Nurse Call Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 4.31 Billion |

| Growth Rate (2026 - 2031) | 9.88% CAGR |

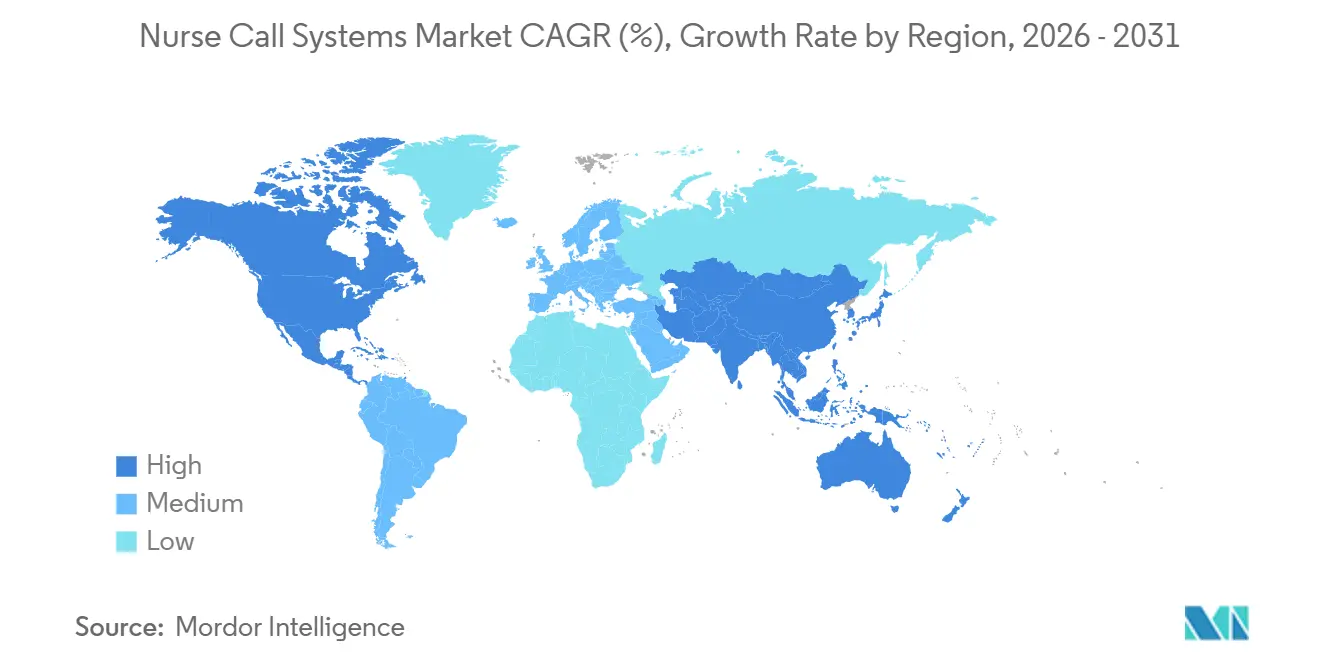

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nurse Call Systems Market Analysis by Mordor Intelligence

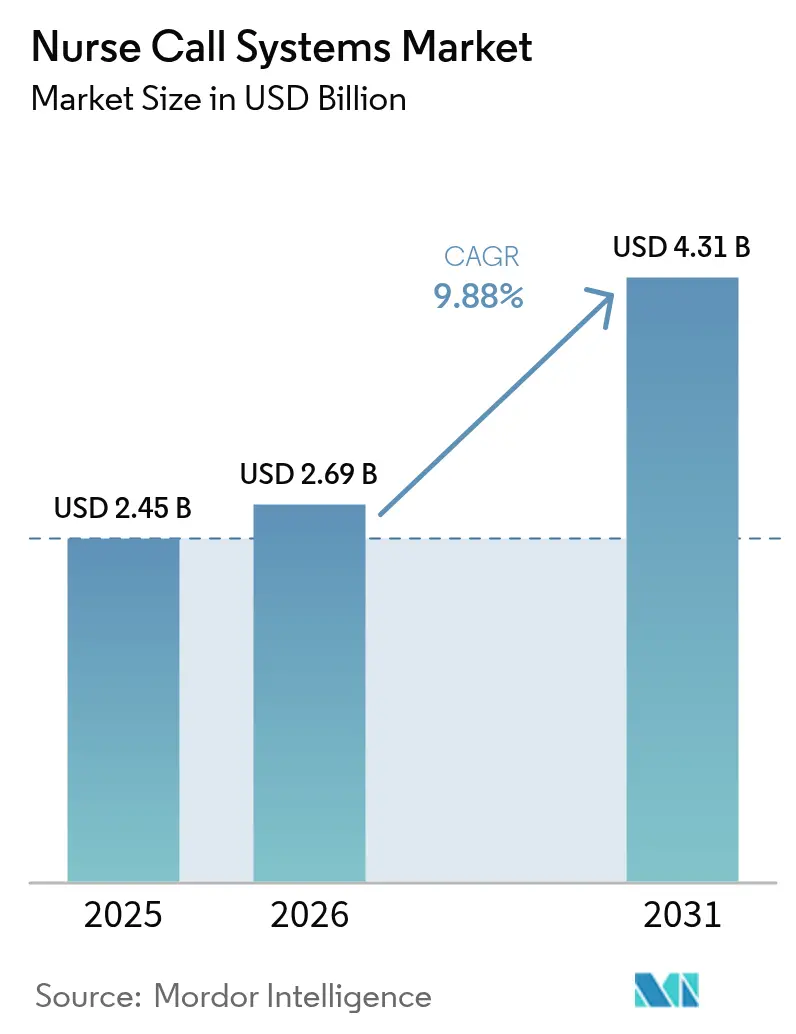

The Nurse Call Systems Market size is expected to grow from USD 2.45 billion in 2025 to USD 2.69 billion in 2026 and is forecast to reach USD 4.31 billion by 2031 at 9.88% CAGR over 2026-2031.

Increasing life expectancy has expanded the over-65 population, driving hospitals to implement automated alarm routing systems. This enables nursing staff to allocate their time to more complex and critical tasks. Healthcare providers are also adopting software-as-a-service (SaaS) models, which shift expenditures from capital budgets to operating budgets—a structure that hospital CFOs can approve without requiring significant bond issuances. Meanwhile, cybersecurity incidents, such as the February 2024 Change Healthcare breach, have elevated security certifications from optional to mandatory criteria in vendor selection, intensifying competition in the market. Additionally, the transition of low-acuity procedures to ambulatory and home care settings is fueling demand for wireless, cloud-native devices that extend alarm visibility beyond hospital premises.

Key Report Takeaways

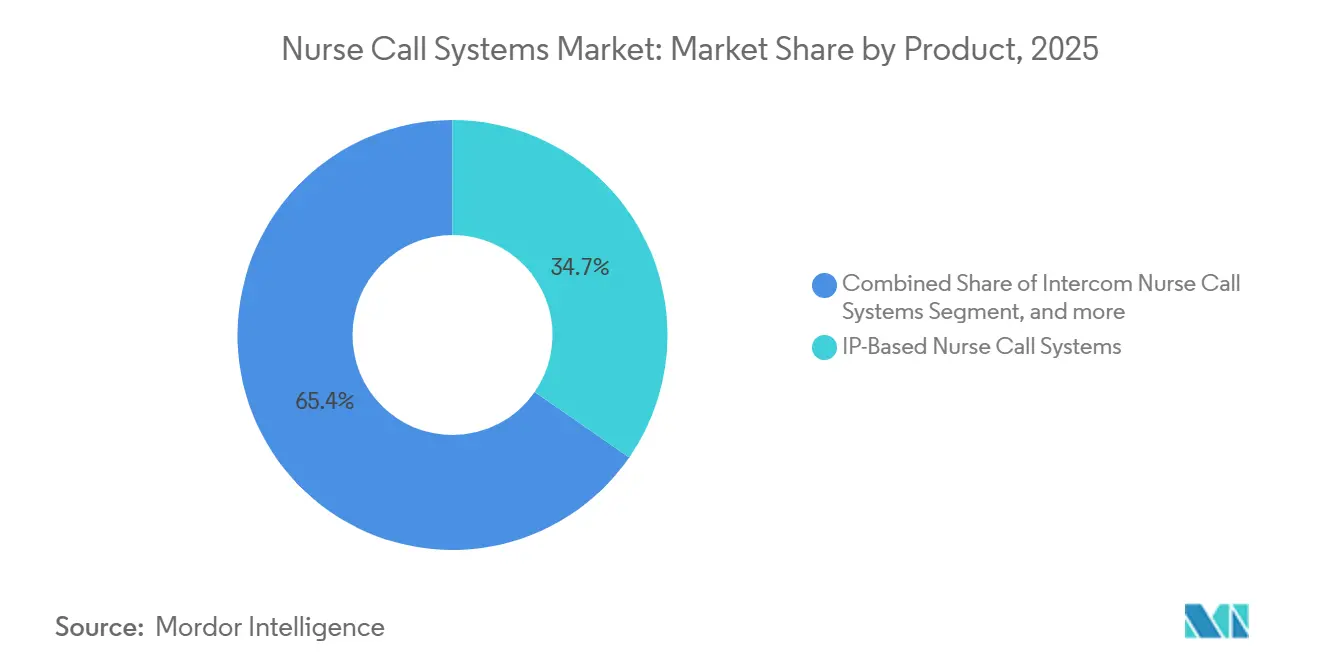

- By product, IP-based nurse call systems led with 34.65% revenue share in 2025, while mobile and cloud-enabled platforms are set to expand at an 11.54% CAGR through 2031.

- By modality, wireless systems dominated with a 62.65% share in 2025 and are projected to grow the fastest at an 11.67% CAGR over 2026-2031.

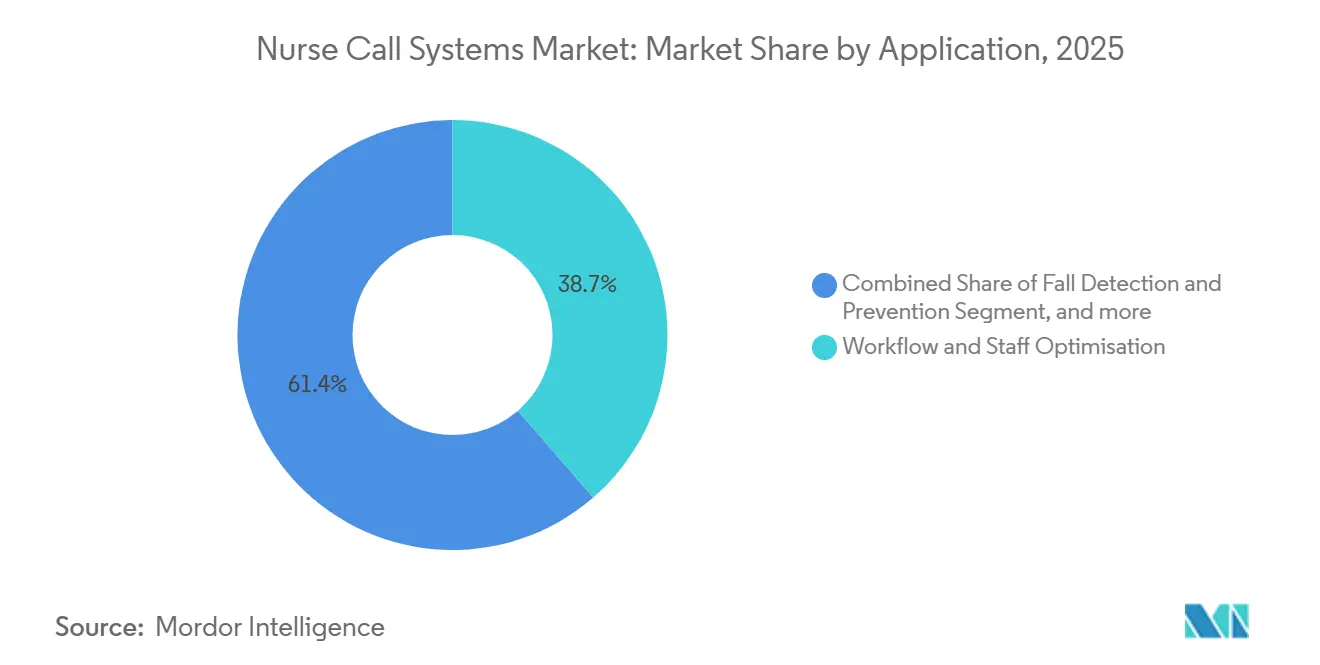

- By application, workflow, and staff optimization held 38.65% of 2025 deployments, whereas fall-detection and prevention solutions are forecast to advance at a 12.12% CAGR to 2031.

- By end user, hospitals and specialty clinics accounted for 48.32% in 2025, while home healthcare settings are poised to register the highest 12.65% CAGR during 2026-2031.

- By geography, North America captured 41.43% of global revenue in 2025, but Asia-Pacific is expected to record the quickest growth at a 10.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nurse Call Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Geriatric Population and Rising Chronic Disease Burden | +2.3% | Global, acute in Japan and Western Europe | Long term (≥ 4 years) |

| Accelerating Hospital Digitalization and Smart Infrastructure Spending | +2.8% | North America, EU, Tier-1 APAC cities | Medium term (2-4 years) |

| Regulatory Push for Patient Safety and Rapid Response Metrics | +1.9% | U.S., EU, Australia | Short term (≤ 2 years) |

| Convergence of Nurse Call with Unified Clinical Communication Platforms | +2.1% | North America and Western Europe | Medium term (2-4 years) |

| Expansion of Home Health and Remote Patient Monitoring Ecosystems | +1.5% | North America, Japan, Australia | Long term (≥ 4 years) |

| Transition From Capex to Subscription-Based “Nurse Call as a Service” Models | +1.4% | Global, especially mid-market hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population and Rising Chronic Disease Burden

The number of people aged 60 and above will double to 2.1 billion by 2050, with 80% living in low- and middle-income countries where bed capacity remains low. Japan already faces a projected nursing shortfall of 270,000 by 2025 despite wage increases, driving hospitals to deploy sensor-based call systems that automatically triage alerts. Multimorbidity further strains legacy hardware: patients with three or more chronic conditions trigger 4.2-times more call-button activations than general med-surg wards. Medicare now penalizes hospitals in the worst quartile for falls, intensifying demand for predictive fall-detection modules. Vendors integrating accelerometer data from wearable pendants can issue pre-emptive alerts up to 30 seconds before an incident, protecting margins tied to value-based purchasing.

Accelerating Hospital Digitalization and Smart Infrastructure Spending

U.S. hospital IT budgets expanded 18.3% per year from 2019-2023, doubling connected-infrastructure outlays to USD 12.8 billion in 2024[1]Healthcare Financial Management Association, “Connected Infrastructure Spending Trends,” hfma.org. EHR vendors now require FHIR-compliant alarm routing, pulling forward refresh cycles by two to three years. A 400-bed site that unified nurse call with RTLS shaved average response times from 4.2 to 1.8 minutes, translating into 12,000 recaptured nurse-hours and USD 1.4 million in avoided overtime. Yet capital for full IP backbones still ranges from USD 500,000 to USD 2 million, pushing many rural hospitals toward wireless overlays or five-year subscription contracts priced at USD 8-15 per bed per month.

Regulatory Push for Patient Safety and Rapid Response Metrics

Joint Commission goal NPG.01.05.01 obliges accredited hospitals to audit response times biennially and remediate any breaches[2]Joint Commission, “National Patient Safety Goal NPG.01.05.01,” jointcommission.org. CMS adds financial teeth: facilities in the poorest safety quartile lose up to 1% of Medicare reimbursements. Australia’s 2025 EQuIP update similarly mandates real-time queue visibility, fueling adoption of RTLS-integrated dashboards. Compliance with IEC 60601-1-8 and ISO 13485 has shifted from procurement preference to hard requirement, trimming the vendor pool to companies with mature quality systems.

Convergence of Nurse Call with Unified Clinical Communication Platforms

Ascom’s Telligence 7 and comparable suites aggregate alarms from pumps, ventilators, and EHR workflows into a single mobile interface, cutting interruptions by 28% per shift. However, fewer than 40% of U.S. hospitals achieved seamless FHIR data exchange by 2025, and proprietary middleware can cost USD 50,000-150,000 per integration. ONC’s TEFCA framework should simplify sharing, but most nurse call vendors have not yet exposed compliant APIs, citing limited reimbursement incentives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for IP Conversions in Legacy Facilities | -1.6% | U.S. rural centers, EU public hospitals | Short term (≤ 2 years) |

| Interoperability and Data Integration Challenges Across Vendor Systems | -1.2% | Global multi-vendor hospital estates | Medium term (2-4 years) |

| Escalating Cybersecurity and Privacy Compliance Costs | -1.4% | Global, heightened in U.S. and EU | Short term (≤ 2 years) |

| Workforce Shortages Limiting Effective Utilization of Advanced Features | -1.0% | U.S., Japan, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for IP Conversions in Legacy Facilities

Retrofitting a 300-bed hospital costs USD 1.2-1.8 million and may disrupt wards for up to nine months[3]American Hospital Association, “Rural Hospital Financial Pressures,” aha.org. Margins at rural U.S. hospitals average below 2%, rendering full migrations unrealistic without grants or bond financing. European public facilities face budget levels still 8-12% below pre-pandemic baselines, extending the life of 1990s wired systems. Battery-powered wireless overlays cut headline costs to USD 300,000-500,000 for a 200-bed site but sacrifice deep EHR and RTLS integration. Subscription pricing eases cap-ex yet meets resistance from finance teams that prefer depreciable assets.

Interoperability and Data Integration Challenges Across Vendor Systems

Hospitals often pay USD 50,000-150,000 per custom API plus 15-20% annual maintenance, a burden that 62% of IT leaders cite as the prime barrier to unified communications. Only six of 22 major vendors published FHIR-compliant APIs by 2025, usually limited to alarm routing rather than workflow analytics required for Joint Commission audits. The vacuum extends to cyber-hardening: connected nurse call devices enlarge attack surfaces, and each breach now costs providers an average USD 4.35 million in remediation and fines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cloud Platforms Outpace IP Infrastructure

Cloud-enabled suites are advancing at a 11.54% CAGR and are on track to eclipse USD 1.6 billion in the nurse call systems market by 2031. IP-based systems still accounted for 34.65% of revenue in 2025 because they embed alerts into RTLS badges and EHR workflows, but adoption remains concentrated in academic medical centers. Basic audio-visual hardware persists in long-term care where Medicaid rates lag private pay. Intercom products serve behavioral units that restrict mobile devices.

Hospitals balancing cap-ex limits and integration demands are shifting toward hybrid models: on-premise servers manage real-time routing while analytics reside in the cloud. Ascom’s Telligence 7 represents this middle path, whereas TekTone’s Tek-CARE300III overlays wireless buttons on existing wires at one-third the cost of full IP migration. Subscription penetration, still below 20%, should accelerate as finance teams acclimate to operating expense treatment and vendors demonstrate lower churn.

By Modality: Wireless Dominance Reflects Retrofit Economics

Wireless platforms accounted for 62.65% revenue in 2025 and will climb at 11.67% CAGR. Retrofit speed and network-rewiring avoidance make them the default for aging facilities and ambulatory surgery centers. Yet battery logistics add USD 18,000 and 600 nursing hours per year for a typical 300-bed hospital, a cost that wired PoE installations avoid.

Cybersecurity has risen in the decision matrix: the 2024 Change Healthcare event illustrated how unsecured IoT nodes can escalate risk exposure. Vendors now tout AES-256 encryption and SOC 2 Type II attestations as table stakes, increasing development costs that smaller entrants struggle to absorb. Wireless also enables at-home monitoring reimbursed by Medicare Advantage at USD 50-65 per patient monthly, opening an adjacent revenue stream.

By Application: Fall Detection Surges on Liability Pressure

Fall-prevention modules will grow at a 12.12% CAGR through 2031, benefiting from CMS penalties that shave 1% off reimbursements for poor performers. Workflow optimization maintained 38.65% deployment share in 2025, but hospitals increasingly view analytics as a gating feature for staffing models rather than a premium add-on.

Each injurious fall adds USD 14,000 in costs and 6.9 days to the length of stay, making predictive algorithms financially compelling. Machine-learning blends of accelerometer, gyroscope, and pressure data have cut false positives below 8%, mitigating alarm fatigue. Privacy regulation, such as California’s 2024 CMIA update, now requires explicit consent for location tracking, adding paperwork but not derailing growth.

By End User: Home Healthcare Redefines Market Boundaries

Home-healthcare demand is projected to grow 12.65% per year, reshaping the nurse call systems market. Hospital and specialty clinics still generated 48.32% revenue in 2025, anchored by Joint Commission audits, yet reimbursement models now pay for remote monitoring under CPT 99453-58.

Long-term care facilities face new CMS staffing minimums of 3.48 hours per resident daily, accelerating purchases of workflow dashboards that document response times. Vendors linking in-hospital and at-home devices, such as Baxter’s Voalte, enable health systems to manage populations holistically, building cross-selling moats while satisfying HIPAA’s minimum necessary data rules.

Geography Analysis

North America delivered 41.43% of 2025 revenue, buoyed by Joint Commission mandates and CMS penalties. Ongoing digitization grants the region an early-adopter edge, yet replacement cycles slow absolute growth. Asia-Pacific will record a 10.43% CAGR, the fastest worldwide, as China’s 2025 health spend reached USD 1.2 trillion and Japan’s seniors now constitute 29% of its population. Nurse shortages exceeding 270,000 have pushed Japan toward acuity-based triage, benefiting advanced call suites.

India’s Ayushman Bharat insurance program stipulates the installation of functional nurse call systems in empaneled hospitals, creating a steady baseline demand. Australia’s 2025 EQuIP update, which mandates queue-depth visibility, has translated into RTLS-linked upgrades across public hospitals.

Europe’s expansion lags because public budgets remain 8-12% below pre-pandemic levels. The Middle East shows a two-speed pattern: Gulf states fund smart hospitals as part of diversification plans, whereas sub-Saharan Africa struggles with limited capital. South America is similarly split; Brazil mandated call coverage for SUS-accredited sites, but Argentina’s 200% inflation in 2024 froze most capital spending.

Mordor Intelligence provides coverage of the nurse call systems market across other key regional markets. Detailed country-level analysis extends to Brazil, Thailand, Vietnam, India, Mexico, Ukraine, South Korea, Taiwan, Kuwait, and Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

The top five suppliers—Ascom, Baxter International (Hillrom), Rauland-Borg, Siemens Healthineers, and Tunstall—held roughly 52% of 2025 revenue, indicating moderate concentration. Rauland-Borg’s Responder Enterprise and Siemens’ Invision lock in clients through proprietary middleware, charging USD 50,000-150,000 per third-party connector. Regional integrators such as IndigoCare in Australia and Fujian Huanyutong in China win share in secondary cities by offering lower service costs and faster on-site support.

Technology differentiation now centers on predictive analytics and cybersecurity. Ascom’s Telligence 7 routes acuity-scored alarms over LTE failover, reducing Wi-Fi congestion, while Austco embeds machine learning to forecast staffing needs across multi-site networks. The shift to “Nurse Call as a Service” subscription is forcing sales teams to master multi-year SaaS negotiations, bringing revenue recognition volatility not yet captured in public guidance.

Nurse Call Systems Industry Leaders

Honeywell International Inc.

Ascom

Baxter International

Rauland-Borg Corporation

Jeron Electronic Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: RF Technologies announces the launch of Enterprise 8.0 with wired nurse call integration built to adapt to emerging technologies, for long-term success in an ever-changing healthcare landscape.

- January 2025: Hippocratic AI secured USD 141 million Series B to scale a virtual nursing assistant that triages non-clinical requests.

- August 2024: Ascom launched Telligence 7 with advanced workflow links and an upgraded interface aimed at shortening nurse onboarding time.

Global Nurse Call Systems Market Report Scope

As per the scope of the report, nurse call systems are telecommunication systems that act as a means of communication, thus enabling the effective transfer of information between the nursing staff and patients within the healthcare facility.

The nurse call systems market is segmented by product, modality, end user, and geography. By product, the market is segmented into nurse call intercom systems, basic audio/visual nurse call systems, IP-based nurse call systems, and digital and mobile nurse call systems. By modality, the market is segmented into wireless and wired nurse call systems. By end user, the market is segmented into hospital and specialty clinics, long-term healthcare facilities, and nursing homes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Nurse Call Buttons |

| Intercom Nurse Call Systems |

| Basic Audio/Visual Systems |

| IP-Based Nurse Call Systems |

| Mobile & Cloud-Enabled Platforms |

| Wired Systems |

| Wireless Systems |

| Emergency Medical Alarms |

| Workflow & Staff Optimisation |

| Fall Detection & Prevention |

| Wanderer Control & Dementia Care |

| Hospitals & Specialty Clinics |

| Long-Term Care Facilities |

| Nursing Homes |

| Home-Healthcare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Nurse Call Buttons | |

| Intercom Nurse Call Systems | ||

| Basic Audio/Visual Systems | ||

| IP-Based Nurse Call Systems | ||

| Mobile & Cloud-Enabled Platforms | ||

| By Modality | Wired Systems | |

| Wireless Systems | ||

| By Application | Emergency Medical Alarms | |

| Workflow & Staff Optimisation | ||

| Fall Detection & Prevention | ||

| Wanderer Control & Dementia Care | ||

| By End User | Hospitals & Specialty Clinics | |

| Long-Term Care Facilities | ||

| Nursing Homes | ||

| Home-Healthcare Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will revenue grow for nurse call solutions?

Revenue is forecast to rise from USD 2.69 billion in 2026 to USD 4.31 billion by 2031, implying a 9.88% CAGR.

Which modality leads current adoption?

Wireless systems dominated with 62.65% share in 2025 thanks to low retrofit costs.

What is the biggest growth opportunity by application?

Fall-detection platforms are projected to expand at 12.12% annually through 2031 as hospitals target Medicare penalty avoidance.

Why are cloud-native platforms gaining traction?

Subscription models convert capital expense into operating expense and integrate easily with RTLS and EHR workflows.

Which region will grow fastest?

Asia-Pacific is expected to post the highest 10.43% CAGR, supported by rising health spend in China and rapid aging in Japan.

How are hospitals addressing cyber risk?

Providers now require SOC 2 Type II attestations and AES-256 encryption, and allocate an average USD 4.35 million per breach for remediation.

Page last updated on: