Web Hosting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 182.28 Billion |

| Market Size (2031) | USD 300.21 Billion |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

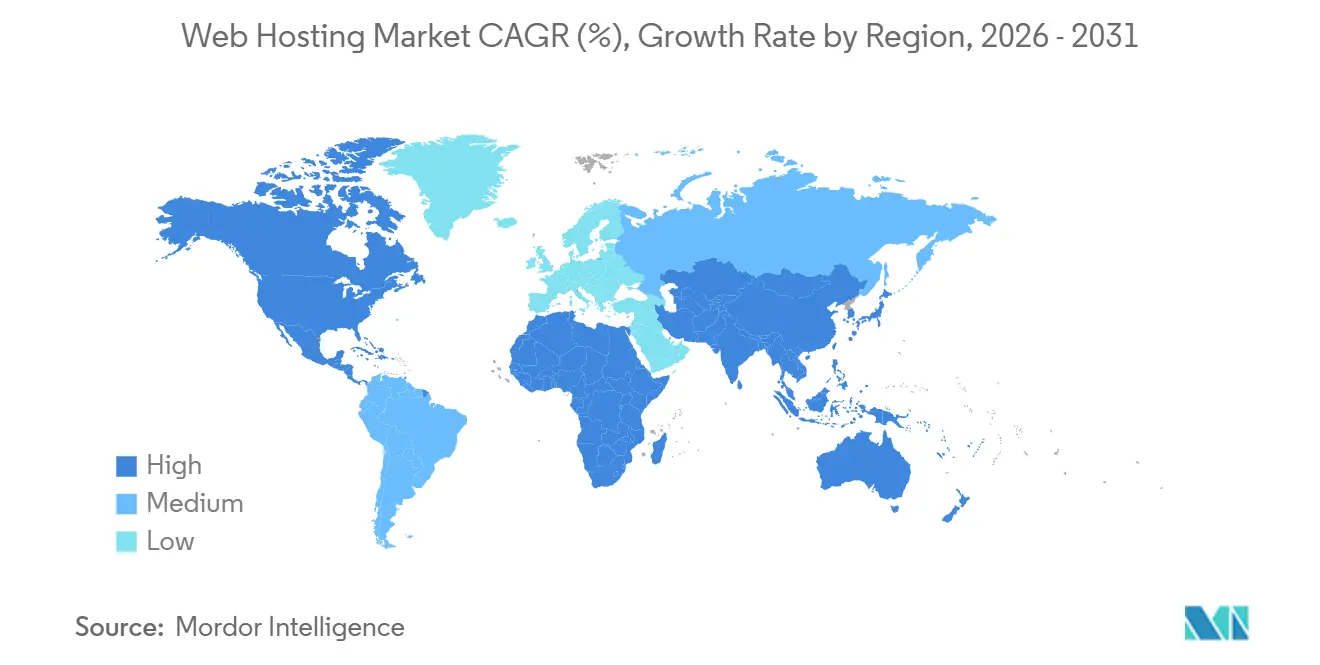

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Web Hosting Market Analysis by Mordor Intelligence

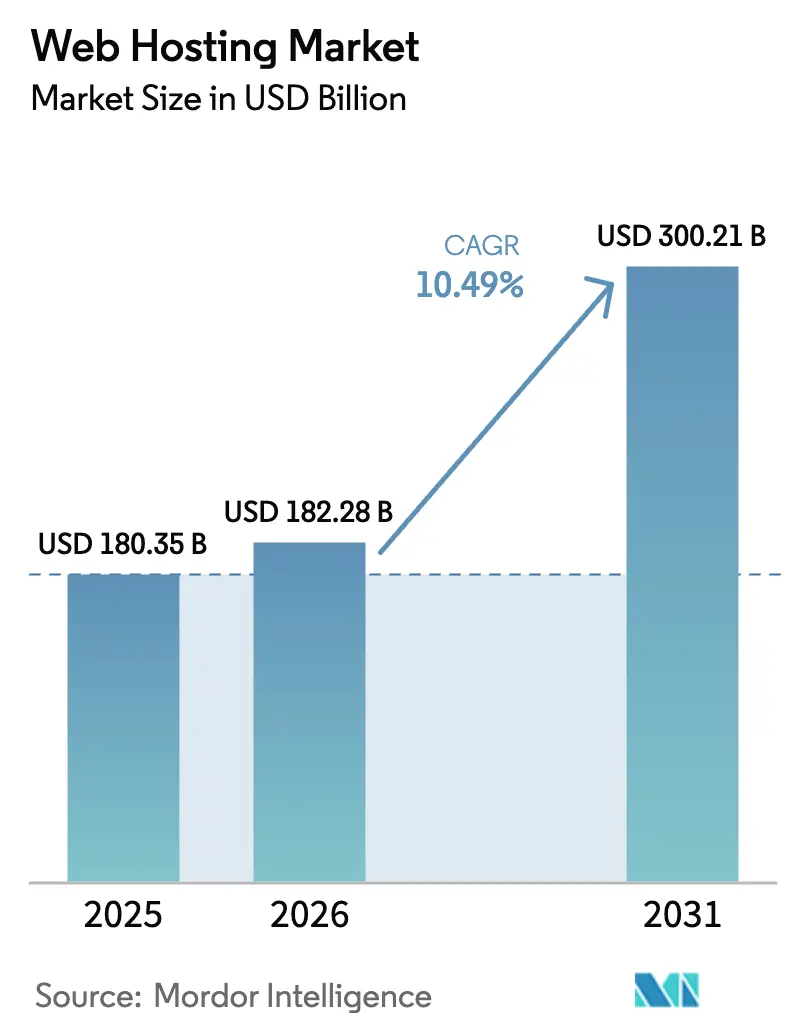

The Web Hosting market size was valued at USD 180.35 billion in 2025 and estimated to grow from USD 182.28 billion in 2026 to reach USD 300.21 billion by 2031, at a CAGR of 10.49% during the forecast period (2026-2031). Ongoing adoption of generative AI workloads is steering enterprises toward GPU-ready edge infrastructure that legacy shared servers cannot support. Data-residency rules in the European Union, India, and China are accelerating hybrid deployments as firms distribute applications across on-premise, sovereign, and hyperscale clouds. Small merchants launching digital storefronts on no-code platforms are demanding 99.99% uptime, which is shifting spend toward cloud and managed WordPress tiers. Providers now compete on bundled observability tools and carbon-neutral credentials because basic uptime promises have become table stakes.

Key Report Takeaways

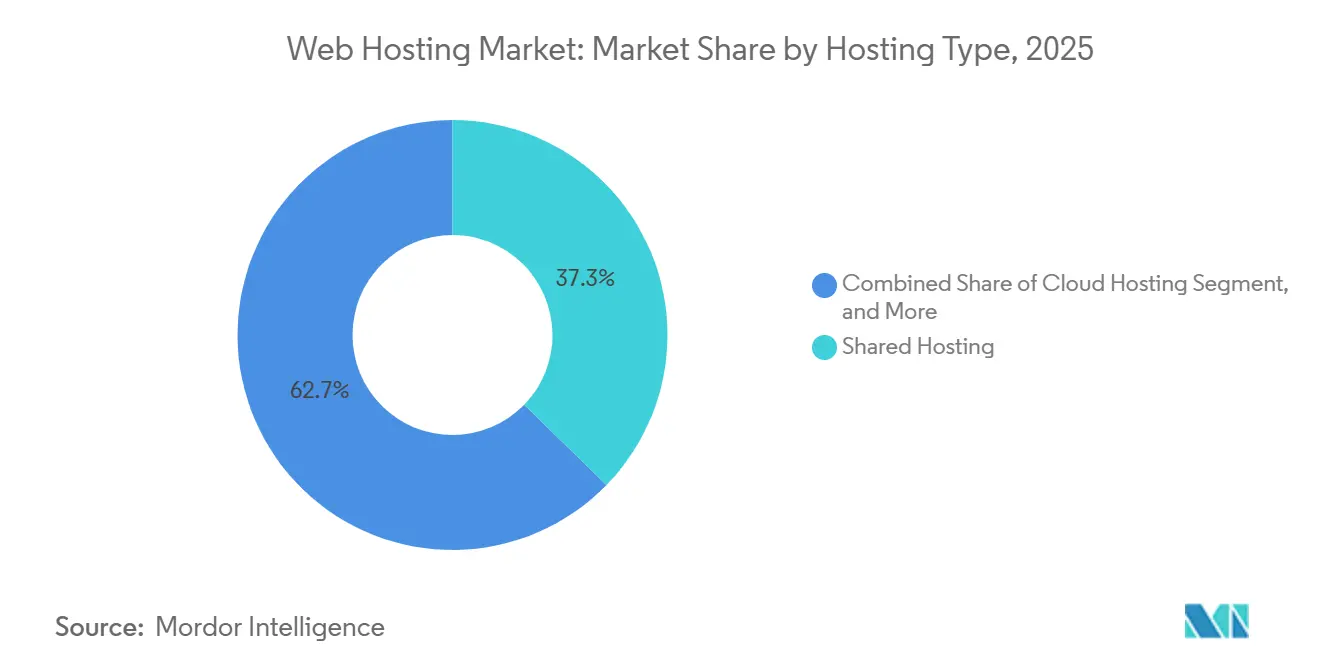

- By hosting type, shared hosting led with 37.28% of 2025 revenue while cloud hosting is advancing at a 10.53% CAGR through 2031.

- By deployment mode, public cloud held 45.58% of the 2025 base yet hybrid and multi-cloud architectures are forecast to expand at a 10.75% CAGR to 2031.

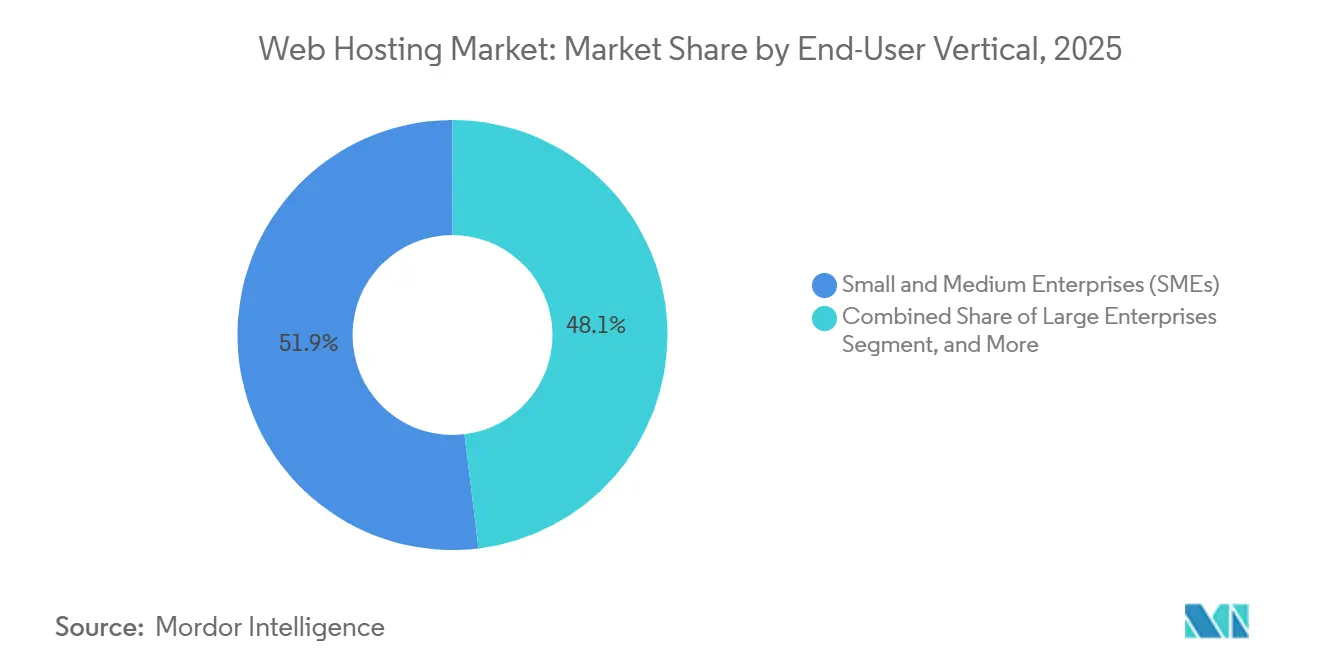

- By end-user vertical, small and medium-sized enterprises accounted for 51.93% share in 2025, whereas software developers and SaaS start-ups are projected to grow at 10.82% CAGR.

- By application, e-commerce stores captured 34.74% revenue in 2025; web applications are set to post the fastest 10.51% CAGR through 2031.

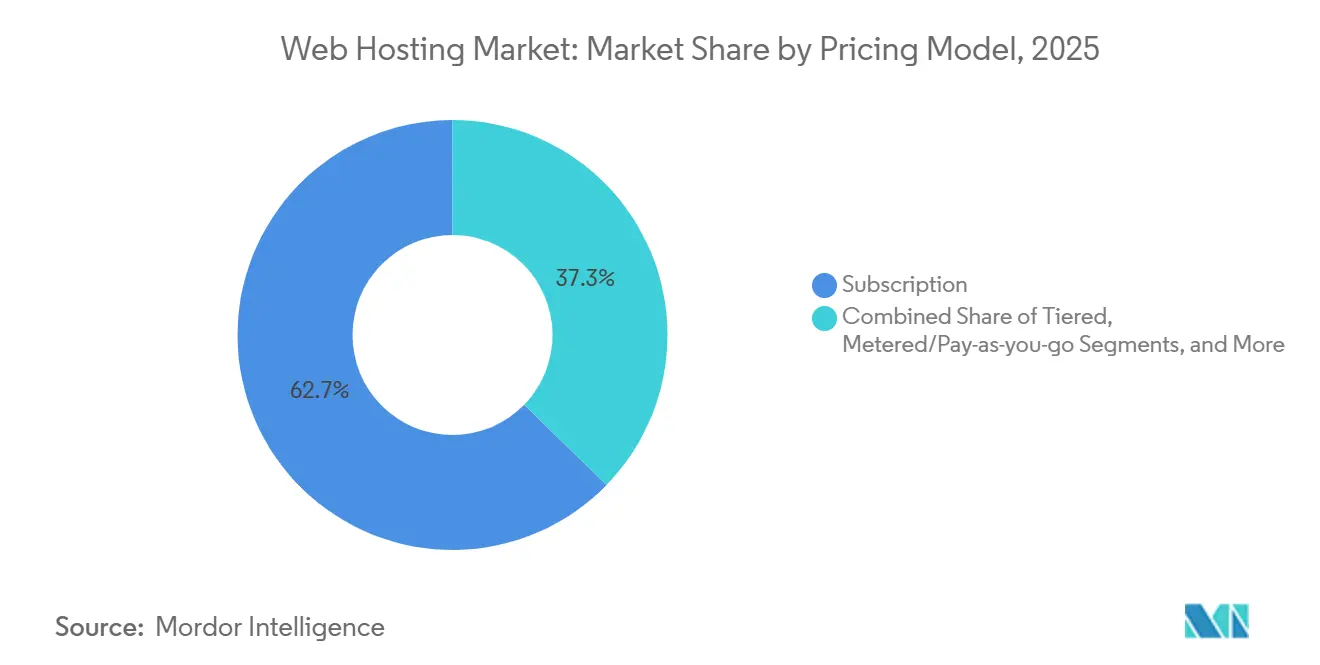

- By pricing model, subscription plans commanded 62.71% of 2025 spending, while metered pay-as-you-go models are projected to rise at a 10.64% CAGR.

- By geography, North America represented 38.63% in 2025 and Asia-Pacific is poised for a 10.93% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Web Hosting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive E-Commerce Expansion Among SMEs | +2.8% | Global, with concentration in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Surging Demand for High-Availability and Low-Latency Sites | +2.3% | Global, particularly North America, Europe, and developed APAC markets | Medium term (2-4 years) |

| Rapid Migration to Hybrid and Multi-Cloud Architectures | +1.9% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Carbon-Neutral Green Hosting Differentiation | +1.6% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Gen-AI-Ready Edge and GPU Server Demand Surge | +1.4% | Global, led by North America and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive E-Commerce Expansion Among SMEs

No-code commerce platforms counted 4.6 million global merchants in late 2024, forcing providers to deliver elastic infrastructure that can absorb flash-sale traffic. Micro-retailers now expect bundles with PCI-DSS scans and integrated payment gateways, so value is shifting from raw server capacity to turnkey storefront enablement. Providers that embed hosting inside end-to-end commerce suites gain share among merchants lacking DevOps staff. Cross-border shopping in Southeast Asia requires edge points of presence to keep latency under 100 milliseconds, encouraging regional data-center rollouts.[1]National Payments Corporation of India, “UPI Crosses 100 Billion Transactions Annually,” npci.org.in Monthly subscription contracts improve agility for retailers but raise churn risk for hosts, prompting investment in predictive-retention tooling.

Surging Demand for High-Availability and Low-Latency Sites

Financial regulators now classify digital-channel uptime as a compliance metric; European Banking Authority rules mandate 99.95% availability for banks. Video streaming, real-time gaming and tele-medicine rely on edge caching within 50 kilometers of users, which only hyperscalers and mature CDN operators can supply at scale. The rise of serverless computing has normalized globally distributed execution, removing the bottleneck of single-region origin servers. Latency-sensitive workloads tied to autonomous vehicles and industrial IoT require 5G-integrated edge hosting, a gap that traditional shared hosts struggle to bridge. Observability dashboards exposing latency and error rates in real time have become differentiators more than basic uptime guarantees.[2]Amazon Web Services, “AWS re:Invent 2024 – Lambda Processes 10 Trillion Invocations,” aws.amazon.com/blogs

Rapid Migration to Hybrid and Multi-Cloud Architectures

Eighty-seven jurisdictions enforce data-location mandates, fragmenting workloads across AWS GovCloud, Alibaba Cloud and sovereign providers such as OVHcloud. Enterprises mix on-premise VMware clusters with Azure SaaS and Google AI pipelines, introducing identity, networking and cost allocation complexity. Kubernetes adoption-7.1 million developers in 2024-lowers switching costs and intensifies price competition across clouds.[3]Cloud Native Computing Foundation, “Kubernetes Annual Survey 2024,” cncf.io Third-party orchestration platforms and managed-service brokers prosper by masking provider-specific quirks. Varying GDPR, ISO 27001 and local breach-notification demands require region-specific audit trails that strain small hosting firms.

Carbon-Neutral Green Hosting Differentiation

Corporate net-zero pledges push providers to secure renewable energy, deploy liquid cooling and publish granular emissions data. Certifications from The Green Web Foundation allow SMEs to display sustainability badges, winning eco-conscious consumers. Custom silicon such as AWS Graviton3 enhances performance-per-watt and widens the moat for integrated clouds. Renewable-power shortages in emerging markets limit green differentiation to regions with mature wind and solar grids. Lack of unified carbon accounting opens space for third-party verification services auditing energy sourcing and hardware life cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Shortage of Cloud-Certified Hosting Engineers | -1.2% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Escalating Cyber-Attacks and Data-Sovereignty Regulation | -1.5% | Global, with heightened impact in Europe and Asia-Pacific | Medium term (2-4 years) |

| Margin Pressure from Race-to-Zero Pricing | -0.9% | Global, particularly in commoditized shared-hosting segments | Medium term (2-4 years) |

| Energy-Price Volatility and Power-CAPEX Inflation | -0.7% | Europe and Asia-Pacific, moderate impact in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Cloud-Certified Hosting Engineers

LinkedIn reported demand for cloud architecture skills outpacing supply by 2.3 times in 2025. Median salaries above USD 150,000 tempt engineers to move from hosting vendors to fintechs and SaaS unicorns. Under-staffed teams delay automation projects that customers expect, while multi-month reskilling programs carry uncertain returns. Remote work narrows traditional wage arbitrage, and credentials alone no longer guarantee competence, lengthening hiring cycles.

Escalating Cyber-Attacks and Data-Sovereignty Regulation

Ransomware groups view hosts as high-leverage targets; one 2024 breach encrypted 3,000 customer servers and demanded USD 10 million. Mandates such as India’s Data Protection Act and China’s Cybersecurity Law force localized storage and conflicting notification deadlines. Fines up to 4% of global revenue make non-compliance existential, prompting consolidation toward well-capitalized providers. Zero-trust migrations divert budget from capacity growth to security hardening, while a global shortfall of four million cybersecurity workers limits in-house defense capability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hosting Type: Cloud Hosting Disrupts Legacy Models

Shared hosting controlled 37.28% revenue in 2025 yet the segment is losing ground as even entry-level users migrate to cloud platforms offering auto-scaling and stronger security. Cloud hosting is forecast to grow at 10.53% and is expected to command a sizeable share of the Web Hosting market size by 2031. VPS and dedicated hosting hold niche positions among developers wanting root access and regulated industries needing single-tenant hardware. Colocation attracts firms retaining physical control while outsourcing facilities operations. Managed WordPress tiers bundle caching and staging, enabling agencies to focus on content rather than infrastructure.

The shift toward cloud accelerated in 2024-2025 as providers deprecated cPanel-based plans in favor of Kubernetes-orchestrated stacks. Multi-cloud became mainstream with 78% of enterprises running workloads across at least two vendors, reflecting strategic avoidance of lock-in. Managed WordPress players now add headless CMS features so clients can push static assets to edge networks, shrinking page-load times and extending the Web Hosting market reach into modern Jamstack workflows.

By Deployment Mode: Hybrid Architectures Gain Traction

Public cloud still accounts for 45.58% of 2025 spend; however, hybrid and multi-cloud environments are projected to grow at a 10.75% CAGR through 2031 as compliance requirements drive workload distribution. This shift will increase the Web Hosting market share of hybrid solutions in regions that enforce strict data-location laws. Private cloud remains relevant where physical isolation is mandated, though hosted private services blur the line between dedicated and multitenant.

Managing hybrid estates demands synchronized identity, replicated databases, and consistent tagging. Kubernetes delivers portability, while FinOps teams optimize cost spikes that occur when always-on workloads migrate unmodified. The rise of confidential computing-Intel SGX, AMD SEV, ARM TrustZone-enables hybrid deployments where sensitive data remains encrypted even during processing, addressing regulatory concerns that previously forced on-premise deployment of workloads handling personally identifiable information.

By End-User Vertical: SMEs Drive Volume Growth

Small and medium-sized enterprises held 51.93% of 2025 revenue, underscoring their outsized influence on Web Hosting market dynamics. Software developers and SaaS start-ups show the highest 10.82% CAGR as containerized pipelines replace monolithic stacks. Large enterprises maintain substantial hosting footprints for customer-facing web properties, internal portals, and data-lake infrastructure, yet increasingly negotiate enterprise discount programs and reserved-instance commitments that compress provider margins.

The proliferation of low-code and no-code development platforms-Gartner estimated 65% of application development will use low-code tools by 2024-enables SMEs to build custom applications without hiring engineering teams, driving demand for hosting that abstracts infrastructure complexity behind visual interfaces and pre-built integrations. SaaS startups increasingly adopt platform-as-a-service offerings like Heroku, Render, and Railway that eliminate server management entirely, allowing developers to deploy code via Git push and scale automatically based on traffic patterns without provisioning load balancers or configuring auto-scaling groups.

By Application: Web Applications Accelerate

E-commerce stores accounted for 34.74% of 2025 spend, driven by continued retail digitization. Web applications, however, are forecast to grow at 10.51% and capture a larger share of the Web Hosting market by 2031. Static-site generators and Jamstack architectures push content to edge networks, eliminating origin latency. Other applications, including game servers, video streaming, and IoT data ingestion, address vertical-specific requirements with distinct performance and scalability characteristics that general-purpose hosting cannot economically serve.

The shift from monolithic applications to microservices architectures-each business capability deployed as an independent service communicating via APIs-drives demand for container orchestration platforms like Kubernetes that automate deployment, scaling, and failure recovery across distributed infrastructure. Jamstack architecture gained traction as developers decouple front-end presentation from backend logic, deploying static assets to CDNs while serverless functions handle dynamic interactions, reducing hosting costs by 60-80% compared to traditional server-rendered applications, according to Netlify's 2024 customer case studies.

By Pricing Model: Metered Models Gain Share

Subscription plans retained 62.71% share in 2025 because predictable invoices simplify budgeting. Metered consumption pricing is projected to grow at a 10.64% CAGR, reflecting CFOs' insistence on transparency and developers' preference for paying only for used resources. Tiered bundles ease the leap from basic to enterprise plans, while freemium models acquire customers at the cost of ad inventory.

Savings Plans and reserved instances accustomed buyers to 30-70% discounts for commitment, obliging smaller hosts to emulate similar economics. The rise of spot-instance marketplaces-where providers auction unused capacity at discounts up to 90%-enables cost-conscious developers to run fault-tolerant workloads like batch processing, CI/CD pipelines, and machine-learning training on interruptible infrastructure that can be reclaimed with 2-minute notice.

Geography Analysis

North America held 38.63% of 2025 revenue, supported by dense hyperscale data-center clusters and early enterprise cloud adoption. Growth is moderating as the region approaches saturation, yet sovereign-cloud variants and AI-specific GPU farms sustain investment. outh America's hosting demand concentrates in Brazil and Argentina, where inflation volatility and currency devaluation force providers to denominate contracts in U.S. dollars and implement dynamic pricing that adjusts monthly based on exchange-rate fluctuations.

Asia-Pacific is projected to expand at a 10.93% CAGR, underpinned by the proliferation of digital payments in India, where UPI volumes crossed 100 billion transactions in 2024. Indonesian and Vietnamese fintechs deploy low-latency nodes in Jakarta and Ho Chi Minh City to comply with national regulations. Edge expansions by providers such as Telehouse added 15 data centers in 2024, cutting round-trip latency from 180 milliseconds to under 50 milliseconds in key metros.

Europe balances GDPR nuances with the need for scale. Regional companies such as OVHcloud and Hetzner promote in-region data storage, while AWS responded in 2024 with an isolated European Sovereign Cloud. Middle East and Africa represent nascent markets where mobile-first internet adoption-smartphone penetration exceeds 80% in UAE and Saudi Arabia-drives demand for hosting optimized for cellular networks with high latency and intermittent connectivity.

Competitive Landscape

The top three hyperscalers-AWS, Microsoft Azure and Google Cloud-capture a considerable share of public-cloud infrastructure spending, yet the broader Web Hosting market remains moderately fragmented. Hyperscalers leverage custom silicon like AWS Graviton3, which delivers 25% better performance per watt, to lock in clients through price-performance advantages. Specialists carve out niches in WordPress, game servers and HIPAA-compliant healthcare hosting.

Sovereign-cloud offerings satisfy data-location mandates, AWS launched its European Sovereign Cloud in 2024 while Alibaba Cloud opened a third Saudi Arabia region the same year. Edge-AI hosts such as CoreWeave capitalize on GPU scarcity by pre-booking H100 allocations via agreements with Nvidia and Google Cloud. Carbon-neutral providers like Kinsta display verified badges that resonate with procurement teams evaluating Scope 3 emissions.

Developer-first platforms Vercel and Netlify redefine hosting as a Git-based workflow. They abstract servers, load balancers and SSL, letting engineers push code and scale globally without infrastructure tuning. Observability, cost dashboards and Terraform integrations have become deciding factors as uptime converges across vendors in the Web Hosting market.

Web Hosting Industry Leaders

GoDaddy Inc.

Amazon Web Services, Inc.

Newfold Digital, Inc.

Google LLC

Alibaba Cloud Computing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Server5.click announced the forthcoming launch of a free hosting platform following a beta that began on January 1 2025.

- February 2025: France and the UAE confirmed a USD 50 billion investment in a 1 GW AI-focused data center in France, one of the largest cross-border hosting projects.

- January 2025: World Host Group completed the acquisition of A2 Hosting, the firm’s largest deal to date.

- January 2025: Microsoft Azure committed USD 3 billion to new data-center regions in Jakarta, Bangkok and Manila, enabling compliance with Indonesian data-localization rules and cutting latency for 700 million users in Southeast Asia.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the web hosting market as every paid service that stores website files on always-on servers, routes traffic to those files, and supplies ancillary uptime, security, and bandwidth support, whether the infrastructure is shared, virtual, dedicated, colocated, or cloud based.

Scope exclusion: Stand-alone domain registration, pure content-delivery networks, and app-platform hosting that never exposes the file system are outside this count.

Segmentation Overview

- By Hosting Type

- Shared Hosting

- Virtual Private Server (VPS) Hosting

- Dedicated Hosting

- Cloud Hosting

- Colocation Hosting

- Managed WordPress Hosting

- Reseller Hosting

- Other Hosting Types

- By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid/Multi-Cloud

- By End-user Vertical

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- Individual Bloggers/Creators

- Software Developers and SaaS Start-ups

- By Application

- Public Websites

- E-commerce Stores

- Web Applications

- Mobile Applications and APIs

- SaaS/PaaS Platforms

- Other Applications

- By Pricing Model

- Subscription (Fixed-Term)

- Metered/Pay-as-you-go

- Tiered (Usage-Bracket)

- Freemium and Ad-Supported

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple interviews with data-center operators, independent web developers, SaaS start-ups, and cloud-network engineers across North America, Europe, and Asia-Pacific helped validate utilization, churn, and hybrid-cloud adoption rates, which we then reconciled with desk findings to plug data gaps and stress-test sensitivities.

Desk Research

We began with granular traffic and connectivity indicators from sources such as ITU, Internet World Stats, and W3Techs, then pulled server shipment trends from IDC public notes and customs manifests. Regulatory references from ICANN, the U.S. Federal Communications Commission, and the European NIS 2 directive clarified compliance cost curves. Market share hints were cross-checked in company 10-Ks, D&B Hoovers extracts, and Dow Jones Factiva news feeds to size leading provider revenue pools. Hosting tariff benchmarks, average transfer volumes, and SME digitization rates from OECD statistics, APNIC routing tables, and UN Comtrade trade codes informed regional ASP and demand differentials. This list is illustrative; many other open databases and journals were reviewed to verify and fine-tune assumptions.

Market-Sizing & Forecasting

A top-down build used internet-active domain counts, average multipage payload size, and regional penetration of paid hosting to approximate demand pools, followed by selective bottom-up supplier revenue roll-ups to align totals. Key variables include SME website formation rates, data-center rack pricing, multi-cloud migration share, edge-node density, and median bandwidth per site. A multivariate regression blended with scenario analysis projects these drivers to 2030; anomalies trigger manual review before figures are frozen.

Data Validation & Update Cycle

Mordor analysts run variance checks against fresh domain-registration, bandwidth-pricing, and provider-earnings data each quarter, then refresh the model annually or sooner if a material event occurs, ensuring clients always receive an up-to-date baseline.

Why Mordor's Web Hosting Baseline Earns Industry Confidence

Published estimates often diverge because firms differ on which hosting types count, how aggressively future ASP erosion is modeled, and how frequently models are refreshed.

Key gap drivers include narrower scopes that drop cloud add-ons, aggressive straight-line growth assumptions for emerging regions, or currency conversions locked at historic rates, whereas our analysts revisit exchange rates and hybrid-cloud share every cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 194.20 B (2025) | Mordor Intelligence | - |

| USD 149.30 B (2025) | Global Consultancy A | Excludes colocation and managed WordPress; applies uniform global ASP |

| USD 124.39 B (2024) | Regional Consultancy B | Uses earlier base year and linear SME counts; no bottom-up cross-check |

In sum, the disciplined scope selection, dual-track (top-down and bottom-up) model, and near-real-time validations mean Mordor Intelligence delivers a balanced, transparent baseline executives can rely on for planning and investment decisions.

Key Questions Answered in the Report

How big is the Web Hosting market in 2026?

The Web Hosting market size is forecast to reach USD 182.28 billion in 2026, up from USD 180.35 billion in 2025.

What is the expected growth rate for Web Hosting between 2026 and 2031?

The market is projected to grow at a 10.49% CAGR during the 2026-2031 period.

Which hosting type is growing fastest?

Cloud hosting is expanding at a 10.53% CAGR, the highest among hosting types through 2031.

Which region offers the strongest growth opportunity?

Asia-Pacific is forecast to post the fastest regional CAGR at 10.93% through 2031 due to digital payment and e-commerce adoption.

Why are hybrid and multi-cloud deployments gaining traction?

Data-sovereignty rules and workload optimization needs push enterprises to distribute applications across on-premise, sovereign and hyperscale clouds, lifting hybrid adoption at a 10.75% CAGR.

What pricing model is rising in popularity?

Metered pay-as-you-go plans are gaining share with a projected 10.64% CAGR, reflecting demand for cost transparency.

Page last updated on: