Market Trends of Semiconductor Back-End Equipment Industry

Assembly and Packaging Segment is Expected to Witness Significant Growth

- The segment's growth is expected to be driven by the increasing acceptance of cutting-edge packaging techniques such as fan-out wafer-level packaging (FOWLP), wafer-level packaging (WLP), and system-in-package (SiP). Furthermore, recent advancements have led to the emergence of packaging technologies like stacked WLCSPs, which enable the integration of multiple integrated circuits in a single package. These advancements encompass a combination of logic and memory chips, as well as stacked memory chips. As a result, the demand for advanced packaging is anticipated to surge, necessitating the acquisition of corresponding equipment.

- The surge in the utilization of semiconductor ICs in various sectors has led to a rise in the requirement for semiconductor packaging and assembly equipment. An example is the electronics industry's expanding necessity for such equipment, driven by the widespread use of electronic devices and their applications. This is anticipated to be a significant factor contributing to the increased demand. Likewise, the growing need for smaller, faster, and more efficient semiconductors is propelling the demand for advanced packaging technologies, fueling the demand for semiconductor packaging equipment.

- The increasing global need for semiconductors in different industries has led to an expansion in their production capacity, consequently fueling the growth of the semiconductor back-end equipment market. In August 2023, TSMC, a prominent semiconductor foundry, initiated new orders with multiple suppliers of state-of-the-art packaging equipment. Gudeng Precision Industrial, Apic Yamada, Disco, and Scientech are among the suppliers working closely with the company. TSMC's decision to engage with equipment suppliers reflects its ongoing commitment to enhancing its advanced packaging capabilities.

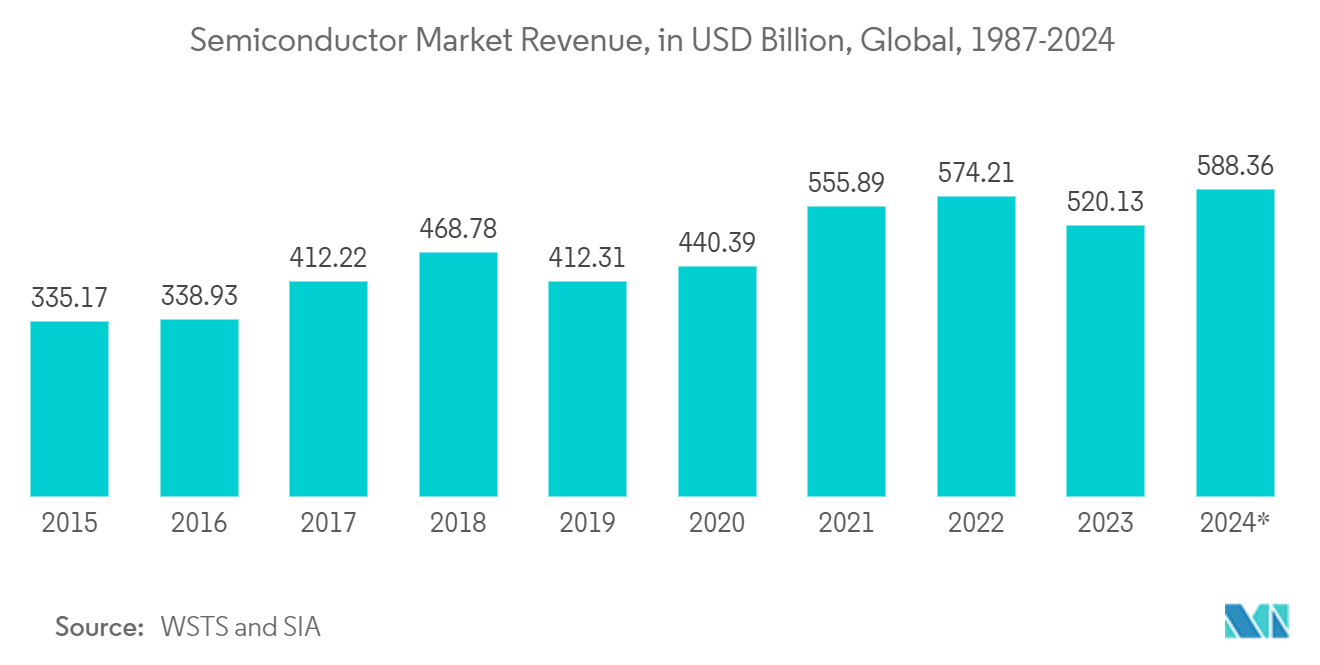

- The significant growth in the utilization and production of semiconductor chips is a key driver behind the expansion of the semiconductor packaging and assembly equipment sector. Moreover, a recent industry forecast by WSTS, supported by SIA, predicts a 9.4% decline in global sales for 2023, followed by a 13.1% increase in 2024. The forecast anticipates that global sales will amount to USD 520 billion in 2023, a decrease from the USD 574.1 billion recorded in 2022. By 2024, global sales are expected to rise to USD 588.4 billion. These positive industry trends will enable packaging equipment vendors to capitalize on market opportunities.

- The market is anticipated to be driven by the investments made by prominent vendors such as Micron, TSMC, and ASE in packaging technologies, along with other vendors capitalizing on the advantages offered by these technologies. Apple, Samsung, and Intel are among the companies that utilize advanced chip packaging (ACP) to enhance device performance and efficiency by consolidating multiple components onto a single substrate. Such adoption by the companies will enhance the growth of ATP equipment.

Understand The Key Trends Shaping This Market

Download Sample

Asia-Pacific Expected to Witness Significant Growth in the Market

- China is pursuing an ambitious semiconductor agenda with the support of USD 150 billion in funding. The country aims to enhance its domestic IC industry and increase its chip production. The ongoing US-China trade war has intensified tensions in this crucial sector, where the most advanced process technology is concentrated, leading many Chinese companies to invest in semiconductor foundries. China has unveiled various initiatives to strengthen its semiconductor sector, such as a substantial expansion campaign in the foundry, gallium-nitride (GaN), and silicon carbide (SiC) markets.

- The growing semiconductor business and increasing chip production capabilities in the region are expected to drive the demand for back-end equipment. China's tech industry aims to ascend the global technology value chain by capitalizing on its strong presence in telecommunications, renewables, and electric vehicles (EVs).

- In addition to these sectors, the industry is now focusing on advanced semiconductors. This transition is primarily driven by advancements in advanced node manufacturing, the expansion of the memory market, active involvement in the silicon carbide (SiC) race, and strategic investments in advanced packaging and manufacturing equipment. The growing foundry business and investments in fabs throughout China are anticipated to stimulate the market.

- South Korea has seen notable growth in its semiconductor industry over the past few years, with a substantial increase in both production and shipments. This surge indicates a resurgence in technological advancement, which bodes well for the country's economy and the global tech sector. Leading South Korean semiconductor companies like Samsung and SK Hynix have established themselves as key players in the global semiconductor industry. The expanding chip production capabilities in the region will further boost the market for back-end equipment.

- The surge in chip demand across various markets in the region has brought attention to the back-end semiconductor business. Companies specializing in back-end processes are anticipated to persist in making aggressive investments and technological advancements in the upcoming years.

Get Analysis on Important Geographic Markets

Download Sample