Market Trends of US Homeowner's Insurance Industry

This section covers the major market trends shaping the US Homeowner's Insurance Market according to our research experts:

InsurTech in the US Homeowner's Insurance

A sustained economic growth coupled with higher interest rate and bigger investment income, helped the US insurance industry to top the charts with an impressive growth. Even though the traditional insurance companies are doing good, to with-stand newer business models, they are coming forward to partner with Insurtech companies. In fact this partnership helps the traditional players to better cater as per the customer demands without investing much on R&D for self-made technology. InsurTech companies manage many niche segments of the market, ranging from operating as Distributors/Aggregators, API developers, HealthTech, Online First Insurance providers and IoT, amongst others.

Among all, Property/casualty sector has been doing well with 12.7% increase in the first half of 2018. The Online first insurance: As the name suggests these companies offer insurance products completely online and connect various distribution channels. For E.g., Lemonade is an online first P2P insurance platform that offers home insurance in New York, California and Illinois. Technology used is AI and Behavioral economics. Another example would be Next Insurance, which is also an online insurance platform that targets SMEs, entrepreneurs who are looking for insurance to cover their business. Hippo, an online platform provides home insurance products.

The Internet of Things: These companies are using technology to reduce the premium amounts for the insurance taken and creating a digital disruption. For E.g., American Well, a web and mobile based platform founded in 2006 and then there is a start-up named Metromile, which turns an ordinary car into a smart car with a plug-in device that calculates the miles travelled to find out the insurance to be paid.

Natural Catastrophes affect Spending on Homeowner’s Insurance

Homeowners insurance is a package policy, providing both property and personal liability insurance. The typical policy covers a house, garage and other structures on the property-as well as personal property inside the house-against a wide variety of perils, such as fire, windstorm, vandalism and accidental water damage. The typical homeowner's policy includes theft coverage on personal property anywhere in the world and liability coverage for accidental harm caused to others. It also reimburses the policyholder for the additional cost of living elsewhere while a house is being repaired or rebuilt after a disaster.

Earthquake damage and flood damage caused by external flooding are not covered by standard homeowners' policies, however special policies can be purchased separately. Flood coverage is provided by the federal governments National Flood Insurance Program and some private insurers.

Storm surge is ocean water that is pushed ahead of a storm and can cause severe damage. States along the U.S. Gulf of Mexico and Atlantic Basin are potentially vulnerable to storm surge damage. In 2019, there were 7.3 million coastal homes along the Gulf and Atlantic Coasts, worth almost $1.8 trillion, at risk for storm surge damage. Along the Gulf Coast, 3.1 million homes are at risk from storm surge, and another 4.1 million homes along the Atlantic Coast are at risk. The reconstruction cost value of homes at risk for storm surge damage is $668 billion along the Gulf of Mexico in the United States and $1.1 trillion along the highly populated Atlantic Coast. The reconstruction cost is based on the 100 percent destruction of the residential structure, using a combined cost of construction materials, equipment and labor costs by geographic location.

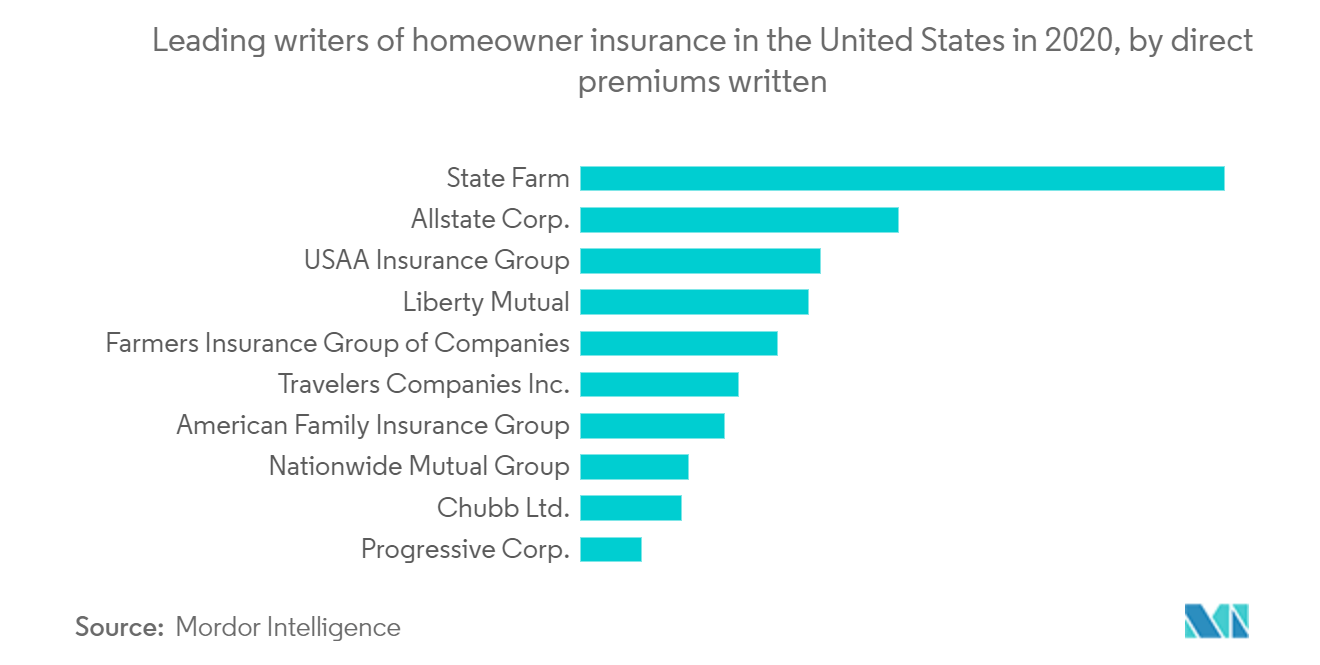

The State Farm mutual automobile insurance from Bloomington, Illinois, was the leading homeowners insurance writer in the United States in 2020. With almost 20 billion U.S. dollars in direct premiums written, this insurance company toppled the second homeowner insurer (Allstate Corp.) in the U.S. by around 10 billion dollars in that year.