Market Trends of Niobium Industry

Construction Sector to Dominate the Market

- The construction industry is the largest consumer of niobium across the world. In the construction industry, high-strength niobium micro-alloyed plate products are used to construct bridges, viaducts, high-rise buildings, etc. Heavy machinery, pressure vessels, etc., represent additional applications of micro-alloyed plates. Structural sections are widely used in civil construction, transmission towers, etc., where niobium competes with vanadium.

- Similarly, steel reinforcing bar is used in large concrete structures to increase their resistance to tensile loads. Larger diameter, high-strength grades are produced via the addition of niobium and vanadium, although some modern steel mills also use water cooling, which negates the need for microalloying.

- Furthermore, niobium has also found application in high-strength and wear-resistant rails for railway tracks operating under high axle loads.The building and construction industry is currently driving the demand for High Strength Low Alloys (HSLA) steel, which provides cost savings through weight reduction in buildings and prevents infrastructure failures.

- The construction sector has witnessed major investments in recent years. According to Oxford Economics, the global construction industry is expected to grow by USD 4.5 trillion, or 42%, between 2020 and 2030 to reach USD 15.2 trillion. Also, China, India, the United States, and Indonesia are expected to account for 58.3% of global growth in construction between 2020 and 2030.

- Growth in population, migration from hometowns to service sector clusters, and the growing trend of nuclear families are some of the factors which have been driving residential construction across the world. Factors such as rapid urban migration in major economies, increased government spending in the real estate market for residential construction, along with the growing demand for high-class residential homes are likely to benefit the growth of the market studied.

- Moreover, the construction sector is an important pillar for the growth of the Indian economy. The Indian government has been actively boosting housing construction, aiming to provide houses to about 1.3 billion people.

- The USD 30 million Arkade Aspire Residential Complex project entails the construction of a 35,366 sq. m. residential complex with two 18-story residential towers in Mumbai, India. Construction began in Q2 2022 and is expected to be completed in Q1 2025. In North America, the United States has a major share in the construction industry. Besides the United States, Canada and Mexico contribute significantly to the investments in the construction sector.

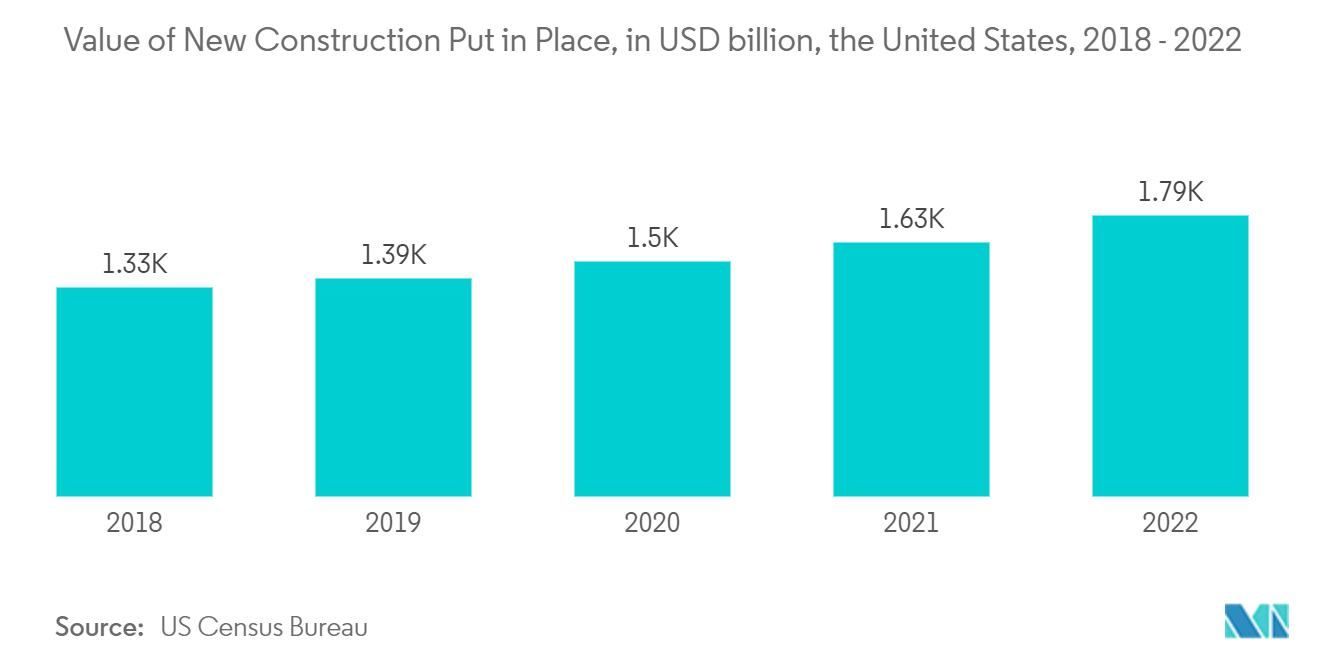

- According to the U.S. Census Bureau, the value of new construction output in the United States amounted to USD 1,792.9 billion in December 2022. The non-residential sector accounted for USD 997.14 billion in March 2023, registering a growth of 18.8% compared to the same period the previous year.

- Furthermore, in Canada, various government projects, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, are set to support the sector's expansion. In August 2022, the Canadian government announced a significant investment of more than USD 2 billion to fund three important initiatives that may collectively help develop approximately 17,000 houses for families across the nation, including thousands of affordable housing units.

- Additionally, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. Business confidence picked up in early 2022, despite price pressures at most EU construction firms, and is expected to reach pre-COVID-19 levels. Moreover, as the crisis due to COVID-19 abates and builders become less reluctant to invest in new corporate buildings and renovate existing properties. Non-residential construction is expected to pick up the pace, thus supporting overall growth in the construction market. The major construction projects in 2022 accounted for non-residential construction (offices, hospitals, hotels, schools, and industrial buildings), accounting for 31.3% of total activity.

- Therefore, such robust growth in construction across the world is likely to boost the demand for the consumption of niobium during the forecast period.

Understand The Key Trends Shaping This Market

Download Sample

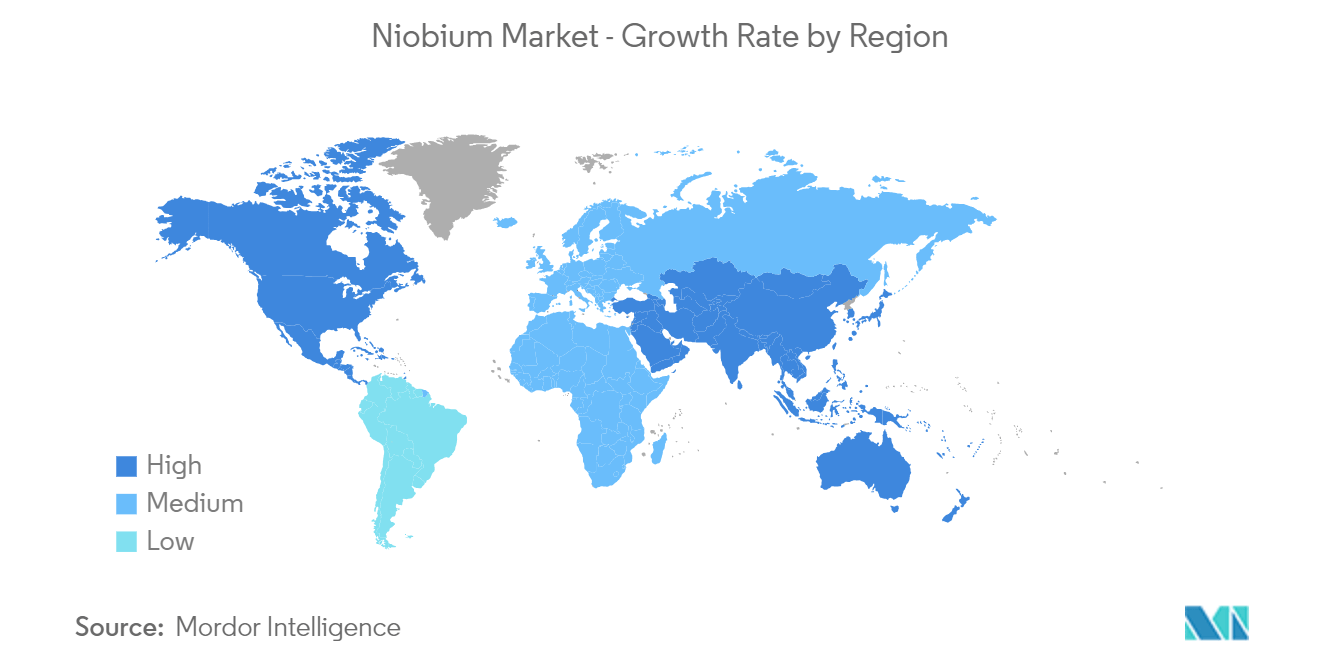

Asia-Pacific to Dominate the Market

- Asia-Pacific dominated the global market. With accelerating usage in structural steel and growing usage in the automobile and aerospace industry in countries such as China, India, and Japan, the consumption of niobium is increasing in the region.

- The consumption of niobium is very high in steel manufacturing in the form of ferroniobium, and the construction industry is thriving in several emerging economies, such as China and India, among others. For instance, according to the World Steel Association, China produced an estimated 92.6 million tonnes of steel in April 2023 and a total of 354.4 million tonnes from January to April 2023, a 4.1% increase compared to the same period in 2022.

- Moreover, according to the China Iron and Steel Association, the economy's benchmark China's steel industry was buoyed by increased demand after the country's declining response to the pandemic and efforts to support the economy. In addition, the steel sector is on an upward trend in 2023, supported by a stable real estate market and a recovery in other steel-consuming industries such as automobiles, ships, and construction. This, in turn, is expected to impact the market positively.

- China is one of the largest producers of passenger cars, due to the improving logistics and supply chains, increased business activity, and the country's raft of pro-consumption measures, among other factors contributing to the passenger car market products in the country. Therefore, this has increased demand for niobium market from the country's passenger car segment. For instance, according to OICA, in 2022, the passenger car production in China amounted to 2,38,36,083 units, which showed an increase of 11% compared to 2021.

- Further, the automobile industry in the country is witnessing switching trends as the consumer inclination toward battery-operated vehicles is on the higher side. Moreover, the government of China estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the electric vehicle sales trend in the country, which went record-breaking high in 2022.

- The infrastructure sector is an important pillar of the Indian economy. The government is taking various initiatives to ensure the timely creation of excellent infrastructure in the country. The government is focusing on railways, road development, housing, urban development, and airport development.

- The residential sector in India is on an increasing trend, with government support and initiatives further boosting the demand. According to the India Brand Equity Foundation (IBEF), the Ministry of Housing and Urban Development (MoHUA) allocated USD 9.85 billion in the 2022-2023 budget to construct houses and create funds to complete the halted projects.

- Furthermore, Indonesia expects to begin construction in the second quarter on apartments worth USD 2.7 billion for thousands of civil servants due to move to its new capital city on Borneo island. Moreover, tndonesian government intends to finance it for 80% through foreign investments. Therefore, this is expected to create an upside demand for the consumption for niobium market from the contry's residential construction.

- Japan is the third-biggest producer of crude steel worldwide, which is a major end-user for the Niobium Market. The crude steel output in Japan fell by around 7.4% in 2022 from the previous year owing to a slow recovery in automobile manufacturing and weaker export demand amid a slowdown in the global economy. As per the data of the Japan Iron and Steel Federation, the crude steel production in the country reached 89.2 million tons in 2022, as compared to 96.3 million tons in 2021.

- Considering the aforementioned factors, the Asia-Pacific niobium market is anticipated to rise steadily over the forecast period.

Get Analysis on Important Geographic Markets

Download Sample