Market Trends of Russian Federation Oil and Gas Midstream Industry

This section covers the major market trends shaping the Russian Federation Oil & Gas Midstream Market according to our research experts:

Transportation as a Significant Segment

Globally, pipelines are a major mode of transportation for crude oil, oil products, and natural gas. Russia's natural gas accounted for 45% of imports and almost 40% of European Union gas demand in 2021.

As of 2021, Russia was the second-largest producer of natural gas, behind the United States, and held the world's largest gas reserves. In 2021, the country produced 762 billion cubic meters (bcm) of natural gas and exported 210 bcm via pipelines to various countries.

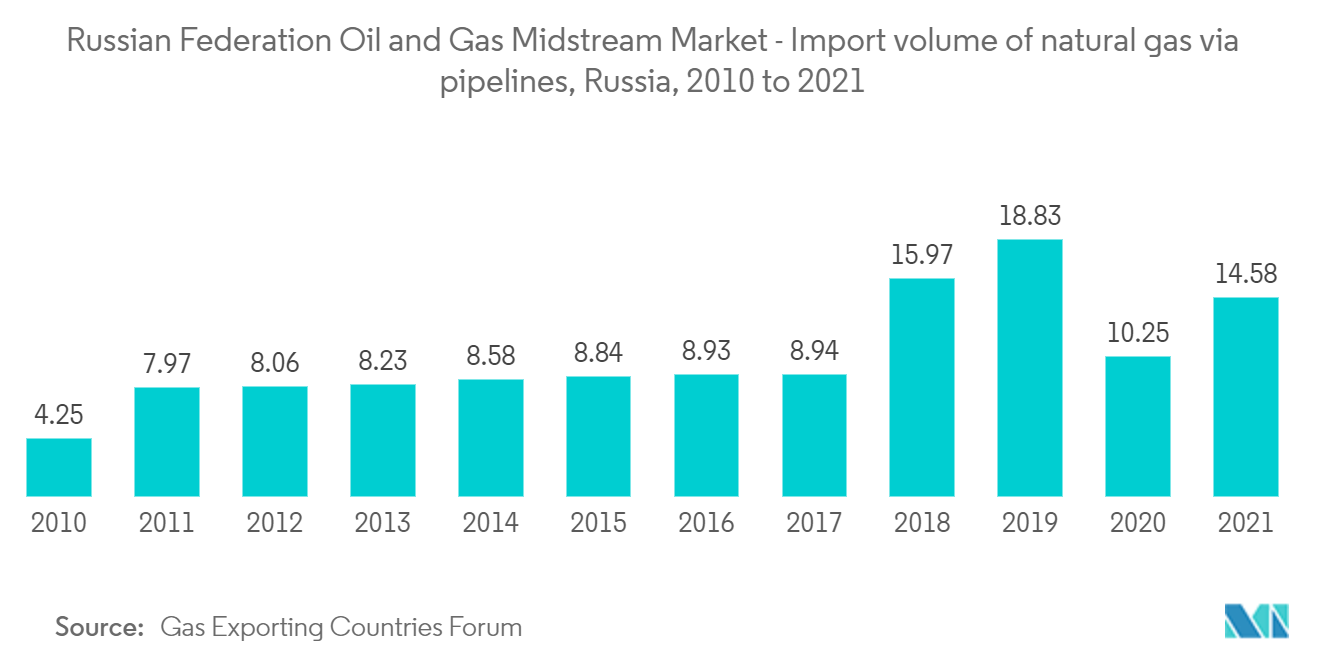

Russia imported nearly 14.6 billion cubic meters (bcm) of natural gas via pipelines in 2021, which was more than in the previous year.

Russia's natural gas accounted for 45% of imports and almost 40% of EU gas demand in 2021. This share has increased in recent years as European natural gas production has declined. Germany, Turkey, and Italy are the largest importers of Russian natural gas.

Russia has expanded its liquefied natural gas capacity to compete with growing LNG exports from the United States, Australia, and Qatar. In 2021, the government of Russia released a long-term LNG development plan, targeting 110-190 bcm/year of LNG exports by 2025.

Due to the above-mentioned factors, the transportation segment is expected to dominate the Russian Federation oil and gas midstream market during the forecast period.

Increasing Development of LNG Terminals

LNG terminals are exporting facilities for natural gas, where it gets converted to liquid form. Various gas pipelines and storage facilities are installed to facilitate terminals with natural gas and export them to various countries.

Russia was the fourth largest exporter of LNG worldwide in 2021. Nearly 30 million metric tons of liquefied natural gas (LNG) were exported from Russia in 2021.

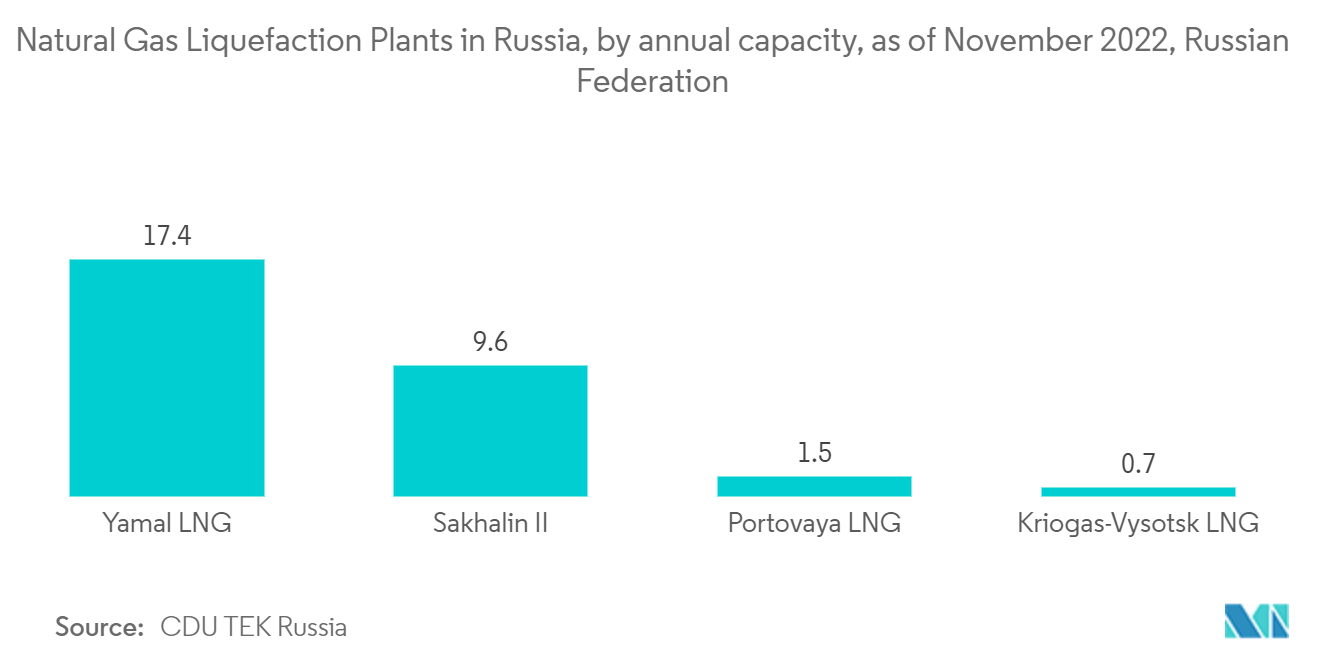

Among operational natural gas liquefaction plants in Russia, Yamal LNG had the largest annual capacity as of November 2022. Each of its first three trains had a capacity of 5.5 million metric tons of LNG, while the fourth one, put into operation in 2021, had a capacity of 0.9 million metric tons. Yamal LNG was operated by Novatek. The second largest operational LNG liquefaction plant was Sakhalin II, whose two trains had a total capacity of 9.6 million metric tons per year.

The country has a few proposed LNG terminal projects. Arctic LNG-2 is one of the key proposed LNG projects with an estimated capacity of 19.8 MTPA. Thus, the commissioning of the ongoing and proposed LNG terminal is expected to boost the LNG terminal capacity and expand the midstream sector of the country during the forecast period.

In February 2022, Yakutia LNG, a 17.7 million metric ton/year (mmty) liquefaction project proposed for the Russian republic of Yakutia, is planned to start up in 2027 to deliver liquefied natural gas (LNG) from Russia's Far Eastern coast to China. This project is expected to reach a final investment decision (FID) in 2023.

Due to the above-mentioned factors, increasing developments of LNG are expected to drive the Russian federation oil and gas market's growth during the forecast period.