Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

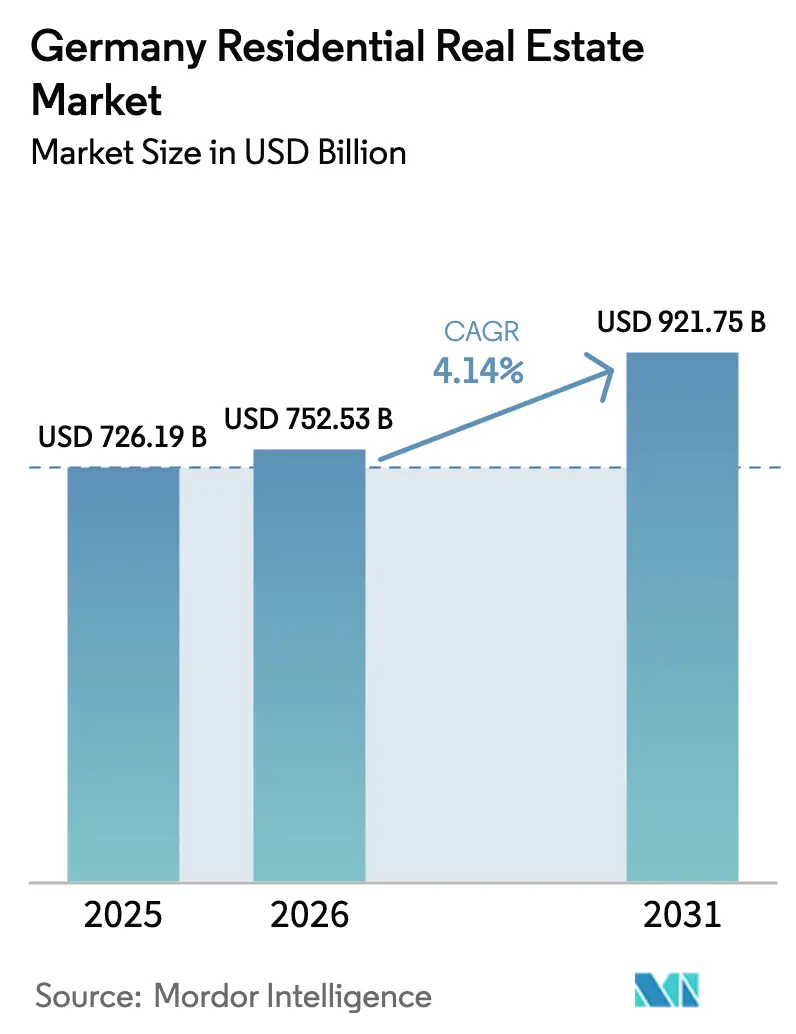

| Base Year Market Size (2025) | USD 726.19 Billion |

| Market Size (2026) | USD 752.53 Billion |

| Market Size (2031) | USD 921.75 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Residential Real Estate Market Analysis by Mordor Intelligence

The Germany Residential Real Estate Market size is expected to grow from USD 726.19 billion in 2025 to USD 752.53 billion in 2026 and is forecast to reach USD 921.75 billion by 2031 at 4.14% CAGR over 2026-2031, underpinned by stringent energy-efficiency mandates, net-migration inflows, and modular-construction innovation[1]European Commission, “Energy Performance of Buildings Directive,” energy.ec.europa.eu. Institutional investors rotate capital toward retrofit-ready multifamily stock, while suburban households pivot to villas that promise energy autonomy and garden space. Affordable-housing stimulus worth USD 19.8 billion through 2027 accelerates social-rental starts and narrows the supply gap for lower-income renters [2]Federal Ministry for Housing, Urban Development and Building, “Social Housing,” bmwsb.bund.de. Mortgage-rate relief from 4.2% in 2023 to 3.3% in 2025 improves first-time-buyer affordability, yet rates above 3.5% still temper demand in Munich and Hamburg. Proptech adoption scales quickly as landlords deploy smart-metering and predictive-maintenance tools to lift net operating income and satisfy corporate green-lease clauses.

Key Report Takeaways

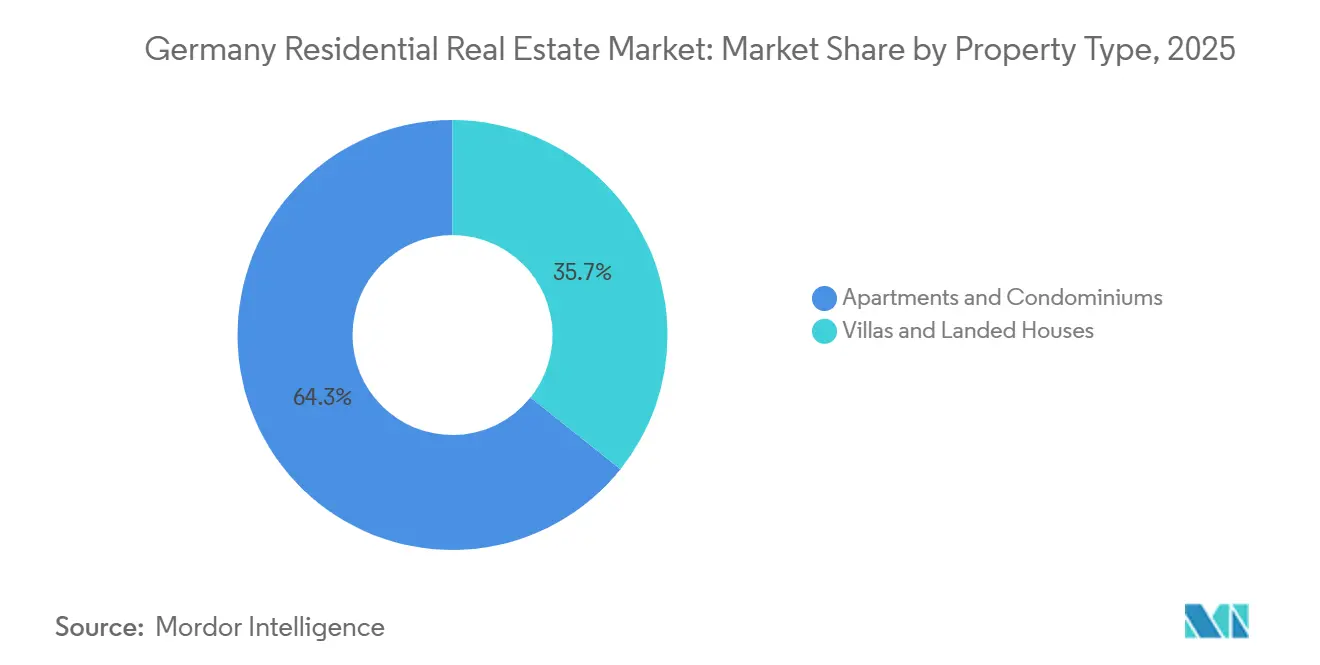

- Apartments and condominiums captured 64.26% of 2025 transaction value, whereas villas and landed houses are forecast to expand at a 5.19% CAGR through 2031.

- Mid-market units held 46.26% of spending in 2025, but the affordable tier is poised for a 5.22% CAGR under the Housing for All program.

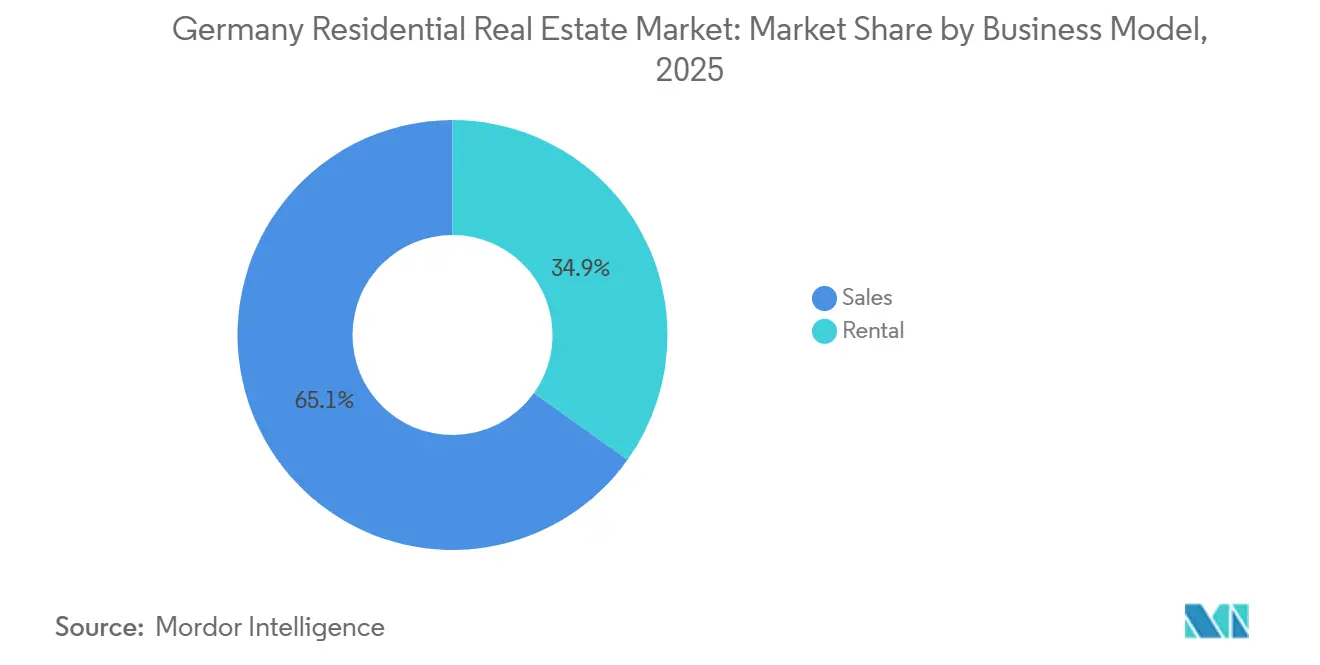

- Sales still represented 65.14% of activity in 2025, yet rental portfolios will rise at a 5.39% CAGR as institutions prize yield stability.

- Secondary-market resales commanded 70.14% of deals in 2025, while primary new-build transactions are projected to post a 5.43% CAGR on faster permitting.

- Berlin led with a 13.94% 2025 market share, and Leipzig is set to achieve the fastest city-level growth at a 5.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USD 19.8 billion Housing for All program | +0.9% | Leipzig, Cologne, Düsseldorf social zones | Short term (≤ 2 years) |

| EPC Class D upgrade mandate | +0.8% | Berlin, Hamburg, Munich legacy stock | Medium term (2–4 years) |

| Mortgage rate rollback | +0.7% | National secondary cities | Short term (≤ 2 years) |

| Skilled Immigration Act reforms | +0.6% | Berlin, Munich, Frankfurt tech hubs | Medium term (2–4 years) |

| AI-enabled modular construction | +0.5% | Hamburg, Leipzig, Düsseldorf | Medium term (2–4 years) |

| Corporate green lease clauses | +0.4% | Berlin, Munich, Frankfurt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

USD 19.8 Billion Housing for All Program Fast-Tracking Affordable Starts

Germany's federal government has pledged USD 19.8 billion to the "Housing for All" initiative through 2027. Annual funding will rise from USD 4.4 billion in 2026 to USD 6.0 billion in 2028. The initiative supports affordable housing via direct grants, low-interest public financing, and faster permitting, reducing approval timelines in pilot municipalities from 18 months to 9 months. The stimulus offsets a 105,000-unit national supply shortfall recorded in 2024, narrowing vacancy and stabilizing rents for 38% of renter households inside the income-eligibility band. Accelerated nine-month permitting cycles lower holding costs and enable modular suppliers to scale volume. Persistent fiscal backing through 2031 should sustain double-digit build rates in designated social-housing corridors.

EPC-Class-D Upgrade Mandate Catalyzing Deep Retrofits

Germany adopted the EU Energy Performance of Buildings Directive in mid-2025, compelling every home to reach at least Class D by 2033, an obligation that redirects USD 273 billion toward insulation, heat pumps, and smart thermostats. Vonovia earmarked USD 1.6 billion in 2024 to modernize 40,000 apartments a year, illustrating the capital shift toward green compliance[3]Vonovia SE, “Annual Report 2024,” vonovia.de. Pre-1990 units, 60% of which are rated below Class D, dominate Berlin and Ruhr portfolios and face elevated retrofit risk. Landlords weighing hefty upgrades or strategic disposals create a vibrant secondary-trading arena for specialist retrofit funds. The mandate, therefore, supports contractors, equipment makers, and ESG-linked financiers while raising entry hurdles for non-compliant stock.

Mortgage-Rate Rollback Unlocking First-Time Buyers

Fixed mortgage costs fell to 3.3% by mid-2025, trimming monthly payments on a USD 327,000 loan by USD 324 relative to 2023. Transaction counts in the USD 218,000–USD 436,000 price band rebounded 18% year-on-year, with Leipzig and Dresden booking the largest volume gains. Nevertheless, Munich and Hamburg remain unaffordable for average earners, implying a two-speed owner-occupier recovery. If rates dip toward 3% by 2027, pent-up demand from 180,000 households could propel additional sales, particularly in secondary cities where prices sit below USD 381,000.

Skilled-Immigration-Act Reforms Intensifying Rental Pressure

Streamlined visa pathways admitted 75,000 skilled workers in 2024, pushing Berlin and Munich vacancy rates below 2%. Median listing periods compressed to under two weeks, prompting landlords to automate tenant onboarding. Furnished units with fiber and IoT sensors fetch 8-12% rent premiums, a clear reward for ESG-certified assets. Corporate relocation clusters amplify the bifurcation between smart, green stock and legacy buildings. Sustained inflows will keep upward pressure on rents and underpin rental-yield resilience in tech corridors.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated 3.5% mortgage plateau | −0.9% | Munich, Hamburg, Stuttgart | Short term (≤ 2 years) |

| Timber and insulation price volatility | −0.6% | Bavaria, Baden-Württemberg | Medium term (2–4 years) |

| 2025 skilled labor wage hike | −0.5% | Berlin, Hamburg, Rhine-Ruhr | Short term (≤ 2 years) |

| Draft Airbnb caps | −0.3% | Berlin, Munich, Hamburg, Cologne | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

ECB Mortgage Plateau Weighing on Buyer Affordability

Ten-year fixed loans averaged 3.5% in late 2025, nearly double 2021 levels, lifting monthly payments above 40% of gross income for Munich properties priced at USD 708,000. Sales volumes in the USD 545,000-plus bracket fell more than one-fifth year-on-year. Developers face higher interest carry, adding up to USD 27,000 per unit, which compresses profit or inflates listing prices. Unless rates retreat toward 3% by 2027, premium-city owner-occupier momentum will lag the broader German residential real estate market recovery.

Material-Cost Volatility Squeezing Developer Margins

Timber swung between USD 196 and USD 262 per m³ in 2024-2025, while insulation costs jumped 12-18% on energy inflation. Mid-tier builders, lacking hedging scale, absorbed 8-12% margin erosion on fixed-price contracts. Thirty-four percent postponed land bids, delaying roughly 18,000 units. Large incumbents counteract volatility through multi-year supply agreements, but sustained swings could still shave 60 basis points off Germany residential real estate market CAGR through 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartments Retain Urban Lion’s Share While Villas Drive Growth

Apartments and condominiums commanded 64.26% of the 2025 transaction value, underlining their entrenched role in dense metros that restrict greenfield land. The Germany residential real estate market size tied to villas and landed houses is forecast to expand at a 5.19% CAGR through 2031, lifted by home-office adoption and rooftop-solar self-sufficiency. Institutional portfolios remain apartment-heavy, with Vonovia’s 548,000 units 92% multifamily and LEG Immobilien’s 167,000 entirely flats, ensuring ample liquidity for urban assets. Leipzig and Dresden record brisk villa absorption, where USD 416,000 prices undercut Munich by 40%, widening the suburban affordability gap.

Energy autonomy fuels villa desirability, as 58% of single-family completions in 2025 included photovoltaic arrays compared with 12% of multifamily deliveries. The EPC mandate penalizes high-rise retrofits that cost USD 27,000-USD 38,000 per unit, nudging capital toward new-build townhouses in exurban belts. Apartment demand still stays solid in Berlin, Hamburg, and Frankfurt, where transit connectivity trumps space considerations, but rental premiums increasingly accrue to EPC-compliant towers outfitted with smart-home dashboards.

By Price Band: Mid-Market Dominates Spend as Affordable Tier Accelerates

Mid-market homes captured 46.26% of 2025 spend, reinforced by Germany’s large cohort earning USD 43,600-USD 87,200. The affordable tier will outpace with a 5.22% CAGR through 2031 on the back of Housing for All subsidies and discounted municipal land parcels. Leipzig, Cologne, and Düsseldorf spearhead volume, offering developers 30-40% land rebates in exchange for 25-year rent caps. Luxury transactions cooled 14% year-on-year in 2025 as buyers awaited rate clarity and wealth-tax negotiations.

TAG Immobilien’s purchase of 1,200 affordable units in Leipzig and Chemnitz illustrates capital rotation into the subsidy-anchored bracket, funded partly by 1.8% KfW loans. Mid-market economics tighten, as USD 2,980 per m² build costs leave slim margins when buyers resist prices above USD 436,000. Consequently, developers embrace modular factories and bulk procurement to defend profitability, a trend likely to widen between tech-enabled builders and small family firms.

By Business Model: Rentals Gain Momentum despite Sales Supremacy

Sales still represented 65.14% of 2025 market value, yet rentals are on track for a 5.39% CAGR through 2031, benefiting from Germany’s 54% renter share and institutions hungry for inflation-indexed yield. Vonovia booked USD 2.3 billion in rental income in the first nine months of 2024, achieving 3.8% like-for-like rent growth despite Berlin rent caps. The Germany residential real estate market share of institutional rentals is likely to rise as pension funds and insurers bulk-buy multifamily blocks to match long-dated liabilities.

Mortgage arithmetic favors renting in premium hubs: a USD 436,000 condo costs USD 1,780 per month to service at 3.5% interest, compared with USD 1,200 median rent for a comparable flat. Leipzig, Dresden, and Erfurt nevertheless register brisk owner-occupier take-up where entry prices sit below USD 381,000 and expected appreciation of 5-7% underpins equity returns. Over the forecast window, a balanced tenure mix emerges, with rental portfolios densifying in metros and sales thriving in secondary growth belts.

By Mode of Sale: Secondary Resales Prevail but New Builds Accelerate

Secondary resales accounted for 70.14% of 2025 transactions, a legacy of Germany’s aging housing stock where 78% of units predate 2000. Primary new-build sales will grow at a 5.43% CAGR to 2031, propelled by nine-month permitting under Construction Turbo rules and consumer preference for warranty and EPC compliance. Leipzig, Düsseldorf, and Frankfurt lead permit issuance as population growth tops 1.2% annually.

Ancillary transaction costs of 8-15% keep resale velocity muted, yet the EPC mandate will force sellers to invest USD 32,000-USD 54,000 in energy upgrades before listing, shrinking the resale price advantage. Vonovia’s delivery of 1,000 smart, Class A apartments in 2024 signals rising appetite for turnkey units that circumvent retrofit headaches. Modular delivery, with 14-month cycle times, feeds pipeline resilience, suggesting the German residential real estate market size attributable to new builds will steadily erode the resale share.

Geography Analysis

Berlin held 13.94% of 2025 market value, buoyed by a 3.7 million population and average rents of USD 17.18 per m², up 12% year-on-year. Vacancy tightened to 2.1% after Skilled Immigration Act flows, prompting municipal debates on stricter rent caps. Short-term rental returns deteriorated under an eight-week annual limit, steering investors toward long-lease multifamily assets equipped with carbon dashboards.

Munich and Hamburg command premium valuations of USD 708,000 and USD 566,000 median prices, respectively, yet sales volumes slipped 18-22% in 2025 as 3.5% mortgage rates eroded affordability. Both cities cap Airbnb stays at 90 days or mandate costly permits, reinforcing institutional dominance in regulated, high-occupancy portfolios. Frankfurt’s 75,000 finance jobs anchor 12,000 corporate-rental units, many under green-lease clauses that demand smart-meter rollouts.

Leipzig is projected to deliver the fastest 5.48% CAGR through 2031, fueled by net in-migration and USD 437 million in Housing for All subsidies. Median homes remain 57% cheaper than in Berlin, attracting first-time buyers and proptech landlords. Cologne, Düsseldorf, and the wider Rhine-Ruhr benefit from logistics corridors and airport connectivity, while secondary hubs such as Nuremberg and Dresden lure equity-minded households with USD 350,000 entry points and 4-6% appreciation.

Regulatory Landscape

Germany's residential market is shaped by a policy mix that targets faster housing delivery while tightening tenant protections and energy-compliance requirements. In October 2025, the federal government enacted the Law for the Acceleration of Housing Construction and Housing Security (Bau-Turbo), introducing Section 246e BauGB to allow more flexible planning permissions for housing delivery in constrained markets.

In May 2026, the Federal Cabinet approved the draft law to modernize urban planning and spatial planning law (Baugesetzbuch-Upgrade), explicitly prioritizing residential construction within planning decisions. At the same time, the government advanced Mietrecht II in April 2026 to curb index-linked rent increases and regulate furnishing surcharges, creating an additional variable for underwriting assumptions in furnished and inflation-indexed rental products. BMWSB also announced an action plan in June 2026 to lower construction costs, including mandatory digital building permit applications by 2028, which pushes developers and municipalities toward standardized, digitized approval workflows.

Value Chain Analysis

The Germany residential real estate value chain covers land sourcing and municipal zoning, project financing, design and engineering, materials procurement, general contracting and specialist trades, and brokerage and transaction services. It then extends into long-tail property management, maintenance, and modernization as energy-performance rules raise compliance workloads and retrofit budgets.

Acceleration policies run into a delivery pipeline that remains lengthy. The average time from building permit to completion reached 27 months in 2025, up from 20 months in 2020, while 2025 completions fell to 206,600 units even as permitting improved. Upstream procurement is still sensitive to supply and pricing, with 9.2% of residential construction companies reporting material-supply constraints as of April 2026. In June 2026, ZDB pointed to a federal decree addressing material supply bottlenecks and price volatility in federal projects, including the use of material price sliding clauses. Midstream indicators show some pipeline rebuild, with building permits rising 10.8% in 2025 versus 2024, and approved residential units up 13.2% year-on-year in January to April 2026, but turning approvals into completions continues to be constrained by labor availability, cost inflation, and lead times.

Competitive Landscape

Market concentration remains moderate as the top five landlords own under 4% of Germany’s 23 million rental units. Vonovia, after the USD 2.5 billion purchase of 18,000 apartments in November 2025, controls 566,000 units and channels USD 1.6 billion annually into retrofit and modular-build programs. LEG Immobilien, focused on North Rhine-Westphalia, financed a USD 655 million green bond to upgrade 50,000 flats, demonstrating the funding edge of ESG issuers.

Mid-cap players prune peripheral holdings to recycle capital into growth corridors. Grand City Properties sold 3,200 non-core units for USD 459 million, redeploying proceeds into Berlin and Düsseldorf, where rent spreads exceed 200 basis points. TAG Immobilien partners with Kaufmann Bausysteme on 1,500 modular affordable apartments, cutting build costs 18% and aligning with subsidy thresholds.

Proptech challengers target fragmented ownership. Platforms offering AI-based maintenance scheduling and blockchain lease contracts claim 20-30% cost savings for landlords with fewer than 50 units. Municipal landlords such as SAGA Hamburg and Degewo leverage subsidized debt but lag in digitization, leaving scope for tech-service outsourcing. Regulatory guidance on tokenized fractional ownership remains a hurdle, yet the innovative capital channel could broaden retail access once prospectus thresholds clarify.

Germany Residential Real Estate Industry Leaders

Vonovia SE

Deutsche Wohnen SE

LEG Immobilien SE

Consus Real Estate

SAGA Unternehmensgruppe Hamburg

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace sits between affordable delivery and faster approvals. BMWSB administrative agreements for social housing for 2026 and 2027 entered into force in March 2026, and the federal government provided EUR 4 billion for 2026, supporting pipelines that align with subsidy-linked rent caps and municipal land programs. The Baugesetzbuch-Upgrade draft approved in May 2026, alongside BMWSB's June 2026 construction-cost action plan (including mandatory digital permit applications by 2028), creates an execution window for developers, modular providers, and proptech vendors to standardize planning, automate permitting documentation, and reduce cycle-time frictions.

A second opportunity focuses on retrofit execution and asset repositioning under energy-performance rules. The market already shows sizable legacy exposure, with pre-1990 stock in major portfolios, and active capital allocation toward modernization by large landlords. This favors platforms and contractors that bundle insulation, heat pumps, smart thermostats, and metering, and it supports secondary-market liquidity for non-compliant assets as owners weigh upgrade capex against disposal. On the capital side, disclosed 2025 real estate investment activity, including EUR 8.1 billion in residential, and the rebound in new residential construction financing in 2025 indicate ongoing deployment, while Mietrecht II and existing rent controls raise the value of operational efficiency, transparent energy reporting, and compliance-ready product design across both rental and for-sale segments.

Recent Industry Developments

- June 2026: LEG Immobilien SE reported a scrip dividend uptake with shareholders reinvesting EUR 63.1 million (28.6% acceptance). The approval helps preserve cash for modernization and portfolio capex while maintaining balance sheet flexibility in a market still shaped by retrofit requirements and cost inflation.

- January 2025: LEG Immobilien SE completed the majority acquisition of Brack Capital Properties, adding about 9,000 apartments to its portfolio. The transaction increased scale in residential operations and broadened the base for renovation, digitization, and portfolio optimization initiatives.

- June 2024: Vonovia SE announced it was doubling investments to EUR 2 billion as it resumed a growth trajectory, emphasizing modernization and portfolio measures. The stepped-up capex highlighted the role of energy upgrades and quality improvements as valuation and lettability increasingly track building performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We size the Germany residential real estate market as the total value of homes meant for private living, captured across new build and resale activity, and also reflected through rental and owner-occupied housing economics within Germany.

Scope exclusions: We exclude temporary accommodation formats such as serviced apartments and purpose-built student dormitories that operate more like lodging.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing Home Resale)

- By Geography

- Berlin

- Hamburg

- Munich

- Cologne

- Frankfurt

- Dusseldorf

- Leipzig

- Rest of Germany

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the factual base for the model and to keep key inputs consistent across years. We typically rely on public datasets such as Destatis releases, Deutsche Bundesbank statistics, OECD housing indicators, Eurostat housing and price series, and land registry and municipal planning publications where available.

On top of this, we review listed company filings, investor presentations, reputable real estate press, and association updates to understand shifts in the housing supply pipeline, financing conditions, and transaction activity. A paid subscription focused on company financials and intelligence helps confirm revenue mix and exposure for larger housing owners and related service providers, and a patent database is used selectively when energy-efficiency upgrade methods change cost and pricing assumptions. These are illustrative sources, and many other references are also used to collect, cross-check, and clarify data points during the work.

Primary Interviews and Surveys

Primary work is used to test the desk assumptions and close gaps that public sources cannot answer cleanly, especially around price band movement, buyer and renter behavior, and how activity differs by city versus the rest of the country. We spoke with housing developers, brokers, property managers, lenders, and institutional owners, and then reconciled their inputs so the final model reflects on-the-ground conditions across Germany rather than one city narrative.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 35% | |

| Smaller Players: 14% | Managers: 53% |

Market-Sizing & Forecasting

A top-down approach is used first, where national housing value and activity signals are reconstructed using Germany-level indicators, and then apportioned across key market lenses like sales versus rental and primary versus secondary transactions. To keep it practical, the totals are corroborated with selective bottom-up checks, such as sampled unit volumes by city, observed price per square meter ranges, and roll-ups of reported exposure for major residential owners and intermediaries.

Inputs that matter most include residential price indices, mortgage rate direction and credit availability, building permits and housing starts, transaction velocity by major cities, rent index movement, and the pace of energy-efficiency renovation adoption (which can shift willingness to pay and upgrade costs). Where a bottom-up view is incomplete, gaps are handled through proxy ratios from comparable cities, and then adjusted back to macro controls so the sum stays consistent.

For forecasting, we use scenario analysis supported by simple multivariate relationships between rates, permits, and price and rent trends, and then stress-tested against interview feedback on buyer sentiment and supply bottlenecks. When the main story is still forming, the forecast is tightened by checking that implied household affordability and absorption do not drift away from what practitioners report as feasible.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including whether price and rent growth implied by the totals matches the direction of official index series and major-city transaction commentary. Outliers are flagged, traced back to the driver assumption, and corrected only after the change is consistent across at least two data points or a re-contacted expert view.

Before sign-off, a second analyst reviews the logic, unit consistency, and year-to-year step changes so any sudden jumps have a clear reason. The report is refreshed annually, and interim updates are made when a material change affects rates, regulation, or transaction behavior. Right before delivery, we do a final pass on the newest releases so clients receive the most current view available.

Mordor Intelligence's Germany Residential Real Estate Market Size Compared With Other Published Estimates

Published market values for Germany residential real estate often look far apart, even when they use the same country name on the cover. The gaps usually come from how each publisher treats rentals versus sales, whether land is counted, and which year and currency timing they lock in.

In this market, a key driver is whether the estimate is built from transaction turnover only, or whether it also reflects the broader housing stock and recurring rental economics, which changes the scale quickly. Differences also show up when price band splits are projected using aggressive appreciation, when energy retrofit impacts are not separated from core home values, and when the refresh cadence misses a fast move in interest rates or a permit slowdown.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 726.19 B (2025) | |

| Global Consultancy A | USD 792.00 B (2024) | Uses a different base year and a broader valuation framing that can blend stock value effects with market activity, which makes year-to-year comparability harder when rates swing. |

| Industry Publisher B | USD 361.69 B (2023) | Anchors the value to a narrower pool that appears closer to measured transaction activity and reported revenue flows, which typically excludes parts of owner-occupied housing economics. |

The spread is mainly explained by what is being counted as market value and how the time anchor is chosen, rather than simple math errors. By separating primary and resale activity and keeping rental economics inside the scope (instead of treating it as a separate service market), the sizing choice becomes clearer, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the Germany residential real estate market and its forecast growth?

The Germany residential real estate market size is USD 752.53 billion in 2026 and is expected to climb to USD 921.75 billion by 2031, growing at a 4.14% CAGR.

How will EPC mandates affect property investment strategies in Germany?

The EPC Class D requirement redirects about USD 273 billion into retrofits, making green-compliant assets more valuable and prompting landlords to modernize or divest older stock.

Which German city is forecast to grow fastest through 2031?

Leipzig is projected to lead with a 5.48% CAGR, driven by net in-migration, affordable entry prices, and Housing for All funding.

Why are rentals gaining ground over sales transactions?

Elevated mortgage costs, institutional demand for yield, and Germany’s 54% renter population are propelling rental portfolios to a 5.39% CAGR, outpacing sales growth.

Page last updated on: