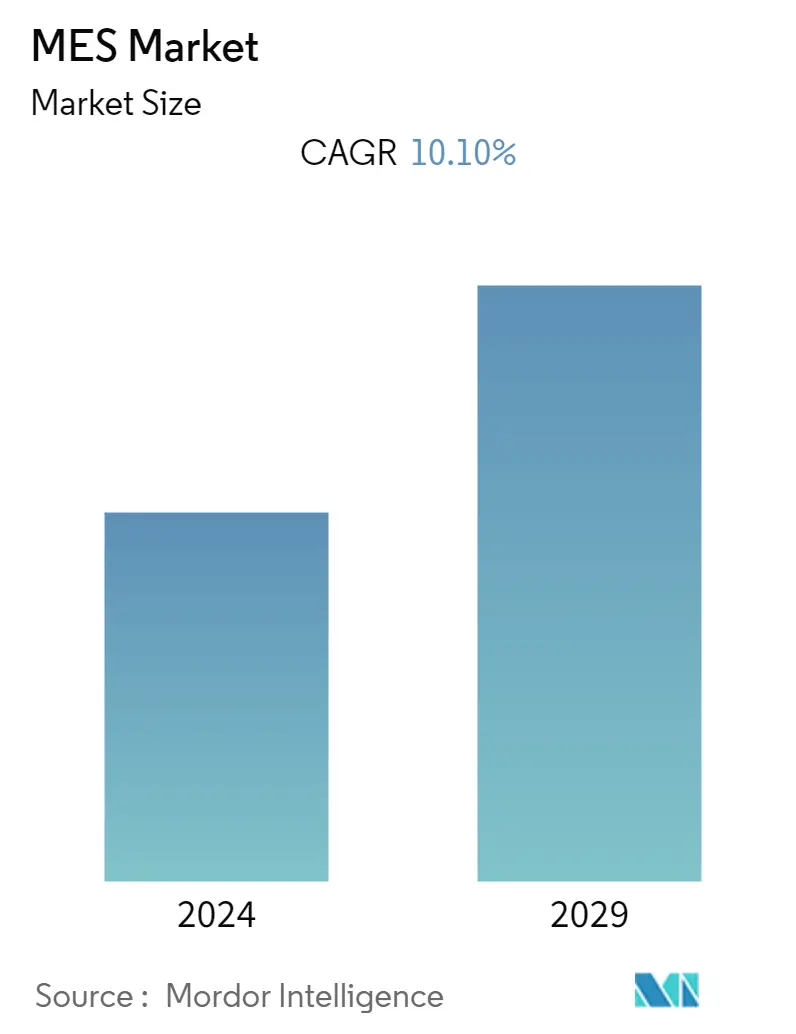

Market Size of MES Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 10.10 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Manufacturing Execution System Market Analysis

The MES Market size is expected to grow from USD 14.87 billion in 2023 to USD 24.06 billion by 2028, at a CAGR of 10.10% during the forecast period (2023-2028).

With the growing adoption of Industry 4.0 and the Industrial Internet of Things (IIoT) in plants, the agility and interoperability of the Manufacturing Execution System (MES) have become even more strategic for managing additional complexity and future-proof businesses.

- The increasing shift towards production orders, process steps, and instructions and documentation, with information being pulled directly from ERP and other enterprise business systems, is driving the adoption of manufacturing execution systems. Furthermore, in recent years, driven by labour shortages and enabled by more automated machining systems, MESs have been picked up by multiple end-use manufacturers to compensate them, which has benefitted market growth and is expected to increase over the forecast period.

- Increasing development by major players in order to raise awareness and knowledge regarding MES solutions is expected to contribute to market growth. For instance, in July 2022, Insequence announced a novel user certification training program for SPD Pro and its Manufacturing Management System. This new curriculum from Insequence University Software gives power-user level information to Insequence clients to help develop an in-house understanding of Insequence products. This might lead to increased efficiency, competence, and cost savings.

- The market growth is being constrained by reasons including SMEs' lack of understanding of the advantages of MES. Additionally, it is predicted that slow development would occur throughout the projection period due to high operating and investment expenses associated with deploying and updating industrial execution technologies for small-scale production.

- Multiple end industry activities, including those in the power generation, oil and gas, and automotive sectors, saw significant transformation during the post-pandemic period. The substantial labor and distribution network issues that led to the development of manufacturing operational system solutions have begun to be resolved in the manufacturing sectors. The growth of the process and discrete sectors is likely to increase demand for MES technologies. The need for manufacturing execution solutions will expand during the projected period due to several COVID-19 operations and recommendations that have been established for easier operations.