Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

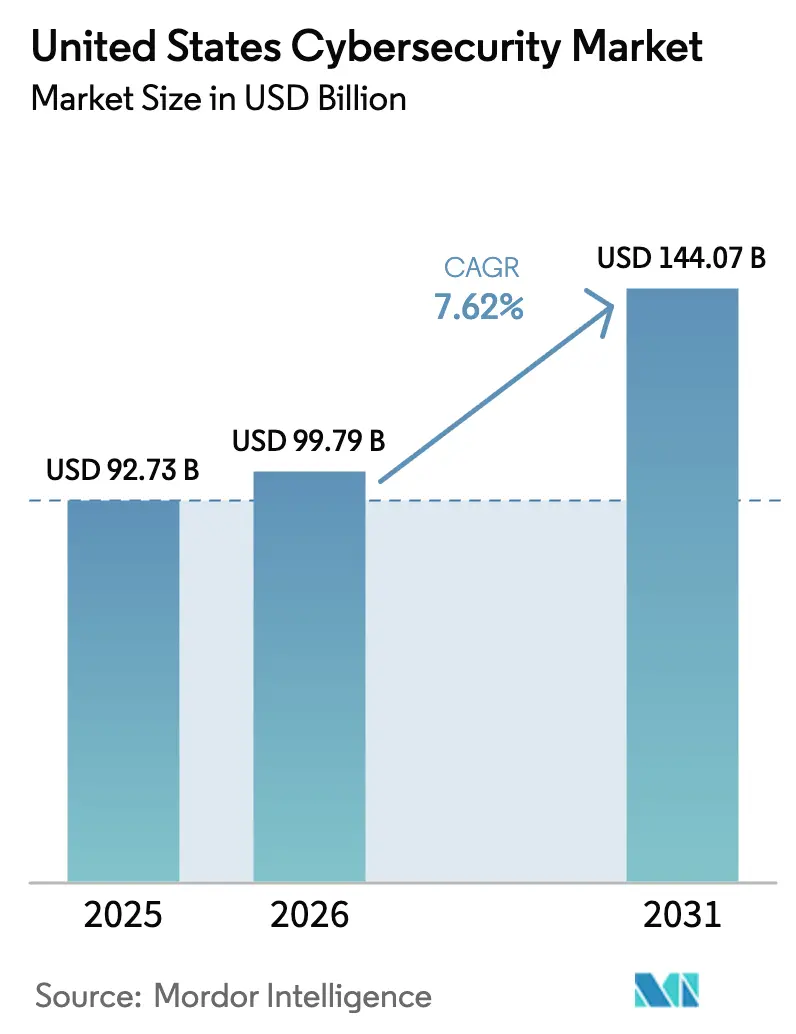

| Base Year Market Size (2025) | USD 92.73 Billion |

| Market Size (2026) | USD 99.79 Billion |

| Market Size (2031) | USD 144.07 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

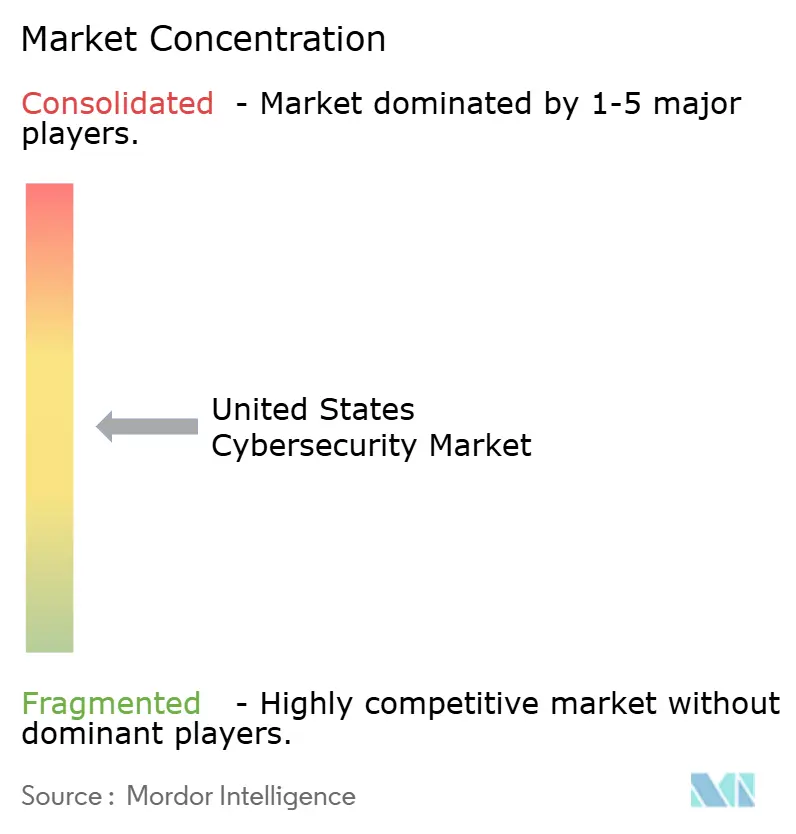

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cybersecurity Market Analysis by Mordor Intelligence

The United States cybersecurity market size was valued at USD 92.73 billion in 2025 and estimated to grow from USD 99.79 billion in 2026 to reach USD 144.07 billion by 2031, at a CAGR of 7.62% during the forecast period (2026-2031). Rising ransomware-as-a-service activity, federally mandated zero-trust architecture, and a burgeoning patchwork of state privacy statutes are intensifying demand for unified security platforms. Service providers are attracting mid-market enterprises that lack in-house resources, while cloud-native adoption continues to outpace on-premises refresh cycles. Heavily regulated sectors such as banking and healthcare are scaling identity governance, data encryption, and managed detection to comply with updated federal guidance. Vendor consolidation is underway as buyers weigh total cost of ownership against best-of-breed depth, paving the way for platform leaders to capture incremental spending.

Key Report Takeaways

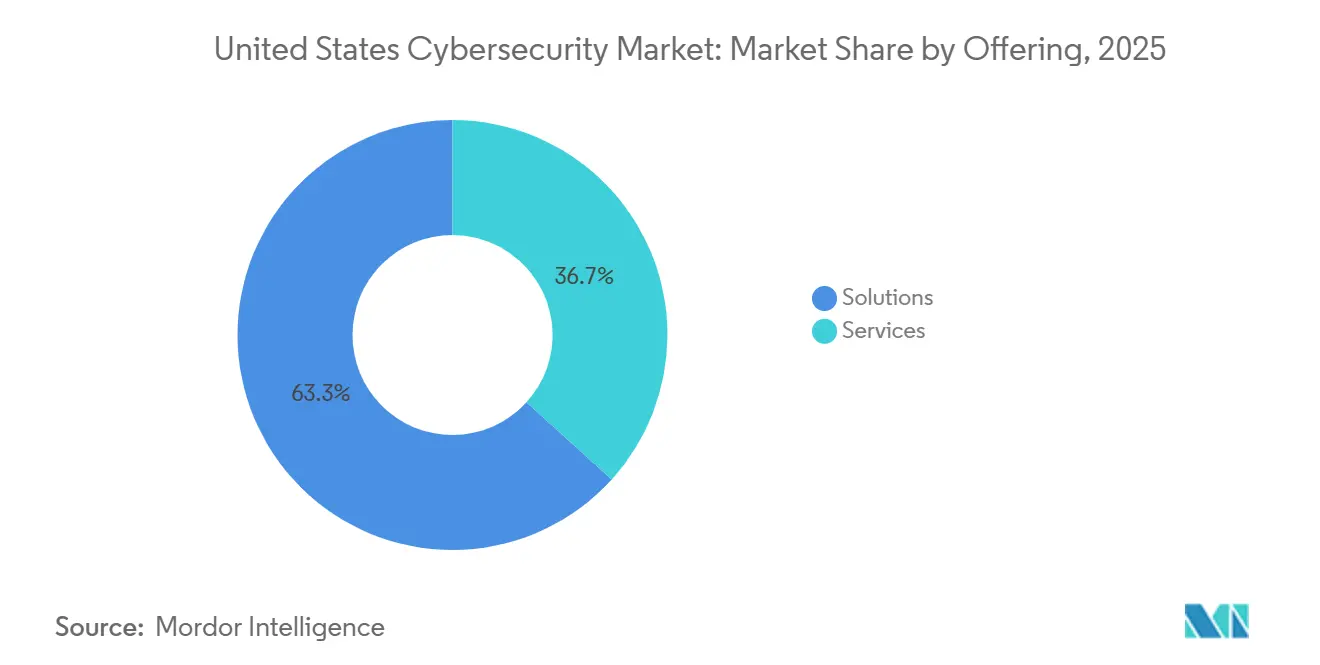

- By offering, solutions led with 63.28% of the United States cybersecurity market share in 2025; the services segment is forecast to expand at an 8.13% CAGR through 2031.

- By deployment mode, cloud accounted for 63.12% of 2025 spending and is projected to grow at 8.64% as hybrid strategies recede.

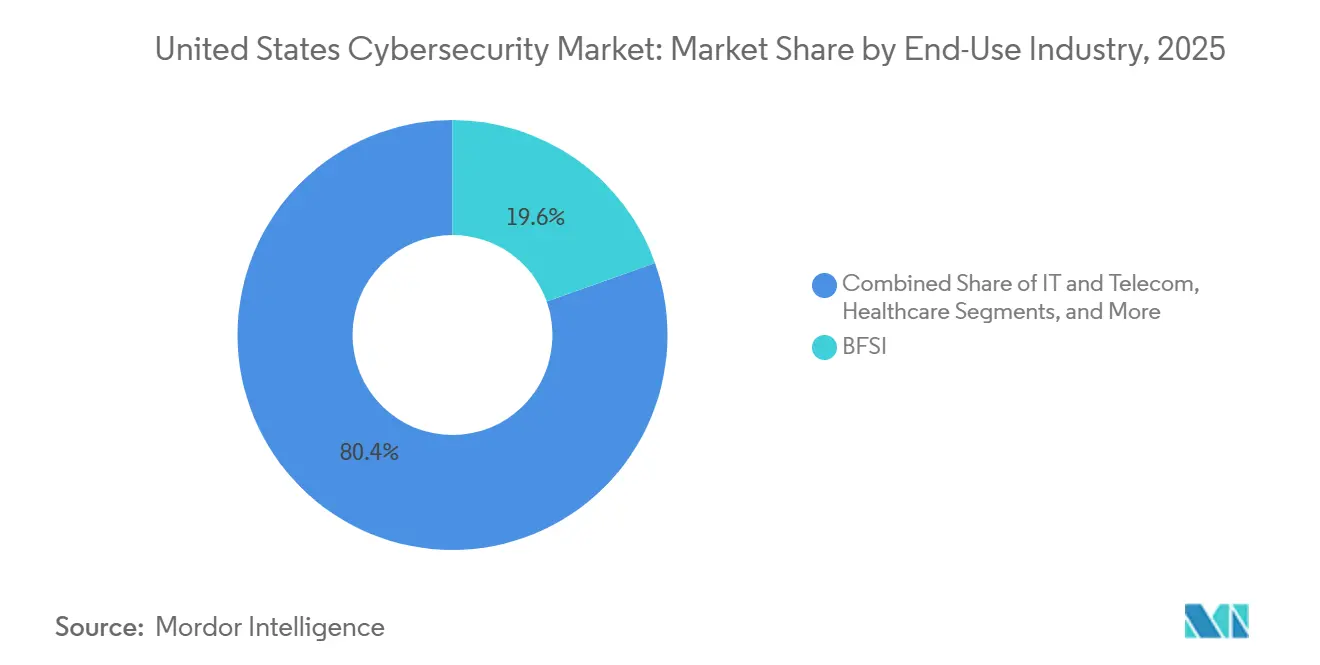

- By end-use industry, BFSI captured 19.56% of outlays in 2025, while healthcare is advancing at a brisk 9.06% CAGR through 2031.

- By enterprise size, large companies commanded 67.29% of expenditures in 2025, yet small and medium enterprises are accelerating at 8.57% on the back of managed detection and response adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Ransomware-as-a-Service Targeting Mid-Sized Enterprises | +1.5% | National, with concentration in healthcare-dense states (Texas, Florida, California) | Short term (≤ 2 years) |

| Mandated Zero-Trust Deadlines Across U.S. Federal Agencies | +1.3% | National, with federal procurement ripple effects in Virginia, Maryland, District of Columbia | Medium term (2-4 years) |

| Accelerated Cloud-Native Application Adoption by Regulated Sectors | +1.2% | National, led by financial hubs (New York, Illinois) and tech corridors (California, Washington) | Medium term (2-4 years) |

| Rapid Uptake of AI-Assisted Threat Detection Platforms | +1.1% | National, early adoption in technology and BFSI sectors | Long term (≥ 4 years) |

| State-Level Data-Privacy Laws Creating Regional Hot-Spots | +0.9% | California, Virginia, Colorado, Connecticut, Utah, with spillover to multi-state retailers | Medium term (2-4 years) |

| Cyber-Insurance Premium Discounts Tied to EDR Deployment | +0.6% | National, strongest in states with high cyber-insurance penetration (New York, California, Texas) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Ransomware-as-a-Service Targeting Mid-Sized Enterprises

Ransomware ecosystems now enable low-skill affiliates to deploy sophisticated payloads, placing mid-market organizations squarely in attackers’ crosshairs. GuidePoint Security recorded that 67% of ransomware incidents in Q3 2025 struck organizations with fewer than 1,000 employees. Coveware pegged the median demand at USD 1.5 million in Q2 2025, up 25% versus late 2024 as adversaries refine victim profiling. Healthcare suffered outsized disruption when the Change Healthcare breach froze claims processing for 100 million patients, illustrating the operational fallout of under-investment.[1]U.S. Department of Health and Human Services, “Change Healthcare Breach Notice,” hhs.gov Cyber-insurance carriers such as Beazley note 40% lower loss severity among policyholders running endpoint detection and response, a statistic that is fueling defensive automation. Together, higher ransom values and premium incentives are nudging previously hesitant mid-sized enterprises to modernize defenses.

Mandated Zero-Trust Deadlines Across U.S. Federal Agencies

Executive Order 14028 and OMB Memorandum M-22-09 require 22 civilian agencies to hit zero-trust milestones by September 2024, catalyzing procurement of identity governance, privileged access management, and continuous device validation tools. Federal momentum is cascading into state and local governments 18 states published zero-trust roadmaps during 2025 and into the defense-industrial base through CMMC 2.0 certification. Contractors exceeding USD 7.5 million in contract value must now pass third-party assessments, widening the addressable market for unified platforms that cover identity, device, network, application, and data pillars. Vendors with FedRAMP authorization hold a clear advantage, accelerating consolidation around players able to meet federal baselines.

Accelerated Cloud-Native Adoption by Regulated Sectors

CISA’s Secure by Design pledge, signed by 68 software suppliers in 2024, encourages cloud delivery with security controls enabled out of the box. The Federal Financial Institutions Examination Council’s updated guidance removed lingering ambiguity over multi-cloud architectures, freeing USD 12 billion in incremental banking cloud spend during 2025. Parallel HIPAA revisions permit cloud storage of protected health information under updated business associate agreements, opening a secondary wave of healthcare migrations. As workloads shift, demand is swelling for container security, API protection, and cloud-native application protection platforms that knit posture management and runtime defense into a single console. Traditional perimeter vendors are forced to acquire specialist capabilities to stay relevant.

Rapid Uptake of AI-Assisted Threat Detection Platforms

Generative AI has slashed the cost of crafting convincing social-engineering lures, with a 135% surge in AI-generated business email compromise attempts logged in 2025.[2]Public Safety Cyber Threat Alliance, “AI-Generated Threats Report 2025,” pscta.org Defenders are striking back by infusing large language models into security operations. CrowdStrike’s Charlotte AI and Microsoft’s Security Copilot both cut triage time by roughly 30% in pilot programs. Despite early gains, only 18% of U.S. enterprises have fully deployed AI-driven anomaly detection, citing false positives and model explainability concerns. Hybrid human-machine workflows are emerging as the compromise, with supervised models escalating ambiguous alerts to analysts while autonomously containing low-risk events. As talent scarcity persists, AI copilots are expected to become a force multiplier rather than a silver-bullet replacement.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Shortage of Certified Cybersecurity Talent | -0.8% | National, acute in rural states with limited university programs | Long term (≥ 4 years) |

| High Total Cost of Ownership for Siloed Best-of-Breed Tool Stacks | -0.7% | National, most pronounced in mid-market enterprises with limited IT budgets | Medium term (2-4 years) |

| Quantum-Readiness Delays Freezing Budget for Near-Term Projects | -0.4% | National, concentrated in financial services and defense sectors | Medium term (2-4 years) |

| Nation State Driven Back Door Bans on Specific Hardware Vendors | -0.3% | National, with supply-chain ripple effects in telecommunications and federal sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Shortage of Certified Cybersecurity Talent

Cyberseek counted 225,000 unfilled roles in 2024, while ISC2’s workforce study estimated a regional shortfall of 500,000 specialists across North America.[3]Cyberseek, “Cybersecurity Supply-Demand Heatmap,” cyberseek.org Salary inflation surpasses USD 120,000 for mid-level positions, yet certification costs deter many from upskilling. Fortinet found 62% of U.S. organizations postponed projects due to staffing constraints, propelling 28% year-over-year growth in managed detection and response services. Operational technology security is squeezed hardest, with fewer than 10,000 professionals nationwide blending industrial and cyber domain expertise. The widening skills gap could cap adoption of advanced controls despite board-level urgency.

High Total Cost of Ownership for Siloed Best-of-Breed Tool Stacks

Panaseer’s 2024 audit revealed mid-sized firms juggle an average of 76 security tools, devouring 40% of security-operations labor hours in integration chores. Lockton’s December 2025 cyber-insurance update showed carriers charging 15% higher premiums when enterprises exceed 50 discrete platforms, viewing complexity as an underwriting red flag. Platform vendors promise relief, but data-migration friction and API incompatibilities extend transition timelines. Decision-makers increasingly factor integration effort alongside feature breadth, driving a gradual but uneven convergence toward unified consoles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain as Outsourcing Accelerates

Solutions dominated spending with 63.28% in 2025, yet services are expanding at an 8.13% CAGR as enterprises unable to recruit staff turn to managed security partners. Within solutions, identity and access management led adoption because zero-trust frameworks require continuous authentication. Application and cloud security tools are embedding vulnerability scanning into DevOps pipelines, driving the shift-left movement. Data-security posture management is a fast-emerging capability that scans cloud storage for misconfigurations and sensitive data exposure, complementing encryption.

The United States cybersecurity market size for services is projected to expand faster than solutions because managed detection, incident response retainers, and compliance consulting offset internal head-count shortages. Platform vendors respond by bundling professional services with product suites, blurring category lines. As breach-notification timelines shorten under state privacy laws, demand for rapid containment services rises, reinforcing the growth trajectory.

By Deployment Mode: Cloud Dominates as Hybrid Fades

Cloud deployments captured 63.12% of 2025 outlays and are advancing at 8.64% as on-premises refreshes taper. CISA’s Secure by Design pledge nudges vendors toward default cloud delivery, and updated FFIEC guidance eases residency requirements for banks, accelerating multi-cloud strategies. Defense contractors still maintain isolated enclaves for controlled unclassified information, but administrative workloads are moving to FedRAMP-authorized clouds.

Hybrid architectures are thinning as enterprises retire legacy hardware, catalyzing demand for secure access service edge platforms that enforce uniform policies across distributed users. The United States cybersecurity market share for on-premises solutions is shrinking in absolute terms, though critical infrastructure owners retain air-gapped installations for safety reasons. Continuous auditing of infrastructure-as-code templates via cloud-security-posture-management tools is now table stakes, driving cross-sell momentum for incumbents.

By End-Use Industry: Healthcare Surges Post-Breach

BFSI remained the largest spender with 19.56% in 2025, channeling budgets into identity, data encryption, and real-time fraud analytics to meet evolving regulatory directives. Healthcare, however, is projected to grow at 9.06% through 2031 after the Change Healthcare and Ascension ransomware crises exposed systemic vulnerabilities in clinical workflows. Energy and utilities spending is climbing on the back of Transportation Security Administration mandates, while manufacturing invests in operational-technology security following a 22% surge in disclosed industrial-control-system vulnerabilities.

The United States cybersecurity market size for healthcare is forecast to swell as chief information officers adopt network segmentation, offline backups, and endpoint detection to preserve patient safety. Meanwhile, retailers confront a web of state privacy laws that mirror GDPR, spurring tokenization and encryption projects. Segment investment reflects a shift from compliance-only mindsets to resilience-driven architectures.

By End-User Enterprise Size: SMEs Embrace Managed Services

Large enterprises accounted for 67.29% of 2025 expenditure, deploying deep best-of-breed stacks that include cloud-workload protection and data-loss prevention. Yet small and medium enterprises will rise at 8.57% through 2031, closing the gap via subscription-based managed detection and response. GuidePoint Security found that two-thirds of Q3 2025 ransomware incidents hit firms under 1,000 headcount, and premium discounts tied to endpoint detection encourage defensive investment.

Converging compliance obligations erode scale advantages, pushing SMEs toward enterprise-grade encryption and access controls. The United States cybersecurity industry is witnessing a democratization of sophisticated tooling, fueled by consumption pricing that aligns costs with usage. Vendor roadmaps increasingly cater to mid-market pain points, further propelling growth in this cohort.

Geography Analysis

Regional demand clusters around federal, financial, and technology centers. Zero-trust deadlines concentrate spending in the National Capital Region, where agencies and contractors must meet September 2024 milestones for identity and device maturity. Financial hubs in New York, Illinois, and Delaware expand budgets to align with the New York Department of Financial Services’ annual penetration-test and board reporting mandates. California’s technology corridor accelerates adoption of cloud-native platforms under the Secure by Design pledge, spurring investments in container security and API protection.

State-level privacy statutes add another layer of complexity. California’s Privacy Rights Act, Virginia’s Consumer Data Protection Act, and similar laws in Colorado, Connecticut, and Utah compel retailers to standardize controls across jurisdictions. The International Association of Privacy Professionals tracks 13 enacted statutes as of 2026, with pending bills in seven additional states, prompting nationwide rollouts of data-discovery, classification, and encryption solutions. Unified controls lower administrative overhead but elevate initial project costs.

Sector-specific triggers influence geographic pockets. Healthcare spending intensifies in Texas, Florida, Pennsylvania, and Ohio following high-profile breaches, while manufacturing outlays rise in the Midwest to protect automotive and chemical plants from industrial-control attacks. Energy investments cluster along the Gulf Coast due to Transportation Security Administration directives. Remote work’s permanence reduces the concentration of endpoints around headquarters, making cloud-delivered secure access indispensable across all fifty states.

Competitive Landscape

The United States cybersecurity market is moderately fragmented. The top five players Palo Alto Networks, Microsoft, CrowdStrike, Cisco, and Fortinet collectively controlled about 35% of 2025 revenue. Platformization is reshaping vendor strategy as buyers crave simpler stacks. Palo Alto Networks bundles Prisma Cloud and Cortex XDR to secure endpoints, networks, and workloads in one console, while Microsoft leverages Windows, Azure, and Office footprints to cross-sell Sentinel, Entra, and Security Copilot. CrowdStrike, despite a July 2024 outage that crashed Windows endpoints worldwide, retained 98% of clients by issuing service credits and fast-tracking fixes.

White-space opportunities remain in operational-technology security and quantum-safe cryptography. NIST’s FIPS 203-205 standards, released in 2024, spark demand for migration consulting and hardware refreshes. Managed detection and response provider Arctic Wolf captured the mid-market with 40% revenue growth in 2024, illustrating appetite for outsourced operations. SentinelOne differentiates on autonomous containment, quarantining rogue endpoints without human intervention. Consolidation accelerates: Cisco closed a USD 28 billion Splunk acquisition in 2024, and Thoma Bravo took Darktrace private for USD 6.6 billion the same year.

FedRAMP authorization governs federal procurement, creating a two-tier ecosystem favoring compliant vendors. As of December 2025, 287 cloud-security products held approvals, cementing competitive barriers. Platform breadth, AI enablement, and regulatory credentials now weigh as heavily as detection efficacy when enterprises down-select suppliers.

United States Cybersecurity Industry Leaders

Palo Alto Networks, Inc.

Cisco Systems, Inc.

Fortinet, Inc.

Microsoft Corporation (Security Business)

CrowdStrike Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft enabled Security Copilot availability in Azure Commercial regions, expanding generative-AI threat correlation for U.S. financial institutions.

- November 2025: Arctic Wolf launched a fixed-fee response retainer guaranteeing on-site support within 24 hours, targeting mid-market hospitals facing ransomware uncertainty.

- July 2025: Zscaler introduced Posture Control 2.0, integrating cloud-native application protection with identity entitlement analytics to curb over-provisioning in multi-cloud estates.

- January 2025: The US Department of the Treasury awarded 10 spots in a USD 20 billion PROTECTS Cyber Support BPA, signaling unprecedented investment in financial-sector resilience.

United States Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The United States Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the projected value of the United States cybersecurity market in 2031?

The sector is forecast to reach USD 144.07 billion by 2031, reflecting a 7.62% CAGR from 2026.

Which deployment mode is expanding fastest across U.S. organizations?

Cloud delivery is growing at 8.64% as hybrid strategies fade and Secure by Design pledges nudge vendors to ship controls enabled by default.

Why is healthcare spending accelerating on cybersecurity?

Ransomware incidents such as the Change Healthcare breach disrupted clinical operations for millions of patients, catalyzing 9.06% CAGR in healthcare security budgets.

How is talent scarcity shaping defensive strategies?

With 225,000 open roles nationwide, enterprises increasingly outsource monitoring to managed detection and response providers that grew 28% year over year in 2025.

What effect do state privacy laws have on cyber budgets?

A patchwork of 13 enacted statutes compels retailers and service firms to deploy unified data-discovery, classification, and encryption tools to automate compliance across jurisdictions.

Page last updated on: