Market Size of satellite attitude and orbit control system Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 2.59 Billion |

|

|

Market Size (2029) | USD 5.25 Billion |

|

|

Largest Share by Orbit Class | LEO |

|

|

CAGR (2024 - 2029) | 15.18 % |

|

|

Largest Share by Region | North America |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Satellite Attitude and Orbit Control System Market Analysis

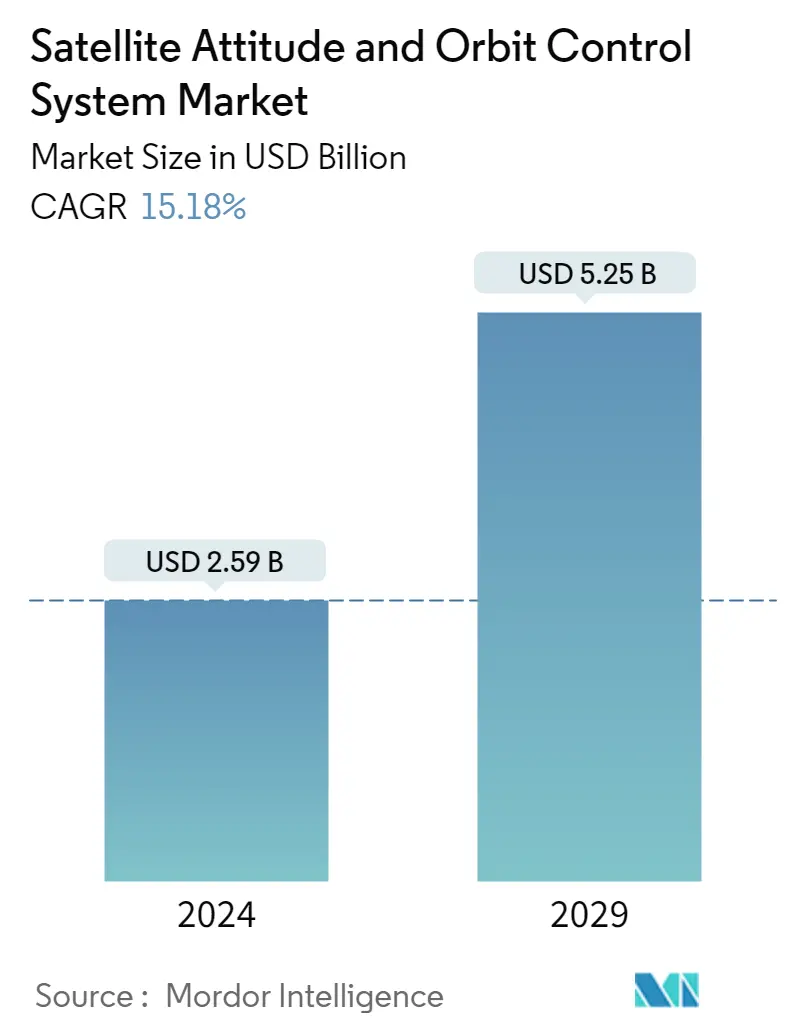

The Satellite Attitude and Orbit Control System Market size is estimated at USD 2.59 billion in 2024, and is expected to reach USD 5.25 billion by 2029, growing at a CAGR of 15.18% during the forecast period (2024-2029).

2.59 Billion

Market Size in 2024 (USD)

5.25 Billion

Market Size in 2029 (USD)

28.26 %

CAGR (2017-2023)

15.18 %

CAGR (2024-2029)

Largest Market by Satellite Mass

65.83 %

value share, 100-500kg, 2022

Minisatellites with expanded capacity for enterprise data (retail and banking), oil, gas, and mining, and governments in developed countries pose high demand. The demand for minisatellites with a LEO is increasing due to their expanded capacity.

Largest Market by Application

78.69 %

value share, Communication, 2022

Governments, space agencies, defense agencies, private defense contractors, and private space industry players are emphasizing the enhancement of the communication network capabilities for various public and military reconnaissance applications.

Largest Market by Orbit Class

72.49 %

value share, LEO, 2022

LEO satellites are increasingly being adopted in modern communication technologies. These satellites serve an important role in Earth observation applications.

Largest Market by End User

69.05 %

value share, Commercial, 2022

The commercial segment is expected to occupy a significant share because of the increasing use of satellites for various telecommunication services.

Leading Market Player

52.48 %

market share, OHB SE, 2022

OHB is the leading player in the global satellite attitude and orbit control system market. The company invests in mission-critical technologies across all applications, especially in Earth observation satellites and their components.

Rapid or increased deployment of LEO satellites driving the adoption rate of AOCS

- The satellite AOCS market is experiencing strong growth, driven by the increasing demand for LEO satellites, which are used for communication, navigation, Earth observation, military surveillance, and scientific missions. The LEO segment is the largest and most widely used among the three orbit classes. It occupies the majority of the share when compared to the other two orbit classes. Between 2017 and 2022, more than 4,100 LEO satellites were manufactured and launched across all the regions, primarily for communication purposes. In addition, the demand for AOCS is increasing because of the increasing adoption of communication satellites for high-speed internet access, particularly in rural and remote areas. This has led companies such as SpaceX, OneWeb, and Amazon to plan the launch of thousands of satellites into LEO.

- MEO satellites constitute the second largest share. The usage of these satellites in the military has increased because of their added advantages, such as increased signal strength, improved communications and data transfer capabilities, and greater coverage area.

- In addition, though the requirement of AOCS for GEO satellites is less, it plays an important role in ensuring the proper functioning of GEO satellites by performing a range of tasks, including controlling the satellite's orientation, stabilizing its position, and correcting any disturbances caused by external factors like solar wind, magnetic fields, and gravity. AOCS system manufacturers provide advanced products for GEO satellite platforms, including innovative star trackers, reaction wheels, gyroscopes, and magnetic torques.

Development and launch of large number of satellites drives the growth of the market

- Satellite AOCS play a vital role in maintaining satellites' precise positioning, stability, and orientation in space. These systems are crucial for ensuring the success of satellite missions, enabling accurate data collection, communication, and Earth observation. The global AOCS market is witnessing significant growth, with North America, Europe, and Asia-Pacific emerging as key regions driving advancements in this industry.

- North America is a leading player in the global AOCS market, with the United States at the forefront of technological advancements. The region boasts a robust space industry comprising established aerospace companies, research institutions, and government agencies. The North American AOCS market is driven by strong demand for satellite-based communication, defense, and scientific missions.

- The European AOCS market benefits from strong collaborations between ESA member states and the European Union. Leading European countries such as France, Germany, and the United Kingdom have a strong presence in satellite manufacturing, contributing to the growth of the AOCS market. The region emphasizes the development of advanced AOCS technologies, including star trackers, reaction wheels, and thruster systems.

- The Asia-Pacific region has emerged as a key player in the global AOCS market, driven by the rapid expansion of its space industry. Countries like China, India, and Japan have invested substantially in space exploration, satellite technology, and indigenous manufacturing capabilities. The growing demand for communication, remote sensing, and navigation services fuels the adoption of AOCS systems.