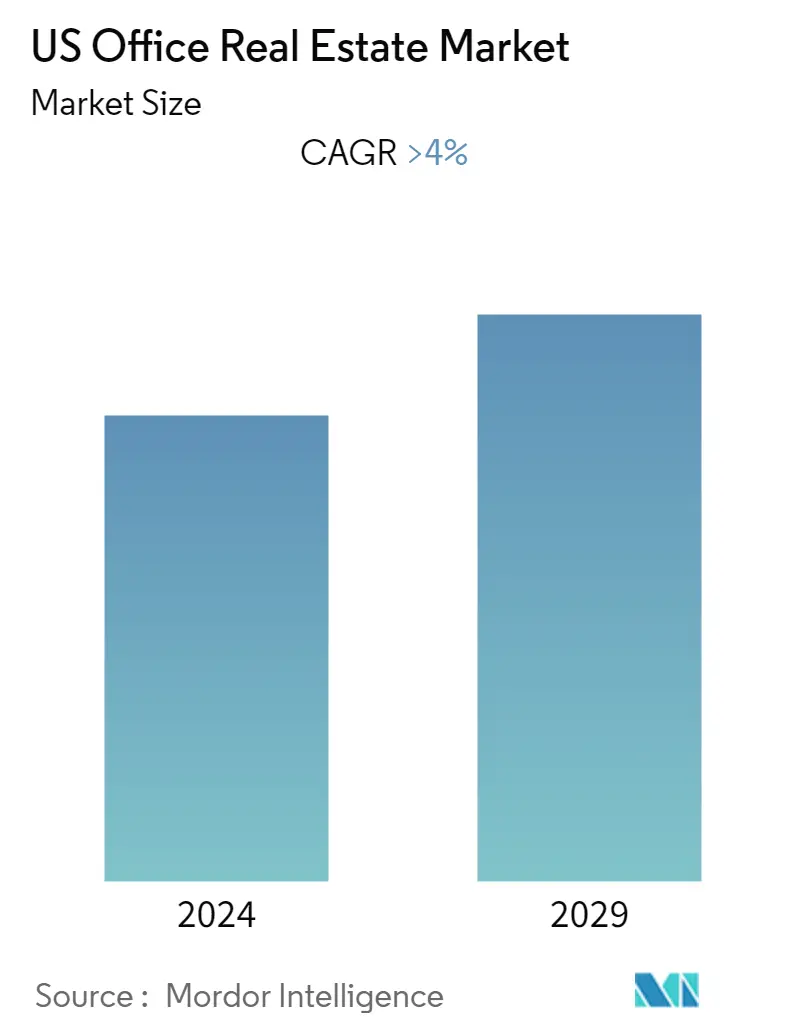

Market Size of US Office Real Estate Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | > 4.00 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

US Office Real Estate Market Analysis

- The US office real estate market is poised to register a CAGR of greater than 4% during the forecast period.

- The COVID-19 pandemic hurt the US office sector a lot, and it may take a while for it to get better.The third quarter of 2021 was promising for the US office market. The vacancy rate was stabilizing, sublease space was decreasing, and net absorption was positive for the first time in Q3 2021 since Q1 2020.

- The property markets also felt the impact of the pandemic. Enterprises and frontline workers had to overcome many obstacles to stay in business. Almost every company in the property industry was compelled to make drastic changes, especially in the retail sector. To accommodate rising consumer demand and overcome acute shortages, retailers swiftly built up their home delivery and curbside pickup services while restructuring their supply chains. Many people who work from home have had to adjust their living environments on the fly. The emerging trend of the year is "flexibility."

- Vacancy rates rose throughout the American office real estate market during the coronavirus outbreak. The quarterly vacancy rate before 2020 was approximately 12 percent, but as the epidemic spread, it increased to more than 15 percent. Around 15.4 percent of office space nationwide was unoccupied in the third quarter of 2022. Businesses are wary of expanding or renewing leases because a sizable portion of the workforce now works from home or uses a hybrid working paradigm.

- In the third quarter of 2022, the fundamentals of the US office market remained negative. The third quarter of 2022 saw minus 4.4 million square feet (msf) of net absorption, bringing the year's total to negative 16.2 msf. With a quarterly net absorption of -2.2 msf and -2.0 msf, respectively, both major gateway and secondary markets lost the same number of tenants. Just 3.8% of the nation's total inventory is held in tertiary markets, which saw negative net absorption of 0.1 msf. Increasing vacancy is a sign of low demand, which is shown by consistently low net absorption, and high supply, which is shown by a lot of new construction in the works.