Uveal Melanoma Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

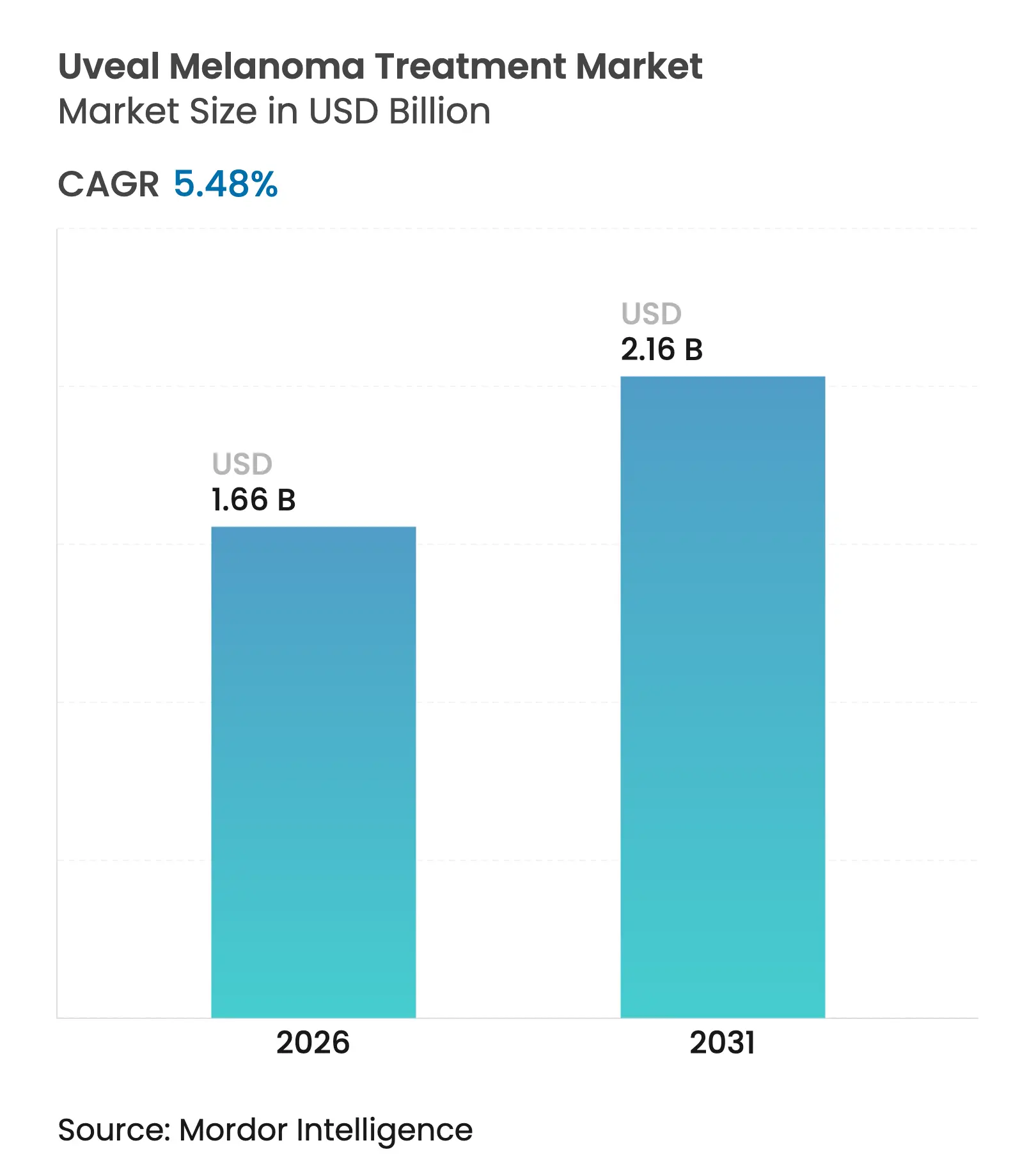

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 5.48 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Uveal Melanoma Treatment Market Analysis by Mordor Intelligence

The uveal melanoma treatment market size is expected to grow from USD 1.57 billion in 2025 to USD 1.66 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at 5.48% CAGR over 2026-2031. Sustained growth stems from the first-in-class survival benefit shown by tebentafusp, expanding orphan-drug incentives, and rapid improvements in gene-based and cell-based modalities. AI-supported screening raises detection of primary tumors at a treatable stage, while precision companion diagnostics open new revenue streams through risk stratification and therapy monitoring. Breakthrough designations for darovasertib and other kinase inhibitors shorten development timelines, and novel ocular delivery platforms reduce systemic toxicity, enhancing product differentiation. Private capital continues to flow into rare oncology, balancing the high cost of individualized care with promising long-term returns.

Key Report Takeaways

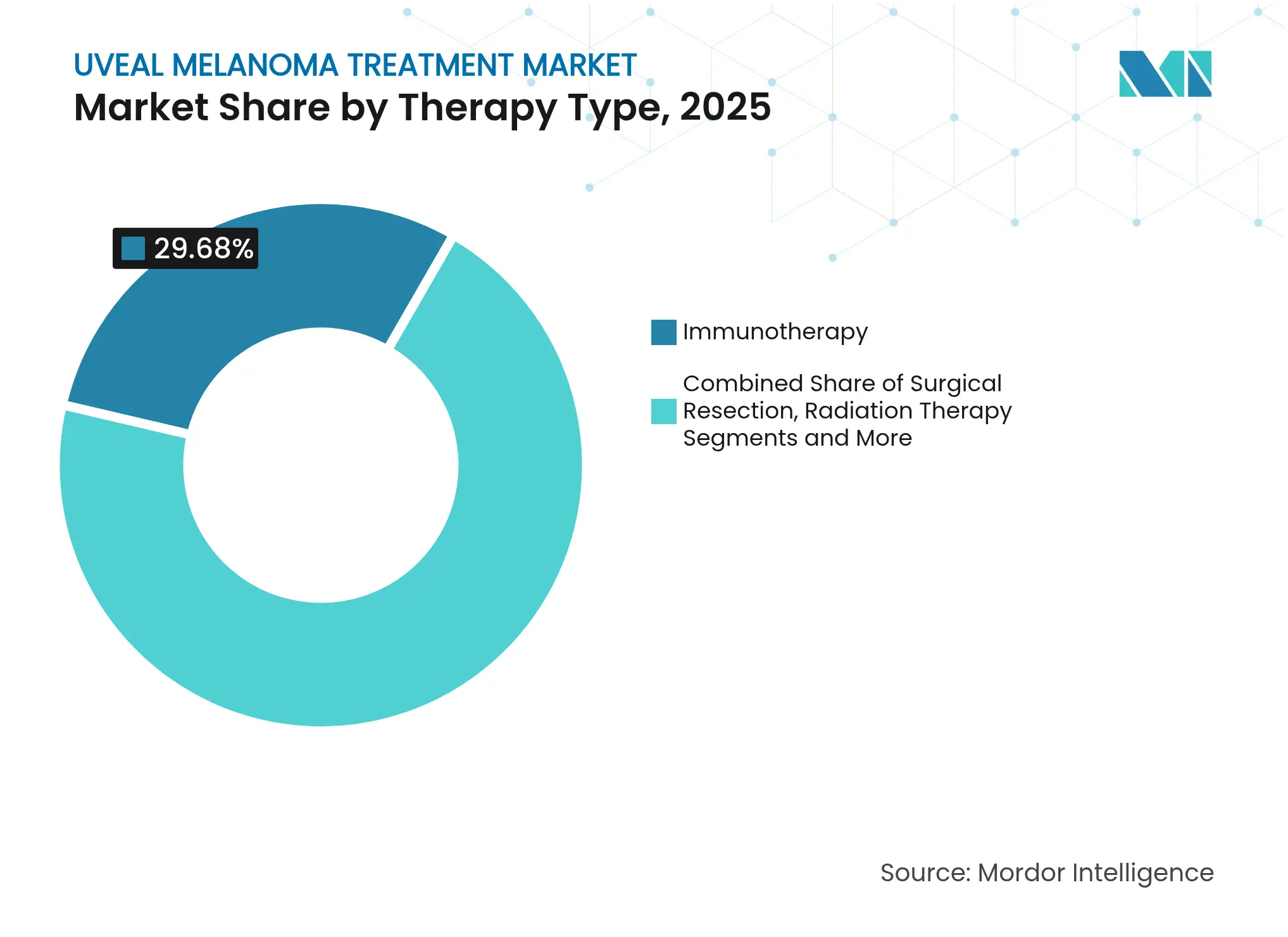

- By therapy type, immunotherapy led with 29.68% revenue share in 2025, while gene therapy is projected to expand at a 6.41% CAGR to 2031.

- By drug class, immune checkpoint inhibitors held 35.12% of the uveal melanoma treatment market share in 2025; protein kinase inhibitors record the highest projected CAGR at 5.52% through 2031.

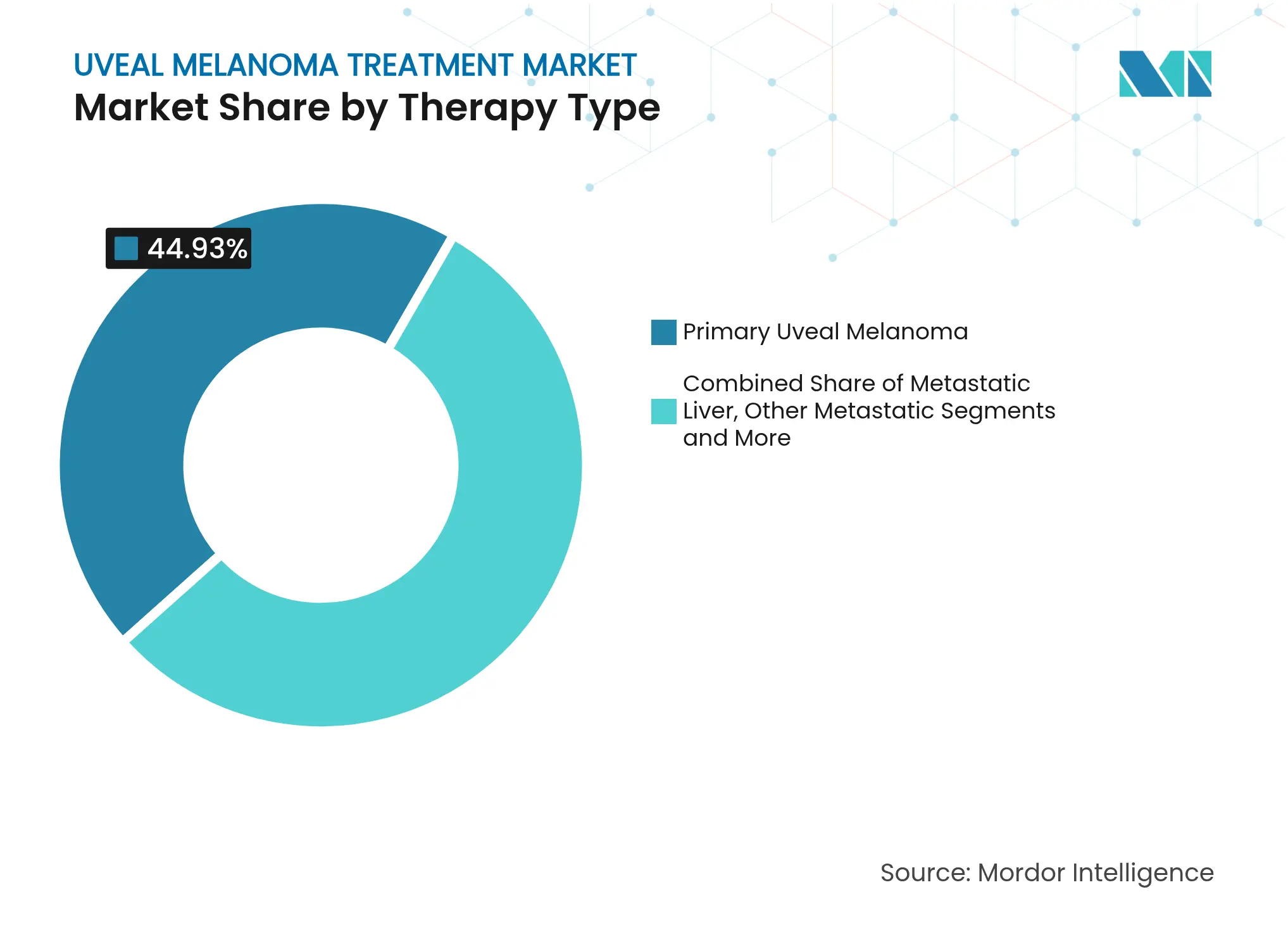

- By disease stage, primary tumors accounted for 44.93% share of the uveal melanoma treatment market size in 2025, whereas metastatic liver disease is advancing at a 4.97% CAGR to 2031.

- By end user, hospitals commanded 31.05% of the uveal melanoma treatment market share in 2025, and academic & research institutes show the fastest growth at 5.19% CAGR.

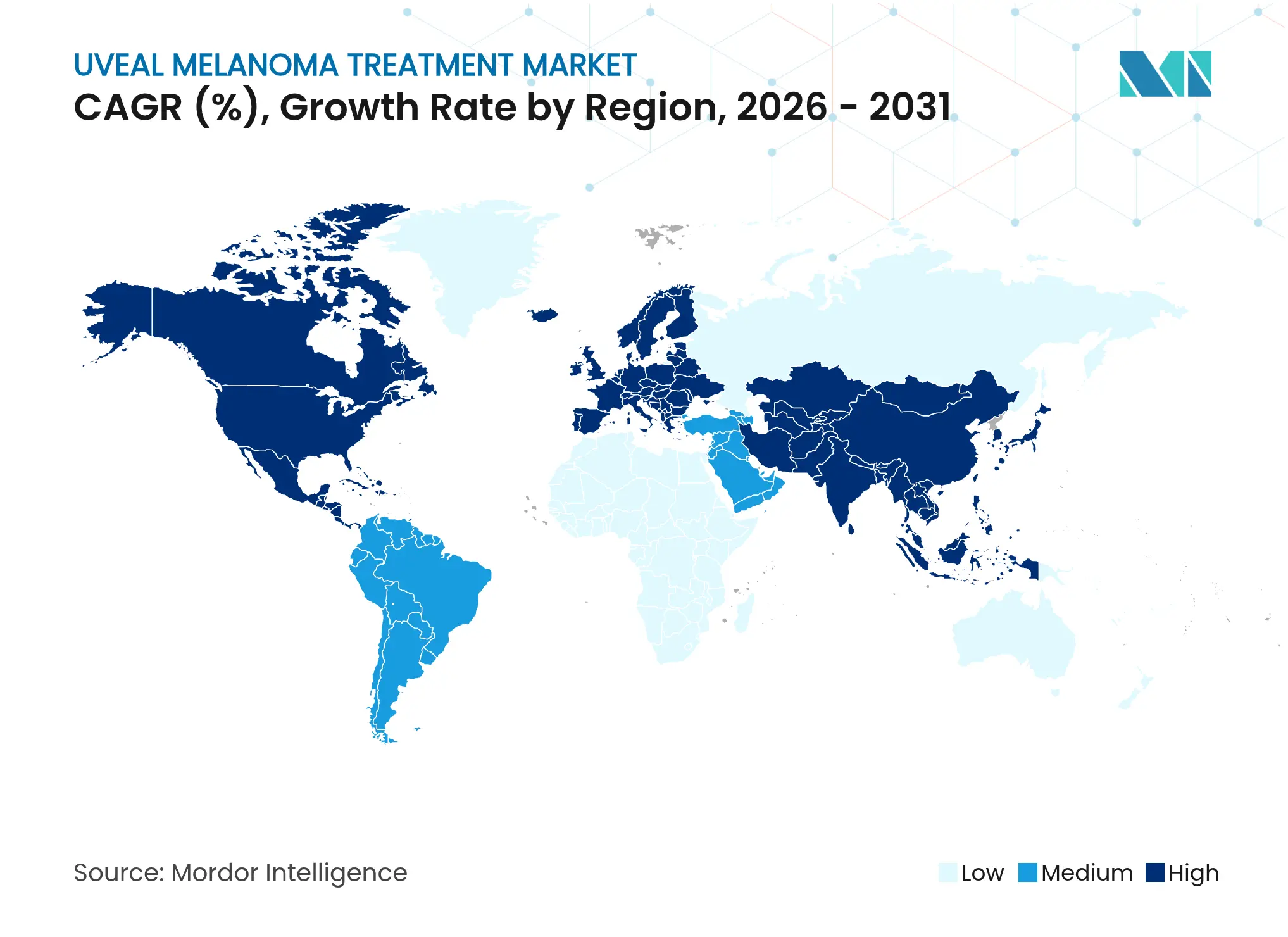

- By geography, North America led with 29.05% revenue share in 2025; Asia Pacific is forecast to grow at 6.18% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Uveal Melanoma Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Incidence of Uveal Melanoma Rising Incidence of Uveal Melanoma | +1.20% | Global, with higher rates in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.20% | Geographic Relevance:Global, with higher rates in North America & Europe | Impact Timeline:Medium term (2-4 years) |

Adoption of Gene & Cellular Therapies Adoption of Gene & Cellular Therapies | +1.80% | North America & EU leading, APAC emerging | Long term (≥ 4 years) | |||

Advancements in Ocular Drug-Delivery Systems Advancements in Ocular Drug-Delivery Systems | +1.10% | Global, with innovation centers in US & Europe | Medium term (2-4 years) | |||

Increased Use of AI-based Early Detection Tools Increased Use of AI-based Early Detection Tools | +0.90% | APAC core, spill-over to North America & EU | Short term (≤ 2 years) | |||

Favorable Orphan-Drug & Fast-Track Approvals Favorable Orphan-Drug & Fast-Track Approvals | +1.30% | Global, with US FDA leading regulatory pathways | Short term (≤ 2 years) | |||

Growing Private Funding for Rare Oncology Growing Private Funding for Rare Oncology | +0.80% | North America & EU primary, selective APAC markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence of Uveal Melanoma

Incidence rates stand at 5.74 per million in North America and 7.30 per million in Europe, compared with 0.2-0.6 per million across major Asian populations.[1]A.M. Stubbings, “Global Patterns of Uveal Melanoma Incidence,” Asian Pacific Journal of Cancer Prevention, apjcp.org Improved surveillance programs and genetic counseling widen the addressable patient pool, while younger presentation ages in Asia suggest distinct genetic pathways. Expanded screening combined with AI-driven fundus analysis supports earlier intervention, shifting case mix toward treatable primary disease and reinforcing demand within the uveal melanoma treatment market.

Adoption of Gene & Cellular Therapies

The February 2024 approval of lifileucel established regulatory precedent for autologous T-cell approaches.[2]Food and Drug Administration, “FDA Approves Lifileucel for Unresectable or Metastatic Melanoma,” fda.gov Suprachoroidal delivery and virus-like drug conjugates now underpin pivotal trials such as bel-sar, which achieved 80% local tumor control with vision preservation. Longer-term, non-viral nano-carriers promise safer repeat dosing, positioning advanced modalities to outpace legacy systemic regimens across the uveal melanoma treatment market.

Advancements in Ocular Drug-Delivery Systems

Implantable reservoirs like Susvimo confirm commercial acceptance of sustained posterior-segment delivery. Biodegradable devices and polymer nanoparticles further reduce surgical burden and permit controlled release of kinase inhibitors or immune modulators. Focused delivery lessens systemic exposure, improving tolerability profiles that differentiate next-generation entrants in the uveal melanoma treatment market.

Increased Use of AI-Based Early Detection Tools

Deep-learning algorithms now distinguish malignant from benign choroidal lesions with 84.8% accuracy.[3]Guan-Bin Song, “Deep Learning for Choroidal Melanoma Detection,” Journal of Clinical Medicine, mdpi.com Multimodal imaging platforms integrate optical coherence tomography and ultrasound, making high-level screening accessible to community clinics and remote regions. Earlier diagnosis enlarges the candidate pool for eye-sparing interventions, boosting procedure volumes and downstream therapy uptake within the uveal melanoma treatment market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Cost of Personalized Therapies High Cost of Personalized Therapies | -1.50% | Global, with acute impact in emerging markets | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.50% | Geographic Relevance:Global, with acute impact in emerging markets | Impact Timeline:Long term (≥ 4 years) |

Limited Patient Pool for Large-Scale Trials Limited Patient Pool for Large-Scale Trials | -0.80% | Global, with concentration challenges in APAC | Medium term (2-4 years) | |||

Adverse Effects & Safety Concerns of Radiotherapy Adverse Effects & Safety Concerns of Radiotherapy | -0.60% | Global, with higher impact in regions with limited alternatives | Medium term (2-4 years) | |||

Competitive Threat from Imaging-Based Surveillance Competitive Threat from Imaging-Based Surveillance | -0.40% | North America & EU primarily, emerging in APAC | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Personalized Therapies

Tebentafusp therapy exceeds USD 400,000 annually, creating reimbursement friction even in mature insurance systems. Mandatory biomarker tests add USD 3,000-5,000 to upfront care. Access disparities emerge where specialized centers are sparse, intensifying reliance on tele-oncology. Sustained cost pressures may temper adoption despite demonstrated survival gains across the uveal melanoma treatment market.

Limited Patient Pool for Large-Scale Trials

The global incidence of nearly 7,000 cases per year constrains conventional Phase III designs. Tebentafusp secured approval on 378-patient data. Regulators are accepting adaptive studies and surrogate endpoints, yet HLA-A*02:01-positive requirements further restrict eligibility to roughly 44% of Caucasian cohorts. These limitations extend timelines and increase per-patient costs for sponsors operating in the uveal melanoma treatment market.

Segment Analysis

By Therapy Type: Immunotherapy Dominance Faces Gene-Therapy Disruption

Immunotherapy held 29.68% of 2025 revenue, reflecting tebentafusp’s landmark survival data. Regulatory acceptance of bispecific T-cell engagers keeps physician reliance high, though objective response rates remain modest. The uveal melanoma treatment market is pivoting to gene therapy as viral-vector refinement and local delivery achieve higher ocular concentrations with lower systemic load. Gene-based candidates show 6.41% CAGR through 2031 as Phase 3 programs mature. Traditional radiation and surgical approaches remain standard for localized tumors, yet combination regimens increasingly integrate adjuvant biologics.

Gene therapy’s momentum is supported by precision delivery platforms that cross the blood-retina barrier without extensive invasive procedures. Early trials demonstrate durable tumor control and vision preservation, signaling a competitive threat to existing immune regimens. Pipeline diversity expands as nano-carriers and non-viral vectors gain traction, further broadening modality choices and intensifying competition within the uveal melanoma treatment market.

Note: Segment shares of all individual segments available upon report purchase

By Drug Class: Checkpoint Inhibitors Lead Despite Efficacy Ceiling

Immune checkpoint inhibitors led with 35.12% of the uveal melanoma treatment market share in 2025 despite response rates below those seen in cutaneous disease. Physician familiarity and reimbursement precedents support ongoing use, and combination regimens aim to overcome intrinsic immune resistance. Protein kinase inhibitors post the fastest growth at 5.52% CAGR on the strength of darovasertib’s breakthrough status and promising ocular preservation outcomes.

Expanded research into novel checkpoints and intracellular targets widens the therapeutic arsenal. Dual-inhibition strategies combining CTLA-4 and PD-1 blockade show incremental survival benefits, underscoring unresolved need. As next-wave small molecules and oncolytic viruses progress, competition will broaden and potentially recalibrate leading drug-class positions in the uveal melanoma treatment market.

By Disease Stage: Primary Focus Shifts Toward Metastatic Innovation

Primary tumors made up 44.93% of the uveal melanoma treatment market size in 2025, a figure fortified by earlier diagnosis and refined eye-conserving surgery. Yet almost half of patients progress to liver metastasis within seven years, spurring breakthrough work in hepatic-directed therapies. Metastatic disease posts a 4.97% CAGR anchored by tebentafusp’s survival edge and percutaneous hepatic perfusion that nearly triples progression-free intervals.

Neoadjuvant kinase inhibition shows 82% tumor shrinkage with 61% eye preservation, implying a future shift toward systemic therapy before local resection. Liquid biopsy assays pick up circulating tumor DNA, informing adjuvant decisions post-therapy. Disease-stage dynamics thus guide changing resource allocation in the uveal melanoma treatment market, with upstream biomarker development gaining urgency.

Note: Segment shares of all individual segments available upon report purchase

By End User: Academic Centers Drive Research Innovation

Hospitals remained the largest care setting with 31.05% of the uveal melanoma treatment market share in 2025, integrating surgery, radiation, and systemic oncology under one roof. Academic & research institutes grow fastest at 5.19% CAGR, reflecting their role in early-phase trials and translational science. Ongoing clinical studies exceed 40 active protocols, positioning these centers as gatekeepers for cutting-edge options.

Tele-oncology and satellite clinics extend specialty expertise to underserved geographies, reducing travel burdens and broadening trial access. Companion diagnostic adoption rises in ophthalmology practices as gene-expression tests solidify risk stratification. These patterns collectively enhance data flow and concentrate innovation, reinforcing the academic ecosystem’s pivotal role within the uveal melanoma treatment market.

Geography Analysis

North America contributed 29.05% of the uveal melanoma treatment market size in 2025, benefiting from FDA leadership on orphan-drug incentives and a dense network of ocular oncology specialists. Reimbursement for high-value biomarker tests is gaining traction, though prior authorizations remain complex. Regional supply chains favor rapid patient access, and venture funds located in Boston and California provide a steady stream of capital to early-stage ventures.

Europe follows with comprehensive coverage under national health schemes and cross-border research through EURACAN. Extensive radiation expertise and well-established surgical protocols complement growing uptake of gene-expression profiling. Health-technology assessments lengthen launch timelines, yet secure long-term revenues once reimbursement is achieved, sustaining a significant proportion of global sales in the uveal melanoma treatment market.

Asia Pacific posts the highest growth at 6.18% CAGR. Lower baseline incidence is offset by rapid expansion of ophthalmology infrastructure, rising insurance penetration, and regulatory modernization exemplified by China’s NMPA acceptance of toripalimab. Japan contributes deep immunotherapy experience, while South Korea and Singapore invest heavily in AI-enhanced diagnostics. Increasing regional trials address ethnic genetic differences, aligning therapy development with local disease biology and reinforcing future demand across the uveal melanoma treatment market.

Competitive Landscape

Market Concentration

Competition centers on specialized biotechnology firms rather than diversified pharmaceutical conglomerates. Immunocore’s tebentafusp enjoys a first-mover advantage, while IDEAYA Biosciences advances the leading kinase-inhibition program with FDA breakthrough designation. Aura Biosciences pioneers virus-like drug conjugates through Phase 3 bel-sar and partners strategically for exclusive dye and delivery assets. Castle Biosciences integrates proprietary gene-expression tests, embedding diagnostics within therapeutic decision chains and capturing ancillary revenues.

Barriers to entry include scarce patient populations, complex trial recruitment, and specialized surgical techniques. Nonetheless, white-space opportunities in AI-guided imaging, sustained-release implants, and liquid biopsies invite new entrants. Collaborative alliances among drug developers, device firms, and academic centers remain the dominant path to market for emerging innovators in the uveal melanoma treatment market.

Continued consolidation is possible as larger oncology players seek rare-disease diversification, evidenced by ANI Pharmaceuticals’ acquisition of Alimera Sciences. Combined with rising private funding, these dynamics shape a moderate-concentration arena where breakthrough data can rapidly shift competitive standings across the uveal melanoma treatment market.

Uveal Melanoma Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The FDA endorsed IDEAYA Biosciences’ Phase 3 darovasertib neoadjuvant design for 520 patients focusing on eye preservation and vision outcomes.

- March 2025: The FDA granted breakthrough therapy designation to darovasertib monotherapy after 82% ocular tumor shrinkage and 61% eye preservation in Phase 2.

- February 2025: Genentech gained FDA approval for Susvimo continuous delivery in diabetic macular edema, validating sustained ocular implant technology applicable to uveal melanoma.

- January 2025: Castle Biosciences presented DecisionDx-Melanoma data linking the assay to 32% mortality risk reduction across 13,500 patients and introduced a 16-protein liquid-biopsy test for small uveal tumors.

Table of Contents for Uveal Melanoma Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence of Uveal Melanoma

- 4.2.2Adoption of Gene & Cellular Therapies

- 4.2.3Advancements in Ocular Drug-Delivery Systems

- 4.2.4Increased Use of AI-based Early Detection Tools

- 4.2.5Favorable Orphan-Drug & Fast-Track Approvals

- 4.2.6Growing Private Funding for Rare Oncology

- 4.3Market Restraints

- 4.3.1High Cost of Personalized Therapies

- 4.3.2Limited Patient Pool for Large-Scale Trials

- 4.3.3Adverse Effects & Safety Concerns of Radiotherapy

- 4.3.4Competitive Threat from Imaging-Based Surveillance

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Clinical Trial Landscape

5. Market Size & Growth Forecasts (Value)

- 5.1By Therapy Type

- 5.1.1Surgical Resection Techniques

- 5.1.2Radiation Therapy

- 5.1.3Transpupillary Thermotherapy

- 5.1.4Targeted Therapy

- 5.1.5Immunotherapy

- 5.1.6Gene Therapy

- 5.1.7Other Therapy Types

- 5.2By Drug Class

- 5.2.1Protein Kinase Inhibitors

- 5.2.2Immune Checkpoint Inhibitors

- 5.2.3Antimetabolites

- 5.2.4Oncolytic Viruses

- 5.2.5Others

- 5.3By Disease Stage

- 5.3.1Primary Uveal Melanoma

- 5.3.2Metastatic Uveal Melanoma (Liver)

- 5.3.3Other Metastatic Sites

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Ophthalmology Centers

- 5.4.3Academic & Research Institutes

- 5.4.4Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Immunocore Holdings plc

- 6.3.2Eli Lilly and Company

- 6.3.3IDEAYA Biosciences Inc.

- 6.3.4Aura Biosciences

- 6.3.5Novartis AG

- 6.3.6Bayer AG

- 6.3.7AstraZeneca plc

- 6.3.8F. Hoffmann-La Roche AG

- 6.3.9Merck & Co., Inc.

- 6.3.10Bristol-Myers Squibb

- 6.3.11Daiichi Sankyo Co., Ltd.

- 6.3.12iOnctura SA

- 6.3.13Regeneron Pharmaceuticals Inc.

- 6.3.14Pfizer Inc.

- 6.3.15Syndax Pharmaceuticals Inc.

- 6.3.16Incyte Corporation

- 6.3.17Genmab A/S

- 6.3.18Checkmate Pharmaceuticals

- 6.3.19Exicure Inc.

- 6.3.20Castle Biosciences Inc.

- 6.3.21Provectus Biopharmaceuticals Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Uveal Melanoma Treatment Market Report Scope

Uveal melanoma is a rare and aggressive form of eye cancer that originates in the uveal tract of the eye, which consists of three parts: the iris, ciliary body, and choroid. This cancer primarily affects adults and is the most common primary intraocular malignancy in this demographic. Despite its rarity, uveal melanoma poses significant clinical challenges due to its potential for metastasis and the critical functions of the affected ocular structures.

The uveal melanoma treatment market is segmented into therapy type, end-user, and geography. By therapy type, the market is segmented into surgical resection techniques, radiation therapy, transpupillary thermotherapy, targeted therapy, and other therapy types. By end-user, the market is segmented into ophthalmic centers, hospitals, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).