Market Trends of North America Insurance Telematics Industry

Increase in Innovation in the Automotive Industry Across the Region to Witness Growth

- Innovation in the automotive sector is a key driver of the growth of insurance telematics, creating opportunities for insurers to leverage technology to offer more personalized and data-driven insurance products. The proliferation of connected car technologies, including embedded telematics systems, onboard sensors, and in-vehicle communication networks, provide insurers with real-time data on vehicle performance, driver behavior, and environmental conditions. These data streams enable more accurate insurance policy risk assessments and pricing models.

- Moreover, developing autonomous and semi-autonomous vehicle technologies is reshaping the automotive industry and presenting new opportunities for insurance telematics. Insurers can leverage telematics data to assess the impact of ADAS and autonomous features on driving behavior, safety, and risk exposure. With the rise of connected and autonomous vehicles, telematics is even more important as these new systems need to monitor effectively and report data related to driving behavior. Telematics technology has become a crucial element in modern vehicles, enabling insurers to precisely determine premiums by assessing a driver's real-time behavior rather than relying on mere speculation.

- The United States is anticipated to be the significant market for connected cars due to the significant presence of automotive OEMs, higher technological awareness among the general car buyers, preference for infotainment and telematics in vehicles, widespread adoption of 4G/5G, and increasing sales of electric, connected and autonomous cars in the country.

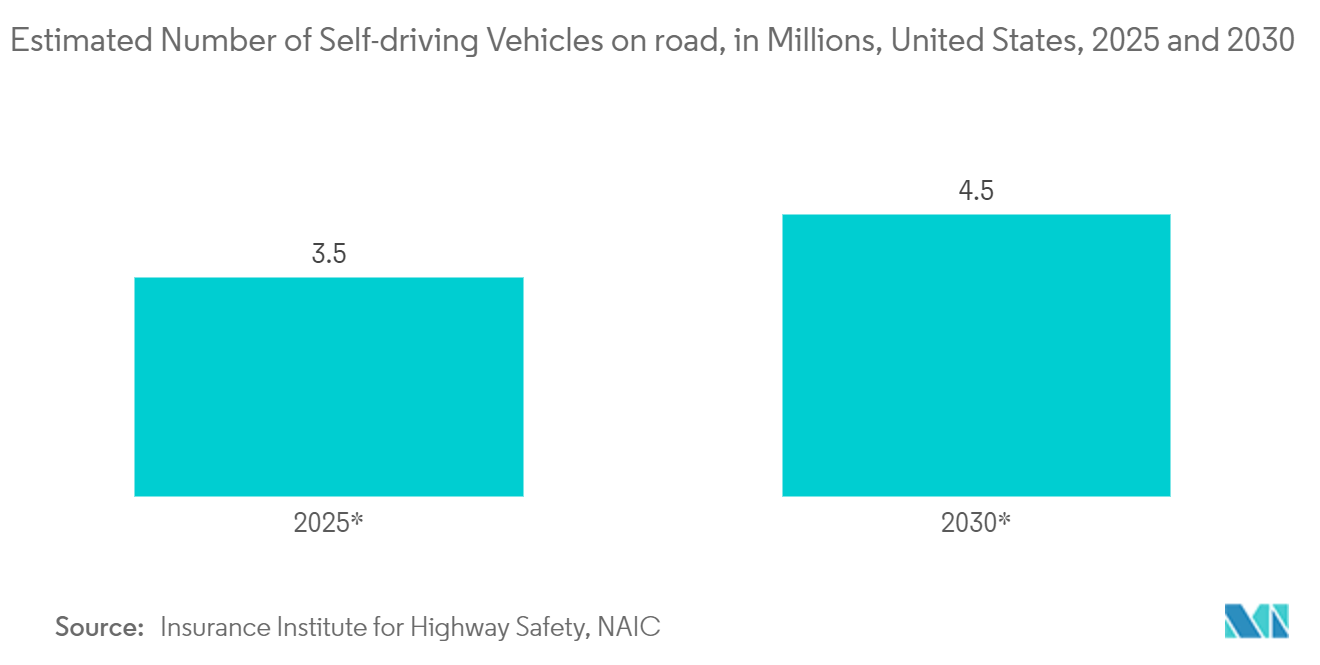

- According to the Insurance Institute for Highway Safety, it is anticipated that there will be around 3.5 million self-driving vehicles on US roads by 2025 and 4.5 million by 2030. However, the institute cautioned that these vehicles would not be fully autonomous but would operate autonomously under certain conditions. Recognizing the symbiotic relationship between insurers and autonomous vehicle manufacturers, insurers are actively engaging in collaborations. By working closely with manufacturers, insurers gain insights into the technology, safety features, and potential risks associated with autonomous vehicles.

- This collaborative approach helps insurers craft policies that align with the evolving landscape of self-driving cars. For instance, Connected Analytic Services, LLC (CAS), an affiliate of Toyota Insurance Management Solutions USA, expanded its partnership with Toyota Motor North America to add new product offerings to enhance the ownership experience for owners of enrolled Toyota vehicles. For Toyota customers who wish to use their driving data to obtain potential insurance savings, CAS is Toyota's exclusive data aggregation service, providing telematics and vehicle build data to insurance companies. Major players in the market are expanding their presence in digital mobility to cater to the increased demand for connected cars.

Understand The Key Trends Shaping This Market

Download Sample

United States to Hold Major Market Share

- Decreasing the cost of development and technology, altering consumer behavior, and stringent government regulations drive the growth of the market studied in the United States. In the United States, consumers prefer usage-based insurance (UBI) snapshot programs. In other regions, motor insurance telematics policies are preferred.

- Introducing insurance telematics has several advantages for insurers and consumers, which are expected to fuel market growth. For consumers, it will promote safe driving, resulting in the mitigation of accident severity and frequency. Over the forecast period, the insurers' claim-handling expenses will likely decrease by at least half, contributing to the market's growth.

- Various US consumers are switching insurers because their premiums have increased despite driving less. Measures imposed during the lockdown during the pandemic led consumers to drive less and ultimately demanded policies that analyzed auto usage to provide personalized policies based on mileage.

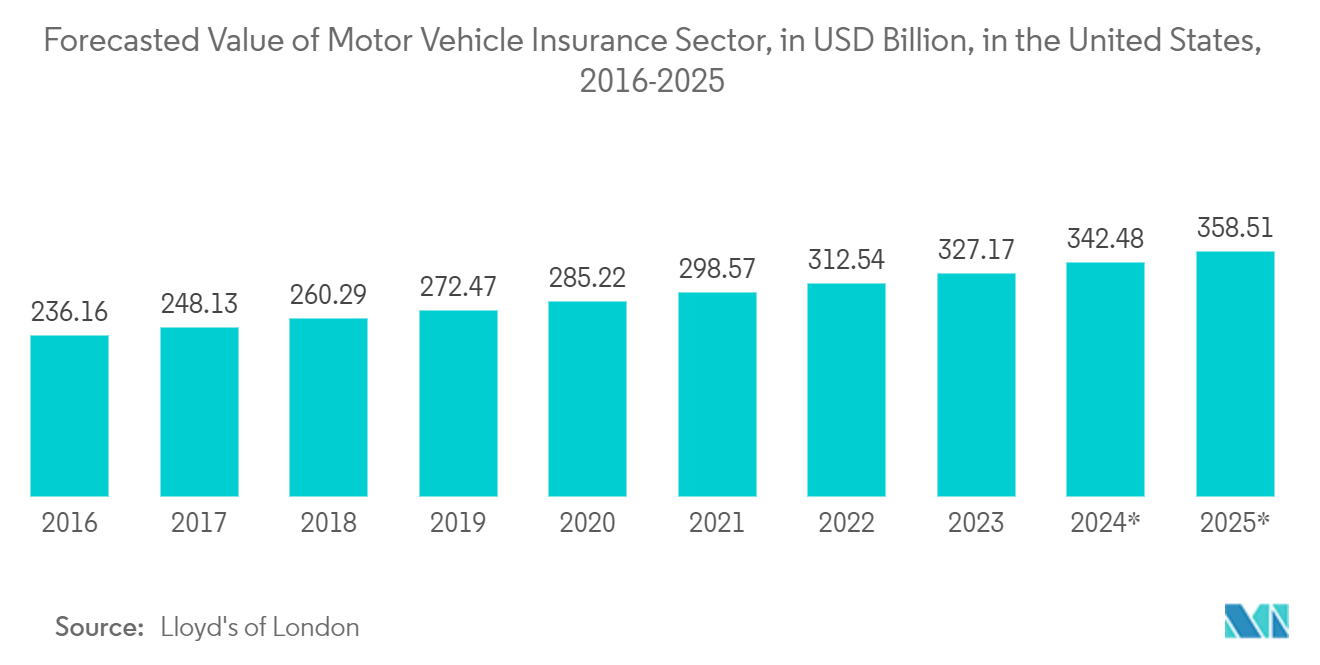

- According to Lloyd's of London, the value of the motor vehicle insurance sector in the United States is expected to amount to approximately USD 224.7 billion in 2015. It was projected to grow to about USD 358.51 billion by 2025.

- According to BEA, in May 2023, 1.07 million vehicles were sold in the United States, including light trucks, which remained the most significant United States auto market segment, contributing to sales of 1.06 million units.

- The United States is anticipated to be the significant market for connected cars in the country due to the substantial presence of automotive OEMs, high levels of technology awareness amongst the general car buyers, preference for infotainment and telematics in vehicles, widespread adoption of 4G/5G and increasing sales of electric, connected and autonomous cars in the country.

Get Analysis on Important Geographic Markets

Download Sample