Market Trends of US FTL Freight Brokerage Industry

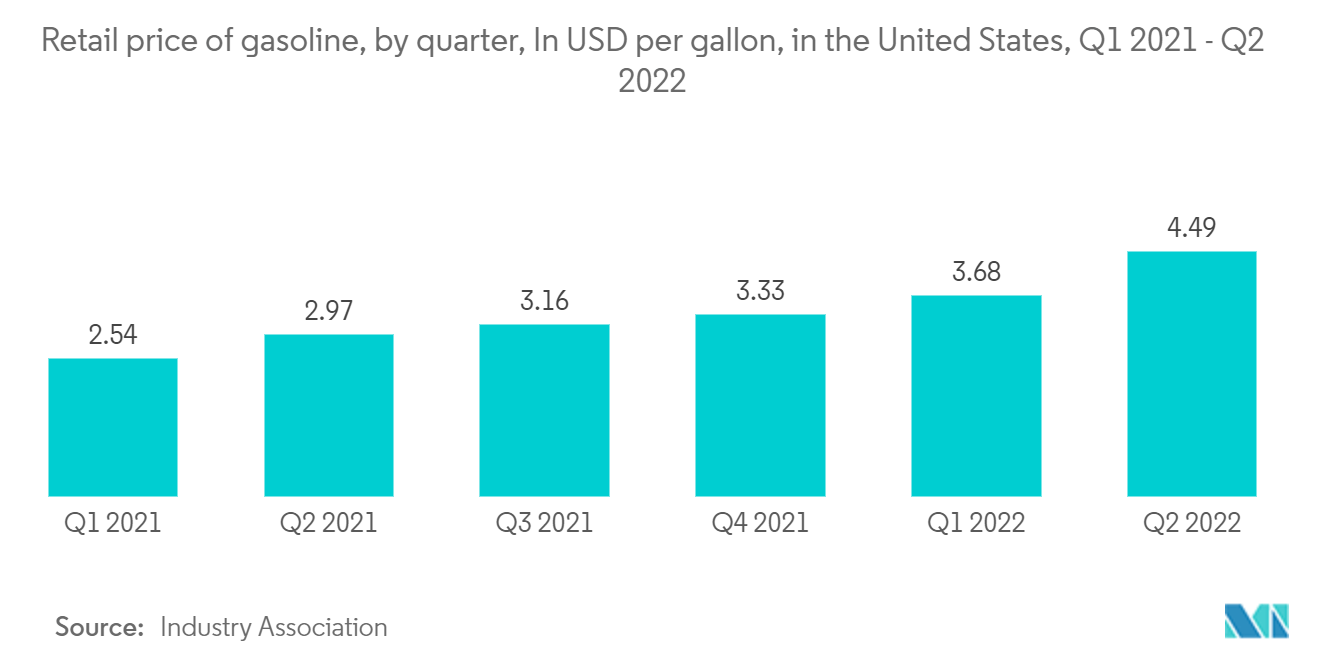

Fluctuating Fuel prices Hampering the Growth of the Market

Carriers (logistics companies) may charge higher rates if market conditions warrant or cover higher operating costs. As a result, if brokerage firms cannot increase pricing for their customers, revenues, and income from operations may decrease. The increased market demand for FTL services and pending regulatory changes may reduce available capacity and raise carrier pricing. Fuel prices can be volatile and challenging to forecast. Over the last five years, fuel prices have fluctuated dramatically. Clients anticipate that lower prices will pass them on to fuel savings. If carriers do not lower their prices to reflect decreases in fuel costs, shipment volume may suffer as customers seek alternative shipping options.

This volume decrease would harm the brokerage companies' gross profits and operating income. In the event of rising fuel prices, carriers can be expected to charge higher fees to cover higher operating expenses. The gross profit of brokerage firms and income from operations may decrease if they cannot continue to pass through to their clients the total amount of these increased costs. Higher fuel costs could also cause material shifts in the percentage of revenue by transportation mode, as clients may elect to utilize alternative transportation modes. Any material shifts to transportation modes concerning which brokerage firms realize lower gross profit margins could impair operating results. The Ukraine-Russia war also caused a spike in fuel prices as Russia is the third-largest producer of crude oil.

Construction Sector is the Fastest-growng End-user Segment

Despite near-term challenges in certain construction sectors, the medium to long-term growth story in the United States remains intact. The construction industry in the United States is expected to grow steadily over the next four quarters. In the United States, several projects are working their way through the planning phase, whereas others have finally resumed after a year of global pandemic-related delays. Despite the challenges associated with the global supply chain, such as rising raw material prices, shortage of building materials, and lack of skilled labor, the residential construction sector will continue its stable growth over the four to eight quarters.

The residential construction sector largely remains supported by low lending rates, strong demand for bigger homes, and low housing inventory in the United States. Over the next few quarters, the healthcare and education sectors will receive more attention. In November 2021, the US Congress passed a USD 1 trillion infrastructure spending bill.

The infrastructure legislation proposes USD 550 billion in new federal expenditure over the next eight years in the United States for the upgrade of roads, bridges, and highways and modernizing the city transit systems and passenger rail networks. While the new infrastructure spending bill falls short of the original USD 2.3 trillion proposals, the USD 1 trillion spending on various United States infrastructure sectors will keep supporting the growth of the construction industry over the next four to eight quarters in the country.