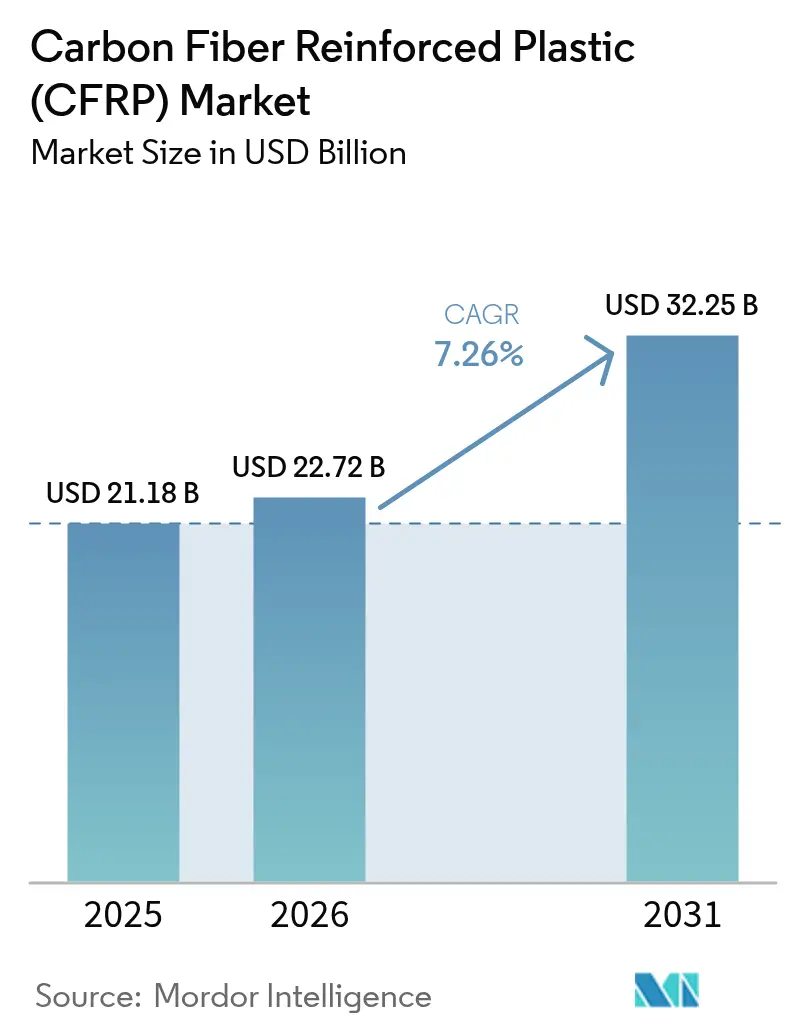

| Market Size (2026) | USD 22.72 Billion |

| Market Size (2031) | USD 32.25 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

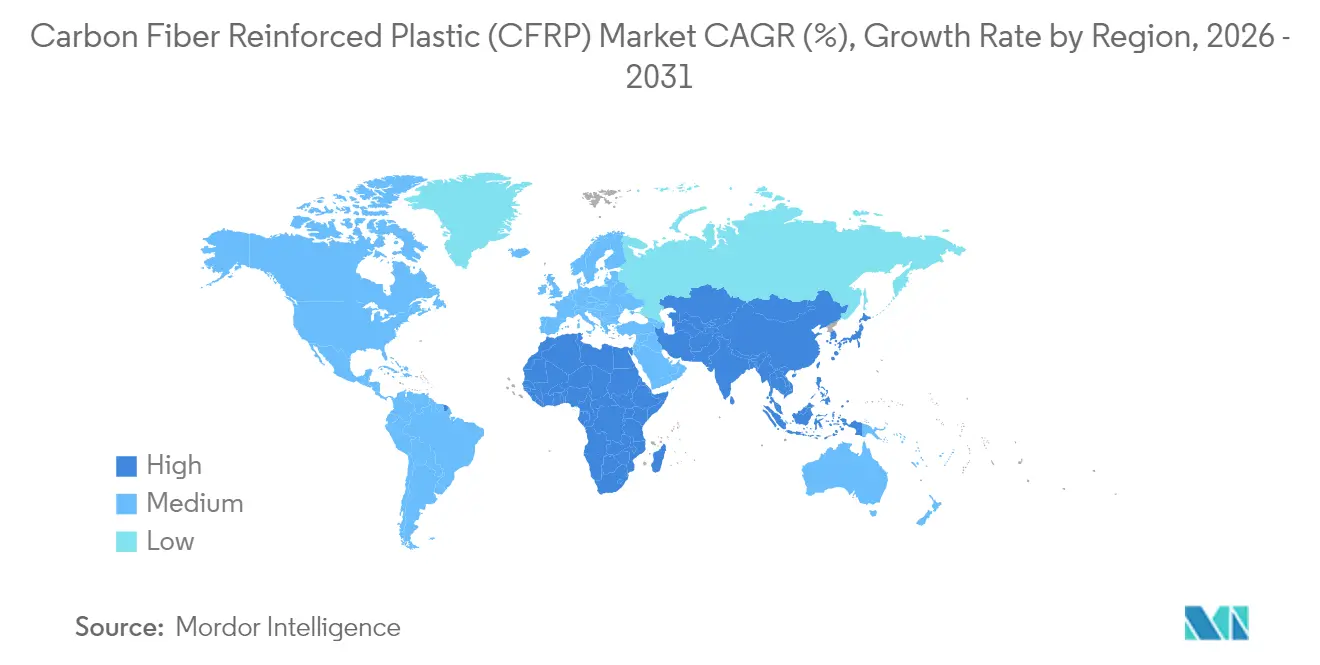

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbon Fiber Reinforced Plastic (CFRP) Market Analysis by Mordor Intelligence

The Carbon Fiber Reinforced Plastic Market was valued at USD 21.18 billion in 2025 and estimated to grow from USD 22.72 billion in 2026 to reach USD 32.25 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031). The growth mirrors the material’s journey from niche aerospace uses to mainstream industrial adoption as designers try to trim weight while safeguarding structural strength. Tighter sustainability rules, the electrification wave in transport, and the need for durable lightweight parts across renewable-energy infrastructure jointly advance the carbon fiber reinforced plastic market. Leading suppliers have shifted investment from pure fiber capacity to downstream processing, recycling, and circular-economy solutions that deepen customer integration. Meanwhile, capacity expansions in China and alternative precursor research in the United States shape a supply chain increasingly defined by security of supply rather than headline tonnage.

Key Report Takeaways

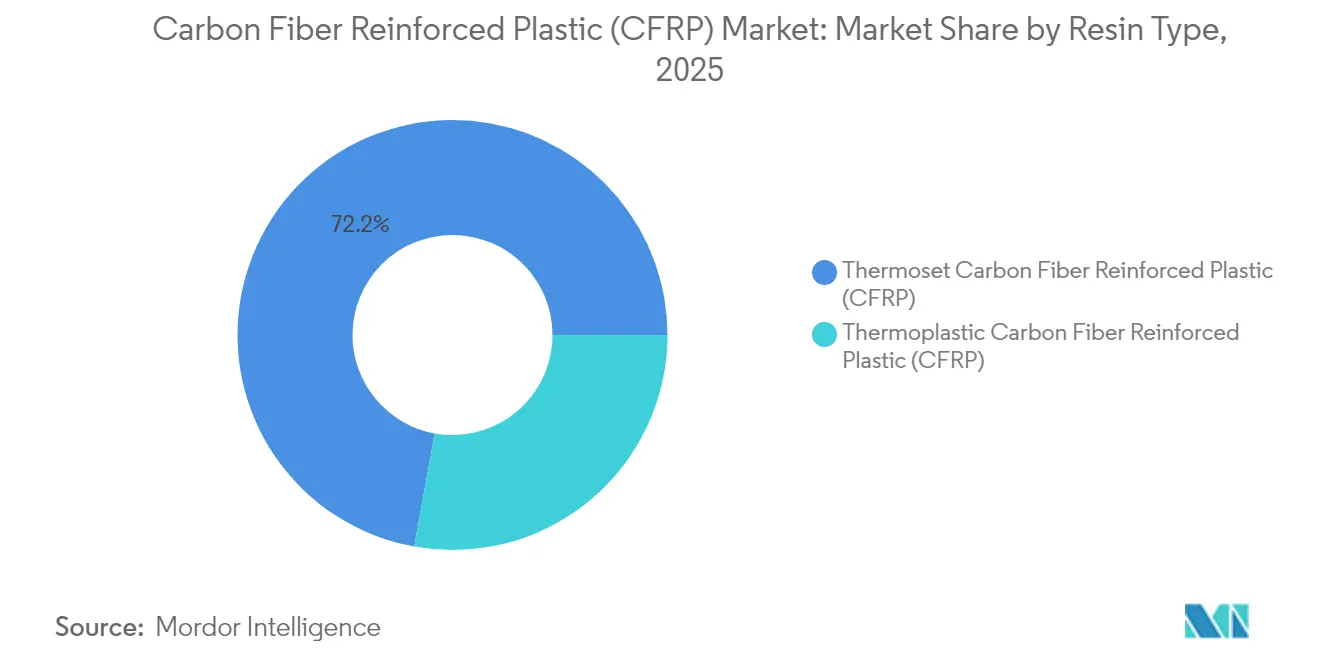

- By resin type, thermoset systems commanded 72.15% share of the carbon fiber reinforced plastic market size in 2025; thermoplastic variants record the highest 8.02% CAGR through 2031.

- By raw-material precursor, PAN fibers represented 94.75% of the carbon fiber reinforced plastic market size in 2025, while rayon-based fibers lead growth at an 8.31% CAGR to 2031.

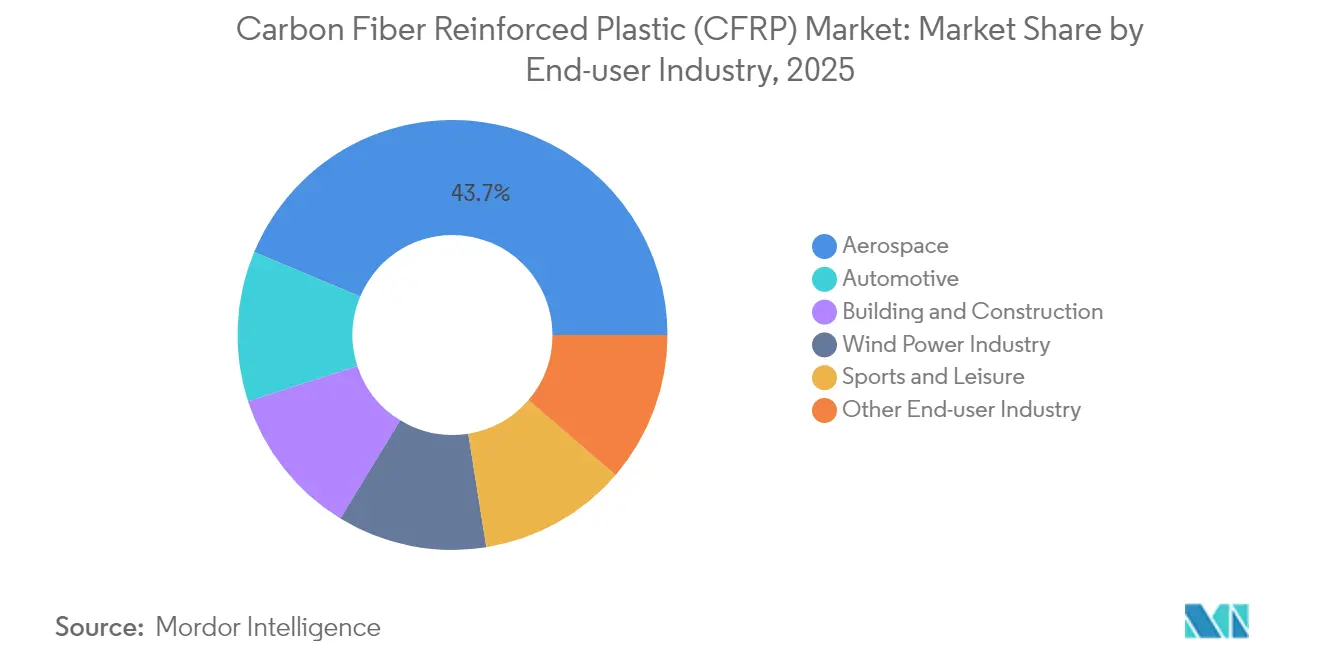

- By end-use industry, aerospace held 43.70% of the carbon fiber reinforced plastic market share in 2025, whereas automotive is projected to expand at an 8.61% CAGR to 2031.

- By geography, Asia-Pacific occupied 42.05% revenue share in 2025 and is advancing at an 8.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Carbon Fiber Reinforced Plastic (CFRP) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in commercial aircraft backlog | +1.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Electrification accelerating CFRP battery enclosures | +2.1% | Global, led by China & North America | Medium term (2-4 years) |

| Mega-blade wind turbines (>100 m) adopting CFRP spar caps | +1.5% | APAC core, spill-over to Europe & North America | Medium term (2-4 years) |

| Hydrogen mobility pressure-vessel build-out | +1.2% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| eVTOL & urban-air-mobility platforms favouring thermoplastic CFRP | +0.6% | North America & Europe, early adoption in China | Long term (≥ 4 years) |

| Closed-loop recycling unlocking low-cost rCF | +0.8% | Global, regulatory-driven in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Commercial Aircraft Backlog

The commercial aviation sector's unprecedented order backlog exceeding 15,000 aircraft creates sustained demand for carbon fiber composites. Air-framer push for thermoplastic secondary structures aims at faster build rates without sacrificing performance. Suppliers respond by qualifying multiple fiber sources to diversify risk and assure uninterrupted deliveries.

Electrification Accelerating CFRP Battery Enclosures

Electric-vehicle makers now specify carbon-fiber battery housings that cut enclosure weight by up to 91% versus aluminum. Each kilogram saved can be redeployed as extra battery capacity, extending range without enlarging the vehicle footprint. Flame-retardant thermoplastics and integrated thermal-management layers help composites meet strict safety codes, moving the carbon fiber reinforced plastic market deeper into high-volume automotive production. [1]SAE International, “Lightweight Battery Enclosures for EVs,” sae.org

Mega-blade Wind Turbines (>100 m) Adopting CFRP Spar Caps

Offshore blades longer than 100 m require carbon fiber spar caps to avoid tower strikes. Carbon fiber’s four-fold stiffness-to-weight advantage over glass reshapes blade design, lowering turbine system costs through lighter hubs and reduced foundation loads. Industry estimates show one in four new turbines already incorporates carbon-fiber caps, underpinning regional demand growth.

Hydrogen Mobility Pressure-vessel Build-out

The hydrogen economy's infrastructure requirements drive demand for Type IV pressure vessels capable of storing hydrogen at 700 bar, with carbon fiber composites essential for achieving the weight and safety targets necessary for commercial viability. Capacity expansions by Hexagon Purus in the United States and Forvia-Faurecia in Germany underline the transition from pilot lines to industrial scale. Looking ahead, liner-less Type V tanks promise further mass reductions and open new avenues for the carbon fiber reinforced plastic market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of aerospace-grade PAN precursor | -1.4% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Industrial-grade fibre capacity bottlenecks | -0.9% | Global, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Export controls on high-modulus fibre | -0.7% | China & other restricted markets | Long term (≥ 4 years) |

| Immature end-of-life recycling infrastructure | -0.5% | Global, regulatory pressure in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Aerospace-grade PAN Precursor

Aerospace-qualified polyacrylonitrile (PAN) sells for USD 33–66 per kg, limiting crossover into cost-sensitive sectors. Few suppliers meet stringent cleanliness and consistency norms, creating supply concentration risk. Water-soluble precursor research promises cost cuts, yet commercial validation in conservative aerospace supply chains will take time.

Industrial-grade Fibre Capacity Bottlenecks

Nameplate capacity of roughly 172,000 t faces quality swings and surge-demand episodes, especially from wind energy. Market cycles have seen some European producers book double-digit revenue drops when turbine orders paused, underscoring the mismatch between process flexibility and end-market volatility.

Segment Analysis

By Resin Type: Thermoplastic Revolution Accelerates

Thermoset systems commanded 72.15% of the carbon fiber reinforced plastic market share in 2025, cemented by aerospace’s long reliance on epoxy prepregs. Yet thermoplastic solutions record an 8.02% CAGR through 2031, reflecting rising needs for fast processing and recyclability. Airbus’s thermoplastic fuselage panels show cycle-time savings compatible with monthly production rates above 70 airframes, while automotive suppliers cut stamping cycles to seconds.

Thermoplastic composites also expand the carbon fiber reinforced plastic market size in mobility, eVTOL, and hydrogen storage because they can be welded or re-melted during assembly. CF-PEEK parts deliver tensile strength of 425 MPa versus 311 MPa for CF-epoxy, together with higher continuous-use temperatures. The shift is far from replacing thermosets in primary aircraft wings, but it unlocks a broad set of secondary structures and automotive parts where cost per component dictates material choice.

Note: Segment shares of all individual segments available upon report purchase

By Raw-Material Precursor: PAN Still Reigns

PAN-based fibers supplied 94.75% of the carbon fiber reinforced plastic market size in 2025 owing to unmatched mechanical performance and decades-old production lines. Rayon and lignin alternatives grow fastest at 8.31% CAGR because they promise cost relief and lower embodied carbon. U.S. Department of Energy pilot lines explore pitch-based fibers aimed at cheaper high-modulus grades for space antennas and sporting goods.

Despite research interest, PAN’s entrenched ecosystem—from solvent recovery to sizing chemistries—gives incumbent producers a scale edge. Any wide adoption of aqueous PAN or bio-precursors hinges on qualifying aerospace-grade consistency and proving economics at multi-kiloton scale. Still, venture investments into low-cost precursor technologies highlight industry readiness to diversify feedstocks as sustainability targets tighten.

By End-user Industry: Automotive Turns Corner

Aerospace retained 43.70% revenue in 2025, but automotive’s 8.61% CAGR through 2031 positions it as the prime growth engine for the carbon fiber reinforced plastic market. Battery-electric vehicles demand lightweight enclosures, roof modules, and structural-battery designs that combine crash safety with range extension. CFRP battery enclosures achieve up to 40% weight savings compared to traditional materials . Single-piece composite trays from Continental Structural Plastics showcase high-volume readiness, and leading EV start-ups embed fiber parts into vehicle floors.

Wind-power installations adopt carbon fiber spar caps for mega-blades, further swelling demand. Sports and leisure keep a steady niche for premium performance, while building and construction starts to specify carbon-fiber wraps in seismic retrofits and bridge decks.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific captured 42.05% of the carbon fiber reinforced plastic market in 2025 and exhibits the highest 8.43% CAGR through 2031. China alone consumed about 69,000 t of composites in 2023, propelled by wind, EV, and hydrogen infrastructure projects. Yet lingering gaps in T1000-level fibers and export-control headwinds could temper its aerospace momentum.

North America leverages aerospace programs and hydrogen-mobility pilots. Boeing’s backlog plus emerging eVTOL firms sustain a robust demand base, while investments in recycling plants and alternative precursors aim to fortify domestic supply. Hexcel reported 5.2% commercial-aerospace revenue growth in Q1 2024 despite logistics challenges.

Europe anchors sustainability leadership. Airbus’s thermoplastic initiatives and EU recycling regulations spur circular-economy advances. The region also channels investment into hydrogen tank manufacturing and offshore wind, both heavy carbon-fiber users. Solvay’s long-term supply deal with Boeing underlines transatlantic collaboration even as European producers tighten local value retention.

Competitive Landscape

The carbon fiber market exhibits moderate concentration, with the presence of major players, including Toray Industries Inc., Hexcel Corporation, SGL Carbon, Mitsubishi Chemical Group, and Teijin Limited. Toray’s decade-long Boeing fiber pact secures high-volume orders, while the company adds lines in California and Europe to serve industrial outlets. Hexcel concentrates on resin-film infusion and 3D-weaving, letting customers integrate value-added parts rather than raw fabrics. However, Mitsubishi Chemical advanced with ceramic-matrix composites for extreme-temperature space uses.

Carbon Fiber Reinforced Plastic (CFRP) Industry Leaders

Toray Industries Inc.

Hexcel Corporation

SGL Carbon

Mitsubishi Chemical Group

Teijin Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Mitsubishi Chemical Group unveiled a carbon-fiber-based ceramic matrix composite (C/SiC) material rated for 1,500 °C, targeting Japan’s space transportation needs.

- October 2023: In October 2023, Mitsubishi Chemical Group announced its full acquisition of CPC SRL (CPC), a prominent Italian firm known for producing and distributing automobile components made from carbon fiber reinforced plastic (CFRP).

Global Carbon Fiber Reinforced Plastic (CFRP) Market Report Scope

Carbon fiber-reinforced plastic is a polymer matrix composite material reinforced by carbon fibers. It is majorly used in the manufacturing of aircraft and rockets, as it increases fuel efficiency and reduces the weight of the aircraft body. Resin, end-user industry, and geography segment the market. By resin type, the market is segmented into thermosetting CFRPs and thermoplastic CFRPs. The market is segmented by end-user industries: aerospace, automotive, sports and leisure, building and construction, wind power industry, and other end-user industries. The report also covers the market size and forecasts for the carbon fiber reinforced plastic (CFRP) market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| Thermoset Carbon Fiber Reinforced Plastics (CFRP) |

| Thermoplastic Carbon Fiber Reinforced Plastics (CFRP) |

| Polyacrylonitrile (PAN) |

| Pitch |

| Rayon |

| Others (Lignin-based, Recycled CF (Carbon Fiber)) |

| Aerospace |

| Automotive |

| Wind Power Industry |

| Sports and Leisure |

| Building and Construction |

| Other End-user Industry |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | Thermoset Carbon Fiber Reinforced Plastics (CFRP) | |

| Thermoplastic Carbon Fiber Reinforced Plastics (CFRP) | ||

| By Raw-Material Precursor | Polyacrylonitrile (PAN) | |

| Pitch | ||

| Rayon | ||

| Others (Lignin-based, Recycled CF (Carbon Fiber)) | ||

| By End-user Industry | Aerospace | |

| Automotive | ||

| Wind Power Industry | ||

| Sports and Leisure | ||

| Building and Construction | ||

| Other End-user Industry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Carbon Fiber Reinforced Plastic Market?

The market size is estimated at USD 22.72 billion in 2026 and is projected to reach USD 32.25 billion by 2031.

Which sector will contribute most to future growth of the carbon fiber reinforced plastic market?

Automotive applications, led by electric-vehicle battery enclosures, are poised to grow at 8.61% CAGR through 2031.

How important is Asia-Pacific in the carbon fiber reinforced plastic market?

The region already commands 42.05% revenue share and shows the fastest 8.43% CAGR due to China’s massive wind-energy and EV programs.

Why are thermoplastic composites gaining share in the carbon fiber reinforced plastic market?

They allow fast, weldable processing and recyclability, helping OEMs meet cost and sustainability targets while trimming assembly cycle times.

What challenges limit wider adoption of carbon fiber in cost-sensitive industries?

High prices for aerospace-grade PAN precursor and occasional industrial-fiber capacity bottlenecks remain key obstacles.