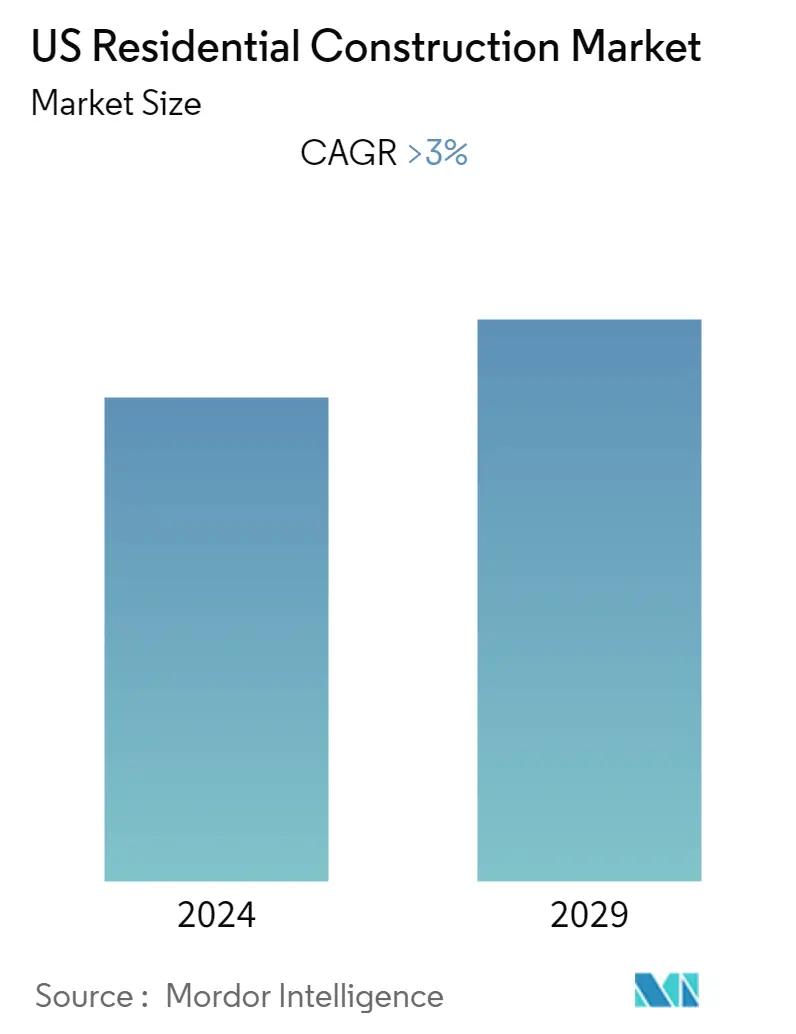

Market Size of US Residential Construction Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR | > 3.00 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

US Residential Construction Market Analysis

The size of the United States Residential Construction Market is around USD 590 billion in the current year and is anticipated to register a CAGR of over 3% during the forecast period. The United States residential construction market is driven by the Affordable Housing trend in the country.

- In 2020, the federal funds rate target was lowered to near zero in response to fears of an economic slowdown from the spread of COVID-19 (coronavirus). Afterward, mortgage rates reached record lows. This, coupled with a low housing supply, fueled residential construction in early 2020. However, the fallout stemming from the coronavirus pandemic was worse than expected, leading to the temporary curtailment or complete shutdown of large bands of the economy. This weighed on residential investment in Q2-2020.

- While other economic indicators embarked on a quick but incomplete rebound, the residential market rebounded exceptionally rapidly, with the value of residential construction investment surpassing pre-pandemic levels before the end of the year 2020. Residential investment was being driven by a low housing stock and historically low mortgage rates. Growth in 2021 accelerated as the release of pent-up demand, alongside increased vaccinations among the population, led to increased residential construction activity. Labor market improvement has also helped support residential demand. Nonetheless, rising inflation in 2022 has pushed the Federal Reserve to raise interest rates to curtail spending amid recessionary fears. As a result, residential investments have slowed considerably with declines expected in 2022 and 2023.

- A divide between construction sectors in the United States has become visible as residential contractors brace for recession - but commercial and industrial buildings continue to boom. Rising interest rates have already driven the single-family homebuilding market into recession, but brisk non-residential activity continues. As recent trends indicate, costs of materials, fulfillment, labor, and land have surged. This had a direct impact on the residential construction industry. Additionally, the negative outlook in the housing market may be creating an even greater perception of discrepancy between the two areas of construction, with higher mortgage rates weighing heavily on demand - or lack thereof - for new housing. Newly released 'Construction Spending' data shows the industry continues to struggle in the current economic environment.

- The data for September 2022 shows that, in seasonally adjusted nominal terms, the industry grew 0.2% from August 2022 and 10.9% compared to the previous year. Overall construction spending growth has remained stable over 2022, mostly maintaining double-digit growth throughout the year. However, as this data is in nominal terms, the expansion mainly reflects the jump in prices across the industry. The balance between residential and non-residential sector growth has also been shifting. The residential sector has shown persistent deceleration in month-on-month (MoM) growth towards the end of 2022, and year-on-year (YoY) growth has followed a downward trend from May 2021. Meanwhile, non-residential construction growth has accelerated, in February 2022, YoY growth turned positive and stood at 9.2% as of September 2022.