Market Size of leo satellite Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 176.98 Billion |

|

|

Market Size (2029) | USD 284.39 Billion |

|

|

Largest Share by Propulsion Tech | Liquid Fuel |

|

|

CAGR (2024 - 2029) | 9.95 % |

|

|

Largest Share by Region | North America |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

LEO Satellite Market Analysis

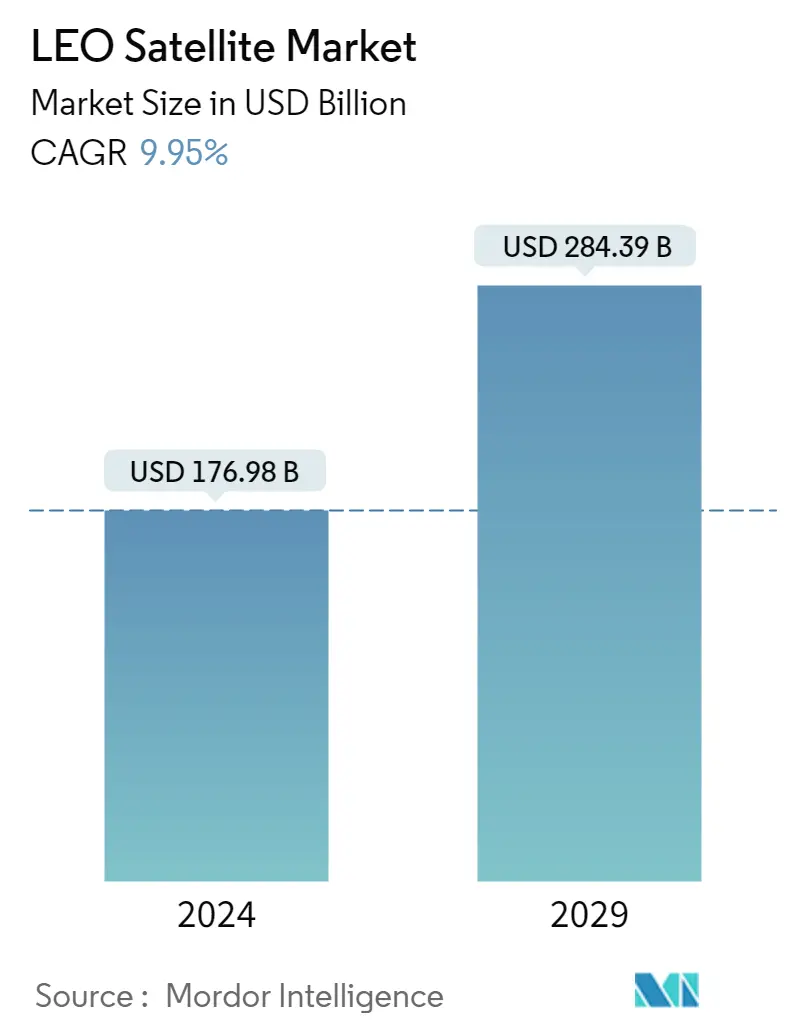

The LEO Satellite Market size is estimated at USD 176.98 billion in 2024, and is expected to reach USD 284.39 billion by 2029, growing at a CAGR of 9.95% during the forecast period (2024-2029).

176.98 Billion

Market Size in 2024 (USD)

284.39 Billion

Market Size in 2029 (USD)

31.95 %

CAGR (2017-2023)

9.95 %

CAGR (2024-2029)

Largest Market by Satellite Mass

75.24 %

value share, 100-500kg, 2022

Minisatellites with expanded capacity for enterprise data (retail and banking), oil, gas, and mining, and governments in developed countries pose high demand. The demand for minisatellites with a LEO is increasing due to their expanded capacity.

Largest Market by Propulsion Tech

73.93 %

value share, Liquid Fuel, 2022

Due to its high efficiency, controllability, reliability, and long lifespan, liquid-fuel-based propulsion technology is an ideal choice for space missions. It can be used in various orbit classes for satellites, including geostationary orbit, low Earth orbit, polar orbit, and sun-synchronous orbit.

Largest Market by End User

77.31 %

value share, Commercial, 2022

The commercial segment is expected to occupy a significant share because of the increasing use of satellites for various telecommunication services.

Largest Market by Region

92.86 %

value share, North America, 2022

The increasing investment in satellite equipment to enhance the defense and surveillance capabilities, critical infrastructure, and law enforcement agencies using satellite systems are expected to drive the LEO satellite market in North America.

Leading Market Player

64.33 %

market share, Space Exploration Technologies Corp., 2022

SpaceX is the leading player in the global LEO satellite market. The company maintains its market share globally through its Starlink project in over 53 countries, and it produces 120 satellites per month.

Liquid fuel propulsion system occupies majority of the market share

- Low Earth orbit (LEO) satellites have become integral to various industries, including telecommunications, Earth observation, navigation, and remote sensing. The propulsion system plays a crucial role in determining the performance, efficiency, and operational capabilities of these satellites.

- Liquid propulsion systems have been widely used in the LEO satellite market, offering high thrust and specific impulse capabilities. These systems typically use liquid fuels, such as hydrazine, combined with oxidizers like nitrogen tetroxide. Liquid propulsion enables precise orbital maneuvers, geostationary transfer orbit (GTO) insertion, and mission flexibility. LEO satellite missions requiring complex orbital adjustments, payload delivery to specific orbits, and satellite decommissioning rely on liquid propulsion systems.

- Electric propulsion has gained significant traction in the LEO satellite market due to its fuel efficiency and extended mission lifetimes. Electric propulsion systems, including ions and Hall-effect thrusters, utilize electric fields to accelerate ions and generate thrust. Electric propulsion enables the deployment of large-scale LEO satellite constellations, as demonstrated by companies like SpaceX's Starlink and OneWeb. These systems are particularly suitable for applications that require precise station-keeping maneuvers and orbital adjustments over extended periods.

- Gas-based propulsion systems, including cold gas and warm gas thrusters, are extensively used in the LEO satellite market. These systems utilize compressed gases, such as nitrogen or xenon, to generate thrust. LEO satellite missions that require rapid orbital changes or frequent repositioning often rely on gas-based propulsion systems due to their higher thrust capabilities.

North America is driving the market demand with a market share of 85.4% in 2029

- The global LEO satellite market is expected to grow significantly in the coming years, driven by increasing demand for high-speed internet, communication services, and data transfer across different industries. The market can be analyzed with respect to North America, Europe, and Asia-Pacific as to market share and revenue generation.

- During 2017-2022, more than 4100 satellites were manufactured and launched by various operators in this segment into LEO.

- North America is expected to dominate the global LEO satellite market due to the presence of several leading market players, such as The Boeing Company, Lockheed Martin, and Northrop Grumman. The US government has also been investing heavily in the development of advanced satellite technology, which is expected to drive the growth of the market in North America. During 2017-2022*, the region accounted for 72% of the total satellites manufactured and launched into LEO.

- The LEO satellite market is expected to grow significantly due to the increasing demand for high-speed internet and communication services in Europe. The European Space Agency (ESA) has been investing heavily in the development of advanced satellite technology, which is expected to drive the growth of the market. During 2017-2022, the region accounted for 12% of the total satellites manufactured and launched into LEO.

- Asia-Pacific is expected to witness significant growth in the LEO satellite market due to the increasing demand for satellite-based communication services in countries such as China, India, and Japan. During 2017-2022, Asia-Pacific accounted for 9% of the total satellites manufactured and launched into LEO.