Market Size of North America Secondary Packaging Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

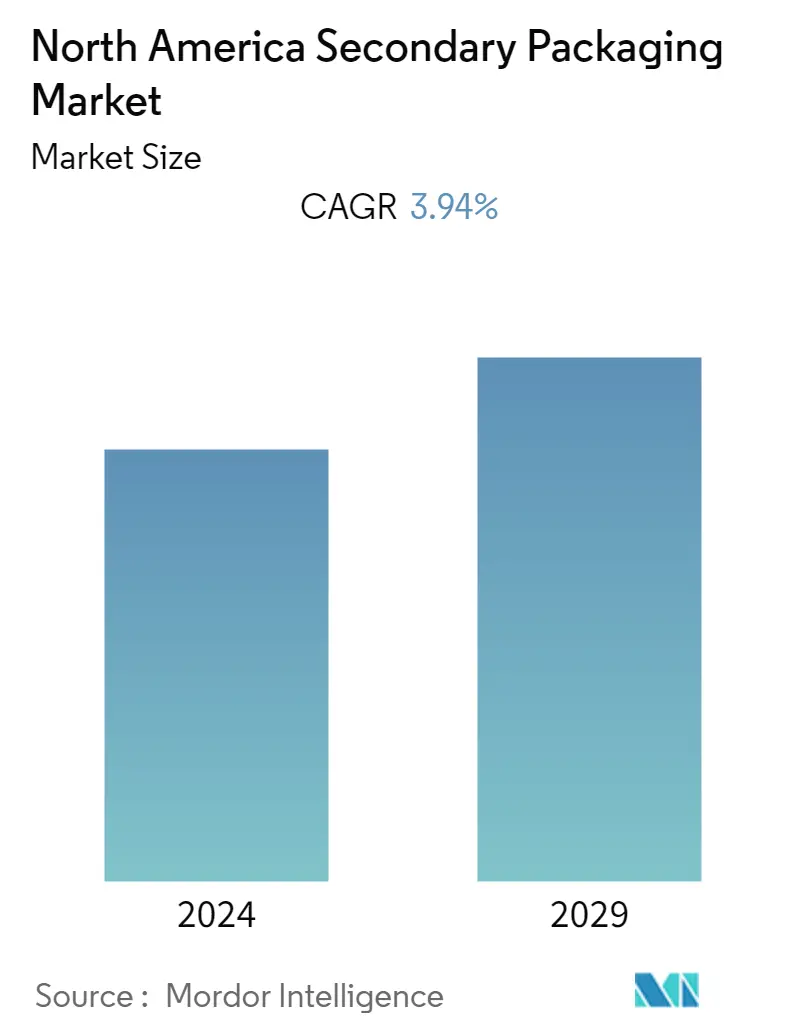

| CAGR | 3.94 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

North America Secondary Packaging Market Analysis

The North American secondary market was estimated at USD 60.40 billion in the previous year. The market is expected to reach USD 76.76 billion over the forecast period, witnessing a CAGR of 3.94%. The United States and Canada are massive consumer markets, and the population's considerable buying power makes it a lucrative market for all package suppliers. As a result, the North American secondary packaging market is anticipated to grow over the upcoming year due to the growing demand for food packaging, a string of successful e-commerce transactions, and the demand for safety in packaging transportation.

- The rising use of environment-friendly materials in packaging is driving the secondary packaging market in North America. Packaging that is recyclable, biodegradable, reusable, non-toxic, and has a minimal environmental impact is considered eco-friendly. The need for environment-friendly packaging materials is becoming increasingly apparent to end users, including the food and beverage industry and manufacturers of household care products. Packaging formats like folding cartons and corrugated boxes have no adverse effects on the environment because they are constructed of recyclable and biodegradable materials, such as paperboard.

- The demand for convenience foods is on the rise due to the busy lifestyle of people. As corrugated board packaging keeps moisture from the products and withstands long shipping times, companies are increasingly adopting it to offer customers better outcomes, especially secondary or tertiary packaging. Processed foods, such as bread, meat products, and other perishable items, need these packaging materials to be used once, thereby driving the demand. Since the corrugated board is easy to recycle and the pulp and paper industry is already skilled at converting it into new generations of containerboard, it is becoming increasingly common in packaging as sustainability concerns become more relevant across the value chain. Due to these benefits, corrugated protective forms have gained popularity over polymer-based substitutes, such as expanded polystyrene (EPS) foams.

- Additionally, increasing courier and messengers' revenue indicates the use of secondary packagings, such as corrugated boards and folding cartons packaging, in transiting the products from one place to another. According to the US Department of Commerce, in 2021, the US couriers and messengers generated almost USD 137.91 billion in operating revenue. UPS is the largest courier and delivery service provider in the United States, with around 40% of the courier market.

- Secondary packaging still raises environmental questions, but there are also other challenges to solve. In online purchasing, all have encountered the bother and disappointment of receiving a flawed, incomplete, or inaccurate product due to subpar or insufficient secondary packaging. However, since secondary packaging comes after primary packaging, any issues resulting from a stoppage impact the rest of the production line. Production and delivery plans are disrupted by downtime, which also increases product waste and brings labor expenses back into the expense column. Production planning should ideally include anticipating and reducing stoppages through advanced planning.

- Some primary drivers of the studied market, post the COVID-19 pandemic, are increased food packaging and an ever-increasing need for secondary packaging in burgeoning e-commerce shipments. Packaging for groceries, healthcare supplies, and e-commerce shipments has seen a substantial surge in demand on e-commerce platforms. Simultaneously, demand for luxury, industrial, and some B2B-transport packaging has decreased. Additionally, the healthcare industry anticipated further gaining traction with increased production of pharmaceutical products during the COVID-19 pandemic, which further attributed to the demands for secondary packaging.