Market Trends of Southeast Asia Oil and Gas EPC Industry

This section covers the major market trends shaping the Southeast Asia Oil & Gas EPC Market according to our research experts:

The Downstream Sector to Dominate the Market

- Southeast Asia's refining sector is witnessing significant growth on account of the increasing demand for refined products from industries such as chemical, petrochemical, and transport. The cumulative population in the region is expected to grow by approximately 13% by 2030, and according to the Asian Development Bank, the region's growth forecast remains unchanged due to the COVID-19 pandemic, which is slightly down to 7% and 5.3% in 2022.

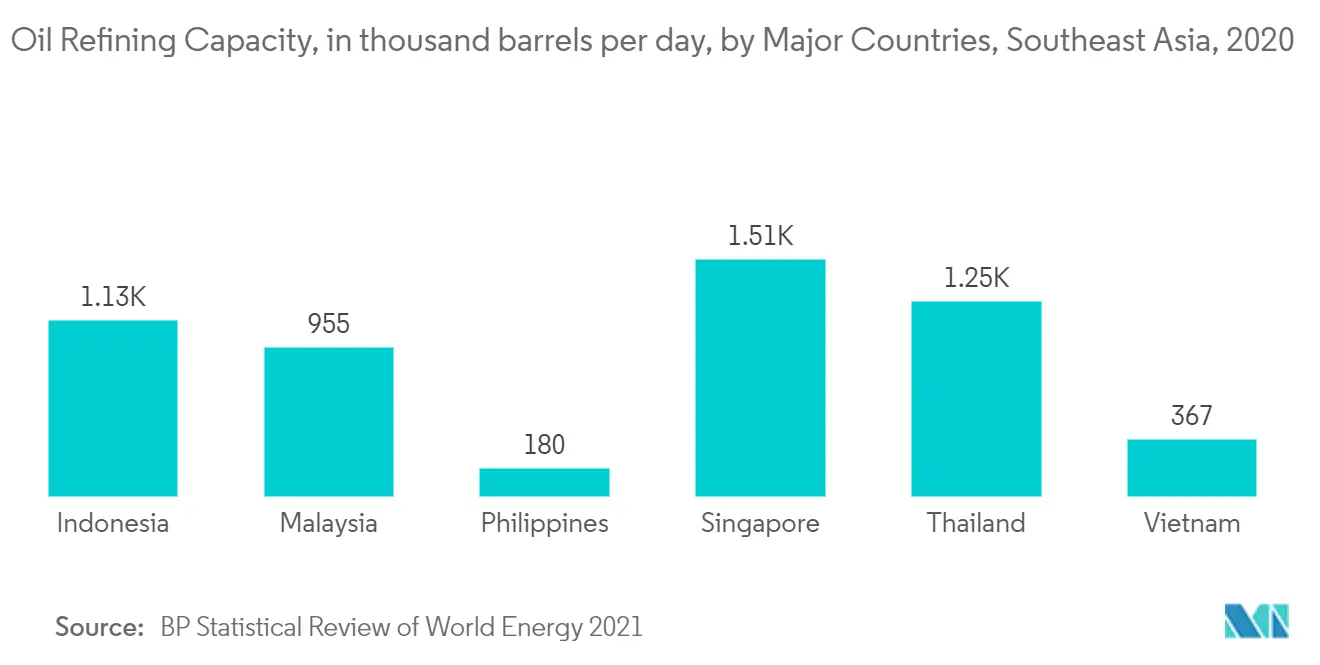

- According to the BP Statistical Review of World Energy 2021, Singapore had the largest refining capacity of 1,514 thousand barrels daily, followed by Thailand, Indonesia, Malaysia, Vietnam, and other Southeast Asian countries. The refining capacity in the region has not witnessed any notable expansion in the past five years, apart from Vietnam, which has previously led to very minimal opportunities for the EPC market players.

- However, with the growing demand for petroleum products and countries working towards being self-reliant to meet the demand, the downstream infrastructure in the region is expected to increase significantly in the coming years. Indonesia, Malaysia, Brunei, Singapore, Thailand, Vietnam, the Philippines, etc., have formulated plans for either expanding the current refineries or constructing new ones.

- Malaysia invested heavily in refining activities during the last two decades, and it can now meet most of its demand for petroleum products domestically after relying on refineries in Singapore for many years. Furthermore, three major integrated petrochemical complexes (IPCs) were established in Kerteh, Gebeng, and Pasir Gudang-Tanjung Langsat in Malaysia.

- Many international firms, such as Chevron's Caltex, ExxonMobil, and Shell PLC, have made significant investments in Singapore's energy sector, including many petrochemical and refining assets. As of May 2019, ExxonMobil had assets worth USD 18 billion in the country, which serves as the Asia-Pacific hub for the company's downstream and chemical businesses.

- Moreover, economies such as Brunei and Vietnam are on the cusp of witnessing the inflow of several EPC contracts in the downstream sector. In Brunei, several large downstream oil and gas projects are expected to commence operations in the coming years, such as Phase 2 of the Pulau Muara Besar Refinery & Petrochemical Complex, for which contracts were let out in August 2020.

- Therefore, owing to the above points, the downstream sector is expected to dominate the Southeast Asia oil and gas EPC market.

Understand The Key Trends Shaping This Market

Download Sample

Indonesia to Dominate the Market

- As of 2020, Indonesia's proven oil reserves stood at 2.4 billion barrels, and the proven gas reserves stood at 44.2 trillion cubic feet. Along with this, it has a diverse geographical profile. The geological basins comprise 60 sedimentary basins, including 36 in Western Indonesia that have already been thoroughly explored, out of which 14 produce oil and gas. Substantial oil and gas reserves increase the country's exploration and production activities, which is likely to stimulate the EPC operations during the forecast timelines.

- In the recent past, the upstream industry of Indonesia failed to meet even the domestic refining capacity. Also, the country's demand for refined products exceeds domestic refining capacity. These factors indicate the need for the development of the upstream and downstream sectors.

- In 2020, the Indonesian government granted 95 exploitation contract areas compared to what it granted in 2019 (92 exploitation contract areas).

- In 2020, SKK Migas finished the longest 2D Seismic Survey in Jambi Merang KKP. The Jambi Merang Contract Area survey was started with a length of 31,908 km in November 2019, and its last acquisition was completed in August 2020. The survey covered 35 basins from 128 basins in Indonesia, consisting of six producing basins, seven discovery basins, five explored basins, and 17 other basins constituting new or unexplored basins that have never been explored.

- Besides, the EPC market for the midstream industry is also expected to register significant growth. With a large number of construction and upgradation projects for refining and petrochemical plants, the demand for the oil transportation infrastructure is growing, which, in turn, is expected to drive the EPC market for oil pipelines during the forecast period.

- Also, the Indonesian government announced its plans to double the refining capacity during 2018-2025, and it is aiming to reach 2.2 million barrels per day. As a result of these plans, major refinery and petrochemical plant construction and upgradation projects are upcoming and are in the pipeline.

- Therefore, owing to the above points, Indonesia is expected to dominate the Southeast Asia oil and gas EPC market during the forecast period.

Get Analysis on Important Geographic Markets

Download Sample