Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

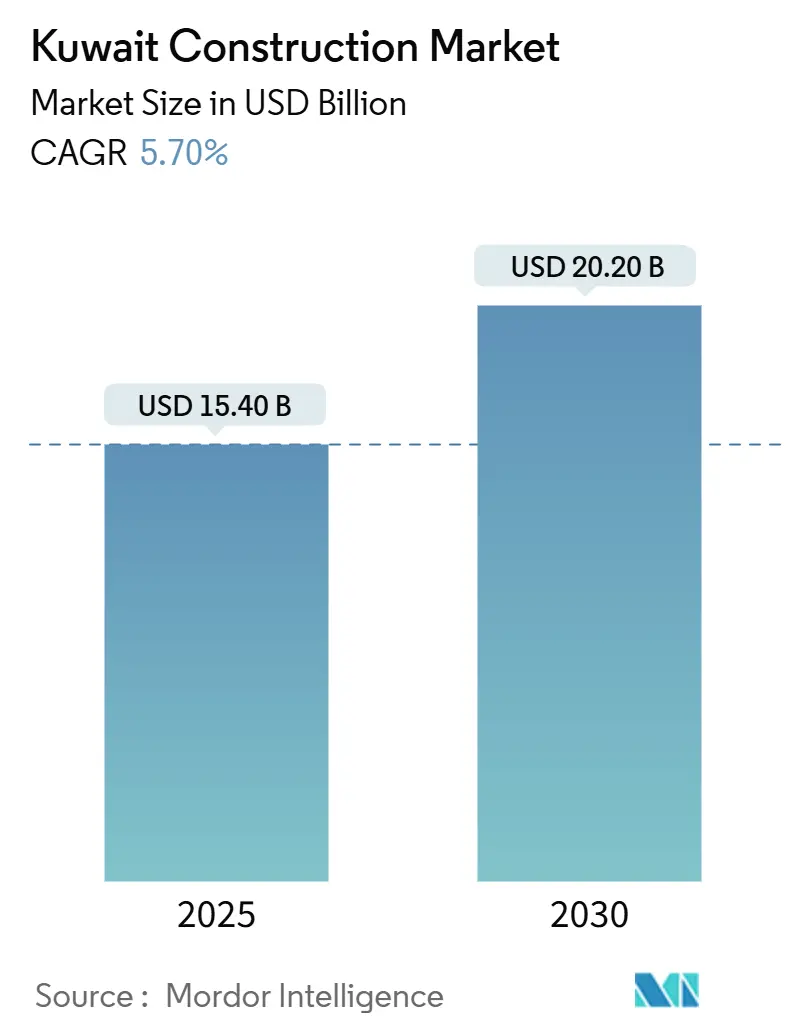

| Market Size (2025) | USD 15.40 Billion |

| Market Size (2030) | USD 20.20 Billion |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kuwait Construction Market Analysis by Mordor Intelligence

The Kuwait construction marke stands at USD 15.40 billion in 2025 and is projected to reach USD 20.20 billion by 2030, advancing at a 5.7% CAGR. Momentum stems from the government’s Vision 2035 program, an agenda that channels sizeable capital into housing, transport, power, and urban regeneration projects. Public investment remains decisive, yet private capital is expanding quickly through a widening portfolio of Public-Private Partnership initiatives that de-risk large schemes and introduce advanced delivery methods. Corporate and public clients are also prioritizing speed-to-market, energy efficiency, and digital coordination, prompting faster adoption of modular construction, Building Information Modeling (BIM), and lean work flows. Persistent labour shortages and volatile material prices temper headline growth, but they likewise accelerate mechanisation and create openings for contractors able to combine off-site fabrication with rigorous cost control. These cross-currents leave the Kuwait construction market on a moderate-growth but increasingly technology-intensive trajectory.

Key Report Takeaways

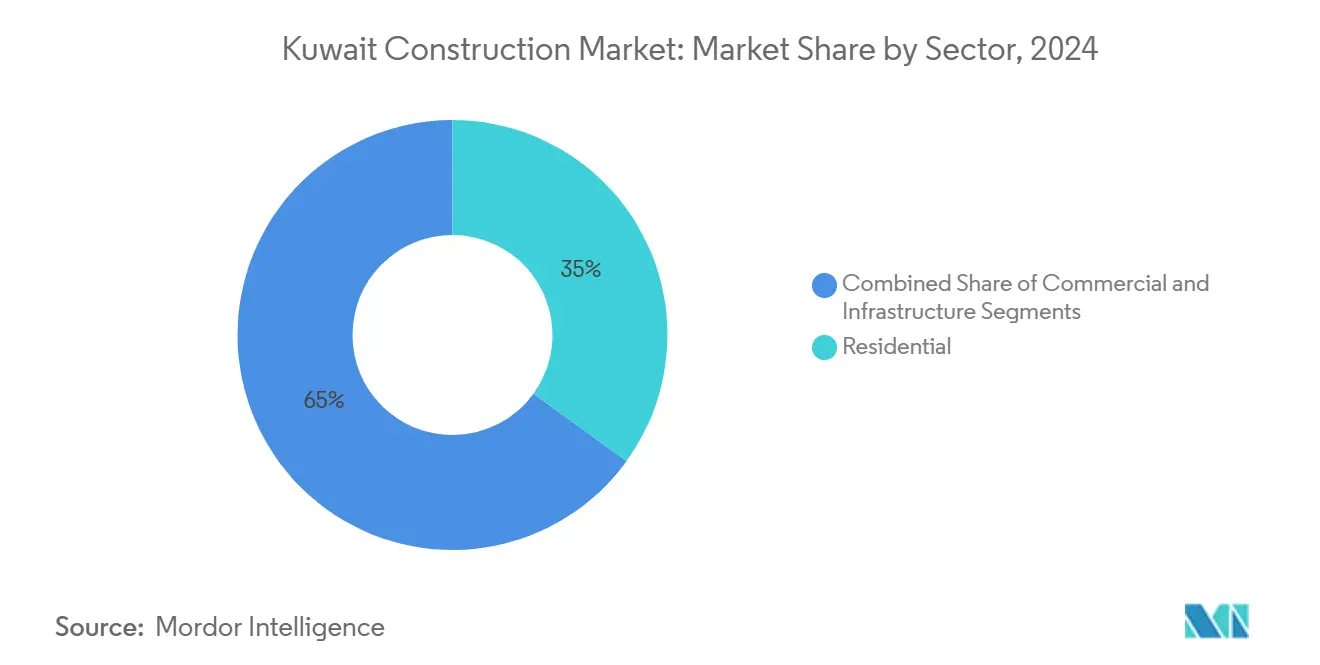

- By sector, Residential captured 35% of the Kuwait construction market share in 2024. Kuwait construction market size for residential is projected to grow at 6.5% CAGR between 2025-2030.

- By construction type, New-build captured 79% of the Kuwait construction market share in 2024. Kuwait construction market size for renovation is projected to grow at 6.5% CAGR between 2025-2030.

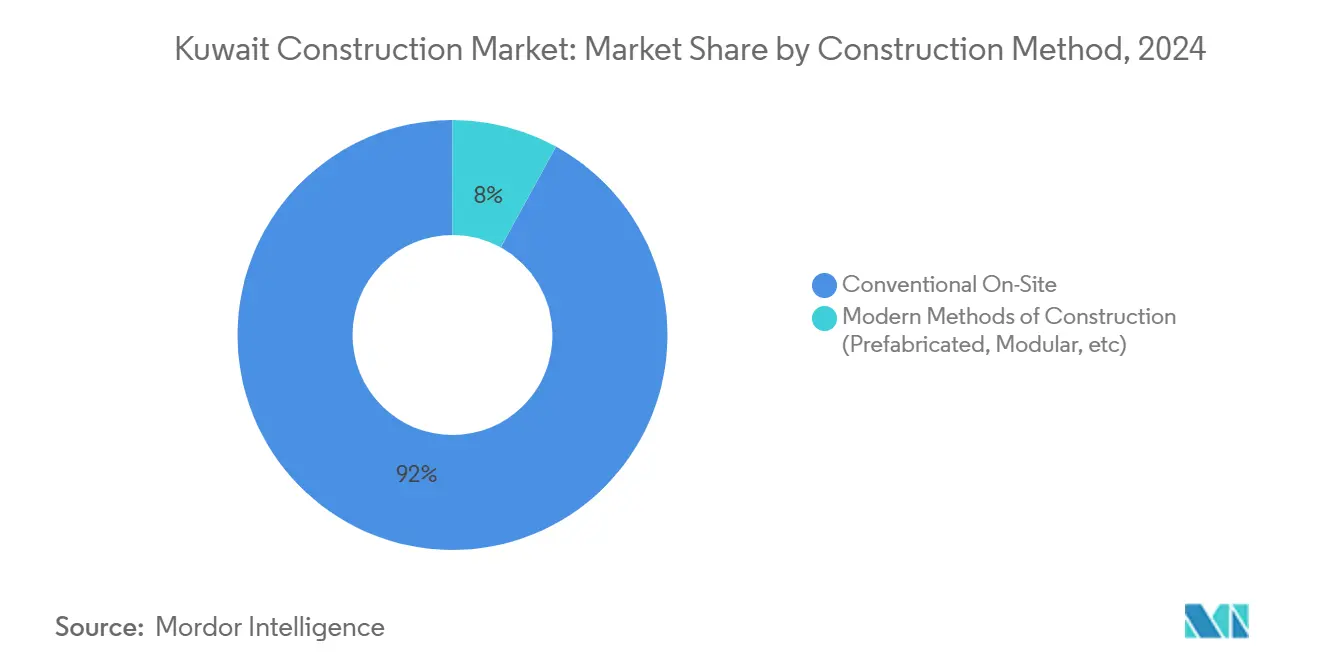

- By construction method, Conventional on-site techniques captured 92% of the Kuwait construction market share in 2024. Kuwait construction market size for modern methods is projected to grow at 7.5% CAGR between 2025-2030.

- By investment source, Public funding captured 71% of the Kuwait construction market share in 2024. Kuwait construction market size for private funding is projected to grow at 6.3% CAGR between 2025-2030.

- By governorate, Kuwait City captured 36% of the Kuwait construction market share in 2024. Kuwait construction market size for areas outside Kuwait City is projected to grow at 6.7% CAGR between 2025-2030.

Kuwait Construction Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Economic Diversification and Infrastructure Push under Kuwait Vision 2035 | 2.0% | National, with concentration in Kuwait City and new urban developments | Long term (≥ 4 years) |

| Expansion of Public–Private Partnership (PPP) Models to Mobilize Domestic and Foreign Capital | 1.5% | National, with emphasis on energy, transportation, and housing sectors | Medium term (2-4 years) |

| Ongoing Oil Sector Investments Driving Demand for Industrial and Support Infrastructure | 1.2% | Al Ahmadi and oil-producing regions | Medium term (2-4 years) |

| Growing Adoption of Precast, Modular, and Industrialized Building Systems for Faster Delivery | 1.0% | Kuwait City and major urban centers | Short term (≤ 2 years) |

| Rollout of Large-Scale Road and Transport Development Programs to Improve Connectivity | 0.8% | National, with focus on intercity connections and Kuwait City | Long term (≥ 4 years) |

Source: Mordor Intelligence

Accelerated infrastructure drive under Vision 2035

Vision 2035 assigns top priority to modern transport corridors, new economic zones, and public-service facilities. Government budgets earmark USD 5.6 billion for 124 projects in FY 2025-2026, ensuring a visible pipeline that anchors contractor order books. Landmark schemes such as Terminal 2 at Kuwait International Airport and the Umm Al-Hayman Wastewater Treatment Plant illustrate the breadth of opportunities spanning aviation, water, and environmental services. New-city programmes—including South Saad Al-Abdullah, set to house 150,000 residents—extend construction activity into previously under-served terrain, while the Northern Economic Zone is designed to lift non-oil GDP and create private-sector jobs.[1]Aisha Al-Ajmi, “Kuwait National Development Plan 2020-2025"Together, these investments underpin long-cycle demand across building, civil, and utilities segments in the Kuwait construction market.

Expansion of Public–Private Partnership frameworks

The Kuwait Authority for Partnership Projects (KAPP) streamlines risk-sharing between government and investors and has become pivotal for power, desalination, and real-estate concessions. Current mandates cover the Khairan power complex and successive phases of the Al-Zour North plant, supporting 2.7 GW of incremental capacity. Real-estate PPPs worth up to USD 10 billion, ranging from shopping malls to leisure parks, are also slated for tender.[3]Ahmed Hagagy, “Kuwait eyes PPP energy projects to help end power crisis" These structures lower fiscal pressure, invite global know-how, and accelerate delivery, broadening the capital base that fuels the Kuwait construction market.

Ongoing oil-sector investment

Kuwait continues to budget roughly USD 10 billion per year for upstream and midstream oil projects, creating a parallel stream of industrial construction. The Kuwait Oil Company’s plan to drill 141 wells and erect a new office complex underscores sustained demand for specialised civil, mechanical, and building packages. Heavy investment in pipelines, gathering centres, and support buildings keeps the Kuwait construction market diversified while funding the broader economic transition.

Rising adoption of modular, precast, and BIM-enabled delivery

Acute labour shortages and tight completion schedules make industrialised construction appealing. Large-span space-frame steel roofs are now common in malls and airport terminals, offering rapid assembly and column-free interiors. Government housing programmes likewise pilot precast panels to cut onsite activity in Kuwait’s harsh climate. Academic studies confirm that BIM adoption within the Ministry of Public Works improves coordination and waste reduction, though skills gaps and traditional mind-sets remain hurdles.[4]Metalart Space Frame, “Space Frame Steel Structures in Kuwait" These technology shifts are set to lift the efficiency baseline across the Kuwait construction market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Labour Shortages Affecting Construction Productivity and Scheduling | -1.2% | National, with acute impact in Kuwait City | Medium term (2-4 years) |

| Land Acquisition Delays and Regulatory Bottlenecks Slowing Project Execution | -0.8% | National, with concentration in new development areas | Medium term (2-4 years) |

| Elevated Construction Material Costs Undermining Project Profitability and Budgeting | -0.5% | National | Short term (≤ 2 years) |

Source: Mordor Intelligence

Chronic labour shortages affecting productivity

The pandemic triggered an exodus of experienced tradespeople, and replacement inflows have not matched demand. Field research among 230 construction professionals links manpower gaps with longer planning windows and project delays. Wage escalation strains budgets, prompting contractors to mechanise tasks and import modular assemblies. Government localisation programmes face structural barriers, meaning workforce tightness will linger, compressing schedules and margins across the Kuwait construction market.

Elevated construction-material costs

Average private-housing build costs jumped 35%, from USD 554 to USD 749.5 per m², between 2020 and 2024; a 1,240 m² home therefore rose to USD 924,000 iflkuwait.com. Inflation, logistics bottlenecks, and global commodity volatility keep procurement risk high. A ministerial committee now monitors pricing and supply yet expects elevated quotations to persist for five years zawya.com. Contractors must hedge materials and engineer value options to sustain profitability.

Segment Analysis

By Sector: Residential Demand Drives Growth

Residential construction retained the largest slice of the Kuwait construction market at 35% in 2024, powered by an acute housing backlog and welfare grants that subsidise land and mortgages for nationals. The Public Authority for Housing Welfare has 217 public buildings in progress, with 92 in Mutlaa City and 74 in the Affordable Housing Project. Ongoing delivery of South Al-Mutlaa—planned for 28,000 families—signals a deep pipeline built around standardised villas and mid-rise blocks. These factors underpin a 6.5% CAGR for the residential slice, outpacing the wider Kuwait construction market.

Commercial development displays mixed momentum. Logistics platforms gain traction owing to Kuwait’s ambitions as a Gulf trade node; the USD 648 million Shuwaikh Port logistics city will add warehouses, offices, and retail by 2028. Office supply is lifted by public entities such as the Kuwait Oil Company’s 1,200-office Ahmadi complex, while retail remains selective but benefits from experiential formats embedded in masterplans. Infrastructure construction, notably rail and metro lines, creates sustained heavy civil demand, and power-generation schemes aim for 25 GW capacity by 2025. Together these drivers keep the Kuwait construction market diversified.[5]Kuwait Direct Investment Promotion Authority, “Investing in Kuwait"

Note: Segment shares of all individual segments available upon report purchase

By Construction Type: Renovation Gains Momentum

New-build work represented 79% of the Kuwait construction market size in 2024, mirroring the emphasis on greenfield cities and transport corridors. Nonetheless, renovation and expansion projects are accelerating at a 6.5% CAGR as authorities refurbish ageing schools, hospitals, and ministries in core urban zones. Recent tenders include structural upgrades at Abdullah Al-Salem University and Ministry of Trade facilities. Private landlords are retro-fitting older commercial blocks to attract tenants seeking modern fire, IT, and sustainability standards. Rising utility tariffs also prompt energy retrofits, further enlarging the renovation slice of the Kuwait construction market.

Maintenance and restoration contracts increasingly bundle performance-based requirements, encouraging contractors to deploy predictive analytics and asset-management software. This evolution fosters recurring revenue streams that offset the cyclicality of new-build awards. As urban districts mature, the renovation segment is expected to command greater Kuwait construction market share beyond 2030.

By Construction Method: Modern Techniques Advance

Conventional on-site techniques still commanded 92% of activity in 2024, reflecting entrenched site practices and existing equipment fleets. Yet modern approaches—precast elements, volumetric modules, and steel space frames—are projected to compound at 7.5%, significantly faster than overall Kuwait construction market growth. Large public projects now mandate BIM for design coordination, and lean performance audits indicate a baseline adherence of 68.5% across pilot sites. Early movers combine laser scanning, digital twins, and just-in-time delivery to shrink programme durations, critical amid labour shortages.

Field trials highlight trade-offs: research shows that fiberglass modular blocks consume more cooling energy than concrete buildings in Kuwait’s hyper-arid climate, pushing designers to integrate advanced insulation and reflective façades. Nevertheless, clients targeting rapid occupancy increasingly prioritise off-site solutions. This shift will continue reallocating Kuwait construction market share toward industrialised suppliers and integrators.

By Investment Source: Private Capital Accelerates

State spending remained dominant at 71% of Kuwait construction market size in 2024, underpinned by USD 5.6 billion budgeted for FY 2025-2026 projects.[2]Nadim Kawach, “Kuwait approves USD 5.6 billion projects in 2025-2026 budget" Still, private investment is rising faster, propelled by structured PPP deals and bank lending of USD 12.5 billion in 2024. KAPP has broadened its remit beyond power to include mixed-use real estate, solid-waste treatment, and district cooling concessions, facilitating risk-adjusted returns attractive to international sponsors.

Corporate social investment also aligns with urban-beautification schemes; the National Bank of Kuwait allocated USD 9.7 million to the Shuwaikh Beach redevelopment. Government outlays of USD 233.3 million for private-sector-support projects further expand the funnel. These dynamics gradually recalibrate the Kuwait construction market toward a more balanced public-private funding mix.

Geography Analysis

Kuwait City’s 36% share stems from its role as the administrative and financial nucleus. Mixed-use skyscrapers, the Sulaibikhat Bay reclamation, and the USD 4.3 billion airport upgrade dominate skyline activity. High land values and limited plots compel vertical density, while metro construction inserts a fresh layer of transit-oriented demand. Ageing public buildings generate steady retrofit work, adding depth to the Kuwait construction market within city limits.

Al Ahmadi ranks second, driven by hydrocarbon capital spend. The USD 80 million Ahmadi Office Complex and drilling support buildings sustain demand for high-spec prefabricated modules and process infrastructure. Surrounding residential projects cater to energy workers, expanding urban boundaries and blending industrial and community facilities.

Peripheral governorates register the steepest growth. South Sabah Al-Ahmad (main roads 48.6% complete) and South Saad Al-Abdullah (32% complete) showcase large-scale masterplans that integrate housing, schools, and utilities.[6]iCorpPro, “New Kuwait National Rail Road System" Rail, highway, water, and power lines link these sites back to Kuwait City, compressing travel times and distributing economic activity. Together, these corridors ensure the Kuwait construction market evolves from a single-city focus into a multi-node national network.

Competitive Landscape

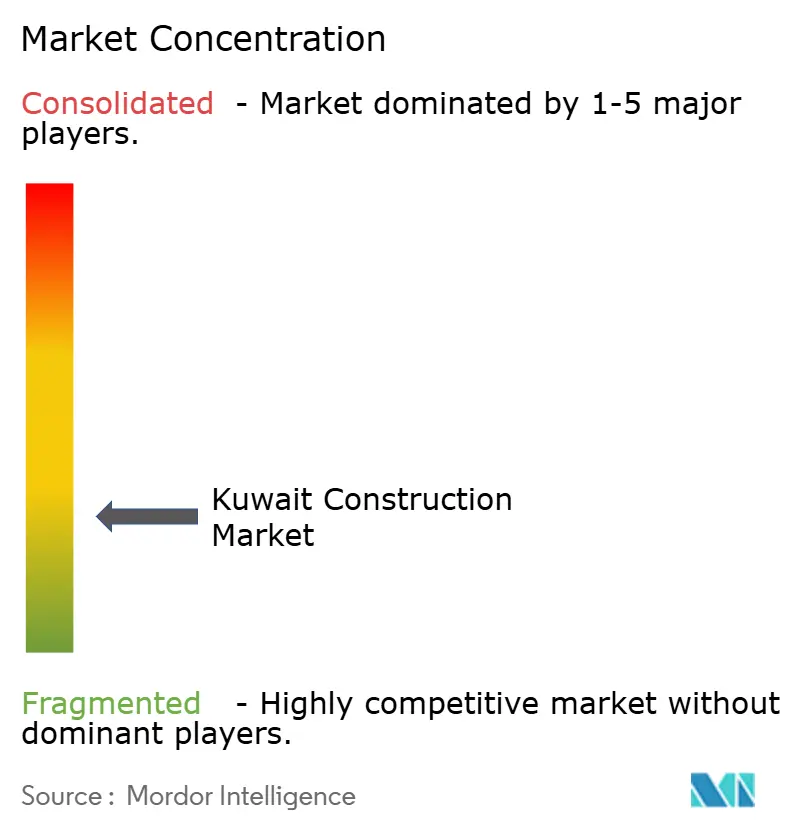

The Kuwait construction market exhibits low concentration. Local heavyweights such as Combined Group Contracting Co, Kuwait Company for Process Plant Construction & Contracting (KCPC), and Mushrif Trading & Contracting Co leverage deep government relationships and equipment fleets. International majors—including Chinese, South Korean, and European contractors—secure mega-projects where EPC skill sets, supply-chain access, and preferential export finance prove decisive. China Gezhouba Group’s infrastructure contracts in new cities and Korean firms’ bids for next-generation clean-energy complexes illustrate the trend.

Competitive differentiation hinges on digital delivery and risk management. Early adopters of BIM and lean analytics report lower re-work and tighter cash cycles, despite sector-wide challenges in senior-management endorsement and skilled BIM modellers. Workforce scarcity also shifts attention to mechanised equipment, robotics, and structured training that raise productivity per head. Contractors able to integrate design, off-site fabrication, and finance are better positioned to capitalise on PPP concessions in power, waste, and transport.

Financiers recalibrate exposure as project risks evolve. Bank financing fell 12.1% month-on-month in December 2024, signalling stricter credit filters, yet absolute lending still reached USD 12.5 billion in 2024. Diversifying funding channels—such as sukuk and export-credit agency guarantees—therefore become strategic weapons in winning work. Overall, competitive intensity remains moderate, with scope for consolidation as clients favour well-capitalised firms capable of delivering complex, fast-track projects.

Kuwait Construction Industry Leaders

-

Combined Group Contracting Co.

-

Kuwait Company for Process Plant Construction & Contracting (KCPC)

-

Mushrif Trading & Contracting Co.

-

Mohammed Abdulmohsin Al-Kharafi & Sons (MAK)

-

Hyundai Engineering & Construction Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Kuwait Build 2025 hosted 120 exhibitors showcasing smart-home, façade, and low-carbon materials, reinforcing supply-side innovation.

- March 2025: China Gezhouba Group signed USD 557 million infrastructure contracts for South Saad Al-Abdullah new city.

- February 2025: The Ministry of Electricity, Water, and Renewable Energy unveiled plans for 20 new buildings, including a training centre and design hub, to ease overcrowding.

- February 2025: Kuwait Oil Company released an RFP for the USD 80 million Ahmadi Office Complex, targeting award in Q2 2025.

Kuwait Construction Market Report Scope

Construction is the installation, maintenance, and repair of buildings and other stationary structures, as well as the construction of roadways and service facilities that form fundamental components of structures and are required for their operation.

Construction encompasses the processes involved in constructing buildings, infrastructure, industrial facilities, and related operations from start to finish. A complete assessment of the construction market in Kuwait includes a review of the economy and the contribution of sectors in the economy, a market overview, market size estimation for key segments, and emerging trends in the market segments in the report.

The report sheds light on the market trends like growth factors, restraints, and opportunities in this sector. The competitive landscape of the market is depicted through the profiles of active, vital players. The report also covers the impact of the COVID–19 pandemic on the market and future projections.

The construction market includes upcoming, ongoing, and growing construction projects in different sectors. The Kuwaiti construction market is by sector (commercial, residential, industrial, infrastructure (transportation construction), and energy and utilities construction). The market size and forecasts for the construction market in Kuwait are provided in terms of value (USD) for all the above segments.

| By Sector | Residential | Apartments/Condominiums | |

| Villas/Landed Houses | |||

| Commercial | Office | ||

| Retail | |||

| Industrial and Logistics | |||

| Others | |||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | ||

| Energy & Utilities | |||

| Others | |||

| By Construction Type | New Construction | ||

| Renovation | |||

| By Construction Method | Conventional On-Site | ||

| Modern Methods of Construction (Prefabricated, Modular, etc) | |||

| By Investment Source | Public | ||

| Private | |||

| By Governorate | Kuwait City | ||

| Al Ahmadi | |||

| Hawalli | |||

| Farwaniya | |||

| Rest of Kuwait | |||

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Governorate

| Kuwait City |

| Al Ahmadi |

| Hawalli |

| Farwaniya |

| Rest of Kuwait |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of Kuwait Construction Market?

The Kuwait Construction Market size is expected to reach USD 14.77 billion in 2025 and grow at a CAGR of 5.93% to reach USD 19.70 billion by 2030.

How fast is the current Kuwait Construction Market expected to grow?

It is projected to expand at a 5.70% CAGR, reaching USD 20.20 billion by 2030.

Which governorate offers the strongest growth prospects?

Areas outside Kuwait City, notably South Saad Al-Abdullah and South Sabah Al-Ahmad, are projected to achieve a 6.7% CAGR through 2030 as new cities rise.

Which segment is growing fastest?

Renovation activity is the fastest-growing construction type, advancing at a 6.5% CAGR as authorities modernize ageing assets.

Page last updated on: June 26, 2025